Global Rigless Intervention Systems Market

Market Size in USD Billion

USD

14.19 Billion

USD

20.03 Billion

2025

2033

USD

14.19 Billion

USD

20.03 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.19 Billion | |

| USD 20.03 Billion | |

| % | |

|

Rigless Intervention Systems Market Size

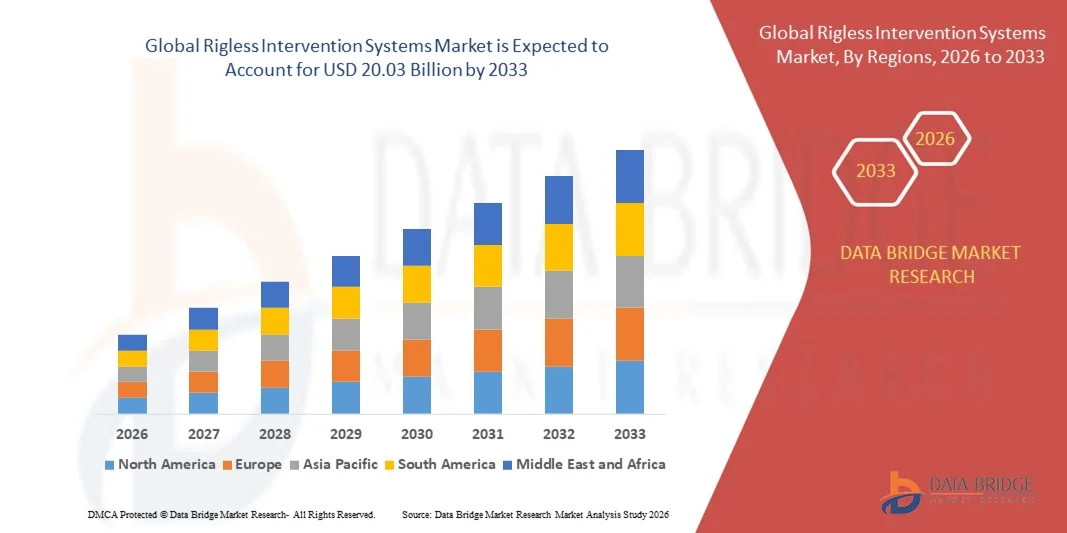

- The global rigless intervention systems market size was valued at USD 14.19 billion in 2025 and is expected to reach USD 20.03 billion by 2033, at a CAGR of 4.40% during the forecast period

- The market growth is largely fuelled by the increasing need for cost-efficient and safer offshore well intervention techniques, reducing downtime and operational risks

- Growing adoption of advanced technologies such as coiled tubing, wireline, and robotic intervention systems is further driving market expansion

Rigless Intervention Systems Market Analysis

- The market is witnessing technological innovations that improve efficiency, reduce environmental impact, and enhance operational safety

- Increasing focus on minimizing production losses and reducing reliance on costly drilling rigs is shaping market strategies and investments

- North America dominated the rigless intervention systems market with the largest revenue share in 2025, driven by the increasing adoption of cost-effective offshore maintenance solutions and growing focus on safe and efficient well operations

- Asia-Pacific region is expected to witness the highest growth rate in the global rigless intervention systems market, driven by growing offshore oil & gas activities, expanding deepwater exploration, and government initiatives supporting energy infrastructure development

- The shelf-stable segment held the largest market revenue share in 2025, driven by its ease of storage, long shelf life, and operational convenience for offshore and onshore intervention projects. Shelf-stable systems reduce dependency on immediate logistics support and allow operators to plan interventions efficiently

Report Scope and Rigless Intervention Systems Market Segmentation

|

Attributes |

Rigless Intervention Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Rigless Intervention Systems Market Trends

Rise of Non-Destructive Subsea Well Intervention

- The growing adoption of rigless intervention systems is transforming offshore well maintenance by enabling non-destructive, cost-effective subsea interventions. These systems allow operators to conduct inspections, maintenance, and minor repairs without the need for full rig mobilization, reducing downtime and operational costs significantly. In addition, the ability to perform multiple interventions in a single deployment is enhancing operational efficiency and minimizing environmental risks

- Increasing demand for remote and deepwater operations is accelerating the deployment of modular and remotely operated intervention tools. These systems are particularly beneficial in harsh offshore environments, reducing reliance on expensive rig-based interventions and improving operational safety. Continuous advancements in automation and remote control technologies are further expanding the applicability of rigless interventions in complex subsea fields

- The ease of integration with existing subsea infrastructure and the ability to perform real-time monitoring make modern rigless intervention systems attractive for routine well intervention. Operators benefit from faster turnaround times and minimized production losses while ensuring operational efficiency. Furthermore, predictive maintenance capabilities provided by sensor integration are allowing operators to plan interventions proactively, reducing unplanned downtime

- For instance, in 2023, several North Sea operators reported enhanced uptime and reduced maintenance costs after adopting coiled tubing and wireline rigless intervention technologies for subsea wells. These systems facilitated quick diagnostics and minor repairs without full rig deployment, resulting in significant savings in operational expenditure. The adoption also allowed companies to comply with stricter safety and environmental regulations efficiently

- While rigless systems are improving operational efficiency and reducing costs, their effectiveness depends on technological sophistication, operator training, and infrastructure compatibility. Manufacturers and service providers must focus on developing adaptable, reliable solutions to fully capitalize on market growth. In addition, advancements in subsea robotics and real-time data analytics are expected to further enhance intervention precision and reliability

Rigless Intervention Systems Market Dynamics

Driver

Increasing Need for Cost-Effective and Safe Offshore Well Operations

- The rising focus on reducing operational expenditure and minimizing offshore risks is driving the demand for rigless intervention solutions. These systems reduce the need for costly rig mobilization while maintaining well integrity and safety standards. Operators are increasingly leveraging such interventions to optimize field economics and extend well life in mature fields

- Operators are increasingly leveraging rigless technologies to perform inspections, maintenance, and interventions in deepwater and ultra-deepwater fields. This trend is supported by advancements in coiled tubing, wireline, and hydraulic intervention tools, enabling efficient and safe subsea operations. In addition, integration with digital twins and remote monitoring platforms is allowing for real-time decision-making and enhanced operational control

- Regulatory frameworks emphasizing safety and environmental protection are promoting non-rig-based interventions. Offshore operators are incentivized to adopt solutions that minimize environmental risks and ensure compliance with stringent safety standards. The shift toward zero-discharge and reduced subsea impact operations is further boosting market demand for rigless systems

- For instance, in 2022, Gulf of Mexico operators implemented multiple rigless subsea intervention projects using coiled tubing and hydraulic workover units, resulting in reduced operational costs and enhanced well uptime. These interventions also minimized the environmental footprint of offshore operations and reduced dependence on conventional rigs

- While the shift toward cost-effective interventions is driving market adoption, continuous innovation and infrastructure upgrades are required to ensure reliability and operational efficiency. Collaboration between operators, equipment manufacturers, and service providers is essential to expand deployment capabilities and address evolving subsea challenges

Restraint/Challenge

High Initial Investment and Technical Complexity

- The high capital expenditure associated with advanced rigless intervention equipment, including coiled tubing units, wireline systems, and remotely operated vehicles (ROVs), limits adoption among smaller operators. These systems require substantial investment in equipment and skilled personnel. In addition, ongoing maintenance costs and technology upgrades add to the overall financial burden, discouraging new entrants

- In remote offshore locations, limited access to trained operators and logistical challenges can delay deployment and reduce operational efficiency. Technical expertise is critical for ensuring successful intervention and avoiding operational mishaps. The need for specialized training programs and certification standards further adds to operational constraints

- Supply chain constraints for specialized components and ROV systems can restrict availability and lead to operational delays. Maintenance and repair of complex subsea equipment require skilled technicians and specialized infrastructure. Moreover, delays in the supply of critical parts can impact multiple concurrent projects, affecting production schedules and revenue

- For instance, in 2023, several operators in Southeast Asia experienced delays in subsea intervention projects due to limited availability of ROV systems and coiled tubing units, affecting planned production schedules. These delays also resulted in higher operational costs and postponed efficiency gains, highlighting the importance of robust supply chains

- While technological advances improve operational capabilities, addressing cost, accessibility, and technical challenges remains crucial for the widespread adoption and long-term growth of the rigless intervention systems market. Investment in modular, scalable, and user-friendly technologies, along with regional training and support infrastructure, is expected to mitigate these challenges over time

Rigless Intervention Systems Market Scope

The rigless intervention systems market is segmented on the basis of type, location, application, end use, and technique.

- By Type

On the basis of type, the market is segmented into shelf-stable creamers and refrigerated liquid creamers. The shelf-stable segment held the largest market revenue share in 2025, driven by its ease of storage, long shelf life, and operational convenience for offshore and onshore intervention projects. Shelf-stable systems reduce dependency on immediate logistics support and allow operators to plan interventions efficiently.

The refrigerated liquid segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its high performance in sensitive applications requiring precise handling and controlled environments. Refrigerated systems are particularly popular for critical subsea operations, ensuring equipment reliability and enhanced intervention outcomes.

- By Location

On the basis of location, the market is segmented into offshore and onshore. The offshore segment held the largest market revenue share in 2025, driven by the increasing number of deepwater and ultra-deepwater projects requiring advanced rigless intervention systems. Offshore operations demand reliable, remotely operated solutions, which are critical for minimizing downtime and reducing operational costs.

The onshore segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising exploration and production activities in onshore fields and the growing adoption of modular, cost-efficient intervention technologies. Onshore applications benefit from easier accessibility and quicker deployment, enhancing operational efficiency.

- By Application

On the basis of application, the market is segmented into abandonment services, pre-installation services, and wireline services. The wireline services segment held the largest market revenue share in 2025, fueled by its widespread use for subsea well inspections, logging, and intervention operations. Wireline interventions offer precise monitoring and maintenance capabilities, reducing the risk of costly downtime.

The abandonment services segment is expected to witness the fastest growth rate from 2026 to 2033, driven by stringent regulatory requirements for safe decommissioning of offshore wells and increasing focus on environmentally compliant interventions. Abandonment services require specialized rigless systems for efficient and secure execution.

- By End Use

On the basis of end use, the market is segmented into supermarkets/hypermarkets, convenience stores, and other. The supermarkets/hypermarkets segment held the largest market revenue share in 2025, driven by large-scale procurement and high-volume subsea operations. These end users prefer standardized systems for operational consistency and reduced logistical complexity.

The convenience stores segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by smaller operators adopting flexible, modular rigless systems for specific subsea interventions. These systems allow rapid deployment and adaptability, meeting the growing demand for cost-efficient solutions.

- By Technique

On the basis of technique, the market is segmented into coiled tubing, hydraulic workover, and wireless. The coiled tubing segment held the largest market revenue share in 2025, driven by its versatility in performing complex interventions such as wellbore cleanouts, scale removal, and plug setting. Coiled tubing operations enhance precision and reduce intervention time, making them ideal for offshore applications.

The wireless segment is expected to witness the fastest growth rate from 2026 to 2033, driven by advancements in remote-controlled intervention technologies and increasing adoption of automated subsea solutions. Wireless systems provide enhanced operational flexibility and real-time monitoring capabilities, reducing reliance on rig-based deployments.

Rigless Intervention Systems Market Regional Analysis

- North America dominated the rigless intervention systems market with the largest revenue share in 2025, driven by the increasing adoption of cost-effective offshore maintenance solutions and growing focus on safe and efficient well operations

- Operators in the region highly value the reduced downtime, operational efficiency, and enhanced safety offered by rigless intervention systems for offshore and deepwater fields

- This widespread adoption is further supported by advanced subsea infrastructure, skilled workforce availability, and regulatory incentives, establishing rigless intervention systems as a preferred solution for both offshore and onshore operations

U.S. Rigless Intervention Systems Market Insight

The U.S. rigless intervention systems market captured the largest revenue share in 2025 within North America, fueled by the rising demand for non-rig-based well maintenance and inspection solutions. Operators are increasingly leveraging coiled tubing, wireline, and hydraulic workover systems to reduce operational costs while ensuring well integrity. The growing trend of deepwater and ultra-deepwater exploration, combined with stringent safety regulations, further drives market growth. In addition, integration with digital monitoring and real-time intervention technologies is significantly contributing to the market’s expansion.

Europe Rigless Intervention Systems Market Insight

The Europe rigless intervention systems market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent safety and environmental regulations in offshore operations. The increase in deepwater exploration projects, along with the adoption of advanced intervention technologies, is fostering market growth. European operators are also drawn to solutions that reduce rig mobilization costs and enhance operational efficiency. The region is experiencing significant growth across North Sea offshore projects, with rigless systems being incorporated into both new developments and maintenance programs.

U.K. Rigless Intervention Systems Market Insight

The U.K. rigless intervention systems market is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing focus on reducing offshore operational expenditure and ensuring well safety. In addition, the growing need for non-invasive subsea maintenance and the adoption of remote intervention technologies are encouraging operators to deploy rigless systems. The U.K.’s mature offshore sector, combined with government incentives for safe and efficient operations, is expected to continue to stimulate market growth.

Germany Rigless Intervention Systems Market Insight

The Germany rigless intervention systems market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing awareness of cost-effective and safe subsea intervention solutions. Germany’s advanced engineering capabilities and focus on innovation promote the adoption of rigless technologies in offshore and onshore wells. Integration with monitoring and digital management systems is becoming increasingly prevalent, with operators preferring solutions that ensure operational efficiency and environmental compliance.

Asia-Pacific Rigless Intervention Systems Market Insight

The Asia-Pacific rigless intervention systems market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising offshore exploration, technological advancements, and increasing investments in subsea infrastructure in countries such as China, Japan, and India. Government initiatives supporting offshore safety and digitalization are driving the adoption of rigless intervention solutions. Furthermore, as APAC emerges as a manufacturing hub for coiled tubing, hydraulic, and wireline systems, the affordability and accessibility of these solutions are expanding to a broader operator base.

Japan Rigless Intervention Systems Market Insight

The Japan rigless intervention systems market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s high-tech offshore sector, rapid adoption of digital monitoring technologies, and focus on safe well interventions. Operators are increasingly deploying coiled tubing and hydraulic workover systems for efficient and non-destructive subsea maintenance. The integration of rigless systems with real-time monitoring platforms is fueling growth, while stringent safety standards continue to drive demand across both offshore and onshore projects.

China Rigless Intervention Systems Market Insight

The China rigless intervention systems market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding offshore exploration activities, rapid technological adoption, and investment in subsea infrastructure. China is one of the largest markets for offshore intervention solutions, and rigless systems are increasingly used for inspection, maintenance, and minor repairs without full rig mobilization. Government policies promoting safe and cost-efficient operations, alongside strong domestic manufacturers, are key factors propelling the market in China.

Rigless Intervention Systems Market Share

The Rigless Intervention Systems industry is primarily led by well-established companies, including:

- Baker Hughes Company (U.S.)

- Schlumberger Limited (U.S.)

- Weatherford (U.S.)

- Halliburton (U.S.)

- EFC Group Ltd (U.K.)

- Oceaneering International, Inc. (U.S.)

- Alpha Plus (U.K.)

- Unity (U.K.)

- AccessESP (U.S.)

- Aker Solutions (Norway)

- Gulf Intervention Services DMCC (U.A.E.)

- Evonate Systems Limited (U.K.)

Latest Developments in Global Rigless Intervention Systems Market

- In August 2025, Schlumberger (U.S.) announced a strategic partnership with a leading technology firm to develop AI-driven rigless intervention solutions. This collaboration aims to enhance predictive maintenance, reduce operational downtime, and optimize costs. The development is expected to set new industry benchmarks for efficiency and reliability, strengthening Schlumberger’s competitive position in the global market

- In September 2025, Halliburton (U.S.) launched an advanced suite of rigless intervention technologies designed to improve well integrity and production performance. These solutions address challenges in aging infrastructure and provide tailored operational enhancements. The launch is likely to bolster Halliburton’s market presence by offering clients innovative, performance-focused intervention options

- In July 2025, Baker Hughes (U.S.) introduced a sustainability initiative targeting the reduction of carbon emissions in rigless interventions. This move supports global environmental goals while demonstrating Baker Hughes’ commitment to responsible practices. The initiative is expected to attract environmentally conscious clients and reinforce the company’s reputation as a sustainable leader in the industry

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Rigless Intervention Systems Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Rigless Intervention Systems Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Rigless Intervention Systems Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.