Global Risk Management Software Market

Market Size in USD Billion

USD

41.40 Billion

USD

87.16 Billion

2024

2032

USD

41.40 Billion

USD

87.16 Billion

2024

2032

| 2025 - 2032 | |

| USD 41.40 Billion | |

| USD 87.16 Billion | |

| % | |

|

Risk Management Software Market Size

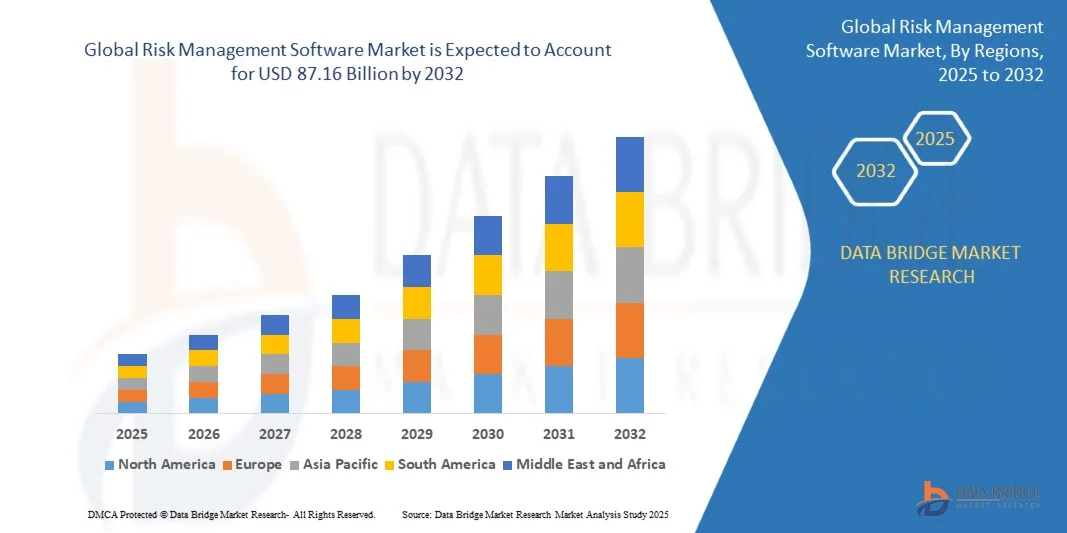

- The Risk Management Software Market size was valued at USD 41.40 billion in 2024 and is projected to reach USD 87.16 billion by 2032, growing at a CAGR of 9.75% during the forecast period.

- The market expansion is primarily driven by the rising need for regulatory compliance, real-time risk assessment, and enhanced decision-making tools across industries, particularly in finance, healthcare, and IT sectors.

- Additionally, the increasing integration of AI, machine learning, and cloud-based platforms into risk management software is transforming organizational capabilities, thereby accelerating adoption and significantly propelling market growth.

Risk Management Software Market Analysis

- Risk management software, designed to identify, assess, and mitigate risks across organizational operations, is becoming an essential tool in modern enterprise ecosystems due to its ability to enhance compliance, reduce operational losses, and improve strategic decision-making through data-driven insights.

- The accelerating demand for risk management solutions is largely driven by the growing complexity of regulatory environments, increased cyber threats, and the need for transparent governance in both public and private sectors.

- North America dominated the Risk Management Software Market with the largest revenue share of 39.01% in 2024, owing to early adoption of digital risk tools, stringent regulatory frameworks, and the strong presence of leading software providers, particularly in the U.S., where financial institutions and healthcare sectors are leading adopters.

- Asia-Pacific is expected to be the fastest-growing region in the Risk Management Software Market during the forecast period, fueled by rapid digital transformation, increased foreign investment, and growing awareness of enterprise risk management.

- The Web segment dominated the market with the largest revenue share of 51.3% in 2024, owing to its wide accessibility, easy integration with enterprise systems, and minimal installation requirements.

Report Scope and Risk Management Software Market Segmentation

|

Attributes |

Risk Management Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Risk Management Software Market Trends

“Enhanced Decision-Making Through AI and Predictive Analytics”

- A significant and accelerating trend in the Risk Management Software Market is the integration of artificial intelligence (AI) and predictive analytics to deliver real-time insights, automate risk detection, and support data-driven decision-making across enterprises. This transformation is enabling organizations to proactively manage risks with greater accuracy and efficiency.

- For instance, IBM’s OpenPages with Watson utilizes AI to automate risk identification and analysis, offering contextual insights that help businesses prioritize threats and compliance issues. Similarly, Oracle Risk Management Cloud uses AI to monitor transactions and detect anomalies, enhancing fraud prevention and governance.

- AI-powered risk management tools can learn from historical data and behavior patterns to predict potential issues before they arise. These systems offer intelligent alerts, suggest mitigation strategies, and adapt to evolving risk landscapes. SAS Viya, for instance, leverages machine learning to improve the accuracy of risk models and streamline regulatory reporting.

- The integration of AI with risk platforms enables centralized oversight and seamless connectivity with other enterprise tools, such as ERP, CRM, and cybersecurity systems. This ensures that risk insights are embedded into operational workflows, promoting more agile and informed business decisions across departments.

- This trend is reshaping how organizations perceive and manage risk, transitioning from reactive approaches to proactive and preventive strategies. Companies like SAP and Microsoft are investing in AI-based solutions that offer customizable dashboards, real-time analytics, and automated compliance tracking for a unified risk management framework.

- The demand for AI-enabled risk management software is rising rapidly across sectors such as finance, healthcare, and manufacturing, as businesses prioritize resilience, transparency, and regulatory alignment in an increasingly complex risk environment.

Risk Management Software Market Dynamics

Driver

“Growing Need Due to Rising Regulatory Pressure and Complex Risk Landscapes”

- The escalating complexity of global business operations, coupled with increasing regulatory scrutiny across sectors such as finance, healthcare, and manufacturing, is significantly driving the demand for risk management software.

- For instance, in March 2024, SAP launched updates to its Governance, Risk, and Compliance (GRC) solutions to help enterprises streamline regulatory adherence, enhance internal controls, and prepare for evolving compliance standards like ESG reporting. These advancements reflect the industry’s strategic focus on compliance automation and risk transparency.

- As organizations face growing threats ranging from cyberattacks and operational disruptions to third-party risks, the need for real-time risk monitoring and mitigation tools becomes imperative. Risk management platforms provide comprehensive features such as predictive analytics, real-time dashboards, and automated alerts, offering a substantial upgrade over manual or fragmented processes.

- Furthermore, the growing digital transformation across industries is integrating risk management directly into business workflows, making such software essential for achieving resilience, continuity, and informed decision-making.

- The ability to assess, quantify, and mitigate various types of risks—financial, operational, reputational, or compliance-related—through centralized, data-driven systems is fueling adoption across large enterprises and mid-sized businesses. This trend is further supported by the growing awareness of the financial and reputational damage caused by unmanaged risks.

Restraint/Challenge

Concerns Regarding Data Privacy and High Implementation Costs”

- Despite its benefits, the Risk Management Software Market faces significant challenges, particularly regarding data privacy concerns and the high cost of deployment. The storage and analysis of sensitive enterprise data in cloud-based risk platforms raise fears of data breaches and unauthorized access.

- For instance, regulatory requirements like the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) have increased pressure on organizations to ensure their risk tools comply with strict data governance and privacy standards.

- To address these concerns, leading vendors like Oracle and IBM emphasize end-to-end encryption, strict access controls, and transparent data handling practices in their risk management offerings. Nonetheless, compliance complexity remains a hurdle for smaller businesses.

- Additionally, the initial cost of implementing comprehensive risk management systems—particularly those involving AI, automation, and cloud integration—can be high, deterring adoption among smaller enterprises or cost-sensitive sectors. Costs associated with licensing, training, integration with existing systems, and ongoing support can strain IT budgets.

- Although many vendors are now offering scalable and modular solutions to lower barriers to entry, affordability and ease of use remain critical for broader market penetration. Addressing these challenges through more cost-effective, privacy-focused, and user-friendly platforms will be essential for sustaining long-term growth in the market.

Risk Management Software Market Scope

The market is segmented on the basis of type, service type, deployment, types of software, and end- users.

• By Type

On the basis of type, the Risk Management Software Market is segmented into web, android native, IoS native, and others. The web segment dominated the market with the largest revenue share of 51.3% in 2024, owing to its wide accessibility, easy integration with enterprise systems, and minimal installation requirements. Web platforms allow organizations to manage risk through centralized dashboards and access real-time analytics across departments, enhancing efficiency and collaboration.

The Android Native segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the proliferation of Android devices among enterprise users and field personnel. Android-native applications offer enhanced performance, offline access, and user-friendly interfaces, particularly useful for mobile risk reporting and audit tasks. As mobile-first strategies become increasingly common in enterprise risk functions, demand for Android-native solutions continues to rise, particularly in industries with remote workforces or on-site operational risk assessments.

• By Service

On the basis of service, the market is segmented into managed service and professional service. The managed service segment dominated the market with the largest revenue share of 58.9% in 2024, due to the increasing reliance on third-party providers for ongoing monitoring, support, and software maintenance. Organizations prefer managed services to minimize in-house IT workload, ensure compliance, and access specialized expertise.

The professional service segment is projected to grow at the fastest CAGR from 2025 to 2032, as companies seek consulting, system integration, training, and customization support during the deployment and scaling of risk management platforms. The demand for tailored solutions and end-to-end implementation guidance is particularly high among large enterprises and regulated industries like finance and healthcare, where precision in risk handling is critical.

• By Deployment

Based on deployment, the market is segmented into on-premises and cloud. The cloud segment dominated the market with the highest revenue share of 64.7% in 2024, driven by its scalability, lower upfront costs, remote accessibility, and seamless updates. Cloud-based risk management platforms are preferred for their rapid deployment and integration capabilities, especially among SMEs and multinational corporations.

The cloud segment is also anticipated to witness the fastest CAGR from 2025 to 2032, as digital transformation and hybrid work environments drive the need for flexible, secure, and real-time risk monitoring tools. The increasing availability of AI-powered features, real-time alerts, and global compliance modules within cloud platforms further supports this trend. Conversely, while On-Premises deployment offers greater control and customization, it is gradually losing traction due to high maintenance and limited scalability.

• By Types of Software

On the basis of software type, the market is segmented into enterprise risk management software, financial risk management software, integrated risk management software, application risk management software, market risk management software, credit risk management software, information technology risk management software, quantitative risk management software, and project risk management software.The Enterprise Risk Management (ERM) Software segment held the largest market share of 28.4% in 2024, supported by increasing demand for holistic frameworks that address multiple risk categories across an organization. ERM software helps align risk strategies with business goals, manage compliance, and improve transparency.

The Integrated Risk Management (IRM) Software segment is projected to witness the fastest growth during 2025–2032, as companies move toward unified platforms that consolidate risk, compliance, audit, and policy management functions. The growing need for cross-functional collaboration and real-time insights is fueling the shift from siloed systems to integrated risk management tools.

• By End-User

On the basis of end-user, the Risk Management Software Market is segmented into banking, insurance, asset management, energy and utilities, educational institutions, healthcare, telecom, information technology, oil and gas, retail, and life sciences. The banking led the market with the largest revenue share of 22.6% in 2024, driven by strict regulatory requirements, fraud risk, and the complexity of financial operations. Banks are investing heavily in risk platforms to manage credit, market, and operational risks efficiently.

The healthcare is expected to grow at the fastest CAGR from 2025 to 2032, spurred by increasing cyber threats, regulatory compliance (such as HIPAA), and the need for data protection and patient safety. As healthcare organizations adopt digital records and telemedicine, risk management software plays a crucial role in safeguarding data, managing vendor risks, and ensuring continuous operations amid growing system dependencies.

Risk Management Software Market Regional Analysis

- North America dominated the Risk Management Software Market with the largest revenue share of 39.01% in 2024, driven by stringent regulatory frameworks, high cybersecurity awareness, and strong adoption of digital risk solutions across key industries such as finance, healthcare, and IT.

- Organizations in the region prioritize comprehensive risk visibility, compliance automation, and advanced analytics to mitigate operational, financial, and reputational risks. The widespread use of cloud infrastructure and integration of AI in enterprise systems further supports the rapid deployment of risk management platforms.

- The market's growth is bolstered by the presence of leading software vendors, a mature IT ecosystem, and a proactive approach to risk mitigation and data protection. As businesses increasingly operate in hybrid and remote environments, North American enterprises continue to invest in scalable, cloud-based risk management solutions that enable real-time monitoring and strategic decision-making across complex risk landscapes.

U.S. Risk Management Software Market Insight

The U.S. Risk Management Software Market captured the largest revenue share of 80% within North America in 2024, driven by rising regulatory scrutiny, increasing data privacy concerns, and the accelerated adoption of digital enterprise solutions. U.S.-based companies are rapidly implementing risk management platforms to ensure compliance with frameworks such as SOX, HIPAA, and CCPA. The growing need for real-time risk monitoring, cyber threat mitigation, and financial governance is further fueling demand. Additionally, the presence of major market players such as IBM, Oracle, and Microsoft, along with widespread cloud infrastructure, supports ongoing innovation and adoption. The expansion of AI and machine learning in risk analytics tools is also helping organizations enhance predictive capabilities and decision-making across financial services, healthcare, and tech industries.

Europe Risk Management Software Market Insight

The Europe Risk Management Software Market is projected to grow at a strong CAGR throughout the forecast period, driven by stringent regulatory standards such as GDPR and ESG reporting mandates. European enterprises are investing heavily in integrated risk platforms to ensure compliance, transparency, and resilience in their operations. The increasing adoption of cloud technologies, particularly in Western Europe, supports flexible and scalable deployment of risk solutions. Additionally, the rise in cyber incidents and data protection concerns is prompting both public and private sector entities to adopt robust risk frameworks. Key countries including Germany, the U.K., and France are seeing accelerated adoption, especially in finance, insurance, and energy sectors.

U.K. Risk Management Software Market Insight

The U.K. Risk Management Software Market is expected to grow at a notable CAGR during the forecast period, supported by the country’s advanced regulatory landscape and growing focus on governance, risk, and compliance (GRC) solutions. British companies are emphasizing operational resilience and third-party risk management in response to post-Brexit market conditions and evolving data protection laws. The financial sector, in particular, is a major adopter due to strict oversight from entities like the FCA and PRA. Additionally, the U.K.'s mature digital infrastructure, combined with increased investment in enterprise AI and analytics, is contributing to the uptake of intelligent, cloud-based risk management platforms.

Germany Risk Management Software Market Insight

The Germany Risk Management Software Market is projected to expand at a significant CAGR during the forecast period, driven by the nation’s strong industrial base, emphasis on data privacy, and demand for operational risk mitigation. With GDPR enforcement and rising cyber risks, German enterprises are turning to risk management software to safeguard data and ensure regulatory compliance. The manufacturing and automotive sectors are increasingly deploying software to manage supply chain and project-related risks. Germany’s preference for secure, localized cloud solutions also supports market growth, particularly among mid-sized firms seeking integrated, AI-powered tools that align with national data protection standards.

Asia-Pacific Risk Management Software Market Insight

The Asia-Pacific Risk Management Software Market is poised to grow at the fastest CAGR of 24% from 2025 to 2032, fueled by digital transformation, regulatory evolution, and increasing enterprise awareness in countries like China, Japan, and India. As regional economies modernize and expand their digital ecosystems, the need for scalable, cloud-based risk platforms is accelerating. Government initiatives promoting cybersecurity, data sovereignty, and digital governance are also boosting adoption across banking, healthcare, and telecom sectors. Furthermore, the rise of regional software vendors and cost-effective solutions is expanding accessibility to SMEs. APAC's rapid cloud adoption and cross-border trade dynamics are positioning the region as a key growth hub for risk management software.

Japan Risk Management Software Market Insight

The Japan Risk Management Software Market is gaining momentum due to its advanced IT infrastructure, strong regulatory environment, and heightened focus on business continuity. Japanese organizations are adopting integrated risk management platforms to address cybersecurity, supply chain disruptions, and operational vulnerabilities. The country’s commitment to innovation is reflected in the growing use of AI-driven analytics and automated compliance tools. Sectors such as finance, manufacturing, and healthcare are leading adopters, with emphasis on predictive risk identification and disaster recovery planning. As Japan continues its push towards digital government and corporate governance reforms, demand for robust, scalable risk software is expected to grow significantly.

China Risk Management Software Market Insight

The China Risk Management Software Market held the largest revenue share in Asia-Pacific in 2024, driven by rapid enterprise digitization, strict regulatory reforms, and an expanding base of tech-savvy companies. The Chinese government’s emphasis on cybersecurity law compliance and digital risk control is accelerating adoption across industries such as banking, e-commerce, and energy. Domestic software providers, alongside global players, are contributing to a competitive and fast-growing market landscape. With ongoing development of smart cities and a shift toward cloud-native enterprise platforms, China continues to invest heavily in risk analytics, compliance automation, and data protection tools, making it a regional leader in the market.

Risk Management Software Market Share

The risk management software industry is primarily led by well-established companies, including:

- Adobe (U.S.)

- Oracle (U.S.)

- HubSpot, Inc. (U.S.)

- SAS Institute Inc. (U.S.)

- HP Development Company, L.P. (U.S.)

- SimplyCast (Canada)

- Act-On Marketing Automation (U.S.)

- Infor (U.S.)

- Vendasta (U.S.)

- Sailthru (U.S.)

- Thryv, Inc. (U.S.)

- Keap (U.S.)

- IBM (U.S.)

- SAP (Germany)

- Microsoft (U.S.)

- Gannett Co, Inc. (U.S.)

- Demandbase (U.S.)

- WordStream (U.S.)

- CAKE (U.S.)

- Chetu Inc. (India)

What are the Recent Developments in Risk Management Software Market?

- In April 2023, IBM launched a new integrated risk management platform designed specifically for financial institutions in South Africa. This initiative aims to enhance regulatory compliance, operational risk visibility, and cyber threat mitigation tailored to the local market’s unique challenges. By leveraging AI-driven analytics and automation, IBM is reinforcing its leadership in delivering advanced risk management solutions globally, addressing the increasing demand for robust software in emerging markets.

- In March 2023, Oracle Corporation introduced its updated risk management suite, focusing on enhanced predictive analytics and real-time monitoring capabilities for educational institutions and government agencies. The new features aim to strengthen emergency response protocols and regulatory adherence, underscoring Oracle’s commitment to developing innovative technologies that safeguard critical public and private sector assets.

- In March 2023, Honeywell International Inc. successfully deployed a comprehensive enterprise risk management system as part of the Bengaluru Smart City Project. This project leverages Honeywell’s advanced software solutions to bolster urban infrastructure resilience and cybersecurity. The initiative exemplifies Honeywell’s focus on integrating risk software with smart city frameworks to create safer, more efficient urban environments.

- In February 2023, SAP SE announced a strategic partnership with the European Banking Federation to develop a specialized risk management marketplace tailored for banking professionals. This collaboration aims to streamline compliance workflows, enhance fraud detection, and improve data governance practices across financial institutions, reflecting SAP’s ongoing dedication to innovation and operational excellence in the risk management sector.

- In January 2023, Microsoft Corporation unveiled the latest version of its cloud-based risk management software at the RSA Conference 2023. The upgraded platform features improved AI-powered threat detection, automated compliance reporting, and seamless integration with Azure cloud services. Microsoft’s advancements highlight its commitment to empowering enterprises with cutting-edge tools to proactively manage risks in a rapidly evolving digital landscape.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.