Global Rosin Resins Market

Market Size in USD Billion

USD

156.20 Billion

USD

255.61 Billion

2025

2033

USD

156.20 Billion

USD

255.61 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 156.20 Billion |

Market Size (Forecast Year) |

USD 255.61 Billion |

CAGR |

% |

Major Markets Players |

|

Rosin Resins Market Overview

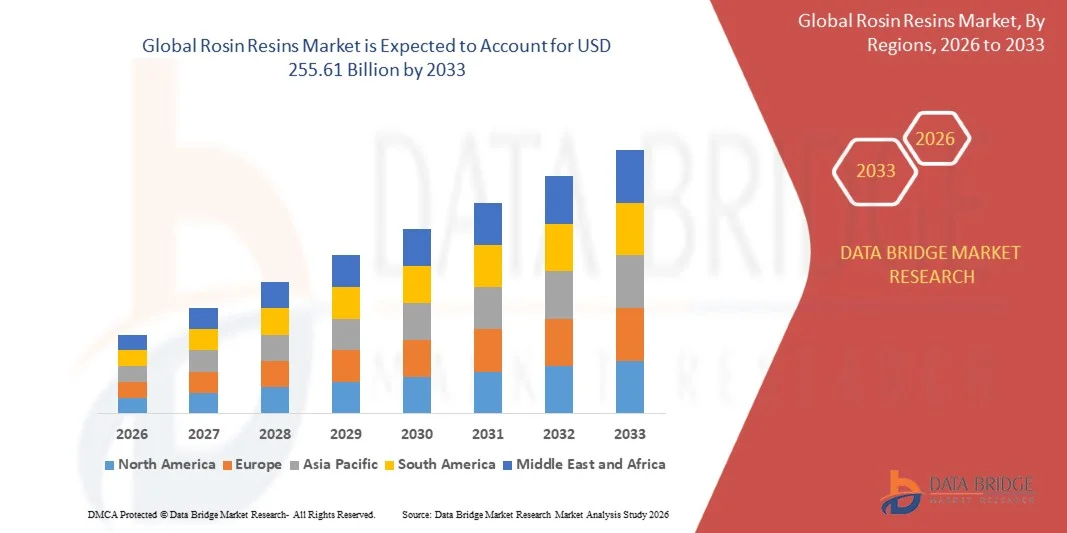

As per Data Bridge Market Research Analysis the Rosin Resins Market was valued at USD 156.2 million in 2025 and is projected to reach USD 255.61 million by 2033, growing at a CAGR of 6.35% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for bio-based and sustainable materials across adhesives, coatings, and rubber industries, rapid advancements in rosin modification technologies, and expanding applications in food packaging, cosmetics, and pharmaceutical sectors .

The increasing consumer awareness regarding environmental sustainability, combined with stringent government regulations on VOC emissions and petrochemical-based products, is compelling manufacturers, formulators, and end-use industries to adopt rosin-based alternatives. Gum rosin and tall oil rosin derivatives are replacing synthetic hydrocarbon resins in many applications, offering renewable sourcing, biodegradability, and excellent tackifying properties for adhesives, coatings, and rubber compounding .

Key Market Trends & Insights

- Asia Pacific dominated the Rosin Resins Market with the largest revenue share of approximately 45% in 2025, supported by China's position as the world's largest gum rosin producer and substantial downstream processing capacity, along with rapid industrialization across India, Japan, and Southeast Asian nations .

- Asia Pacific is expected to be the fastest-growing region at a CAGR of 7.09% from 2026 to 2033, fueled by increasing urbanization, expanding manufacturing sectors, growing packaging industry, and rising automotive production in China, India, and Japan .

- The Rosin Acids segment led the market with a 32.23% share in 2024, driven by widespread use as tackifiers in adhesives, rubber compounding, and as precursors for modified rosin derivatives .

- Hydrogenated Rosin Resins are the fastest-growing type segment, projected to register a CAGR of 6.51%, reflecting the surge in demand for thermally stable, light-colored rosin derivatives for high-performance adhesives, coatings, and food-contact applications .

- The Adhesives segment dominated the application category with a 34.60% revenue share in 2024, driven by extensive use of rosin esters as tackifiers in hot-melt adhesives, pressure-sensitive adhesives, and packaging applications .

- The Gum Rosin segment accounted for 62.51% of the market share in 2024, preferred for its superior quality characteristics including lighter color, lower impurity content, and more consistent chemical composition for high-grade applications .

- Gum Rosin remains the dominant source segment, supported by growing demand for premium-grade rosin in electronics solder flux, specialty adhesives, and food-grade formulations .

- The Coatings segment is the fastest-growing application category, with a CAGR of 6.26%, driven by demand for low-VOC, bio-based coating formulations and increasing adoption in automotive, construction, and industrial applications .

- Eastman Chemical Company and Kraton Corporation remain key players in the rosin resins market, focusing on biobased product innovation and strategic partnerships to develop sustainable adhesive solutions with reduced environmental impact .

Market Size & Forecast

- Global Market Value (2025): USD 156.2 Million

- Expected Market Value (2033): USD 255.61 Million

- Forecast CAGR (2026–2033): 6.35%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: Asia-Pacific

Report Scope and Rosin Resins Market Segmentation

|

Attributes |

Rosin Resins Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Eastman Chemical Company (U.S.) · Kraton Corporation (U.S.) · Harima Chemicals Group Inc. (Japan) · Arakawa Chemical Industries Ltd. (Japan) · Dérivés Résiniques et Terpéniques (DRT) (France) · Ingevity Corporation (U.S.) · Lawter Inc. (U.S.) · Foreverest Resources Ltd. (China) · Resin Chemicals Co., Ltd. (China) · Florachem Corporation (U.S.) · Guilin Songquan Forest Chemical Industry Co., Ltd. (China) · Hindustan Resins & Terpenes (India) · G.C. RUTTEMAN & Co. (Netherlands) · Pinopine (Portugal) · SpecialChem (France) · Jubilant Ingrevia Limited (India) · DIC Corporation (Japan) · Sinofi Ingredients LLC (U.S.) · Guangdong Komo Co. Ltd. (China) · Xinyi Sonyuan Chemical Co. Ltd. (China) · Wuzhou Sun Shine Forestry and Chemicals (China) · Baolin Chemical Group Co., Ltd. (China) |

|

Market Opportunities |

· Growing demand for bio-based and sustainable packaging solutions · Development of water-dispersible low-VOC formulations · Technological advancements in hydrogenation and esterification processes |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Rosin Resins MarketTrends

Trend: Growth in Bio-Based and Sustainable Product Innovation

Major companies operating in the rosin resins market are increasingly focusing on developing biobased and sustainable product innovations through strategic partnerships and technology collaborations to reduce carbon emissions, enhance performance, and meet the growing demand for eco-friendly adhesive and coating solutions . For instance, in March 2024, Henkel AG & Co. KGaA partnered with Kraton Corporation, where Kraton supplies Henkel with biobased tackifiers and its patented REvolution™ rosin ester technology, enabling significant carbon emission reductions in Henkel's Technomelt hot melt adhesive portfolio . The collaboration supports Henkel's goal to expand eco-friendly packaging and consumer goods solutions without compromising performance, with Kraton's REvolution offering a renewable, high-performance alternative to fossil-based tackifiers .

Rosin Resins Market Dynamics

Key Market Driver: Rising Demand for Bio-Based and Sustainable Materials

The global transition toward sustainable and renewable resources is fundamentally reshaping the chemical industry landscape, with rosin resin emerging as a preferred bio-based alternative to petroleum-derived synthetic resins . Extracted from pine trees through environmentally responsible tapping processes, rosin resin offers biodegradability and renewable sourcing advantages that align with increasingly stringent environmental regulations and corporate sustainability commitments . According to the U.S. Environmental Protection Agency (EPA), demand for renewable chemical inputs has grown by over 12% annually since 2019, while the pine-derived chemicals market is projected to reach US$ 9.6 billion by 2035 with a CAGR of 4.4%, creating a supportive ecosystem for rosin resin adoption across complementary applications in adhesives, paints, and surfactants where sustainability credentials are increasingly non-negotiable .

In May 2025, Solena Materials announced a US$6.7 million seed funding round to expand production of biodegradable, bio-based protein fibres for the apparel industry. The investment reflects growing commercial interest in replacing petroleum-derived synthetic textiles with sustainable alternatives.

Key Restraint/Challenge: Raw Material Price Volatility and Supply Chain Vulnerabilities

A significant restraint in the global rosin resin market is the high volatility in raw material prices and supply chain vulnerabilities. Production depends entirely on pine resin extraction from live trees or processing of pine stumps and tall oil byproducts from kraft paper manufacturing . Global pine resin supply is concentrated in specific geographical regions, primarily China, creating supply concentration risks. Climate variations, forest fires, regulatory restrictions on pine tapping practices, and competing land uses for pine forests contribute to supply uncertainty and periodic price spikes that impact manufacturing cost structures . The 2023-2024 period witnessed pine resin prices fluctuate by 15-20% due to reduced tapping activities in key producing regions of Guangxi and Yunnan provinces in China, affecting downstream rosin resin production economics .

In February 2025, the Indian Chemical News Compendium 2025 highlighted that the specialty chemicals industry remains highly dependent on imported petrochemical feedstocks and intermediates. The report identified global raw material price volatility, reliance on imports (particularly from Asia), logistics bottlenecks, and feedstock shortages as major challenges affecting production costs and supply chain resilience.

Key Market Opportunity: Integration of AI and Autonomous Formulation Development

The integration of artificial intelligence in rosin resin formulation development presents a significant market opportunity. AI utilizes molecular dynamics simulations as well as machine learning to determine the ideal chemical composition for new resins, enhancing properties such as durability and heat resistance while decreasing trial-and-error experimentation . AI determines data from sensors to automate complex machinery, thus adjusting processing conditions in real-time to guarantee consistent quality. AI platforms aid in matching specific polymer properties to end-user application needs, enhancing material selection and reducing waste. The development of cloud-based formulation tools and collaborative research platforms is further democratizing access to advanced rosin modification technologies, opening growth opportunities across cost-sensitive markets in Asia-Pacific, Latin America, and the Middle East.

In June 2025, Researchers at the U.S. National Institute of Standards and Technology (NIST) published the development of an Autonomous Formulation Lab (AFL) that uses artificial intelligence, robotics, and active learning algorithms to automatically prepare, test, and optimize soft material formulations. The platform significantly accelerates formulation discovery and demonstrated its ability to replace petroleum-derived ingredients with sustainable alternatives through autonomous experimentation.

Rosin Resins Market Scope

The rosin resins market is segmented on the basis of type, source, application, and end-use industry

- By Type

On the basis of type, the Rosin Resins Market is segmented into rosin acids, rosin esters, hydrogenated rosin resins, dimerized rosin resins, and modified rosin resins. The Rosin Acids segment dominated the market with a 32.23% share in 2024, owing to widespread use as tackifiers in adhesives, rubber compounding, and as precursors for modified rosin derivatives . These systems deliver essential adhesive and processing properties, making them the preferred choice for adhesive formulators, rubber manufacturers, and coating producers.

The Hydrogenated Rosin Resins segment is projected to register the fastest growth at a CAGR of 6.51% from 2026 to 2033, driven by rising demand for thermally stable, light-colored rosin derivatives for high-performance adhesives, coatings, and food-contact applications . Advances in hydrogenation technology, combined with declining processing costs and growing adoption in food packaging and pharmaceutical applications, are accelerating segment expansion .

- By Source

On the basis of source, the Rosin Resins Market is segmented into gum rosin, wood rosin, and tall oil rosin. The Gum Rosin segment led the market with a 62.51% share in 2024, supported by superior quality characteristics including lighter color, lower impurity content, and more consistent chemical composition compared to alternative sources . Gum rosin is preferred for high-grade applications in adhesives, coatings, and pharmaceutical formulations, with China dominating global gum rosin production .

The Tall Oil Rosin segment is expected to experience the fastest growth at a CAGR of 5.89% from 2026 to 2033, driven by increasing demand for sustainable raw materials and the segment's position as a byproduct of the kraft paper pulping process, offering a renewable alternative to gum rosin . The growing availability of tall oil rosin from integrated pulp mills in North America and Europe, combined with its cost-competitive nature, is accelerating segment expansion .

- By Application

On the basis of application, the Rosin Resins Market is segmented into rubbers, coatings, inks, adhesives, food & beverages, cosmetics & personal care, and others. The Adhesives segment dominated the market with a share of 34.60% in 2024 due to its widespread adoption by adhesive formulators, packaging manufacturers, and construction material producers, increasing demand for bio-based and sustainable tackifiers, and growing integration with advanced modification technologies such as hydrogenation, esterification, and polymerization . Additionally, rising focus on eco-friendly packaging, regulatory compliance, and reducing carbon footprint further supports the strong adoption of rosin resin solutions in adhesive applications .

The Coatings segment is anticipated to witness the fastest CAGR of 6.26% from 2026 to 2033, driven by this growth fueled by the increasing reliance on rosin resins for low-VOC, bio-based coating formulations for automotive, construction, and industrial applications . Paint manufacturers, coating formulators, and automotive OEMs are adopting advanced rosin derivatives to conduct cost-effective, environmentally compliant, and high-performance coating solutions. Additionally, the integration of waterborne and solvent-free coating technologies is enhancing the applicability and efficiency of rosin-based coating formulations, further driving segment growth .

- By End-Use Industry

On the basis of end-use industry, the Rosin Resins Market is segmented into packaging, construction, automotive, electronics, and others. The Packaging segment dominated the market with a share of approximately 35% in 2024 due to its critical role in providing sustainable and biodegradable adhesive solutions for paperboard, corrugated materials, and packaging applications . The widespread adoption of rosin resin-based hot-melt adhesives for carton sealing, case sealing, and bookbinding, combined with the segment's essential role in sustainable packaging solutions, is driving strong demand for rosin resin formulations .

The Construction segment is expected to witness the fastest CAGR of approximately 6.5% from 2026 to 2033, driven by the rising need for eco-friendly adhesive and coating solutions for flooring, lamination, and wood panel applications . Construction material manufacturers and contractors are increasingly integrating rosin resin-based adhesives into building applications to reduce VOC emissions and improve sustainability credentials. Additionally, the growing emphasis on green building materials, regulatory compliance, and sustainable construction practices is further accelerating the adoption of rosin resin technologies across construction operations .

Rosin Resins Market Regional Analysis

Asia Pacific dominated the rosin resins market and accounted for the largest revenue share of approximately 45% in 2025, supported by China's position as the world's largest gum rosin producer at 400,000-450,000 metric tons annually, substantial downstream processing capacity, and the presence of established adhesive, rubber, and coating manufacturing industries . The region also benefits from rapid industrialization, expanding manufacturing sectors, growing packaging industry, and rising automotive production across China, India, Japan, and Southeast Asian nations . Increasing focus on bio-based materials and sustainable sourcing continues to strengthen Asia Pacific's leadership position in the global market.

U.S. Rosin Resins Market Insight

The U.S. rosin resins market is experiencing steady growth, supported by rising adoption of bio-based materials in professional adhesive formulations, automotive coatings, and packaging applications . Increasing investments in sustainable infrastructure and growing demand for cost-effective, eco-friendly alternatives to petroleum-based resins are contributing to market growth. Furthermore, integration of advanced hydrogenation and esterification technologies is improving rosin resin performance and formulation efficiency, positioning the U.S. as a key innovation hub in the rosin resins industry.

Germany Rosin Resins Market Insight

The Germany rosin resins market is expanding steadily due to the country's strong automotive manufacturing base, advanced chemical research capabilities, and increasing adoption of next-generation bio-based material technologies . Automotive companies, adhesive manufacturers, and coating formulators are increasingly utilizing rosin resins for sustainable formulations, vehicle interior bonding, and R&D activities. Continuous advancements in hydrogenation technology, AI integration, and sustainable formulation approaches, along with strong government focus on circular economy and innovation, are further driving market growth in Germany .

China Rosin Resins Market Insight

The China rosin resins market is growing rapidly, driven by increasing urbanization, expanding transportation infrastructure, and rising government focus on sustainable materials and environmental protection . Growing adoption of advanced rosin modification platforms across commercial, automotive, and packaging sectors is significantly boosting market demand. In addition, rising investments in chemical R&D, increasing awareness regarding sustainable manufacturing practices, and rapid technological advancements are positioning China as one of the fastest-growing markets for rosin resins globally .

Asia-Pacific Driving Simulators Market Insight

The Asia-Pacific driving simulators market is expected to witness rapid growth, driven by increasing urbanization, expanding automotive production, and rising investments in driver training infrastructure across countries such as China, India, and Japan. Growing awareness regarding road safety, rising adoption of advanced simulation technologies, and increasing demand for scalable and cost-effective training solutions are supporting regional market expansion. Additionally, the growing presence of automotive R&D centers and motorsport activities is accelerating simulator adoption across commercial and academic sectors.

Japan Rosin Resins Market Insight

The Japan rosin resins market is witnessing consistent growth due to rising investments in advanced chemical technologies, automotive innovation, and sustainable material initiatives . Automotive manufacturers, electronics companies, and adhesive formulators are increasingly adopting high-performance rosin derivatives for precision bonding, electronic encapsulation, and coating applications. Moreover, increasing integration of AI-enabled formulation tools and the country's focus on efficient and sustainable manufacturing are further contributing to market growth .

India Rosin Resins Market Insight

The India rosin resins market is growing steadily, driven by increasing urbanization, expanding automotive production, and rising investments in driver training infrastructure across the country . Growing awareness regarding sustainable materials, rising adoption of advanced rosin modification technologies, and increasing demand for scalable and cost-effective bio-based solutions are supporting regional market expansion. Additionally, the growing presence of chemical R&D centers and increasing industrial activity is accelerating rosin resin adoption across commercial and industrial sectors .

Rosin Resins Market Share

The rosin resins industry is primarily led by well-established companies, including:

- Eastman Chemical Company (U.S.)

- Kraton Corporation (U.S.)

- Harima Chemicals Group Inc. (Japan)

- Arakawa Chemical Industries Ltd. (Japan)

- Dérivés Résiniques et Terpéniques (DRT) (France)

- Ingevity Corporation (U.S.)

- Lawter Inc. (U.S.)

- Foreverest Resources Ltd. (China)

- Resin Chemicals Co., Ltd. (China)

- Florachem Corporation (U.S.)

- Guilin Songquan Forest Chemical Industry Co., Ltd. (China)

- Hindustan Resins & Terpenes (India)

- C. RUTTEMAN & Co. (Netherlands)

- Pinopine (Portugal)

- SpecialChem (France)

- Jubilant Ingrevia Limited (India)

- DIC Corporation (Japan)

- Sinofi Ingredients LLC (U.S.)

- Guangdong Komo Co. Ltd. (China)

- Xinyi Sonyuan Chemical Co. Ltd. (China)

- Wuzhou Sun Shine Forestry and Chemicals (China)

- Baolin Chemical Group Co., Ltd. (China)

Latest Developments in Rosin Resins Market

- In September 2024, Kraton Corporation launched its REvolution™ Rosin Ester technology, offering a sustainable alternative for the adhesive industry . This technology uses renewable resources, primarily derived from pine rosin, to produce versatile rosin esters capable of replacing petroleum-based products. Emphasizing circularity, Kraton's solution ensures products can be recycled or repurposed at the end of their lifecycle, supporting eco-friendly principles and fostering innovation in industries seeking to reduce their carbon footprint and transition to bio-based materials .

- In March 2024, Henkel AG & Co. KGaA partnered with Kraton Corporation to enhance sustainability in adhesive technologies . Under the agreement, Kraton will supply Henkel with biobased tackifiers and its patented REvolution rosin ester technology, enabling significant carbon emission reductions in Henkel's Technomelt hot melt adhesive portfolio. Two of Henkel's Technomelt adhesives achieved a ~25% cradle-to-gate carbon footprint reduction through use of Kraton's SYLVALITE™ 2200 biobased tackifiers developed with REvolution rosin ester technology .

- In March 2024, Grupo Resinas Brasil (RB), a Brazil-based producer of pine oleoresin, gum rosin, and related derivatives, acquired Pinopine for an undisclosed amount . Through this acquisition, Grupo RB aims to strengthen its presence in Europe by securing a logistics hub and derivatives-production capability near major consuming regions, thereby expanding its global distribution network and downstream rosin resin product offerings .

- In September 2023, Eastman Chemical Company expanded its rosin resin production by 20% in response to the growing demand for rosin resins in a variety of applications .

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Rosin Resins Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Rosin Resins Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Rosin Resins Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.