Global Satellite Ground Station Market

Market Size in USD Billion

USD

50.94 Billion

USD

144.82 Billion

2025

2033

USD

50.94 Billion

USD

144.82 Billion

2025

2033

| 2026 - 2033 | |

| USD 50.94 Billion | |

| USD 144.82 Billion | |

| % | |

|

Satellite Ground Station Market Size

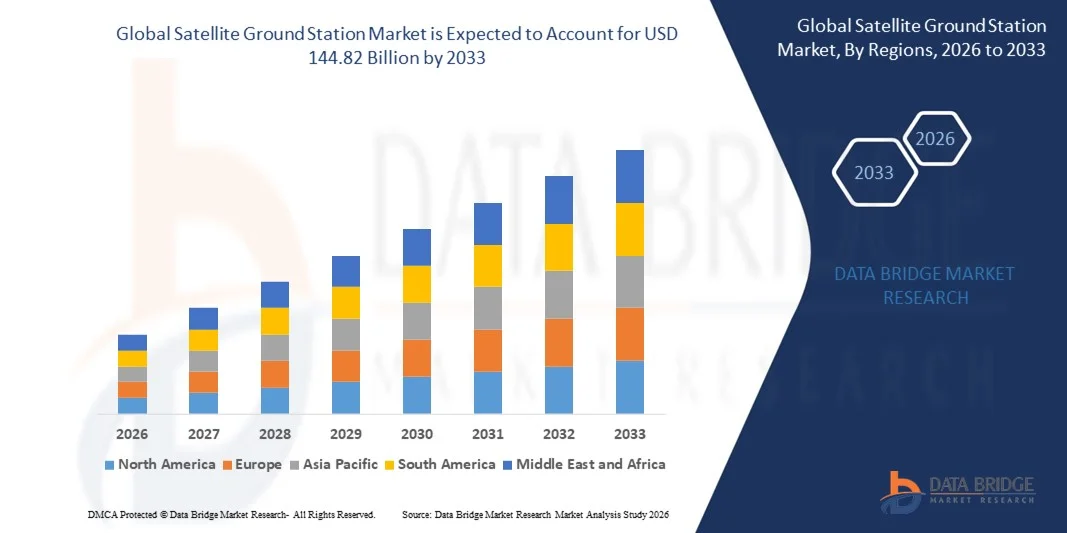

- The global satellite ground station market size was valued at USD 50.94 billion in 2025 and is expected to reach USD 144.82 billion by 2033, at a CAGR of 13.95% during the forecast period

- The market growth is largely fuelled by the rising deployment of LEO, MEO, and GEO satellites for communication, navigation, and Earth observation applications

- Increasing demand for high-speed data transmission, satellite internet services, and broadband connectivity is supporting market expansion

Satellite Ground Station Market Analysis

- The market is witnessing increasing adoption of remote and automated ground stations, enabling real-time satellite monitoring and data processing

- Rising collaboration between satellite operators, telecom providers, and defense organizations is promoting the expansion of ground station networks

- North America dominated the satellite ground station market with the largest revenue share of 38.5% in 2025, driven by extensive government investments, growing commercial satellite deployments, and high adoption of advanced ground infrastructure

- Asia-Pacific region is expected to witness the highest growth rate in the global satellite ground station market, driven by rapid urbanization, rising investment in satellite broadband and Earth observation programs, and the expansion of commercial ground station infrastructure in countries such as China, Japan, and India

- The Hardware segment held the largest market revenue share in 2025, driven by the high demand for robust and reliable ground infrastructure capable of supporting diverse satellite missions. Hardware solutions provide essential components for communication, data reception, and satellite tracking, making them indispensable for both commercial and government applications. These systems are critical for ensuring uninterrupted satellite connectivity and maintaining the integrity of high-speed data transmissions. Increasing satellite launches and growing dependence on satellite networks across industries further strengthen the demand for hardware-based solutions

Report Scope and Satellite Ground Station Market Segmentation

|

Attributes |

Satellite Ground Station Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Satellite Ground Station Market Trends

Rising Adoption of Satellite Communication And Data Services

- The increasing demand for reliable and high-speed satellite communication is significantly shaping the satellite ground station market, as governments, enterprises, and telecom providers seek advanced ground infrastructure to support expanding satellite networks. Ground stations are gaining traction due to their ability to manage high-volume data, enable remote monitoring, and improve connectivity without compromising service quality. This trend is accelerating deployment across telecommunication, defense, and space exploration applications, encouraging manufacturers to innovate with scalable solutions

- Growing utilization of Earth observation, satellite imaging, and navigation services has further driven the need for advanced ground stations. Industries such as agriculture, weather forecasting, disaster management, and transportation increasingly rely on accurate satellite data, prompting investments in high-performance antennas, tracking systems, and real-time data processing technologies

- Sustainability and energy efficiency trends are influencing ground station operations, with providers focusing on low-power solutions, eco-friendly cooling, and optimized resource management. These factors enhance operational reliability, reduce environmental impact, and improve cost-efficiency for service operators

- For instance, in 2024, SES in Luxembourg and Intelsat in the U.S. expanded their ground station networks by integrating advanced telemetry, tracking, and control (TT&C) systems. These deployments were introduced to meet the growing satellite communication needs of enterprises and governments, while enabling faster data transfer and improved connectivity across multiple regions

- While the demand for satellite ground stations is rising, sustained market expansion depends on continuous R&D, cost-effective infrastructure, and integration with new satellite constellations. Providers are also focusing on improving scalability, cybersecurity, and operational efficiency to ensure reliable performance and long-term adoption

Satellite Ground Station Market Dynamics

Driver

Expansion Of Satellite-Based Applications

- Increasing reliance on satellite-based broadband, IoT connectivity, and remote sensing is a major driver for the satellite ground station market. Organizations are deploying ground stations to support communication with Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary (GEO) satellites, ensuring efficient data handling and network coverage

- Growing government and commercial initiatives in space exploration, satellite imaging, and Earth observation are further fueling market growth. Ground stations help monitor satellite health, process high-resolution data, and support critical decision-making for defense, research, and environmental monitoring

- Providers are actively enhancing ground station capabilities with automation, cloud integration, and AI-based data analytics. These efforts are driven by the demand for real-time data, reduced operational costs, and improved accuracy in satellite communications

- For instance, in 2023, Viasat in the U.S. and Kratos Defense & Security Solutions in the U.K. reported upgrades to their ground station networks, including automated telemetry systems and high-throughput antennas. This expansion enabled improved operational efficiency, faster data transmission, and enhanced connectivity for commercial and governmental users

- Although satellite-based application growth supports market expansion, adoption depends on infrastructure investment, frequency spectrum availability, and technological integration. Investment in high-capacity antennas, automated control systems, and secure communication protocols is critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Infrastructure Cost And Complex Integration Requirements

- The substantial capital expenditure required for building and maintaining satellite ground stations remains a key challenge, limiting adoption among smaller enterprises and emerging markets. High costs include antennas, tracking systems, data processing units, and secure communication infrastructure

- Integration complexities with multiple satellite constellations, varying frequency bands, and legacy systems pose operational challenges. Ensuring compatibility and seamless data exchange requires advanced engineering, specialized expertise, and ongoing maintenance

- Regulatory compliance and spectrum allocation issues further restrict rapid deployment. Ground station operators must adhere to local and international regulations governing satellite communication, data security, and interference management

- For instance, in 2024, operators in Brazil and South Africa reported delays in ground station commissioning due to high installation costs, licensing challenges, and integration hurdles with new LEO satellite networks. These issues impacted service rollouts and limited operational scalability

- Overcoming these challenges will require cost-effective infrastructure, standardized protocols, and collaborative efforts with satellite operators, telecom providers, and regulatory bodies. Focused R&D, modular station designs, and enhanced automation can help unlock the long-term growth potential of the global satellite ground station market while improving operational efficiency and reducing deployment time

Satellite Ground Station Market Scope

The market is segmented on the basis of offering, hardware sub-segment, function, frequency band, orbit, application, platform, and end user.

- By Offering

On the basis of offering, the global satellite ground station market is segmented into Hardware, Software, and Ground Station as a Service (GSaaS). The Hardware segment held the largest market revenue share in 2025, driven by the high demand for robust and reliable ground infrastructure capable of supporting diverse satellite missions. Hardware solutions provide essential components for communication, data reception, and satellite tracking, making them indispensable for both commercial and government applications. These systems are critical for ensuring uninterrupted satellite connectivity and maintaining the integrity of high-speed data transmissions. Increasing satellite launches and growing dependence on satellite networks across industries further strengthen the demand for hardware-based solutions.

The GSaaS segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing adoption of cloud-based solutions and the need for flexible, scalable, and cost-effective ground station services. GSaaS enables operators to access satellite connectivity without the need for heavy upfront investment in physical infrastructure, making it particularly attractive for startups, small enterprises, and emerging space programs. The model supports pay-per-use or subscription-based access, helping reduce operational costs. Rapid growth in LEO satellite constellations and increasing demand for real-time data also boost GSaaS adoption.

- By Hardware Sub-Segment

On the basis of hardware sub-segment, the market is categorized into Antenna Systems, Tracking Equipment, Receivers & Transmitters, Ground Station Terminal, and Others. Antenna Systems held the largest market share in 2025, owing to their critical role in ensuring high-precision signal transmission and reception for various satellite operations. These systems are designed to handle high-frequency bands and large data throughput while minimizing signal loss. Continuous advancements in phased-array antennas and adaptive beamforming technologies further enhance their performance. The integration of antenna systems with automated tracking and control systems provides seamless operations across multiple satellite missions.

The Receivers & Transmitters sub-segment is expected to grow at the highest CAGR during 2026–2033, driven by advancements in high-speed data transmission and the growing requirement for reliable, high-bandwidth communication channels for LEO and MEO satellite constellations. These components enable accurate signal decoding and robust uplink/downlink communication for commercial, government, and defense satellites. The rising adoption of multi-band and software-defined receivers improves operational flexibility. Increasing demand for satellite broadband and IoT applications is also a key driver for growth in this sub-segment.

- By Function

Based on function, the market is segmented into Telemetry, Tracking & Command (TT&C), Data Reception & Processing, Communication & Backhaul, and Network Management & Integration. TT&C held the largest market share in 2025, as it is fundamental for monitoring satellite health and maintaining operational efficiency. This function ensures precise control of satellite trajectories, operational safety, and mission continuity. Ground stations providing TT&C services are critical for both commercial and government satellites. Growing satellite deployment in LEO, MEO, and GEO orbits drives the need for robust TT&C capabilities. Integration with advanced software for anomaly detection and predictive maintenance enhances operational reliability.

Data Reception & Processing is projected to record the fastest growth from 2026 to 2033, driven by the surge in Earth observation missions, scientific research satellites, and high-resolution imaging services that require rapid and accurate processing of large volumes of satellite data. Advanced algorithms for image correction, data compression, and real-time analysis improve the quality of information delivered to end users. The demand for analytics-ready data in applications such as climate monitoring, agriculture, and urban planning is rising. Increasing investments in AI-enabled processing platforms further accelerate growth in this function.

- By Frequency Band

On the basis of frequency band, the market is classified into C Band, Ku Band, Ka Band, S Band/X Band, and Others. The Ka Band segment led the market in 2025 due to its capability to support high-throughput satellite communication and broadband services. Ka Band frequencies offer faster data transfer rates and lower latency compared to traditional bands, making them suitable for next-generation satellite networks. Rising adoption of broadband satellites and high-resolution Earth observation satellites drives market growth. Technological advancements in adaptive modulation and power-efficient transceivers further enhance Ka Band performance.

The Ku Band segment is expected to witness significant growth during 2026–2033, fueled by its widespread use in direct-to-home (DTH) services, VSAT networks, and regional satellite communication networks. Ku Band supports reliable video, voice, and data transmission over long distances. Growth in emerging markets and increasing consumer demand for satellite TV and internet connectivity contribute to its adoption. The band’s compatibility with small and transportable ground stations makes it attractive for commercial operators. Continuous development of dual-band and multi-band systems further strengthens the Ku Band segment.

- By Orbit

Based on orbit, the market is segmented into LEO, MEO, and GEO. GEO satellites dominated the market in 2025 owing to their extensive coverage area and established use in communication and navigation services. GEO orbit allows constant coverage over a fixed region, making it ideal for broadcasting, navigation, and meteorological applications. Large-scale infrastructure and established ground networks support GEO satellite operations. Increasing adoption of hybrid networks combining GEO and non-GEO satellites is enhancing service quality and coverage. GEO satellites remain critical for reliable, long-term global connectivity.

LEO satellites are expected to register the fastest growth from 2026 to 2033, driven by the rise of mega-constellations providing broadband internet and IoT connectivity across remote and underserved regions. LEO satellites offer low-latency communication, high throughput, and scalable deployment advantages. The growth of private satellite operators and increasing demand for global internet coverage accelerate LEO adoption. Miniaturized satellites and cost-efficient launch technologies further support this trend. Integration with GSaaS platforms enhances accessibility for commercial and defense applications.

- By Application

On the basis of application, the market is divided into Communication, Earth Observation, Navigation & Positioning, Military & Intelligence, Scientific Research, and Space Exploration. Communication applications held the largest share in 2025, supported by the growing demand for broadband connectivity and data relay services. Ground stations play a critical role in supporting telecommunication satellites and data networks. Expansion of global internet services, cloud connectivity, and media broadcasting further boost demand. The need for uninterrupted and high-quality data transmission underpins the growth of communication-oriented ground stations.

Earth Observation is projected to witness the highest growth rate over the forecast period, fueled by increasing requirements for climate monitoring, disaster management, agricultural analytics, and urban planning. High-resolution imaging satellites generate massive data volumes that require advanced reception and processing capabilities. Governments, research institutions, and commercial enterprises are increasingly relying on Earth observation data for strategic decision-making. Growing emphasis on environmental sustainability and resource management also drives the market. Integration of AI and machine learning in data analysis enhances the utility of Earth observation applications.

- By Platform

Based on platform, the market is segmented into Fixed, Transportable, and Mobile. Fixed ground stations held the largest share in 2025, as they provide stable, high-performance infrastructure for long-term satellite operations. These stations offer high reliability, robust connectivity, and the ability to handle large volumes of data. Long-term government and commercial satellite programs rely on fixed platforms for continuous monitoring. Advanced automation and remote control capabilities increase operational efficiency. Fixed platforms are also critical for supporting multi-orbit satellite networks and high-throughput communications.

Transportable and Mobile platforms are expected to grow rapidly from 2026 to 2033, driven by the need for deployable ground stations in remote locations, field operations, and defense missions. These stations offer flexibility for temporary setups, rapid deployment, and mission-specific operations. They are particularly useful for disaster response, military exercises, and experimental satellite missions. Compact, lightweight, and energy-efficient designs enhance their usability in challenging environments. Increasing interest in portable GSaaS solutions also supports their adoption.

- By End User

On the basis of end user, the market is categorized into Commercial, Government, and Defense. Government organizations held the largest revenue share in 2025, due to extensive investments in national satellite programs, navigation systems, and scientific research initiatives. Government-backed satellite programs ensure national security, environmental monitoring, and space exploration. Investments in infrastructure, R&D, and advanced ground systems reinforce market dominance. Collaboration with private players and international space agencies further strengthens capabilities. Regulatory support and funding also encourage government-led projects.

The Commercial segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by the expansion of private satellite operators, increasing space startups, and the rising adoption of GSaaS for cost-efficient satellite operations. Commercial users require scalable, flexible, and efficient ground station solutions to manage satellite fleets and data services. Growth in satellite broadband, IoT connectivity, and Earth observation services contributes to market demand. Partnerships with cloud service providers and technological innovations enhance operational efficiency. Rising entrepreneurial activity in space technology fuels commercial adoption.

Satellite Ground Station Market Regional Analysis

- North America dominated the satellite ground station market with the largest revenue share of 38.5% in 2025, driven by extensive government investments, growing commercial satellite deployments, and high adoption of advanced ground infrastructure

- The region’s focus on space programs, satellite broadband initiatives, and defense communication networks fuels demand for reliable ground station solutions

- High technological expertise, supportive regulatory frameworks, and the presence of leading aerospace companies further contribute to market dominance

U.S. Satellite Ground Station Market Insight

The U.S. satellite ground station market captured the largest revenue share in 2025 within North America, driven by rapid expansion of commercial satellite operators and government-funded space missions. Increased deployment of LEO and GEO satellites, coupled with demand for high-speed data reception and cloud-based ground services, supports market growth. The adoption of GSaaS and advanced hardware platforms for telemetry, tracking, and command (TT&C) is gaining traction. Moreover, U.S. operators are increasingly integrating automation, AI-driven analytics, and IoT-enabled solutions to enhance ground station efficiency.

Europe Satellite Ground Station Market Insight

The Europe satellite ground station market is expected to witness the fastest growth rate from 2026 to 2033, driven by strategic investments in Earth observation, navigation systems, and space research programs. Stringent regulations and focus on technological innovation encourage adoption of advanced ground infrastructure. European countries are deploying transportable and mobile ground stations to support scientific missions and defense operations. The integration of GSaaS platforms and high-throughput Ka and Ku band capabilities is further accelerating market growth.

U.K. Satellite Ground Station Market Insight

The U.K. satellite ground station market is expected to witness rapid growth from 2026 to 2033, fueled by increasing commercial satellite launches and government-backed space initiatives. Rising demand for secure and scalable ground station solutions for telemetry, data reception, and satellite communication is driving adoption. The country’s strong satellite manufacturing ecosystem, combined with investments in LEO and GEO satellite networks, supports growth. In addition, the focus on hybrid ground station platforms and cloud-based GSaaS solutions strengthens the market outlook.

Germany Satellite Ground Station Market Insight

The Germany satellite ground station market is projected to witness significant growth from 2026 to 2033, driven by technological advancements in antenna systems, tracking equipment, and receivers/transmitters. The country’s emphasis on precision, automation, and eco-efficient solutions boosts the deployment of fixed and transportable ground stations. Germany’s strategic role in European space programs and private satellite initiatives contributes to market expansion. Integration with IoT devices and AI-enabled data processing platforms further enhances operational efficiency and service reliability.

Asia-Pacific Satellite Ground Station Market Insight

The Asia-Pacific satellite ground station market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing satellite launches, rapid urbanization, and growing commercial space programs in countries such as China, Japan, and India. Government initiatives promoting digital infrastructure and space connectivity support market adoption. The region is also benefiting from cost-efficient manufacturing of ground station hardware, making solutions more accessible. Rising demand for Earth observation, communication, and navigation services further drives market expansion across both commercial and defense applications.

Japan Satellite Ground Station Market Insight

The Japan satellite ground station market is expected to witness strong growth from 2026 to 2033 due to high technological penetration, urbanization, and adoption of advanced satellite networks. The country prioritizes secure and reliable telemetry, tracking, and communication systems for commercial and scientific satellite operations. Integration with high-speed data processing platforms, Ka/Ku band communication systems, and GSaaS offerings fuels market adoption. Japan’s focus on space exploration, smart cities, and IoT-enabled satellite services further supports growth in both fixed and transportable ground stations.

China Satellite Ground Station Market Insight

The China satellite ground station market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid satellite deployment, government investment in space infrastructure, and growing private satellite operators. The country’s expansion of satellite broadband, Earth observation, and navigation programs drives demand for both fixed and mobile ground stations. Affordable hardware solutions and rising GSaaS adoption increase accessibility for commercial users. In addition, China’s strategic focus on high-throughput Ka/Ku band networks and advanced data processing capabilities strengthens its position as a leading market in the region.

Satellite Ground Station Market Share

The Satellite Ground Station industry is primarily led by well-established companies, including:

- SES S.A. (Luxembourg)

- Intelsat S.A. (U.S.)

- Eutelsat Communications (France)

- Telesat (Canada)

- Viasat, Inc. (U.S.)

- Inmarsat Plc (U.K.)

- Gilat Satellite Networks (Israel)

- Comtech Telecommunications Corp. (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Kratos Defense & Security Solutions, Inc. (U.S.)

- Airbus Defence and Space (France)

- General Dynamics Mission Systems, Inc. (U.S.)

- Kongsberg Satellite Services AS (KSAT) (Norway)

- Thales Alenia Space (France)

- CPI Satcom & Antenna Technologies (U.S.)

Latest Developments in Global Satellite Ground Station Market

- In May 2025, the U.S. Space Force awarded a USD 17.6 million contract to Colorado-based defense firms Boecore (operating as Auria) and Sphinx Defense to develop the Joint Antenna Marketplace (JAM), a prototype cloud-based marketplace for antenna resources. This initiative aims to streamline satellite communication procurement and enhance operational flexibility, potentially accelerating adoption of cloud-enabled ground station solutions across defense and commercial sectors

- In May 2025, Telesat announced a partnership to build and manage a comprehensive ground station network valued at up to USD 1 billion, supporting its Lightspeed LEO satellite constellation. The network is expected to improve global connectivity, reduce latency, and strengthen Telesat’s competitive position in the LEO broadband market, driving demand for scalable ground infrastructure

- In July 2025, Kongsberg Satellite Services (KSAT) expanded its collaboration with Amazon Web Services (AWS) by integrating AWS Ground Station capabilities into its commercial offerings. This allows customers to access satellite data faster and more efficiently via cloud infrastructure, enhancing service flexibility and boosting GSaaS adoption in commercial markets

- In July 2024, Dhruva Space, Hyderabad, received authorization from IN-SPACe to offer Ground Station as a Service (GSaaS), enabling commercial clients to access satellite connectivity without investing in physical infrastructure. This move strengthens India’s commercial ground station ecosystem and supports the growth of private satellite operations

- In May 2024, KSAT Inc., a subsidiary of Kongsberg Satellite Services, announced a study with NOAA to evaluate next-generation satellite ground network architectures, including phased array antennas, APIs, virtualization, and data processing enhancements. The research aims to improve network efficiency and reliability, driving innovation in advanced ground station technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.