Global Scientific Instruments Market

Market Size in USD Billion

USD

46.39 Billion

USD

66.98 Billion

2024

2032

USD

46.39 Billion

USD

66.98 Billion

2024

2032

| 2025 - 2032 | |

| USD 46.39 Billion | |

| USD 66.98 Billion | |

| % | |

|

Scientific Instruments Market Size

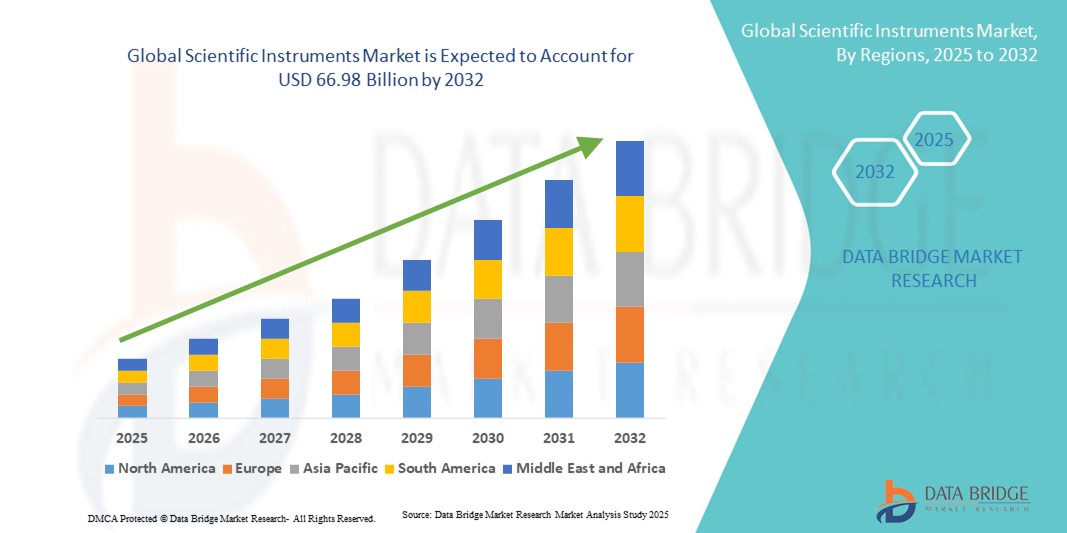

- The global scientific instruments market size was valued at USD 46.39 billion in 2024 and is expected to reach USD 66.98 billion by 2032, at a CAGR of 4.7% during the forecast period

- The market growth is largely fueled by increasing research and development activities across pharmaceuticals, biotechnology, and material sciences, coupled with advancements in precision instrumentation and analytical technologies

- Furthermore, rising demand for accurate measurement, testing, and monitoring solutions in laboratories, healthcare, and industrial applications is establishing scientific instruments as essential tools for innovation and quality control. These converging factors are accelerating the adoption of advanced scientific instruments, thereby significantly boosting the industry's growth

Scientific Instruments Market Analysis

- Scientific instruments, encompassing devices such as microscopes, spectrometers, and X-ray diffraction systems, are integral to research, diagnostics, and quality control across industries such as pharmaceuticals, biotechnology, and environmental science. Their precision and reliability make them essential in both laboratory and field applications

- The rising demand for scientific instruments is primarily driven by increased research and development activities, technological advancements in instrumentation, and a growing emphasis on quality control and regulatory compliance in various sectors

- North America dominated the scientific instruments market with the largest revenue share of 34.5% in 2024, characterized by robust research infrastructure, substantial investments in healthcare and biotechnology, and the presence of leading industry players. The U.S. experienced significant growth in the adoption of analytical instruments, particularly in pharmaceutical and environmental applications

- Asia-Pacific is expected to be the fastest-growing region in the scientific instruments market during the forecast period due to expanding research activities, increasing industrialization, and rising investments in healthcare and education sectors

- The benchtop modality dominated the scientific instruments market with a market share of 45.5% in 2024, driven by its widespread use in laboratory settings due to stability, precision, and ease of use

Report Scope and Scientific Instruments Market Segmentation

|

Attributes |

Scientific Instruments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Scientific Instruments Market Trends

Adoption of Automation and AI in Laboratory Instruments

- A significant and accelerating trend in the global scientific instruments market is the integration of automation and artificial intelligence (AI) in laboratory and analytical equipment, enhancing precision, throughput, and data analysis capabilities

- For instance, automated liquid handling workstations and robotic sample preparation systems allow laboratories to perform complex assays with minimal human intervention, reducing errors and increasing efficiency

- AI-enabled analytical instruments can predict maintenance needs, optimize workflows, and provide intelligent insights from complex datasets. For instance, some high-end mass spectrometers use AI algorithms to detect anomalies and suggest calibration adjustments in real-time

- The seamless integration of automated and AI-driven instruments with laboratory information management systems (LIMS) facilitates centralized data management, enabling researchers to monitor experiments, track samples, and generate reports from a unified interface

- This trend towards more intelligent, automated, and interconnected laboratory solutions is reshaping research and industrial expectations for scientific instruments. Consequently, companies such as Thermo Fisher Scientific are developing AI-enabled instruments with predictive maintenance and workflow optimization capabilities

- The demand for scientific instruments that offer automation and AI-assisted functionalities is growing rapidly across research, clinical, and industrial laboratories, as organizations increasingly prioritize efficiency, accuracy, and comprehensive data insights

Scientific Instruments Market Dynamics

Driver

Rising R&D Investments and Industrial Quality Control Needs

- The increasing investments in research and development, biotechnology, pharmaceuticals, and industrial quality control are a significant driver of growth for scientific instruments

- For instance, in March 2024, Agilent Technologies announced expansion of its analytical instrument solutions for pharmaceutical quality control, enhancing precision and throughput in laboratory workflows

- Organizations are seeking high-precision instruments for testing, monitoring, and analysis to ensure regulatory compliance and product quality, driving demand for advanced scientific equipment

- Furthermore, the growth of clinical research, environmental monitoring, and material sciences is expanding the need for specialized scientific instruments capable of high-throughput, reliable analysis

- The convenience, accuracy, and efficiency offered by modern scientific instruments for laboratory and industrial operations, coupled with integrated software for data analysis, are key factors driving adoption. The trend towards automation and smart laboratory setups further accelerates market growth

Restraint/Challenge

High Costs and Technical Complexity

- The high initial cost of advanced scientific instruments and their technical complexity pose significant challenges to broader market adoption, particularly in developing regions

- For instance, specialized spectroscopy or X-ray diffraction instruments require trained personnel and ongoing maintenance, limiting adoption among smaller laboratories or budget-conscious organizations

- Addressing these challenges through cost-effective instrument variants, simplified user interfaces, and training programs is crucial for market expansion. Companies such as Bruker and Shimadzu provide service and training packages to ensure efficient use

- Furthermore, compliance with stringent regulatory standards and quality certifications adds to operational and financial burdens for manufacturers and end-users, acting as a market restraint

- While prices are gradually decreasing for basic analytical instruments, premium features such as high-resolution imaging, AI integration, or robotic automation still carry a higher cost, which may restrict adoption among smaller research institutions

- Overcoming these challenges through product innovation, enhanced training, and localized support will be vital for sustained market growth in the scientific instruments sector

Scientific Instruments Market Scope

The market is segmented on the basis of product, modality, application, end user, and distribution channel.

- By Product

On the basis of product, the scientific instruments market is segmented into microscopes, spectrometers, X-ray diffraction, thermal analyzers, optical measurement systems, and others. The thermal analyzers segment dominated the market with the largest market revenue share of 58.29% in 2023, driven by their critical role in chemical, pharmaceutical, and environmental testing. Laboratories and industrial facilities prioritize analyzers for their high precision, reliability, and ability to deliver consistent results. Spectrometers, chromatographs, and other analytical instruments are widely used across research and manufacturing workflows. The dominance is further supported by increasing R&D activities in pharmaceuticals and biotechnology. Continuous technological advancements, coupled with growing demand for quality control and regulatory compliance, strengthen the segment’s market position.

The microscopes segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by technological advancements such as super-resolution and electron microscopy. Microscopes are increasingly adopted in life sciences, nanotechnology, and material research for detailed visualization. Academic and research institutions use advanced microscopy for experiments, diagnostics, and innovative studies. Portable and digital microscopy solutions enable usage outside traditional labs, enhancing accessibility. Rising focus on cellular-level research and imaging precision further accelerates adoption. Increased government and private funding for research also drives segment growth.

- By Modality

On the basis of modality, the scientific instruments market is segmented into handheld, benchtop, portable, and others. The benchtop segment dominated the market with a share of 45.5% in 2024, driven by its stability, accuracy, and suitability for laboratory workflows. Benchtop instruments are preferred for complex analyses, offering reliable and consistent performance. Their design allows integration into routine laboratory operations, making them essential for research, clinical, and industrial applications. They are widely used in pharmaceutical, biotech, and environmental laboratories. Ease of calibration, maintenance, and durability further enhances adoption. The growing need for precise measurements and data reproducibility strengthens this segment.

The portable segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by the demand for on-site testing and field applications. Portable instruments are compact, battery-operated, and suitable for remote locations. They enable researchers and technicians to perform accurate measurements outside the laboratory. Environmental monitoring, point-of-care diagnostics, and industrial testing are driving growth. Portable solutions reduce dependency on stationary lab equipment, increasing flexibility. Expanding applications in emerging markets contribute to rapid adoption.

- By Application

On the basis of application, the scientific instruments market is segmented into clinical diagnostics and research. The research segment dominated the market with a share of 42.90% in 2023, driven by rising investments in scientific research across pharmaceuticals, biotechnology, and material sciences. Research laboratories require high-precision instruments for experiments, testing, and data analysis. Academic and industrial research institutions continue to adopt advanced instruments to support innovation. Government and private funding initiatives strengthen market dominance. The increasing focus on product development and experimental studies sustains demand. Research instruments remain central to scientific advancements worldwide.

The clinical diagnostics segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by rising healthcare needs and growing adoption of advanced testing technologies. Hospitals and laboratories are investing in instruments that enhance diagnostic accuracy. Personalized medicine, preventive healthcare, and early disease detection drive demand. Integration with laboratory information management systems (LIMS) improves operational efficiency. Expansion of diagnostic centers globally further contributes to rapid growth. Rising awareness of quality healthcare strengthens adoption of clinical diagnostic instruments.

- By End User

On the basis of end user, the scientific instruments market is segmented into hospitals, laboratories, healthcare companies, academic and research institutes, and others. The hospitals and clinics segment dominated the market with a share of 31.02% in 2023, driven by the need for accurate diagnostics, patient monitoring, and therapeutic interventions. Hospitals rely on scientific instruments for laboratory testing, imaging, and clinical analysis. The increasing prevalence of chronic diseases and expansion of healthcare infrastructure support segment growth. High adoption of advanced instruments enhances clinical efficiency. Government healthcare initiatives and funding further bolster dominance. Hospitals remain major purchasers of high-end scientific instruments globally.

The academic and research institutes segment is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing investments in education, R&D, and scientific discovery. Institutes require instruments for experiments, teaching, and innovation. Laboratories in universities and research centers adopt automated and AI-enabled instruments. Funding for research and innovation supports infrastructure development. The growing need for advanced training and experimental studies accelerates adoption. Collaborative research initiatives further enhance growth potential.

- By Distribution Channel

On the basis of distribution channel, the scientific instruments market is segmented into direct tender, retail sales, online sales, and others. The direct tender segment dominated the market with a share of 58.3% in North America in 2024, driven by institutional and government procurement practices. Direct tender ensures standardized equipment, warranties, and regulatory compliance. Hospitals, universities, and research centers prefer bulk purchases via this channel. Institutional contracts and long-term service agreements reinforce dominance. Standardized procurement reduces operational and compliance risks. Direct tender remains a reliable choice for large-scale buyers globally.

The online sales segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by the growing trend of digital procurement and e-commerce platforms. Online platforms enable easy comparison of specifications, pricing, and reviews. Small laboratories, research institutes, and individual researchers increasingly adopt online purchasing. Digital procurement allows faster delivery and improved customer experience. Rising familiarity with online marketplaces accelerates adoption. Cost efficiency and accessibility contribute to rapid growth in this segment.

Scientific Instruments Market Regional Analysis

- North America dominated the scientific instruments market with the largest revenue share of 34.5% in 2024, characterized by robust research infrastructure, substantial investments in healthcare and biotechnology, and the presence of leading industry players

- Organizations in the region prioritize precision, reliability, and advanced capabilities in laboratory and analytical instruments. The adoption of AI-enabled and automated instruments enhances efficiency and accuracy in research and industrial applications

- This widespread adoption is further supported by a strong research infrastructure, high government and private funding, and the presence of key market players such as Thermo Fisher Scientific, Agilent Technologies, and Bruker

U.S. Scientific Instruments Market Insight

The U.S. scientific instruments market captured the largest revenue share of approximately 40% in 2024, fueled by substantial investments in R&D, healthcare, and industrial quality control. Laboratories and research institutions increasingly prioritize precision, automation, and AI-enabled instrumentation. The growing adoption of high-throughput analytical instruments and advanced imaging systems is driving market expansion. Universities, pharmaceutical companies, and biotechnology firms are key end-users, leveraging instruments for innovation and product development. Integration with laboratory information management systems (LIMS) further enhances operational efficiency. Moreover, strong government and private funding initiatives continue to support the adoption of advanced scientific instruments.

Europe Scientific Instruments Market Insight

The Europe scientific instruments market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by well-established research infrastructure and stringent regulatory standards. High adoption rates in academic institutions, pharmaceutical laboratories, and industrial testing facilities support market growth. Increasing urbanization and the expansion of research programs foster the deployment of advanced scientific instruments. European consumers and institutions prioritize accuracy, reliability, and compliance in laboratory equipment. The market is experiencing significant growth across both industrial and academic applications. Innovation-focused policies and funding initiatives in countries such as Germany and France further accelerate adoption.

U.K. Scientific Instruments Market Insight

The U.K. scientific instruments market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong research and innovation initiatives and a growing focus on life sciences and biotechnology. Academic institutions, hospitals, and laboratories are increasingly investing in high-precision instruments. The trend of automation, data-driven analysis, and AI integration in laboratories supports faster adoption. Concerns regarding data accuracy and experimental reproducibility encourage investment in reliable instruments. The U.K.’s robust research infrastructure and growing e-commerce availability for laboratory instruments further stimulate market growth. Government grants and R&D funding initiatives continue to promote adoption across the country.

Germany Scientific Instruments Market Insight

The Germany scientific instruments market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced industrial and research infrastructure. Emphasis on technological innovation and precision in manufacturing and scientific research drives adoption. Laboratories, universities, and healthcare institutions increasingly rely on automated and AI-enabled instruments for analysis and quality control. Germany’s sustainability-focused policies encourage the use of energy-efficient and eco-conscious scientific equipment. The integration of instruments with laboratory networks and data management systems is becoming more prevalent. Demand for secure, high-precision instruments aligns with local industry and regulatory standards.

Asia-Pacific Scientific Instruments Market Insight

The Asia-Pacific scientific instruments market is poised to grow at the fastest CAGR during the forecast period, driven by rising investments in R&D, urbanization, and industrial expansion in countries such as China, India, and Japan. Growing adoption of advanced laboratory equipment and automated instruments supports research, diagnostics, and industrial testing. Government initiatives promoting digitalization and innovation accelerate market penetration. The availability of cost-effective instruments from local manufacturers enhances accessibility across research and healthcare institutions. Rising focus on quality control and regulatory compliance in manufacturing industries further propels adoption. Increasing academic and industrial collaborations across APAC contribute to rapid growth.

Japan Scientific Instruments Market Insight

The Japan scientific instruments market is gaining momentum due to high technological advancement, rapid urbanization, and strong focus on research and innovation. Academic institutions, hospitals, and manufacturing laboratories prioritize high-precision, automated instruments. Integration with IoT and AI-based analytics enhances efficiency and operational accuracy. Japan’s aging population also increases demand for easy-to-use and reliable diagnostic instruments. Adoption of connected laboratory systems and smart instruments in research centers drives market growth. Government initiatives and private R&D funding further support rapid expansion in the Japanese market.

India Scientific Instruments Market Insight

The India scientific instruments market accounted for a growing market revenue share in Asia-Pacific in 2024, attributed to rising R&D investments, rapid urbanization, and a strong academic and industrial research base. India is emerging as a key hub for life sciences, pharmaceuticals, and industrial research, increasing demand for advanced instruments. The availability of affordable scientific instruments from domestic manufacturers enhances accessibility. Government initiatives supporting smart laboratories, innovation, and quality testing accelerate market growth. Hospitals, academic institutions, and research centers increasingly adopt automated and high-precision instruments. Expanding collaboration with international research organizations further propels market expansion.

Scientific Instruments Market Share

The scientific instruments industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- KEYENCE CORPORATION (Japan)

- Agilent Technologies, Inc. (U.S.)

- Danaher Corporation (U.S.)

- AMETEK, Inc. (U.S.)

- PerkinElmer (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Bruker (U.S.)

- Sartorius AG (Germany)

- Illumina, Inc. (U.S.)

- Shimadzu Corporation (Japan)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Eppendorf AG (Germany)

- Waters Corporation (U.S.)

- METTLER TOLEDO (Switzerland)

- Tecan Group Ltd (Switzerland)

- Fortive (U.S.)

- Coherent Corp. (U.S.)

- Cognex Corporation (U.S.)

- Sequoia Scientific, Inc. (U.S.)

What are the Recent Developments in Global Scientific Instruments Market?

- In June 2025, Thermo Fisher Scientific introduced the Orbitrap Astral Zoom and Orbitrap Excedion Pro mass spectrometers at the American Society for Mass Spectrometry (ASMS) annual conference. These instruments offer enhanced speed and sensitivity, setting a new benchmark for high-resolution, accurate mass spectrometry in biopharma applications and omics research

- In May 2025, Agilent Technologies unveiled the InfinityLab Pro iQ Series at the American Society for Mass Spectrometry (ASMS) conference. This next-generation LC-mass detection system delivers exceptional performance and sensitivity, making it ideal for monitoring complex biomolecules and detecting impurities, thereby enhancing analytical capabilities in laboratories

- In April 2025, Bruker Corporation launched the Ascend Evo 700 and 800 MHz 54mm magnets, which are more compact, lighter, and consume significantly less helium than previous high-field magnets. These advancements in NMR technology aim to improve operational efficiency and reduce costs in scientific research

- In March 2025, PerkinElmer introduced the QSight 500 LC/MS/MS System at the Pittcon conference. This system is designed to handle the most challenging sample matrices with unparalleled reliability and cost efficiency, making it suitable for a wide range of analytical applications

- In March 2025, HORIBA launched the Veloci BioPharma Analyzer, a unique A-TEEM spectroscopy solution for the biopharma and pharma industries. This instrument combines the selectivity of chromatography with the advantages of optical spectroscopy, offering a powerful tool for analyzing complex biological samples

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.