Global Sclerotherapy Market

Market Size in USD Billion

USD

1.28 Billion

USD

2.17 Billion

2025

2033

USD

1.28 Billion

USD

2.17 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.28 Billion | |

| USD 2.17 Billion | |

| % | |

|

Sclerotherapy Market Size

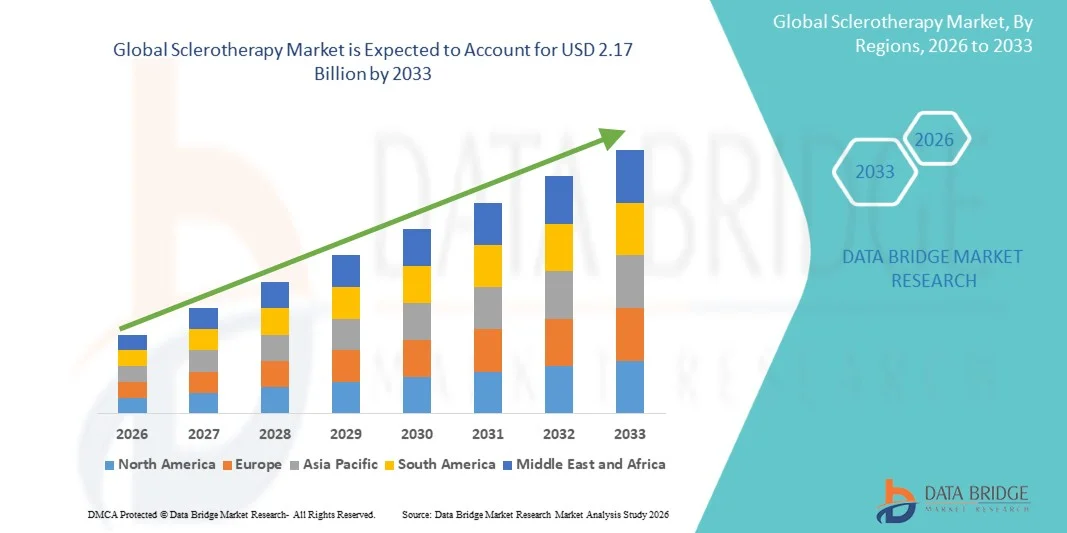

- The global sclerotherapy market size was valued at USD 1.28 billion in 2025and is expected to reach USD 2.17 billion by 2033, at a CAGR of 6.85% during the forecast period

- The market growth is largely fueled by the increasing prevalence of varicose veins, spider veins, and chronic venous disorders, along with growing awareness regarding minimally invasive cosmetic and therapeutic procedures, leading to greater adoption of sclerotherapy treatments in healthcare and aesthetic settings

- Furthermore, rising consumer demand for safe, effective, and non-surgical vein treatment options, coupled with advancements in sclerosant formulations and outpatient treatment procedures, is establishing sclerotherapy as a preferred solution for venous disorders. These converging factors are accelerating the uptake of Sclerotherapy solutions, thereby significantly boosting the market growth

Sclerotherapy Market Analysis

- Sclerotherapy, a minimally invasive procedure used to treat varicose veins, spider veins, and other venous disorders through injection of sclerosant solutions, is becoming increasingly vital in modern vascular and aesthetic care due to its effectiveness, quick recovery time, and outpatient convenience

- The escalating demand for sclerotherapy is primarily fueled by the rising prevalence of chronic venous diseases, growing preference for non-surgical cosmetic procedures, and increasing awareness regarding early treatment of vein disorders, along with advancements in foam and liquid sclerosant formulations

- North America dominated the Sclerotherapy market with the largest revenue share of approximately 42.1% in 2025, characterized by advanced healthcare infrastructure, high demand for cosmetic vein treatments, and strong presence of specialized vascular clinics, with the U.S. leading in procedure volumes and adoption of innovative treatment techniques

- Asia-Pacific is expected to be the fastest growing region in the Sclerotherapy market during the forecast period due to rising healthcare awareness, growing disposable incomes, increasing demand for aesthetic procedures, and expanding access to minimally invasive vein treatment services

- The Foam segment dominated the largest market revenue share of 49.2% in 2025, driven by superior efficacy in treating larger veins and improved contact with vessel walls

Report Scope and Sclerotherapy Market Segmentation

|

Attributes |

Sclerotherapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Boston Scientific Corporation (U.S.) · Medtronic plc (Ireland) · Merz Pharma GmbH & Co. KGaA (Germany) · BTG International Ltd. (U.K.) · Bausch Health Companies Inc. (Canada) · Pfizer Inc. (U.S.) · Cook Medical LLC (U.S.) · Teleflex Incorporated (U.S.) · Terumo Corporation (Japan) · AngioDynamics, Inc. (U.S.) · Chemische Fabrik Kreussler & Co. GmbH (Germany) · Troikaa Pharmaceuticals Ltd. (India) · Vascular Solutions, Inc. (U.S.) · LGM Pharma (U.S.) · Eifelm GmbH (Germany) · F Care Systems NV (Belgium) · Croma Pharma GmbH (Austria) · Candela Corporation (U.S.) · Veinlite LLC (U.S.) |

|

Market Opportunities |

· Growing Demand for Minimally Invasive Cosmetic and Vein Treatments · Expansion of Advanced Foam and Ultrasound-Guided Procedures |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Sclerotherapy Market Trends

“Enhanced Preference for Minimally Invasive and Outpatient Procedures”

- A significant and accelerating trend in the global sclerotherapy market is the rising preference for minimally invasive procedures that offer effective treatment with limited downtime and improved patient comfort. Patients increasingly seek vein treatment options that avoid surgical intervention while delivering visible cosmetic and therapeutic outcomes

- For instance, sclerotherapy is widely adopted for the treatment of spider veins and small varicose veins because it can be performed in outpatient clinics without the need for hospitalization or general anesthesia. This convenience has made it a preferred option among working professionals and aging populations

- Continuous improvements in sclerosant formulations, injection precision, and ultrasound-guided techniques are enhancing treatment outcomes and expanding the use of sclerotherapy for larger and deeper veins. These advancements are improving safety profiles while reducing recurrence rates

- The growing focus on aesthetic appearance and skin wellness is also contributing to higher procedure volumes, especially among middle-aged consumers seeking cosmetic vein correction

- This trend toward safer, faster, and cosmetically favorable treatment options is reshaping patient expectations and encouraging providers to expand vein care services

- The demand for sclerotherapy procedures is growing steadily across hospitals, dermatology clinics, and specialized vein treatment centers as awareness of non-surgical vein therapies increases

Sclerotherapy Market Dynamics

Driver

“Growing Need Due to Rising Incidence of Venous Disorders and Aging Population”

- The increasing prevalence of chronic venous insufficiency, spider veins, varicose veins, and related vascular conditions is a major driver for the growth of the sclerotherapy market

- For instance, according to healthcare studies, varicose veins affect a substantial portion of adults globally, particularly women and elderly individuals, creating strong demand for minimally invasive treatment procedures such as sclerotherapy

- Sedentary lifestyles, obesity, prolonged standing occupations, and hormonal changes are also contributing to a higher number of patients affected by venous diseases

- Sclerotherapy offers a cost-effective and clinically proven treatment method, making it a preferred first-line option for many superficial vein conditions

- The expanding availability of vein treatment clinics and growing awareness regarding early diagnosis are further propelling market demand across both developed and emerging economies

Restraint/Challenge

“Risk of Side Effects and Limited Effectiveness for Severe Cases”

- Despite its widespread use, concerns regarding side effects such as skin discoloration, swelling, allergic reactions, and temporary discomfort may limit adoption among some patients

- For instance, some patients undergoing sclerotherapy may require multiple follow-up sessions due to incomplete vein closure or recurrence, while others may prefer laser-based alternatives because of fear of injections or pigmentation risks

- In certain severe or complex venous cases, sclerotherapy may be less effective than surgical or endovenous laser procedures, restricting its use for advanced disease stages

- Multiple treatment sessions are often required to achieve desired results, which can increase overall treatment costs and reduce patient convenience

- In developing regions, limited access to trained specialists and lack of awareness regarding modern vein treatment options may further restrain market penetration

- Overcoming these challenges through improved sclerosant agents, better patient selection, practitioner training, and broader education on treatment benefits will be vital for sustained market growth

Sclerotherapy Market Scope

The market is segmented on the basis of product, type, and application.

- By Product

On the basis of product, the Sclerotherapy market is segmented into Detergents, Osmotic Agents, and Chemical Irritants. The Detergents segment dominated the largest market revenue share of 46.8% in 2025, driven by its widespread clinical use, high efficacy, and favorable safety profile in treating varicose and spider veins. Detergent sclerosants such as polidocanol and sodium tetradecyl sulfate are commonly preferred due to their ability to damage vein endothelium effectively while minimizing patient discomfort. Increasing prevalence of chronic venous disorders is significantly supporting segment demand. Physicians favor detergent agents because they can be used in both liquid and foam formulations, enhancing treatment flexibility. Rising awareness regarding minimally invasive cosmetic procedures is further boosting adoption. Strong demand from outpatient vascular clinics is contributing to revenue growth. North America leads the segment due to higher treatment volumes and strong reimbursement systems. Europe also shows steady expansion with increasing aesthetic procedures. Continuous product innovation and regulatory approvals are improving market penetration. Growing elderly population prone to venous insufficiency is another major growth factor. Overall, this segment remains dominant due to proven effectiveness and broad clinical acceptance.

The Osmotic Agents segment is expected to witness the fastest CAGR of 14.9% from 2026 to 2033, driven by rising preference for cost-effective and accessible treatment alternatives. Osmotic agents such as hypertonic saline are increasingly used in smaller vein procedures and cosmetic indications. Their lower acquisition cost makes them attractive in price-sensitive markets. Increasing number of vein treatment centers in emerging economies is supporting adoption. Healthcare providers are using these agents for patients requiring economical solutions. Rising awareness of non-surgical vein management is accelerating demand. Technological advancements in injection techniques are improving treatment outcomes. Expanding medical tourism for aesthetic procedures is also contributing to growth. Asia-Pacific is expected to witness strong uptake due to expanding dermatology clinics. Physicians are increasingly combining osmotic agents with adjunctive therapies. Growing demand for outpatient procedures is boosting procedural volume. Overall, this segment is growing rapidly due to affordability and expanding availability.

- By Type

On the basis of type, the Sclerotherapy market is segmented into Ultrasound, Liquid, and Foam. The Foam segment dominated the largest market revenue share of 49.2% in 2025, driven by superior efficacy in treating larger veins and improved contact with vessel walls. Foam sclerotherapy is widely preferred because the foam displaces blood effectively, allowing better sclerosant action and enhanced treatment outcomes. Increasing adoption for varicose vein treatment is supporting strong market growth. Physicians prefer foam procedures due to reduced dosage requirements and improved precision. Growing awareness of minimally invasive venous treatments is increasing patient demand. Hospitals and specialty clinics are expanding foam therapy offerings due to faster recovery benefits. Technological advancements in foam preparation techniques are improving consistency and safety. North America remains a key market due to higher awareness and advanced vascular care infrastructure. Europe is also witnessing rising adoption through cosmetic and medical applications. Increasing geriatric population with venous disorders further supports segment demand. Overall, foam sclerotherapy dominates due to high effectiveness and broad clinical usage.

The Ultrasound segment is expected to witness the fastest CAGR of 15.6% from 2026 to 2033, driven by increasing use of image-guided procedures for deeper and complex veins. Ultrasound-guided sclerotherapy improves treatment accuracy and minimizes procedural complications. Growing demand for precision-based vascular interventions is accelerating adoption. Physicians increasingly rely on ultrasound for recurrent varicose vein cases and hidden vein networks. Rising healthcare investments in diagnostic imaging systems are supporting market growth. Outpatient clinics are expanding ultrasound-assisted treatment capabilities. Increasing awareness among patients regarding safer procedures is also boosting demand. Emerging markets are witnessing higher installation of portable ultrasound systems. Favorable clinical outcomes and lower recurrence rates are attracting practitioners. Integration of AI-assisted imaging tools may further strengthen segment growth. Expanding training programs for specialists are improving adoption rates. Overall, this segment is expected to grow rapidly due to superior visualization and treatment precision.

- By Application

On the basis of application, the Sclerotherapy market is segmented into Venous Disease, Gastrointestinal Bleeding, Bronchopleural Fistula, Cystic Disease, and Systemic Diseases. The Venous Disease segment accounted for the largest market revenue share of 57.4% in 2025, driven by the high global prevalence of varicose veins, spider veins, and chronic venous insufficiency. Sclerotherapy is widely recognized as a first-line minimally invasive treatment for cosmetic and therapeutic vein conditions. Rising sedentary lifestyles and obesity rates are contributing to growing venous disease incidence. Increasing demand for aesthetic leg vein correction is further boosting procedures. Hospitals and vein clinics are increasingly offering same-day treatment services. Growing female patient population seeking cosmetic vein treatment also supports demand. North America leads due to high awareness and insurance coverage for select conditions. Europe follows with strong adoption in vascular medicine centers. Technological advancements in sclerosants and delivery systems are improving outcomes. Expanding outpatient care models are increasing accessibility. Overall, venous disease remains the leading application area due to large patient volume and recurring treatment demand.

The Gastrointestinal Bleeding segment is expected to witness the fastest CAGR of 13.8% from 2026 to 2033, driven by increasing use of sclerosants in endoscopic management of bleeding varices and vascular lesions. Rising incidence of liver cirrhosis and portal hypertension is increasing demand for emergency treatment solutions. Sclerotherapy remains an important option where advanced alternatives are limited or unavailable. Hospitals are strengthening endoscopy units to manage gastrointestinal bleeding cases effectively. Increasing healthcare access in developing countries is supporting adoption. Physicians prefer minimally invasive interventions that reduce surgical risk. Growing elderly population with gastrointestinal complications is further driving need. Technological advances in endoscopic devices are improving procedural success rates. Asia-Pacific is expected to witness strong growth due to rising liver disease burden. Training programs for gastroenterologists are enhancing treatment availability. Demand for rapid hemostatic solutions is increasing globally. Overall, this segment is expanding steadily due to urgent care needs and broader endoscopy adoption.

Sclerotherapy Market Regional Analysis

- North America dominated the sclerotherapy market with the largest revenue share of approximately 42.1% in 2025, characterized by advanced healthcare infrastructure, high demand for cosmetic vein treatments, and a strong presence of specialized vascular clinics

- The region benefits from increasing awareness regarding venous disorders, strong preference for minimally invasive aesthetic procedures, and broad availability of outpatient treatment centers. The U.S. leads the region in procedure volumes and adoption of innovative treatment techniques

- Rising prevalence of varicose veins and spider veins, growing aging population, and increasing focus on cosmetic appearance are major factors driving market growth across North America. Technological advancements in injectable sclerosants and image-guided treatment methods are further supporting market expansion.

U.S. Sclerotherapy Market Insight

The U.S. sclerotherapy market captured the largest revenue share within North America in 2025, driven by high demand for cosmetic vein procedures and strong availability of specialized vascular and dermatology clinics. Increasing awareness of minimally invasive treatments, coupled with growing preference for outpatient cosmetic procedures, is boosting market growth. In addition, rising cases of chronic venous insufficiency are supporting long-term demand.

Europe Sclerotherapy Market Insight

The Europe sclerotherapy market is projected to expand at a substantial CAGR during the forecast period, supported by increasing prevalence of venous disorders and growing adoption of minimally invasive treatment options. Strong healthcare systems, expanding aesthetic medicine sector, and rising patient awareness regarding vein health are contributing to regional market growth.

U.K. Sclerotherapy Market Insight

The U.K. sclerotherapy market is anticipated to grow at a noteworthy CAGR, driven by increasing demand for cosmetic and therapeutic vein treatment procedures. Growing availability of private aesthetic clinics and rising awareness about varicose vein management are encouraging treatment adoption. In addition, demand for non-surgical outpatient procedures is supporting market expansion.

Germany Sclerotherapy Market Insight

The Germany Sclerotherapy market is expected to expand at a considerable CAGR, fueled by advanced healthcare infrastructure and increasing demand for precision vein treatment services. Germany’s strong network of specialty clinics and emphasis on minimally invasive care are promoting adoption of sclerotherapy procedures. Rising aging population is further contributing to market growth.

Asia-Pacific Sclerotherapy Market Insight

The Asia-Pacific sclerotherapy market is poised to grow at the fastest CAGR during the forecast period due to rising healthcare awareness, growing disposable incomes, increasing demand for aesthetic procedures, and expanding access to minimally invasive vein treatment services. Rapid urbanization and improving healthcare infrastructure are also accelerating adoption across the region.

Japan Sclerotherapy Market Insight

The Japan sclerotherapy market is gaining momentum due to strong healthcare standards, increasing aging population, and growing demand for minimally invasive cosmetic procedures. Rising awareness of venous health and expanding adoption of outpatient treatment techniques are supporting market growth. In addition, demand for effective and quick recovery procedures is increasing steadily.

China Sclerotherapy Market Insight

The China sclerotherapy market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rising disposable incomes, growing aesthetic consciousness, and expanding healthcare infrastructure. Increasing demand for cosmetic vein treatments and wider access to private specialty clinics are key factors driving market growth. Furthermore, rapid urbanization and healthcare modernization continue to support adoption in China.

Sclerotherapy Market Share

The Sclerotherapy industry is primarily led by well-established companies, including:

- Boston Scientific Corporation (U.S.)

- Medtronic plc (Ireland)

- Merz Pharma GmbH & Co. KGaA (Germany)

- BTG International Ltd. (U.K.)

- Bausch Health Companies Inc. (Canada)

- Pfizer Inc. (U.S.)

- Cook Medical LLC (U.S.)

- Teleflex Incorporated (U.S.)

- Terumo Corporation (Japan)

- AngioDynamics, Inc. (U.S.)

- Chemische Fabrik Kreussler & Co. GmbH (Germany)

- Troikaa Pharmaceuticals Ltd. (India)

- Vascular Solutions, Inc. (U.S.)

- LGM Pharma (U.S.)

- Eifelm GmbH (Germany)

- F Care Systems NV (Belgium)

- Croma Pharma GmbH (Austria)

- Candela Corporation (U.S.)

- Veinlite LLC (U.S.)

Latest Developments in Global Sclerotherapy Market

- In January 2021, Merz Aesthetics continued expansion of its Asclera (polidocanol injection) portfolio across international markets for treatment of uncomplicated spider veins and reticular veins. The product’s growing adoption supported minimally invasive cosmetic and therapeutic vein treatment procedures worldwide

- In June 2021, physicians and vascular clinics increasingly adopted ultrasound-guided foam sclerotherapy for chronic venous insufficiency and varicose veins, driven by improved treatment precision, faster recovery time, and reduced need for surgical intervention

- In March 2022, BTG International (Boston Scientific) expanded utilization of Varithena (polidocanol endovenous microfoam) in outpatient vascular centers, supporting treatment of incompetent great saphenous veins and associated varicosities with minimally invasive procedures

- In September 2022, healthcare providers reported rising preference for foam sclerotherapy over liquid sclerotherapy due to improved vein wall contact, higher occlusion effectiveness, and broader use in larger varicose vein treatments

- In April 2023, vascular treatment centers globally expanded combination therapies integrating sclerotherapy with endovenous laser and radiofrequency ablation, designed to improve outcomes in complex venous disease cases. This development highlighted the growing role of multimodal vein treatment strategies

- In October 2023, Boston Scientific advanced development activities around its Varithena microfoam platform, focusing on improved venous occlusion outcomes and reduced post-procedural inflammation for chronic venous disease management

- In February 2024, Merz Aesthetics expanded Asclera and polidocanol-based sclerosant offerings into additional emerging markets across Asia and Latin America, addressing growing demand for aesthetic and therapeutic vein care solutions

- In May 2024, outpatient vein clinics and ambulatory centers accelerated adoption of office-based sclerotherapy procedures, supported by rising patient demand for minimally invasive cosmetic treatment of spider veins and reticular veins

- In January 2025, industry-wide developments highlighted increasing use of single-session foam sclerotherapy protocols designed to reduce repeat visits and improve patient convenience in venous disease treatment pathways

- In August 2025, continued innovation in the sclerotherapy market focused on improved sclerosant formulations, ultrasound-guided delivery systems, and combination treatment approaches, supporting enhanced efficacy and faster recovery in varicose vein management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.