Global Sea Liner Compounds Market

Market Size in USD Billion

USD

18.19 Billion

USD

32.19 Billion

2025

2033

USD

18.19 Billion

USD

32.19 Billion

2025

2033

| 2026 - 2033 | |

| USD 18.19 Billion | |

| USD 32.19 Billion | |

| % | |

|

Sea Liner Compounds Market Overview

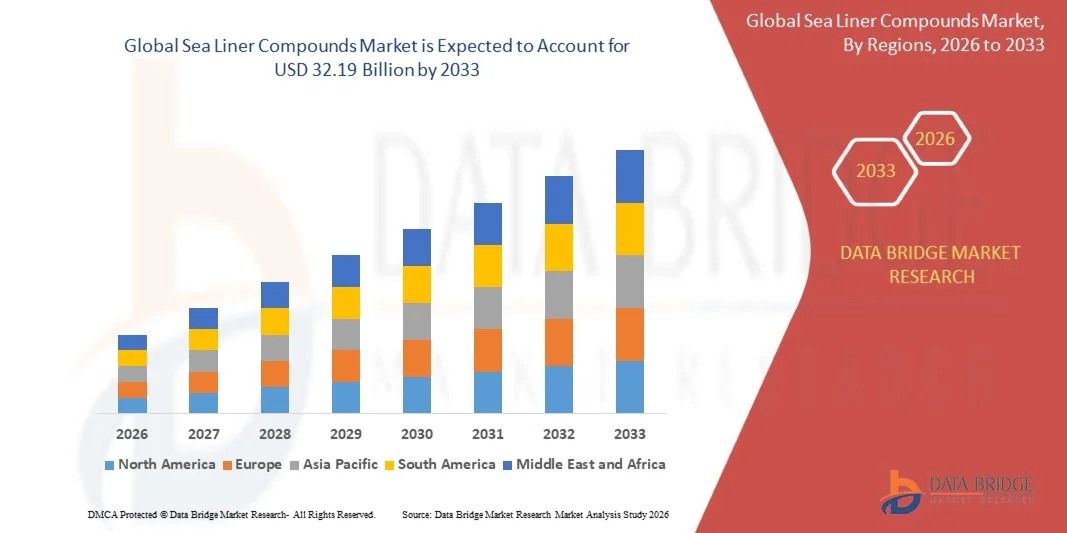

The Sea Liner Compounds Market was valued at USD 18.19 billion in 2025 and is projected to reach USD 32.19 billion by 2033, growing at a CAGR of 7.40% from 2026 to 2033. The market is experiencing steady growth driven by increasing global maritime trade activities, rising demand for durable and corrosion-resistant marine materials, and growing investments in commercial shipping, offshore infrastructure, and port modernization projects. Expanding adoption of advanced polymer-based and composite sea liner compounds for enhanced vessel protection, cargo safety, and operational efficiency is further contributing to market expansion across developed and emerging economies.

The continuous growth of international seaborne trade, combined with increasing regulatory emphasis on vessel durability, environmental compliance, and maintenance cost reduction, is encouraging shipbuilders, marine operators, and offshore infrastructure developers to utilize high-performance sea liner compounds. Modern marine vessels increasingly require specialized compounds that offer superior resistance to saltwater corrosion, chemical exposure, abrasion, and extreme weather conditions. In addition, advancements in material science are enabling the development of lightweight, high-strength liner compounds that improve fuel efficiency and extend vessel service life. The growing expansion of offshore energy projects, container shipping fleets, and marine logistics networks is also generating substantial demand for advanced sea liner compound solutions, establishing them as critical materials for enhancing operational reliability, safety, and long-term performance in marine environments.

Key Market Trends & Insights

- North America dominated the sea liner compounds market with the largest revenue share of 36.8% in 2025, supported by strong marine manufacturing capabilities, extensive offshore energy operations, advanced materials adoption, and continuous investments in commercial and defense maritime sectors.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 8.9% from 2026 to 2033. Growth is driven by expanding shipbuilding industries in China, South Korea, and India, increasing port infrastructure development, rising maritime trade volumes, and growing demand for high-performance marine-grade compounds.

- The Polyethylene segment held the largest market revenue share of approximately 27.6% in 2025 driven by its superior moisture resistance, chemical stability, impact strength, and cost-effectiveness across marine, industrial, packaging, and transportation applications. Polyethylene compounds are widely utilized in liner manufacturing due to their excellent durability in corrosive and high-humidity operating environments. Growing demand for lightweight and recyclable materials is further supporting segment dominance.

- The Polyamide segment is projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by increasing demand for high-performance engineering plastics with enhanced mechanical strength, wear resistance, and thermal stability. Rising adoption across marine equipment, industrial machinery, automotive components, and advanced infrastructure applications is accelerating segment expansion. Manufacturers are increasingly investing in reinforced polyamide compounds to improve operational performance in demanding environments.

- The Packaging segment held the largest market revenue share of approximately 24.8% in 2025 driven by increasing demand for protective liner materials across bulk storage, marine cargo transportation, industrial packaging, and logistics operations. Sea liner compounds are extensively used to improve durability, moisture protection, chemical resistance, and product safety during transportation and storage. The expansion of global trade and shipping activities continues to support strong demand across this segment.

- The Building & Construction segment is projected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by rising investments in coastal infrastructure, ports, marine terminals, offshore facilities, and waterfront development projects. Increasing demand for corrosion-resistant and long-lasting construction materials is encouraging adoption of advanced liner compounds across marine and industrial construction applications. Growing infrastructure modernization programs across Asia-Pacific and the Middle East are further contributing to segment growth.

Market Size & Forecast

- Global Market Value (2025): USD 18.19 Billion

- Expected Market Value (2033): USD 32.19 Billion

- Forecast CAGR (2026–2033): 7.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Sea Liner Compounds Market Segmentation

|

Attributes |

Sea Liner Compounds Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• DuPont (U.S.) |

|

Market Opportunities |

• Increasing Adoption Of Sustainable And Recyclable Marine Liner Materials • Expansion Of Offshore Renewable Energy And Marine Infrastructure Projects |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Sea Liner Compounds Market Trends

Trend: Rising Adoption Of High-Performance And Sustainable Marine Protection Materials

Increasing demand for durable, corrosion-resistant, and environmentally compliant materials across commercial shipping, offshore energy, and marine infrastructure sectors is driving the adoption of advanced sea liner compounds. Traditional marine protection materials often require frequent maintenance and replacement due to prolonged exposure to saltwater, ultraviolet radiation, mechanical abrasion, and harsh weather conditions. As shipping operators and port authorities seek to reduce maintenance costs and improve vessel longevity, demand for advanced polymer-based and composite liner compounds is increasing significantly.

In modern marine vessels, manufacturers are integrating advanced sea liner compounds, For instance high-density polyethylene (HDPE), polypropylene, and reinforced composite formulations, to improve corrosion resistance, reduce structural degradation, and extend service life. Offshore platforms and port facilities are also utilizing specialized liner systems to protect storage tanks, cargo holds, pipelines, and marine structures from chemical exposure and environmental wear. The growing focus on sustainable shipping operations is accelerating adoption of recyclable and low-emission liner materials that comply with evolving maritime environmental regulations. In addition, increasing investments in offshore wind farms and marine logistics infrastructure are creating new application opportunities. Industry assessments conducted during 2025 indicated that advanced marine liner compound installations improved corrosion protection performance by approximately 20–30% while reducing maintenance frequency across large commercial vessel fleets.

Sea Liner Compounds Market Dynamics

Key Market Driver: Expansion Of Global Maritime Trade And Offshore Infrastructure Development

Global maritime trade continues to expand as international commerce, energy transportation, and containerized shipping activities increase across major economies. Growing cargo volumes and rising investments in marine infrastructure are creating significant demand for materials capable of protecting vessels and offshore assets from corrosion, abrasion, and environmental degradation. This is generating strong demand for high-performance sea liner compounds across shipping, logistics, and energy industries.

Shipping companies, port operators, and offshore energy developers are increasingly deploying advanced liner compounds to improve operational efficiency and asset durability. Marine operators are utilizing specialized sea liner systems, For instance in cargo containers, storage tanks, ship hull components, and offshore structures, to minimize maintenance costs and extend equipment lifespan. Similarly, offshore oil and gas facilities are investing in corrosion-resistant liner materials to improve infrastructure reliability in aggressive marine environments. Real-world marine infrastructure projects completed across Southeast Asia and the Middle East during 2024 reported maintenance cost reductions of approximately 15–20% following implementation of advanced protective liner compound technologies.

Key Restraint/Challenge: High Raw Material Costs And Stringent Environmental Regulations

Manufacturers of sea liner compounds face increasing challenges associated with fluctuating raw material prices and evolving environmental compliance requirements. Many advanced liner formulations depend on specialty polymers, additives, and composite materials that are subject to supply chain volatility and cost pressures. These factors increase overall production expenses and can impact product affordability for marine operators and infrastructure developers.

In addition, stringent international environmental regulations governing marine emissions, hazardous substances, and material disposal are requiring manufacturers to continuously reformulate products and invest in sustainable alternatives. Compliance with regulations issued by maritime authorities often increases development costs and extends product qualification timelines. Smaller manufacturers may face additional challenges related to research and certification expenses. Industry analyses indicate that specialty polymer prices experienced fluctuations of approximately 10–15% during recent years, creating procurement and cost management challenges throughout the sea liner compounds value chain.

Key Market Opportunity: Growing Adoption Of Sustainable Marine Materials And Offshore Renewable Energy Projects

The increasing emphasis on sustainability across the maritime industry is creating substantial opportunities for innovative sea liner compound manufacturers. Shipping companies, port operators, and offshore developers are seeking environmentally responsible materials that improve performance while supporting sustainability objectives. This trend is encouraging investment in recyclable, bio-based, and low-emission liner compound technologies.

Manufacturers are increasingly developing advanced sea liner compounds, For instance recyclable polymer liners, lightweight composite materials, and environmentally friendly protective coatings, to meet evolving customer and regulatory requirements. In addition, rapid expansion of offshore renewable energy projects, particularly offshore wind farms, is generating significant demand for durable marine protection materials capable of withstanding harsh ocean environments. Advancements in polymer engineering and composite technologies are further enhancing material performance and lifecycle durability. Offshore renewable energy projects commissioned during 2025 across Europe and Asia-Pacific reported service-life extension benefits of approximately 20–25% for critical marine infrastructure components protected using advanced liner compound systems, highlighting significant growth opportunities for the market.

Sea Liner Compounds Market Scope

The market is segmented on the basis of product and end user.

• By Product

On the basis of product, the sea liner compounds market is segmented into Polyethylene, Polypropylene (PP), Thermoplastic Vulcanizates (TPV), Thermoplastic Polyolefins (TPO), Poly Vinyl Chloride (PVC), Polystyrene, Polyethylene Terephthalate (PET), Polybutylene Terephthalate (PBT), Polyamide, Polycarbonate, Acrylonitrile Butadiene Styrene (ABS), and Others. The Polyethylene segment held the largest market revenue share of approximately 27.6% in 2025 driven by its superior moisture resistance, chemical stability, impact strength, and cost-effectiveness across marine, industrial, packaging, and transportation applications. Polyethylene compounds are widely utilized in liner manufacturing due to their excellent durability in corrosive and high-humidity operating environments. Growing demand for lightweight and recyclable materials is further supporting segment dominance.

The Polyamide segment is projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by increasing demand for high-performance engineering plastics with enhanced mechanical strength, wear resistance, and thermal stability. Rising adoption across marine equipment, industrial machinery, automotive components, and advanced infrastructure applications is accelerating segment expansion. Manufacturers are increasingly investing in reinforced polyamide compounds to improve operational performance in demanding environments.

• By End User

On the basis of end user, the sea liner compounds market is segmented into Automotive, Building & Construction, Electrical & Electronics, Packaging, Consumer Goods, Industrial Machinery, Medical Devices, Optical Media, and Others. The Packaging segment held the largest market revenue share of approximately 24.8% in 2025 driven by increasing demand for protective liner materials across bulk storage, marine cargo transportation, industrial packaging, and logistics operations. Sea liner compounds are extensively used to improve durability, moisture protection, chemical resistance, and product safety during transportation and storage. The expansion of global trade and shipping activities continues to support strong demand across this segment.

The Building & Construction segment is projected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by rising investments in coastal infrastructure, ports, marine terminals, offshore facilities, and waterfront development projects. Increasing demand for corrosion-resistant and long-lasting construction materials is encouraging adoption of advanced liner compounds across marine and industrial construction applications. Growing infrastructure modernization programs across Asia-Pacific and the Middle East are further contributing to segment growth.

Sea Liner Compounds Market Regional Analysis

North America Sea Liner Compounds Market Insight

North America dominated the sea liner compounds market with the largest revenue share of 38.42% in 2025, supported by strong demand from automotive, packaging, industrial machinery, and construction sectors. The region benefits from a well-established polymer manufacturing industry, advanced material processing capabilities, and increasing investments in lightweight and durable compound solutions. Growing adoption of high-performance thermoplastics for marine and industrial applications, combined with stringent quality standards and sustainability initiatives, continues to support market expansion across the region.

U.S. Sea Liner Compounds Market Insight

The U.S. sea liner compounds market captured the largest revenue share in 2025 within North America, fueled by robust demand from automotive manufacturing, industrial packaging, consumer goods, and electrical equipment industries. Manufacturers are increasingly adopting advanced polymer compounds to improve durability, corrosion resistance, and operational efficiency across end-use applications. The growing emphasis on lightweight materials, recycling initiatives, and technological advancements in polymer engineering is further contributing to market growth in the country.

Europe Sea Liner Compounds Market Insight

The Europe sea liner compounds market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing investments in sustainable materials, circular economy initiatives, and advanced manufacturing technologies. The region's strong automotive, packaging, and construction sectors are accelerating demand for high-performance polymer compounds with enhanced environmental characteristics. In addition, regulatory support for recyclable materials and reduced carbon emissions is encouraging manufacturers to develop innovative sea liner compound solutions across multiple industries.

U.K. Sea Liner Compounds Market Insight

The U.K. sea liner compounds market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for sustainable packaging materials, advanced industrial components, and lightweight construction products. Growing investments in infrastructure modernization and increasing adoption of engineered plastics across manufacturing industries are supporting market development. Furthermore, the country's focus on recycling technologies and resource-efficient materials is expected to stimulate long-term demand for sea liner compounds.

Germany Sea Liner Compounds Market Insight

The Germany sea liner compounds market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country's strong automotive manufacturing base and leadership in advanced materials engineering. German manufacturers are increasingly utilizing high-performance compounds to improve product durability, weight reduction, and sustainability across industrial applications. The integration of innovative polymer technologies and increasing demand for recyclable materials are further supporting market expansion throughout the forecast period.

Asia-Pacific Sea Liner Compounds Market Insight

The Asia-Pacific sea liner compounds market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding manufacturing activities, and increasing demand from packaging, automotive, and electronics industries. Rising investments in polymer production facilities and favorable government initiatives supporting industrial growth are accelerating market development across the region. In addition, growing consumer demand for durable and cost-effective products is encouraging wider adoption of advanced compound materials.

Japan Sea Liner Compounds Market Insight

The Japan sea liner compounds market is expected to witness the fastest growth rate from 2026 to 2033 due to the country's advanced manufacturing ecosystem and strong focus on high-performance materials. Japanese industries are increasingly utilizing specialized compounds in automotive components, electronics, and industrial equipment to improve performance and reliability. The growing emphasis on lightweight materials, technological innovation, and sustainable manufacturing practices is further contributing to market growth.

China Sea Liner Compounds Market Insight

The China sea liner compounds market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's extensive manufacturing sector, large-scale polymer production capacity, and growing domestic consumption. China remains a major hub for automotive, packaging, consumer goods, and industrial production, generating substantial demand for advanced compound materials. The expansion of infrastructure projects, increasing exports, and continued investments in high-performance plastics manufacturing are key factors propelling the market in China.

Sea Liner Compounds Market Share

The Sea Liner Compounds industry is primarily led by well-established companies, including:

• DuPont (U.S.)

• BASF SE (Germany)

• Dow Inc. (U.S.)

• Arkema S.A. (France)

• Kuraray Co., Ltd. (Japan)

• Adell Plastics, Inc. (U.S.)

• Asahi Kasei Corporation (Japan)

• RTP Company (U.S.)

• LyondellBasell Industries Holdings B.V. (U.K.)

• Kraton Corporation (U.S.)

• PolyVisions, Inc. (U.S.)

• Akro-Plastic GmbH (Germany)

• Aurora Plastics LLC (U.S.)

• Exxon Mobil Corporation (U.S.)

• DSM-Firmenich AG (Netherlands)

• SABIC (Saudi Arabia)

• Sojitz Corporation (Japan)

• Celanese Corporation (U.S.)

• HEXPOL AB (Sweden)

• Covestro AG (Germany)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Sea Liner Compounds Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Sea Liner Compounds Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Sea Liner Compounds Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.