Global Secondary Otalgia Market

Market Size in USD Million

USD

200.00 Million

USD

316.37 Million

2024

2032

USD

200.00 Million

USD

316.37 Million

2024

2032

| 2025 - 2032 | |

| USD 200.00 Million | |

| USD 316.37 Million | |

| % | |

|

Secondary Otalgia Market Size

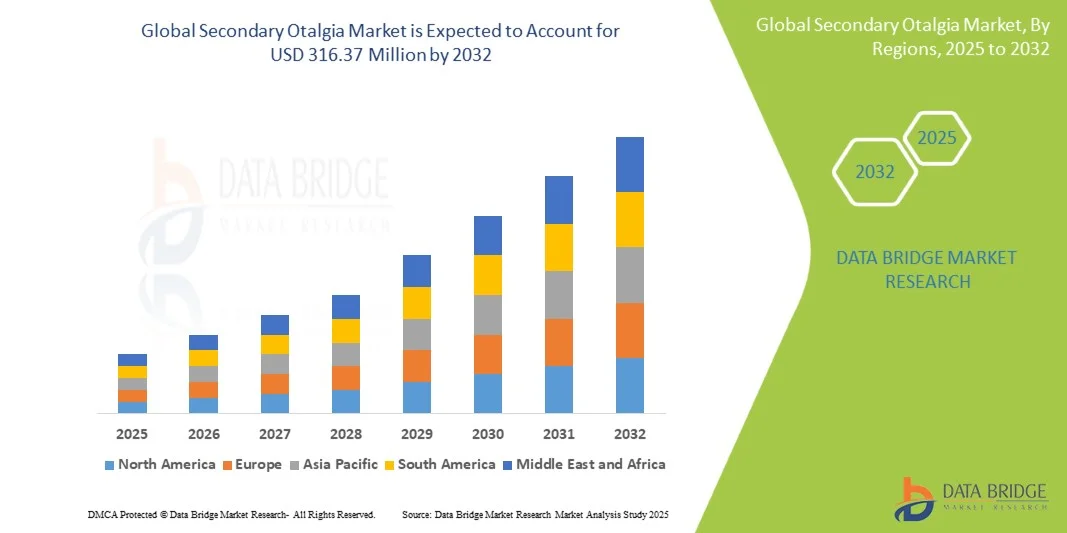

- The global secondary otalgia market size was valued at USD 200.00 million in 2024 and is expected to reach USD 316.37 million by 2032, at a CAGR of 5.90% during the forecast period

- The market growth is largely fueled by increasing prevalence of conditions causing referred ear pain, such as dental disorders, temporomandibular joint (TMJ) dysfunction, throat infections, and other systemic ailments, coupled with rising awareness about targeted treatment options

- Furthermore, growing adoption of advanced diagnostic tools, minimally invasive therapies, and patient-focused pain management solutions is driving demand for effective secondary otalgia treatments, thereby significantly boosting the market’s expansion

Secondary Otalgia Market Analysis

- Secondary otalgia, referring to ear pain originating from conditions outside the ear such as dental, temporomandibular joint (TMJ), or throat disorders, is gaining clinical attention, driving demand for effective pharmacological and procedural interventions in both adults and pediatric populations

- The escalating demand for secondary otalgia treatments is primarily fueled by rising prevalence of underlying conditions, increased patient awareness, and growing adoption of convenient drug-based therapies and minimally invasive procedures

- North America dominated the secondary otalgia market with the largest revenue share of 40.8% in 2024, due to advanced healthcare infrastructure, high awareness of ENT and dental disorders, and strong presence of key pharmaceutical and medical device players

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, driven by improving healthcare access, rising incidence of dental and throat conditions, and growing adoption of modern pharmacological treatments

- Antibiotics segment is dominated the secondary otalgia market with a market share of 42.5% in 2024, reflecting their widespread use for treating underlying bacterial infections causing referred ear pain

Report Scope and Secondary Otalgia Market Segmentation

|

Attributes |

Secondary Otalgia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Secondary Otalgia Market Trends

“Advancements in Targeted Pharmacological and Minimally Invasive Therapies”

- A significant and accelerating trend in the global secondary otalgia market is the increasing development and adoption of targeted antibiotics, nasal steroids, decongestants, and minimally invasive procedures to address underlying causes such as dental, TMJ, or throat disorders, improving patient outcomes and comfort

- For instance, the use of image-guided myringotomy combined with antibiotic therapy allows precise treatment of referred ear pain while minimizing side effects and recovery time

- Advanced drug delivery systems and formulations are emerging that optimize dosage, reduce systemic exposure, and enhance efficacy, thereby improving patient compliance and satisfaction

- The integration of digital health tools, such as telemedicine consultations and remote monitoring apps, facilitates timely diagnosis, prescription management, and follow-up care for patients with secondary otalgia

- This trend towards precision treatment and technology-assisted patient care is fundamentally reshaping therapeutic approaches, with companies developing novel drug formulations and procedural innovations to improve safety, convenience, and clinical outcomes

- The demand for therapies that combine efficacy, convenience, and minimally invasive intervention is growing rapidly across both hospital and homecare settings, as patients increasingly seek effective and low-risk solutions

Secondary Otalgia Market Dynamics

Driver

“Rising Prevalence of Underlying Disorders and Awareness of Treatment Options”

- The increasing incidence of dental infections, TMJ disorders, and throat-related ailments, combined with growing awareness about secondary otalgia among patients and healthcare providers, is a significant driver for heightened demand for effective treatments

- For instance, rising cases of chronic tonsillitis leading to referred ear pain have prompted hospitals and specialty clinics to adopt standardized treatment protocols incorporating antibiotics and supportive therapies

- As patients and physicians become more aware of the impact of referred ear pain on quality of life, adoption of timely pharmacological interventions and procedural options has increased

- Furthermore, the expansion of telehealth and online pharmacy services facilitates easier access to secondary otalgia medications and guidance, driving uptake across diverse populations

- Convenience of home-based care, coupled with growing availability of prescription drugs and minimally invasive procedures, is propelling adoption in both clinical and outpatient settings, expanding market reach

Restraint/Challenge

“Side Effects, Misdiagnosis, and Regulatory Hurdles”

- Concerns surrounding adverse effects of antibiotics, nasal steroids, and other treatments, as well as risks of misdiagnosis due to referred nature of ear pain, pose significant challenges to broader market penetration

- For instance, misattribution of dental-origin ear pain to primary ear infections can lead to inappropriate therapy, affecting patient trust and treatment outcomes

- Addressing these challenges through accurate diagnostic protocols, clinical guidelines, and patient education is crucial for building confidence in therapies. Companies and clinics are increasingly emphasizing standardized evaluation methods and evidence-based treatment plans

- In addition, regulatory compliance and approval timelines for new drugs or procedural devices can delay market introduction, while costs of advanced therapies may limit access for certain populations

- Overcoming these hurdles through enhanced clinical training, safer treatment formulations, and streamlined regulatory strategies will be vital for sustained market growth

Secondary Otalgia Market Scope

The market is segmented on the basis of drug class, mode of administration, distribution channel, and end user.

- By Drug Class

On the basis of drug class, the secondary otalgia market is segmented into antibiotics, decongestants, nasal steroids, and myringotomy. The antibiotics segment dominated the market with the largest market revenue share of 42.5% in 2024, driven by its widespread use in treating bacterial infections causing referred ear pain from dental, throat, or TMJ disorders. Patients and healthcare providers prefer antibiotics due to their effectiveness in addressing the root cause of secondary otalgia. Hospitals and specialty clinics frequently adopt standardized antibiotic regimens for rapid symptom relief and to prevent complications. The segment also benefits from strong availability across hospital and retail pharmacies, supporting consistent patient access. In addition, combination therapies that integrate antibiotics with supportive treatments enhance efficacy and patient compliance. The growing awareness of antibiotic treatment protocols in North America and Europe further reinforces market dominance.

The myringotomy segment is expected to witness the fastest growth rate of 18.2% from 2025 to 2031, fueled by increasing adoption of minimally invasive procedures for managing persistent or severe referred ear pain. Myringotomy allows precise drainage of middle ear fluid, offering rapid relief and reducing the need for prolonged medication. Rising preference for procedure-based solutions in pediatric and adult populations drives demand in hospital and specialty clinic settings. The segment benefits from technological advancements, including image-guided and laser-assisted myringotomy techniques, which enhance safety and efficacy. Awareness campaigns by ENT specialists are encouraging adoption among patients with recurrent otalgia. Furthermore, the procedure’s integration with post-operative antibiotic therapy enhances treatment outcomes and patient satisfaction.

- By Mode of Administration

On the basis of mode of administration, the secondary otalgia market is segmented into injectable, oral, and others. The oral segment dominated the market in 2024 with a market share of 55%, driven by convenience, ease of self-administration, and wide patient acceptance. Oral formulations of antibiotics, decongestants, and nasal steroids allow outpatient management of secondary otalgia, reducing hospital visits. Physicians often prescribe oral drugs as first-line therapy for mild to moderate cases of referred ear pain. The availability of oral drugs through retail and online pharmacies supports adherence and continuous treatment. In addition, pharmaceutical innovations, such as extended-release and combination oral therapies, further boost adoption. Oral administration is also preferred for homecare and specialty clinic settings due to patient comfort and familiarity.

The injectable segment is expected to witness the fastest growth rate of 16.5% from 2025 to 2031, driven by the rising need for rapid onset of action in severe or acute cases of secondary otalgia. Injectable antibiotics and steroids provide immediate therapeutic effects, especially in hospital and emergency care settings. The segment is supported by growing availability of injectable formulations and trained healthcare personnel. Adoption is increasing in specialty clinics and high-dependency units, where precise dosing and fast response are critical. Injectable therapy is also preferred when oral intake is limited due to comorbid conditions or gastrointestinal issues. Technological improvements in prefilled syringes and safer injection devices further encourage growth in this segment.

- By Distribution Channel

On the basis of distribution channel, the secondary otalgia market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The hospital pharmacies segment dominated the market with a share of 48.6% in 2024, owing to the concentration of treatment protocols, accessibility of prescription medications, and presence of trained healthcare professionals. Hospitals serve as primary treatment centers for patients with severe or persistent secondary otalgia, where antibiotics, nasal steroids, and procedural interventions are readily administered. Hospital pharmacies ensure controlled dispensing of medications, supporting patient safety and compliance. In addition, established partnerships with pharmaceutical companies enhance the availability of specialized drugs. Hospital pharmacies also play a central role in post-procedure medication management, particularly for patients undergoing myringotomy. The segment’s dominance is reinforced by consistent demand from inpatient and outpatient departments.

The online pharmacies segment is expected to witness the fastest CAGR of 19% from 2025 to 2031, fueled by the growing penetration of digital healthcare platforms and e-pharmacies. Patients increasingly prefer online channels for the convenience of home delivery, access to medication information, and teleconsultation support. E-commerce platforms also allow access to a wider range of drug classes, including antibiotics and decongestants, particularly in regions with limited brick-and-mortar retail coverage. Rising smartphone usage and digital literacy contribute to the segment’s rapid adoption. Furthermore, online pharmacies facilitate subscription-based medicine delivery, improving adherence for chronic cases. The convenience and expanding trust in online healthcare services continue to drive robust growth.

- By End User

On the basis of end user, the secondary otalgia market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with a share of 45.3% in 2024, driven by high patient inflow for severe or persistent secondary otalgia cases, including pediatric and adult populations. Hospitals provide integrated care combining diagnostics, pharmacological therapy, and procedural interventions such as myringotomy. The availability of trained ENT specialists and comprehensive treatment protocols reinforces hospital dominance. Hospitals also ensure effective monitoring of therapy outcomes, particularly for antibiotics and injectable treatments. Strong partnerships with pharmaceutical companies enable timely supply of medications. The segment benefits from insurance coverage and structured patient care pathways, enhancing accessibility and adoption.

The homecare segment is expected to witness the fastest growth rate of 17.8% from 2025 to 2031, driven by the rising demand for convenient treatment management outside hospital settings. Oral medications, nasal sprays, and telemedicine-guided therapies support home-based management of secondary otalgia. Increasing patient awareness, improved access to online pharmacies, and the trend toward outpatient care contribute to adoption. The segment is further boosted by digital health monitoring tools that allow remote tracking of symptoms and medication adherence. Homecare solutions reduce treatment costs and hospital visits, improving patient satisfaction and compliance. Growing focus on patient-centric care models in developed and emerging regions reinforces this trend.

Secondary Otalgia Market Regional Analysis

- North America dominated the secondary otalgia market with the largest revenue share of 40.8% in 2024, due to advanced healthcare infrastructure, high awareness of ENT and dental disorders, and strong presence of key pharmaceutical and medical device players

- Patients and healthcare professionals in the region highly value timely diagnosis, effective pharmacological therapies, and access to procedural interventions such as myringotomy, contributing to widespread adoption of secondary otalgia treatments

- This dominance is further supported by advanced healthcare infrastructure, well-established hospitals and specialty clinics, high insurance coverage, and the presence of key pharmaceutical and medical device companies offering innovative solutions, establishing North America as the leading region for secondary otalgia management

U.S. Secondary Otalgia Market Insight

The U.S. secondary otalgia market captured the largest revenue share of 81% in 2024 within North America, fueled by the high prevalence of dental, TMJ, and throat-related disorders leading to referred ear pain. Patients and healthcare providers increasingly prioritize timely diagnosis and effective treatment through antibiotics, nasal steroids, and procedural interventions such as myringotomy. The growing preference for outpatient care, telemedicine consultations, and home-based management further propels the market. In addition, the widespread adoption of advanced diagnostic tools and clinical protocols is significantly contributing to the market’s expansion.

Europe Secondary Otalgia Market Insight

The Europe secondary otalgia market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of ENT and dental disorders and the rising demand for effective therapies. Urbanization, aging populations, and expanding healthcare infrastructure are fostering treatment adoption. European patients are also drawn to minimally invasive procedures and evidence-based pharmacological therapies. The region is experiencing significant growth across hospitals, specialty clinics, and homecare settings, with secondary otalgia management being incorporated into standard treatment protocols.

U.K. Secondary Otalgia Market Insight

The U.K. secondary otalgia market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of referred ear pain and the adoption of targeted treatment options. Increasing cases of TMJ and throat-related disorders are encouraging patients to seek timely interventions. The U.K.’s robust healthcare infrastructure, alongside growing telemedicine and pharmacy services, is expected to continue to stimulate market growth. In addition, public health initiatives promoting early diagnosis and treatment support market expansion.

Germany Secondary Otalgia Market Insight

The Germany secondary otalgia market is expected to expand at a considerable CAGR during the forecast period, fueled by high awareness of ENT disorders and the growing demand for advanced pharmacological and minimally invasive therapies. Germany’s well-developed healthcare system, combined with a focus on clinical innovation and patient safety, promotes adoption. Hospitals and specialty clinics are increasingly offering integrated treatment protocols. Patients prefer evidence-based approaches, emphasizing both safety and effectiveness, aligning with local regulatory and healthcare standards.

Asia-Pacific Secondary Otalgia Market Insight

The Asia-Pacific secondary otalgia market is poised to grow at the fastest CAGR of 24% from 2025 to 2031, driven by rising incidence of dental, throat, and TMJ disorders, improving healthcare access, and increasing patient awareness in countries such as China, Japan, and India. Government initiatives to expand healthcare infrastructure and digital health services are supporting the adoption of secondary otalgia treatments. Rising disposable incomes and urbanization contribute to greater healthcare spending. The availability of affordable drug therapies and procedural interventions is further driving market growth across hospital and homecare settings.

Japan Secondary Otalgia Market Insight

The Japan secondary otalgia market is gaining momentum due to increasing prevalence of TMJ, dental, and throat-related ear pain, coupled with a high-tech healthcare culture. The growing number of outpatient clinics and specialty centers offering targeted therapies, along with telemedicine and digital prescription services, is fueling adoption. In addition, Japan’s aging population is such asly to spur demand for convenient, effective, and minimally invasive treatments in both residential and clinical settings. The integration of digital health tools enhances patient monitoring and compliance, further supporting market growth.

India Secondary Otalgia Market Insight

The India secondary otalgia market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rising awareness of ENT and dental disorders, rapid urbanization, and improving healthcare access. India is witnessing increasing adoption of oral and injectable therapies, as well as procedural interventions in hospitals, specialty clinics, and homecare settings. The expansion of telemedicine, online pharmacies, and affordable treatment options is propelling market growth. In addition, the push toward smart healthcare delivery and government initiatives to improve diagnostic and treatment facilities are key factors supporting the market in India.

Secondary Otalgia Market Share

The secondary otalgia industry is primarily led by well-established companies, including:

- eosera (U.S.)

- Amneal Pharmaceuticals LLC (U.S.)

- Hisamitsu Pharmaceutical Co.,Inc. (Japan)

- Grünenthal (Germany)

- Johnson & Johnson and its affiliates. (U.S.)

- Sanofi (France)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Novartis AG (Switzerland)

- Merz Pharma (Germany)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Eisai Co., Ltd. (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Bayer AG (Germany)

- Biogen (U.S.)

- AstraZeneca (U.K.)

- H. Lundbeck A/S (Denmark)

- Amgen Inc. (U.S.)

What are the Recent Developments in Global Secondary Otalgia Market?

- In March 2024, A study published in The American Journal of Otolaryngology reviewed and synthesized current evidence on the role of otolaryngologists in diagnosing and managing otalgia resulting from temporomandibular joint disorders (TMD). The study emphasizes the importance of a multidisciplinary approach in treating patients with TMD-related otalgia

- In August 2023, Eosera introduced single-use vials of its Ear Wax MD and Ear Pain MD formulations. These single-dose products offer convenience for on-the-go consumers seeking effective ear care solutions

- In January 2023, A comprehensive systematic review and meta-analysis published in European Archives of Oto-Rhino-Laryngology examined the aetiology and management options for secondary referred otalgia. The study highlighted the diverse causes of secondary otalgia and emphasized the importance of identifying the underlying pathology for effective treatment

- In January 2022, A case report published in SAGE Open Medical Case Reports described a rare instance of secondary otalgia caused by a foreign body embedded in the lateral surface of the tongue. This case underscores the complexity of diagnosing secondary otalgia and the need for thorough examination to identify uncommon causes

- In April 2021, The American Academy of Otolaryngology-Head and Neck Surgery Foundation (AAO-HNSF) released an updated clinical practice guideline for the evaluation and management of otalgia. The guideline provides evidence-based recommendations to clinicians for diagnosing and treating both primary and secondary otalgia, aiming to standardize care and improve patient outcomes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.