Global Self Cleaning Filters Market

Market Size in USD Billion

USD

8.25 Billion

USD

14.60 Billion

2024

2032

USD

8.25 Billion

USD

14.60 Billion

2024

2032

| 2025 - 2032 | |

| USD 8.25 Billion | |

| USD 14.60 Billion | |

| % | |

|

Self Cleaning Filters Market Size

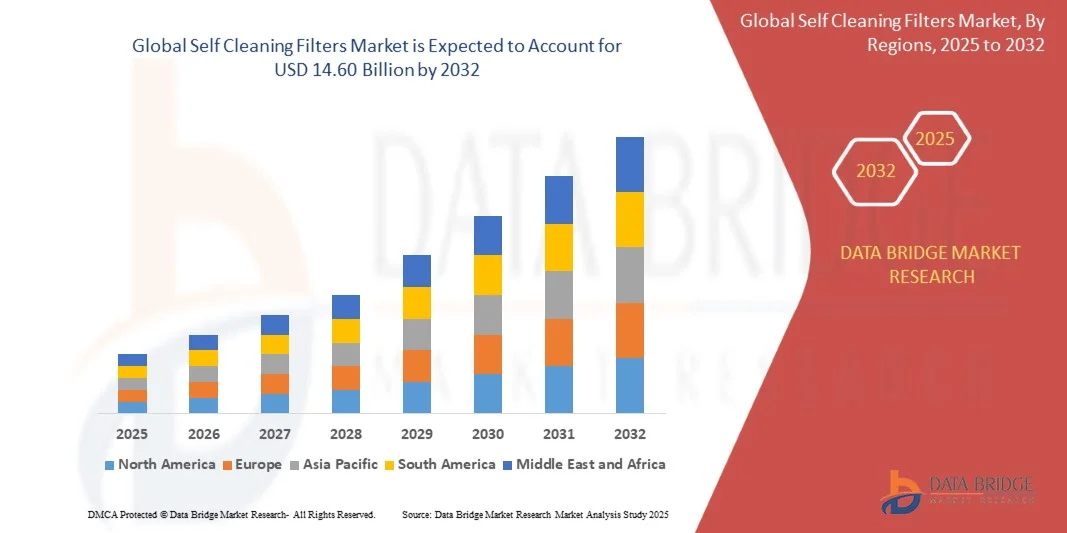

- The global self cleaning filters market size was valued at USD 8.25 billion in 2024 and is expected to reach USD 14.60 billion by 2032, at a CAGR of 7.40% during the forecast period

- The market growth is largely fueled by the increasing adoption of automated and efficient filtration systems across municipal, industrial, and commercial sectors, leading to improved water and wastewater management, reduced maintenance costs, and enhanced operational efficiency

- Furthermore, rising demand for reliable, low-maintenance, and high-capacity self-cleaning filters in industries such as chemicals, pharmaceuticals, power generation, and food and beverages is establishing these filters as the preferred solution for continuous and uninterrupted processes. These converging factors are accelerating the uptake of self-cleaning filtration systems, thereby significantly boosting the industry's growth

Self Cleaning Filters Market Analysis

- Self-cleaning filters, designed to automatically remove accumulated debris and suspended solids, are increasingly essential in municipal water treatment, industrial processes, and manufacturing operations due to their ability to ensure consistent filtration, minimize downtime, and reduce manual cleaning efforts

- The escalating demand for self-cleaning filters is primarily fueled by stringent regulatory requirements for water quality, increasing industrialization, rising focus on sustainable water management, and the need for process efficiency and automation across various end-use sectors

- Asia-Pacific dominated the self cleaning filters market with a share of over 44% in 2024, due to rapid industrialization, increasing municipal water treatment projects, and the expanding chemical and power sectors

- North America is expected to be the fastest growing region in the self cleaning filters market during the forecast period due to increasing industrial automation, robust demand in chemicals, power, and municipal water sectors, and technological advancements in filtration systems

- Vertical segment dominated the market with a market share of 62.5% in 2024, due to its compact design, high filtration efficiency, and ability to handle large volumes in continuous flow operations. Vertical filters are particularly preferred in municipal water treatment and power generation sectors for their consistent performance and reduced footprint, which facilitates installation in constrained spaces

Report Scope and Self Cleaning Filters Market Segmentation

|

Attributes |

Self Cleaning Filters Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Self Cleaning Filters Market Trends

“Rising Use of Automated Self-Cleaning Filters”

- The self-cleaning filters market is experiencing strong growth as industries increasingly adopt automated filtration systems to ensure uninterrupted operations and improved fluid management efficiency. Automated self-cleaning filters provide continuous filtration without manual intervention, reducing downtime and improving overall process reliability across diverse industrial applications

- For instance, Eaton Corporation and Amiad Water Systems have introduced automated self-cleaning filters integrated with programmable control systems that enable real-time cleaning cycles and remote monitoring. These advancements exemplify how major manufacturers are addressing operational efficiency and maintenance reduction in sectors such as water treatment, chemicals, and food processing

- The rising trend toward automation and Industry 4.0 is propelling the development of intelligent self-cleaning filtration systems equipped with sensors, IoT connectivity, and performance analytics. This technological integration allows operators to track filter conditions, activate cleaning cycles remotely, and optimize filtration performance with minimal human oversight

- In municipal water treatment systems, self-cleaning filters are being widely adopted to ensure uninterrupted supply and compliance with stringent water quality standards. Their ability to remove suspended solids and contaminants effectively reduces clogging issues and extends system lifespan, supporting public infrastructure reliability

- The growing awareness about sustainable water management initiatives is driving industries to deploy self-cleaning filters that minimize waste and optimize energy consumption. Their automated functionality significantly reduces water usage during backwashing compared with traditional filtration systems, aligning with global sustainability targets

- As industries continue to seek high-performance, maintenance-free filtration solutions, automated self-cleaning filters are becoming central to modern fluid handling systems. The increasing preference for smart, durable, and energy-efficient filters ensures their vital role in achieving cleaner production and resource conservation goals worldwide

Self Cleaning Filters Market Dynamics

Driver

“Growing Demand for Low-Maintenance Industrial and Municipal Filters”

- The increasing need for efficient filtration systems that reduce manual maintenance and operational downtime is driving the adoption of self-cleaning filters across industries. Their ability to automatically remove debris and contaminants without halting system operations enhances reliability and productivity in continuous manufacturing environments

- For instance, GEA Group AG and Parker Hannifin Corporation have developed advanced self-cleaning filtration units designed for processing fluids in food, beverage, and petrochemical industries. These products demonstrate how innovation in filter automation is enabling consistent throughput and minimizing human intervention in filtration processes

- The growing complexity of industrial systems and the emphasis on operational efficiency are encouraging end users to replace conventional strainers and disposable filters with automated alternatives. Self-cleaning filters effectively handle high solid loads and viscous fluids, reducing the frequency of maintenance and filter replacements

- Municipal water treatment and wastewater facilities are increasingly investing in automatic filtration units to maintain uninterrupted supply and meet regulatory compliance. The reduced need for manual cleaning supports lower labor costs while improving process sustainability and safety

- The rising integration of maintenance-free designs and robust operation capabilities in industrial setups ensures continued demand for self-cleaning filters. This transition toward automation and reduced human dependency is expected to remain a defining growth driver for the global filtration industry

Restraint/Challenge

“High Upfront Costs”

- The substantial initial investment required for installing self-cleaning filtration systems presents a major challenge, particularly for small and medium-sized facilities. The advanced automation mechanisms, control software, and durable materials used in these systems significantly raise upfront costs compared with traditional filters

- For instance, companies such as Eaton Corporation and Forsta Filters report higher equipment costs for fully automated filter units due to specialized sensors, actuators, and control modules. These expenses often discourage initial adoption, especially in emerging regions with limited capital budgets

- The complexity of integrating automated filtration units with existing process systems adds to installation and setup costs. Customization requirements to meet specific fluid characteristics or industry standards further increase engineering and commissioning expenses for manufacturers and end users

- Maintenance savings over the long term are countered initially by high procurement and installation spending, which affects short-term financial feasibility. Many small-scale industries prefer semi-automated or manual systems to balance cost efficiency against functionality

- Addressing these financial challenges requires continued innovation in system design, scalable production, and modular component development to reduce cost per unit. As automation technologies become more accessible and economies of scale improve, the cost barriers for self-cleaning filter adoption are expected to diminish across global markets

Self Cleaning Filters Market Scope

The market is segmented on the basis of mode of operation, material type, type, source, and end use.

• By Mode of Operation

On the basis of mode of operation, the self-cleaning filters market is segmented into integrated and individual. The integrated segment dominated the market with the largest revenue share in 2024, driven by its capability to seamlessly combine filtration and cleaning processes in a single system, reducing downtime and operational complexity. Industries increasingly prefer integrated filters for their enhanced efficiency, reliability, and reduced maintenance costs, particularly in continuous process applications. The compatibility of integrated systems with automated monitoring and control systems further strengthens their adoption in modern industrial setups.

The individual segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by demand in small-to-medium scale operations requiring flexible and modular filtration solutions. For instance, companies such as Pall Corporation are promoting modular, individually operable filters for chemical and food processing industries, allowing tailored filtration solutions for varying process requirements. Individual filters provide ease of installation, selective maintenance, and cost-effective replacement of worn components, enhancing their appeal for operations with frequent process changes.

• By Material Type

On the basis of material type, the self-cleaning filters market is segmented into carbon steel, stainless steel, reinforced plastic, and others. The stainless steel segment dominated the market in 2024, owing to its exceptional corrosion resistance, durability, and suitability for high-pressure and high-temperature applications. Stainless steel filters are widely used across pharmaceuticals, chemicals, and food processing industries due to their compliance with hygiene standards and long operational life. Their resistance to wear and ease of cleaning also contribute to reduced operational costs and improved process efficiency.

The reinforced plastic segment is expected to witness the fastest CAGR from 2025 to 2032, driven by lightweight, cost-effective, and corrosion-resistant properties. For instance, Eaton Corporation has introduced reinforced plastic self-cleaning filters suitable for water treatment and industrial chemical processes, offering easy handling and lower maintenance compared to metal-based alternatives. Reinforced plastic filters provide flexibility in design and installation, making them increasingly preferred in applications where weight and chemical resistance are critical.

• By Type

On the basis of type, the self-cleaning filters market is segmented into vertical and horizontal. The vertical segment dominated the market with a share of 62.5% in 2024, driven by its compact design, high filtration efficiency, and ability to handle large volumes in continuous flow operations. Vertical filters are particularly preferred in municipal water treatment and power generation sectors for their consistent performance and reduced footprint, which facilitates installation in constrained spaces.

The horizontal segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing adoption in industrial processes requiring ease of maintenance and filter replacement. For instance, Parker Hannifin offers horizontal self-cleaning filters for industrial water and chemical applications, allowing simplified cleaning and reduced downtime. Horizontal designs provide operational flexibility and enhanced access for inspection and maintenance, making them attractive for industries with frequent process variations.

• By Source

On the basis of source, the self-cleaning filters market is segmented into electrical and pneumatic. The electrical segment dominated the market in 2024, owing to precise automation, consistent cleaning cycles, and integration with advanced monitoring systems. Electrical self-cleaning filters are widely preferred in critical applications such as pharmaceuticals and chemicals, where precise control over filtration is essential to maintain product quality.

The pneumatic segment is expected to witness the fastest CAGR from 2025 to 2032, driven by its energy efficiency, simplicity, and suitability for remote or off-grid operations. For instance, Donaldson Company provides pneumatic self-cleaning filters for industrial dust and liquid separation, reducing reliance on external power sources. Pneumatic filters offer reliable cleaning cycles and minimal maintenance, which appeals to industries operating in areas with limited electrical infrastructure.

• By End Use

On the basis of end use, the self-cleaning filters market is segmented into municipal, chemicals and power, oil and gas, food and beverages, pharmaceuticals, textiles, paper and pulps, automotive, steel, marine, and others. The municipal segment dominated the market in 2024, driven by the growing demand for efficient water treatment solutions, stricter regulatory norms for potable water quality, and rising urbanization. Municipal authorities increasingly rely on self-cleaning filters for continuous, large-scale water purification with minimal manual intervention.

The chemicals and power segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by the rising need for process water filtration and wastewater treatment in chemical plants and power generation facilities. For instance, Veolia Water Technologies offers specialized self-cleaning filters to optimize cooling water and process water filtration in power plants, improving operational efficiency and reducing downtime. Industries in this sector value high-capacity, durable filters capable of handling varied water quality and chemical load, driving accelerated adoption.

Self Cleaning Filters Market Regional Analysis

- Asia-Pacific dominated the self cleaning filters market with the largest revenue share of over 44% in 2024, driven by rapid industrialization, increasing municipal water treatment projects, and the expanding chemical and power sectors

- The region’s cost-effective manufacturing ecosystem, growing adoption of automated filtration solutions, and rising infrastructure investments are accelerating market expansion

- Availability of skilled labor, supportive government initiatives for water and wastewater management, and rising demand across pharmaceuticals, food and beverages, and steel industries are contributing to increased consumption of self-cleaning filters

China Self-Cleaning Filters Market Insight

China held the largest share in the Asia-Pacific self-cleaning filters market in 2024, owing to its strong industrial base, extensive water treatment infrastructure, and expanding chemical and power industries. The country’s investments in smart and automated filtration systems, along with favorable government policies promoting industrial modernization, are major growth drivers. Demand is further bolstered by rapid urbanization, high manufacturing output, and increasing focus on environmental compliance and sustainable water management.

India Self-Cleaning Filters Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by expanding municipal water projects, rising investments in chemicals and power sectors, and growing industrial automation. Initiatives such as “Smart Cities” and government-led water treatment programs are strengthening the demand for self-cleaning filters. In addition, increasing focus on industrial wastewater management, growth in pharmaceutical and food processing industries, and rising adoption of advanced filtration solutions are contributing to robust market expansion.

Europe Self-Cleaning Filters Market Insight

The Europe self-cleaning filters market is expanding steadily, supported by stringent regulatory standards, emphasis on sustainable water treatment, and high adoption in pharmaceuticals, chemicals, and power industries. The region prioritizes energy-efficient and low-maintenance filtration solutions, particularly in municipal and industrial applications. Growing investments in smart filtration technologies, coupled with increasing focus on compliance and environmental sustainability, are further enhancing market growth.

Germany Self-Cleaning Filters Market Insight

Germany’s self-cleaning filters market is driven by its leadership in advanced industrial automation, high standards in water and wastewater treatment, and strong chemical and pharmaceutical industries. The country’s focus on R&D, innovative filtration technologies, and energy-efficient solutions fosters continuous market growth. Demand is particularly strong in municipal water treatment, power generation, and chemical manufacturing sectors.

U.K. Self-Cleaning Filters Market Insight

The U.K. market is supported by mature municipal infrastructure, growing industrial automation in chemicals and pharmaceuticals, and increasing investments in water and wastewater management. Focus on sustainable solutions, advanced filtration technologies, and regulatory compliance is encouraging adoption of self-cleaning filters. The market is further strengthened by collaborations between industrial operators, technology providers, and research institutions.

North America Self-Cleaning Filters Market Insight

North America is projected to grow at the fastest CAGR from 2025 to 2032, driven by increasing industrial automation, robust demand in chemicals, power, and municipal water sectors, and technological advancements in filtration systems. Strong focus on energy-efficient and low-maintenance solutions, rising industrial output, and government-led environmental initiatives are boosting demand. In addition, growing reshoring of chemical and industrial production and increasing adoption of automated filtration in water treatment are supporting market expansion.

U.S. Self-Cleaning Filters Market Insight

The U.S. accounted for the largest share in the North America market in 2024, underpinned by its extensive industrial base, advanced water treatment infrastructure, and strong chemical and pharmaceutical sectors. The country’s focus on innovation, regulatory compliance, and adoption of automated self-cleaning filtration systems is encouraging market growth. Presence of key players, well-established distribution networks, and ongoing investments in municipal and industrial filtration projects further solidify the U.S.’s leading position in the region.

Self Cleaning Filters Market Share

The self cleaning filters industry is primarily led by well-established companies, including:

- Eaton (U.S.)

- RUSSELL FINEX SIEVES AND FILTERS PVT LTD. (India)

- Forsta Filters (U.S.)

- CHENGDU FILTRASCALE CO., LTD (China)

- North Star Water Treatment Systems (U.S.)

- Amiad Water Systems Ltd. (Israel)

- ALFA LAVAL (Sweden)

- Rotorflush Filters Ltd (U.K.)

- Jiangsu YLD Water Processing Equipment Co. Ltd. (China)

- Russell Finex Ltd. (U.K.)

- HiFlux Filtration A/S (Denmark)

- Parker Hannifin Corp (U.S.)

- Edelflex S.A. (France)

- Orival Inc. (U.S.)

- Trinity Filtration Technologies Pvt. Ltd. (India)

- Lenntech B.V. (Netherlands)

- Baleen Filters Pty Limited (Australia)

- 3M (U.S.)

- HYDAC (Germany)

- Oxford Filtration Limited (U.K.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Self Cleaning Filters Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Self Cleaning Filters Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Self Cleaning Filters Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.