Global Semiconductor Chemical Vapor Deposition Equipment Market

Market Size in USD Billion

USD

5.34 Billion

USD

10.65 Billion

2025

2033

USD

5.34 Billion

USD

10.65 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.34 Billion | |

| USD 10.65 Billion | |

| % | |

|

Semiconductor Chemical Vapor Deposition Equipment Market Overview

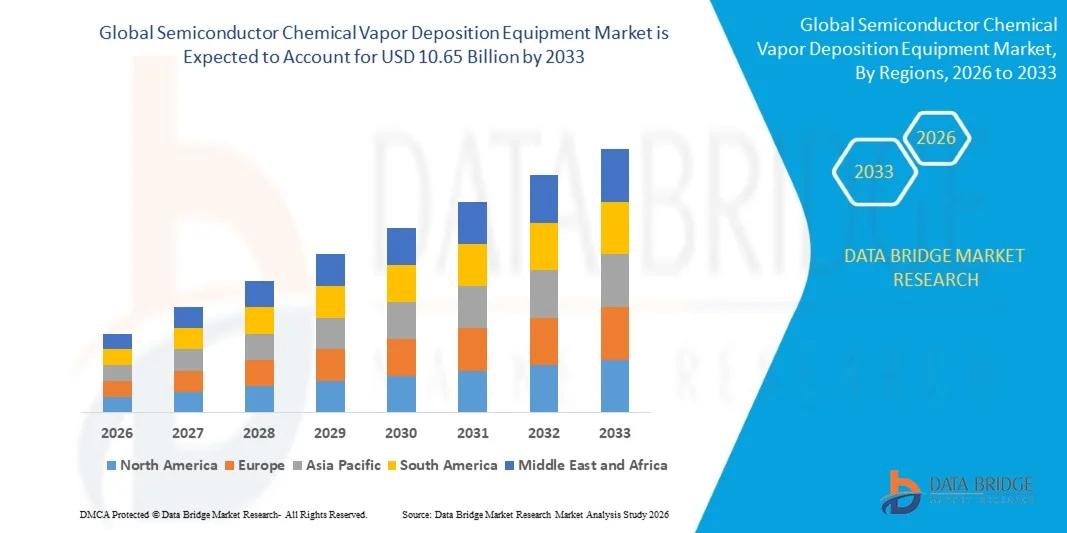

The global semiconductor chemical vapor deposition equipment market was valued at USD 5.34 billion in 2025 and is projected to reach USD 10.65 billion by 2033, growing at a CAGR of 9.00% from 2026 to 2033. The market is experiencing strong growth driven by rising demand for advanced semiconductor fabrication technologies, increasing production of high-performance integrated circuits, and expanding applications across artificial intelligence, automotive electronics, consumer devices, and high-performance computing systems.

The rapid transition toward smaller semiconductor nodes, combined with increasing investments in advanced wafer fabrication facilities globally, is compelling semiconductor manufacturers to adopt highly precise and efficient chemical vapor deposition equipment. Advanced CVD systems are increasingly being utilized for thin-film deposition in logic chips, memory devices, and power semiconductors, offering superior film uniformity, scalability, and process reliability. In addition, growing demand for electric vehicles, 5G infrastructure, and AI-driven computing is accelerating the need for advanced semiconductor manufacturing processes, supporting continuous innovation and expansion within the chemical vapor deposition equipment market.

Key Market Trends & Insights

- North America dominated the semiconductor chemical vapor deposition equipment market with the largest revenue share of 36.8% in 2025, supported by strong semiconductor manufacturing investments, presence of leading chipmakers, and increasing government initiatives promoting domestic semiconductor production and advanced wafer fabrication technologies.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 10.4% from 2026 to 2033. Growth is driven by rapid semiconductor manufacturing expansion, rising consumer electronics production, increasing investments in advanced fabrication plants, and strong government support for semiconductor self-sufficiency across China, Taiwan, South Korea, and Japan.

- The Low-pressure Chemical Vapor Deposition (LP CVD) segment held the largest market revenue share of approximately 39.4% in 2025 driven by its extensive use in advanced semiconductor fabrication processes requiring high film uniformity, excellent step coverage, and superior deposition precision. LP CVD systems are widely preferred in memory chip manufacturing, logic semiconductor production, and advanced wafer processing applications due to their ability to support high-volume and high-performance semiconductor manufacturing.

- The Metal-organic Chemical Vapor Phase Deposition (MO CVD) segment is projected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by increasing demand for compound semiconductors, LED manufacturing, and advanced optoelectronic devices. Rising adoption of gallium nitride and silicon carbide semiconductor technologies across electric vehicles, 5G infrastructure, and high-frequency communication systems is accelerating segment expansion.

- The Foundry segment held the largest market revenue share of approximately 46.8% in 2025 driven by continuous expansion of outsourced semiconductor manufacturing activities and increasing investments in advanced wafer fabrication facilities globally. Leading foundries are rapidly deploying advanced CVD systems to support production of AI processors, high-performance computing chips, and next-generation mobile semiconductors at advanced process nodes.

- The Memory Manufacturers segment is projected to register the fastest growth at a CAGR of 10.9% from 2026 to 2033, driven by rising demand for NAND flash, DRAM, and high-bandwidth memory solutions required for AI servers, cloud computing, and data center infrastructure. Increasing multilayer memory architectures and transition toward advanced semiconductor packaging technologies are further accelerating demand for precision deposition equipment across memory fabrication facilities.

Market Size & Forecast

- Global Market Value (2025): USD 5.34 Billion

- Expected Market Value (2033): USD 10.65 Billion

- Forecast CAGR (2026–2033): 9.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Semiconductor Chemical Vapor Deposition Equipment Market Segmentation

|

Attributes |

Semiconductor Chemical Vapor Deposition Equipment Key Market Insights |

|

Segments Covered |

· By Product Type: Atmospheric-Pressure Chemical Vapor Deposition (AP CVD), Density-Plasma Chemical Vapor Deposition (DP CVD), Low-pressure Chemical Vapor Deposition (LP CVD), and Metal-organic Chemical Vapor Phase Deposition (MO CVD) · By End User: Foundry, Memory Manufacturers, IDMs, and Other |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• AIXTRON (Germany) |

|

Market Opportunities |

• Increasing Investments In Advanced Semiconductor Fabrication Facilities |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Global Semiconductor Chemical Vapor Deposition Equipment Market Trends

Trend: Growth In Advanced AI Chips And High-Precision Thin Film Deposition Technologies

Increasing demand for high-performance semiconductor devices across artificial intelligence, automotive electronics, 5G infrastructure, and advanced computing applications is accelerating adoption of advanced chemical vapor deposition equipment. Conventional semiconductor fabrication technologies face limitations in achieving ultra-thin, highly uniform film deposition at advanced process nodes, encouraging manufacturers to deploy next-generation CVD systems capable of delivering superior precision, scalability, and process efficiency.

Leading semiconductor foundries are increasingly integrating advanced plasma-enhanced and low-pressure CVD systems, For instance for deposition of dielectric, conductive, and insulating thin films in sub-5nm chip manufacturing processes, to improve transistor performance and wafer yield. In memory manufacturing, NAND and DRAM producers are utilizing atomic-level deposition technologies to support increasing chip density and multilayer architectures required for AI and data center applications.

The rapid expansion of AI-driven computing infrastructure and electric vehicle electronics is also increasing demand for advanced semiconductor fabrication equipment capable of handling high-volume production with minimal defect rates. In addition, aerospace and defense sectors continue to rely on advanced semiconductor components for radar, communication, and autonomous systems requiring highly reliable thin-film deposition processes. Industry expansion projects announced during 2025 across Taiwan, South Korea, and the U.S. integrating advanced CVD systems into new wafer fabrication plants are expected to improve wafer processing efficiency by nearly 10–14% under high-volume manufacturing conditions

Global Semiconductor Chemical Vapor Deposition Equipment Market Dynamics

Key Market Driver: Rising Investments In Advanced Semiconductor Manufacturing Facilities

Governments and semiconductor manufacturers worldwide are significantly increasing investments in advanced wafer fabrication facilities to strengthen domestic chip production capacity and reduce supply chain dependency. Growing global demand for high-performance processors, AI accelerators, automotive chips, and memory devices is creating strong demand for highly precise deposition technologies essential for advanced semiconductor fabrication.

Semiconductor companies are increasingly deploying advanced chemical vapor deposition equipment to support production of smaller and more complex integrated circuits with improved power efficiency and processing capabilities. Leading foundries and integrated device manufacturers are expanding fabrication facilities, For instance in the U.S., Taiwan, South Korea, and Europe, to meet rising demand for next-generation semiconductor technologies.

Similarly, increasing deployment of AI servers and advanced data centers is accelerating demand for high-density semiconductor devices requiring sophisticated thin-film deposition processes. Real-world fab expansion projects announced during 2024 by major chip manufacturers demonstrated planned investments exceeding USD 100 billion collectively in advanced semiconductor manufacturing infrastructure, significantly increasing demand for CVD equipment across global markets

Key Restraint/Challenge: High Equipment Costs And Process Complexity

Advanced semiconductor chemical vapor deposition systems require highly specialized manufacturing environments, precision engineering, and complex process integration, significantly increasing equipment acquisition and operational costs. The transition toward smaller semiconductor nodes and multilayer chip architectures further increases technical complexity and maintenance requirements for deposition equipment.

In addition, high capital expenditure requirements for cleanroom facilities, advanced process control systems, and skilled technical workforce create affordability challenges for smaller semiconductor manufacturers and emerging economies. Stringent contamination control standards and increasing process variability at advanced nodes also limit operational scalability and increase production risks.

Commercial semiconductor fabrication benchmarking studies indicate that advanced CVD equipment used in sub-5nm manufacturing environments can cost several million dollars per production unit, while overall wafer fabrication facility investments often exceed USD 10–20 billion for leading-edge semiconductor production plants

Key Market Opportunity: Expansion Of AI, Electric Vehicle, And 5G Semiconductor Applications

Rapid growth in artificial intelligence, autonomous vehicles, 5G communication infrastructure, and high-performance computing is creating substantial opportunities for semiconductor chemical vapor deposition equipment manufacturers. Modern semiconductor devices increasingly require ultra-thin and defect-free film deposition processes to support higher transistor density, lower power consumption, and improved thermal performance.

Automotive semiconductor manufacturers are increasingly utilizing advanced deposition technologies, For instance for power semiconductors and EV battery management chips, to improve energy efficiency and operational reliability in electric vehicles. In consumer electronics and AI processors, rising chip complexity and thermal density are accelerating demand for advanced deposition equipment capable of supporting high-performance logic and memory production.

In addition, advancements in atomic layer deposition integration, plasma-enhanced processing, and hybrid semiconductor manufacturing technologies are improving deposition precision and throughput, opening opportunities across advanced packaging, photonics, and quantum computing applications in Asia-Pacific and North America. Semiconductor manufacturing expansion programs announced during 2025 across Japan and the U.S. reported expected wafer output increases of approximately 15–20% after integrating advanced CVD systems into high-volume production lines.

Global Semiconductor Chemical Vapor Deposition Equipment Market Scope

The market is segmented on the basis of product type and end user.

- By Product Type

On the basis of product type, the semiconductor chemical vapor deposition equipment market is segmented into Atmospheric-Pressure Chemical Vapor Deposition (AP CVD), Density-Plasma Chemical Vapor Deposition (DP CVD), Low-pressure Chemical Vapor Deposition (LP CVD), and Metal-organic Chemical Vapor Phase Deposition (MO CVD). The Low-pressure Chemical Vapor Deposition (LP CVD) segment held the largest market revenue share of approximately 39.4% in 2025 driven by its extensive use in advanced semiconductor fabrication processes requiring high film uniformity, excellent step coverage, and superior deposition precision. LP CVD systems are widely preferred in memory chip manufacturing, logic semiconductor production, and advanced wafer processing applications due to their ability to support high-volume and high-performance semiconductor manufacturing.

The Metal-organic Chemical Vapor Phase Deposition (MO CVD) segment is projected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by increasing demand for compound semiconductors, LED manufacturing, and advanced optoelectronic devices. Rising adoption of gallium nitride and silicon carbide semiconductor technologies across electric vehicles, 5G infrastructure, and high-frequency communication systems is accelerating segment expansion.

- By End User

On the basis of end user, the semiconductor chemical vapor deposition equipment market is segmented into Foundry, Memory Manufacturers, IDMs, and Other. The Foundry segment held the largest market revenue share of approximately 46.8% in 2025 driven by continuous expansion of outsourced semiconductor manufacturing activities and increasing investments in advanced wafer fabrication facilities globally. Leading foundries are rapidly deploying advanced CVD systems to support production of AI processors, high-performance computing chips, and next-generation mobile semiconductors at advanced process nodes.

The Memory Manufacturers segment is projected to register the fastest growth at a CAGR of 10.9% from 2026 to 2033, driven by rising demand for NAND flash, DRAM, and high-bandwidth memory solutions required for AI servers, cloud computing, and data center infrastructure. Increasing multilayer memory architectures and transition toward advanced semiconductor packaging technologies are further accelerating demand for precision deposition equipment across memory fabrication facilities.

Global Semiconductor Chemical Vapor Deposition Equipment Market Regional Analysis

North America Semiconductor Chemical Vapor Deposition Equipment Market Insight

North America dominated the semiconductor chemical vapor deposition equipment market with the largest revenue share of 36.8% in 2025, supported by strong semiconductor manufacturing investments, rapid expansion of AI and high-performance computing infrastructure, and increasing government support for domestic chip production. The region benefits from the presence of leading semiconductor companies, advanced research facilities, and significant investments in next-generation wafer fabrication plants. Growing adoption of advanced deposition technologies for AI processors, automotive semiconductors, and defense electronics is further strengthening regional market growth.

U.S. Semiconductor Chemical Vapor Deposition Equipment Market Insight

The U.S. semiconductor chemical vapor deposition equipment market captured the largest revenue share in 2025 within North America, fueled by large-scale investments in semiconductor fabrication facilities and increasing demand for advanced chip manufacturing technologies. Semiconductor manufacturers are rapidly expanding production capacities to support AI computing, cloud infrastructure, automotive electronics, and 5G applications. The growing implementation of advanced process nodes and increasing integration of high-performance logic and memory chips are significantly contributing to the expansion of the CVD equipment industry in the country.

Europe Semiconductor Chemical Vapor Deposition Equipment Market Insight

The Europe semiconductor chemical vapor deposition equipment market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing investments in semiconductor self-sufficiency initiatives and growing demand for automotive and industrial semiconductors. The region’s strong automotive manufacturing ecosystem and rising adoption of electric vehicles are increasing demand for advanced semiconductor devices and wafer fabrication technologies. European governments are also supporting domestic semiconductor production through funding programs and strategic technology partnerships.

U.K. Semiconductor Chemical Vapor Deposition Equipment Market Insight

The U.K. semiconductor chemical vapor deposition equipment market is expected to witness steady growth from 2026 to 2033, driven by rising investments in semiconductor R&D, AI infrastructure, and advanced electronics manufacturing. The country’s growing focus on chip design innovation, quantum computing, and next-generation communication technologies is accelerating adoption of advanced semiconductor processing equipment. In addition, collaboration between universities, technology firms, and semiconductor research centers is supporting market development.

Germany Semiconductor Chemical Vapor Deposition Equipment Market Insight

The Germany semiconductor chemical vapor deposition equipment market is expected to witness strong growth from 2026 to 2033, fueled by increasing demand for automotive semiconductors, industrial automation technologies, and energy-efficient electronic systems. Germany’s advanced manufacturing infrastructure and emphasis on Industry 4.0 are encouraging semiconductor companies to adopt high-precision deposition equipment for advanced chip production. Rising investments in electric vehicle supply chains and power semiconductor technologies are further supporting market expansion.

Asia-Pacific Semiconductor Chemical Vapor Deposition Equipment Market Insight

The Asia-Pacific semiconductor chemical vapor deposition equipment market is expected to witness the fastest growth rate from 2026 to 2033, supported by strong semiconductor manufacturing expansion, increasing consumer electronics production, and rising investments in advanced wafer fabrication facilities across China, Taiwan, South Korea, and Japan. The region’s dominance in semiconductor supply chains and increasing adoption of AI, 5G, and smart electronics are driving demand for advanced deposition technologies. Government incentives supporting domestic semiconductor manufacturing are also accelerating market growth.

Japan Semiconductor Chemical Vapor Deposition Equipment Market Insight

The Japan semiconductor chemical vapor deposition equipment market is expected to witness significant growth from 2026 to 2033 due to the country’s strong semiconductor equipment manufacturing capabilities and increasing investments in advanced electronics and automotive technologies. Japan continues to focus on high-precision semiconductor production and advanced material innovation for next-generation chip manufacturing. The integration of advanced CVD technologies in memory devices, sensors, and power semiconductors is further fueling market expansion.

China Semiconductor Chemical Vapor Deposition Equipment Market Insight

The China semiconductor chemical vapor deposition equipment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid semiconductor manufacturing expansion, strong government support for domestic chip production, and increasing investments in advanced fabrication facilities. China remains one of the largest electronics manufacturing hubs globally, creating strong demand for advanced semiconductor processing equipment. The country’s focus on semiconductor self-reliance, AI chip development, and high-volume consumer electronics production is significantly propelling the market growth.

Global Semiconductor Chemical Vapor Deposition Equipment Market Share

The Semiconductor Chemical Vapor Deposition Equipment industry is primarily led by well-established companies, including:

• AIXTRON (Germany)

• Veeco Instruments Inc (U.S.)

• ASM International (Netherlands)

• Tokyo Electron Limited (Japan)

• CVD Equipment Corporation (U.S.)

• LAM RESEARCH CORPORATION (U.S.)

• Applied Materials, Inc. (U.S.)

• Hitachi Kokusai Electric Inc (Japan)

• Plasma-Therm (U.S.)

• ADEKA CORPORATION (Japan)

Latest Developments in Global Semiconductor Chemical Vapor Deposition Equipment Market

- In September 2023, Gallium Semiconductor launched the GTH2e-2425300P ISM CW amplifier featuring GaN-on-SiC HEMT technology for high-efficiency industrial and semiconductor applications. The amplifier delivers 300W power output in the 2.4–2.5GHz range and is designed for semiconductor plasma sources and microwave plasma chemical vapor deposition equipment used in synthetic diamond manufacturing. This development strengthens high-performance semiconductor processing capabilities while improving operational efficiency and reliability across advanced manufacturing environments.

- In May 2023, FUJIFILM Corporation acquired the semiconductor high purity process chemicals business of KMG Corporation for USD 700 million to expand its electronic materials portfolio. The acquisition enhanced Fujifilm’s capabilities in semiconductor wafer etching and cleaning solutions critical for advanced chip manufacturing. This strategic move strengthened the company’s position in the growing semiconductor chemicals market while supporting increasing global demand for high-performance semiconductor fabrication materials.

- In October 2021, Oxford Instruments, in collaboration with Industrial Technology Research Institute (ITRI), introduced advanced GaN MISHEMT technology designed to improve performance of Gallium Nitride high electron mobility transistors. The new architecture enables higher voltage operation, enhanced energy efficiency, and improved reliability for applications across electric vehicles, data centers, and 5G infrastructure. This innovation supports next-generation semiconductor device development while accelerating adoption of advanced power electronics technologies globally.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Semiconductor Chemical Vapor Deposition Equipment Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Semiconductor Chemical Vapor Deposition Equipment Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Semiconductor Chemical Vapor Deposition Equipment Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.