Global Sezary Syndrome Treatment Market

Market Size in USD Million

USD

476.50 Million

USD

714.80 Million

2025

2033

USD

476.50 Million

USD

714.80 Million

2025

2033

| 2026 - 2033 | |

| USD 476.50 Million | |

| USD 714.80 Million | |

| % | |

|

Sezary Syndrome Treatment Market Size

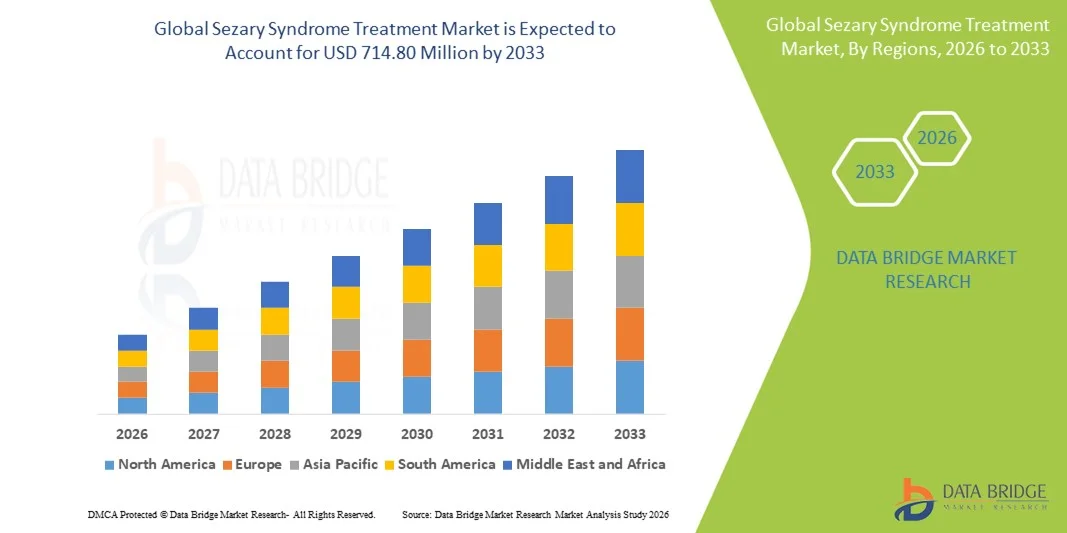

- The global Sezary Syndrome Treatment market size was valued at USD 476.5 Million in 2025 and is expected to reach USD 714.80 Million by 2033, at a CAGR of 5.20% during the forecast period

- The market growth is largely fueled by increasing awareness of rare cutaneous T-cell lymphomas and ongoing advancements in targeted and immunotherapy-based treatment options, leading to improved diagnosis rates and expanded treatment adoption across oncology and dermatology care settings

- Furthermore, rising demand for effective, personalized, and less toxic treatment approaches for Sezary syndrome is establishing advanced biologics, monoclonal antibodies, and combination therapies as preferred treatment modalities. These converging factors are accelerating the uptake of Sezary syndrome treatment solutions, thereby significantly boosting overall market growth

Sezary Syndrome Treatment Market Analysis

- Sezary syndrome treatments, which include immunotherapies, targeted therapies, and systemic chemotherapies, are increasingly vital components of modern oncology care due to their role in managing this aggressive and rare cutaneous T-cell lymphoma and improving patient survival and quality of life

- The escalating demand for Sezary syndrome treatments is primarily fueled by rising awareness of rare hematologic malignancies, increasing diagnostic accuracy, and continuous advancements in biologics and immune-modulating therapies that offer improved efficacy with reduced toxicity

- North America dominated the Sezary Syndrome Treatment market with the largest revenue share of approximately 41.6% in 2025, supported by strong oncology research infrastructure, high adoption of novel therapies, favorable reimbursement frameworks, and the presence of leading pharmaceutical companies, with the U.S. accounting for the majority of regional demand

- Asia-Pacific is expected to be the fastest-growing region in the Sezary Syndrome Treatment market during the forecast period, registering a CAGR of approximately 18.9%, driven by improving cancer diagnosis capabilities, expanding access to specialty oncology care, and rising healthcare investments across emerging economies

- The parenteral segment dominated the largest market revenue share of approximately 55.6% in 2025, driven by widespread use of injectable biologics and infusion-based therapies

Report Scope and Sezary Syndrome Treatment Market Segmentation

|

Attributes |

Sezary Syndrome Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Sezary Syndrome Treatment Market Trends

Advancements in Targeted Therapies and Personalized Treatment Approaches

- A significant and accelerating trend in the global Sezary syndrome treatment market is the growing adoption of targeted therapies and personalized medicine approaches aimed at improving clinical outcomes and minimizing systemic toxicity

- These therapies focus on specific molecular pathways involved in disease progression, enabling more precise treatment strategies

- For instance, histone deacetylase (HDAC) inhibitors such as vorinostat and romidepsin are increasingly used in the management of Sezary syndrome due to their ability to selectively target malignant T-cells while preserving normal immune function

- Immunotherapy is also gaining traction, with monoclonal antibodies and immune-modulating agents demonstrating improved response rates in patients with advanced or refractory disease. Drugs such as mogamulizumab, a CCR4-targeting monoclonal antibody, have shown significant efficacy in reducing circulating malignant cells

- In addition, advancements in combination therapy regimens, integrating systemic therapies with skin-directed treatments such as photopheresis, are enhancing disease control and improving patient quality of life

- This shift toward more effective, patient-specific treatment protocols is reshaping clinical management strategies and driving ongoing research and development efforts across the Sezary syndrome treatment landscape

Sezary Syndrome Treatment Market Dynamics

Driver

Rising Disease Awareness and Increasing Diagnosis of Cutaneous T-Cell Lymphomas

- The increasing awareness of rare hematological malignancies, including Sezary syndrome, along with improvements in diagnostic techniques, is a key driver fueling market growth

- For instance, the expanded use of advanced immunophenotyping, flow cytometry, and molecular diagnostic tools has enabled earlier and more accurate diagnosis of Sezary syndrome, leading to timely initiation of treatment

- The rising prevalence of cutaneous T-cell lymphomas (CTCLs), particularly among aging populations, is further contributing to the growing demand for effective treatment options

- In addition, improved access to specialized oncology and dermatology centers, particularly in developed regions, is supporting greater adoption of advanced therapeutic interventions

- Ongoing clinical trials and increased investment by pharmaceutical companies in rare cancer research are also accelerating the development and availability of novel therapies for Sezary syndrome

Restraint/Challenge

High Treatment Costs and Limited Availability of Approved Therapies

- One of the major challenges restraining the Sezary syndrome treatment market is the high cost associated with advanced therapies, including biologics and targeted agents, which can limit patient access, particularly in low- and middle-income regions

- For instance, treatments such as monoclonal antibody therapies and novel immunomodulators often require prolonged administration and specialized clinical settings, increasing overall treatment expenses

- The limited number of FDA- and EMA-approved drugs specifically indicated for Sezary syndrome also restricts treatment choices and can delay optimal disease management

- Furthermore, variability in reimbursement policies across regions and the lack of standardized treatment guidelines for this rare disease pose additional barriers to widespread adoption

- Overcoming these challenges through expanded clinical research, broader regulatory approvals, improved reimbursement frameworks, and increased awareness initiatives will be critical for sustaining long-term market growth

Sezary Syndrome Treatment Market Scope

The market is segmented on the basis of diagnosis, treatment type, drugs, route of administration, end users, and distribution channel.

- By Diagnosis

On the basis of diagnosis, the Sezary Syndrome Treatment market is segmented into immunophenotyping, T-cell receptor (TCR) gene rearrangement test, and others. The immunophenotyping segment dominated the largest market revenue share of approximately 46.7% in 2025, owing to its critical role in the definitive diagnosis of Sezary syndrome through flow cytometric analysis. Immunophenotyping enables precise identification of malignant circulating T-cells by evaluating surface markers such as CD4 positivity and loss of CD7 or CD26 expression. This diagnostic method is widely adopted in tertiary hospitals and oncology laboratories due to its rapid turnaround time and reproducibility. Clinicians rely heavily on immunophenotyping for both initial diagnosis and disease staging. The technique also supports treatment response monitoring, which increases repeat testing frequency. Strong availability of flow cytometry infrastructure in developed healthcare systems further strengthens adoption. Increasing awareness of early diagnosis of cutaneous T-cell lymphomas also contributes to growth. Integration with automated laboratory platforms improves efficiency. Favorable reimbursement policies for flow cytometry diagnostics support revenue generation. The method’s reliability across disease stages ensures consistent utilization. Rising incidence of rare lymphomas further sustains demand. Consequently, immunophenotyping remained the dominant diagnostic approach in 2025.

The T-cell receptor (TCR) gene rearrangement test segment is expected to witness the fastest CAGR of around 11.9% from 2026 to 2033, driven by increasing adoption of molecular diagnostics in oncology. TCR gene rearrangement testing allows confirmation of clonality in malignant T-cell populations, which is crucial in ambiguous or early-stage cases. Growing emphasis on precision medicine encourages molecular confirmation of diagnosis. Advances in PCR and next-generation sequencing technologies enhance test sensitivity and accuracy. Increasing availability of molecular pathology laboratories supports adoption. Clinical guidelines increasingly recommend TCR testing alongside immunophenotyping. Rising research funding in hematologic malignancies accelerates usage. The test is also used for disease monitoring and relapse detection. Expanding awareness among dermatologists and oncologists boosts demand. Declining costs of molecular testing improve accessibility. Adoption is increasing in academic and research hospitals. As a result, the TCR gene rearrangement segment is projected to grow rapidly.

- By Treatment Type

On the basis of treatment type, the Sezary Syndrome Treatment market is segmented into standard treatment and advanced treatment. The standard treatment segment accounted for the largest market revenue share of about 52.4% in 2025, driven by the continued use of conventional therapeutic approaches such as extracorporeal photopheresis, systemic corticosteroids, interferon therapy, and traditional chemotherapy. These treatments are widely accepted as first-line therapy due to long-standing clinical evidence and established treatment protocols. Physicians often initiate standard treatments immediately after diagnosis to control symptoms such as erythroderma and pruritus. Standard therapies are more accessible in both developed and developing regions. Lower treatment costs compared to biologics support widespread adoption. Hospitals are well equipped to deliver these therapies efficiently. Availability of reimbursement for conventional treatments further strengthens demand. Standard treatments are frequently used in combination regimens, increasing utilization. Familiarity among clinicians enhances prescription rates. Patient tolerance and predictable safety profiles support continued use. Long-term clinical experience reinforces confidence. Hence, standard treatment remains the dominant segment.

The advanced treatment segment is anticipated to register the fastest CAGR of approximately 13.6% from 2026 to 2033, driven by increasing adoption of targeted therapies, immunotherapies, and biologics. Advanced treatments offer improved disease control and better progression-free survival outcomes. Growing R&D investments in rare hematologic malignancies support pipeline expansion. Regulatory approvals for novel monoclonal antibodies accelerate market penetration. Patients increasingly prefer advanced therapies due to better tolerability profiles. Personalized medicine trends encourage targeted treatment approaches. Advanced therapies are gaining traction in second-line and refractory cases. Increased clinical trial activity boosts awareness and adoption. Expanding insurance coverage for biologics supports growth. Improved survival outcomes strengthen physician confidence. Uptake is particularly strong in developed healthcare markets. Consequently, advanced treatment is expected to grow rapidly.

- By Drugs

On the basis of drugs, the Sezary Syndrome Treatment market is segmented into vorinostat, mogamulizumab, and others. The vorinostat segment dominated the largest market revenue share of nearly 38.9% in 2025, driven by its established role as an HDAC inhibitor in cutaneous T-cell lymphoma management. Vorinostat is widely prescribed due to its oral route of administration and proven efficacy in relapsed or refractory cases. Strong physician familiarity contributes to sustained demand. The drug’s ability to alleviate severe pruritus improves patient quality of life. Long-standing regulatory approval supports global availability. Generic formulations enhance affordability and accessibility. Vorinostat is commonly included in combination therapy regimens. Favorable clinical trial outcomes reinforce confidence. Consistent inclusion in treatment guidelines strengthens utilization. High prescription volume supports revenue share. Availability across hospital and retail pharmacies increases reach. Therefore, vorinostat remains the leading drug segment.

The mogamulizumab segment is expected to witness the fastest CAGR of approximately 15.2% from 2026 to 2033, driven by its targeted action against CCR4-expressing malignant T-cells. Mogamulizumab has demonstrated superior efficacy in advanced and refractory Sezary syndrome cases. Increasing regulatory approvals across regions expand patient access. Growing adoption in second-line therapy supports growth. Strong clinical evidence enhances physician confidence. Expansion of biologics manufacturing improves supply stability. Rising preference for targeted immunotherapies accelerates uptake. Improved safety and efficacy profiles drive demand. Increasing reimbursement coverage supports affordability. Adoption is rising in specialty oncology centers. Ongoing clinical studies further expand indications. As a result, mogamulizumab is projected to grow rapidly.

- By Route of Administration

On the basis of route of administration, the Sezary Syndrome Treatment market is segmented into oral and parenteral. The parenteral segment dominated the largest market revenue share of approximately 55.6% in 2025, driven by widespread use of injectable biologics and infusion-based therapies. Most advanced treatments require intravenous administration in controlled settings. Hospitals prefer parenteral administration for severe disease cases. Controlled dosing improves therapeutic outcomes. Higher bioavailability supports effectiveness. Infusion centers facilitate treatment delivery. Parenteral therapies are commonly used in combination regimens. Strong clinical supervision ensures safety. Availability of trained healthcare professionals supports usage. Established reimbursement mechanisms favor hospital-based administration. High patient volume sustains revenue. Thus, parenteral administration remains dominant.

The oral segment is expected to grow at the fastest CAGR of around 12.8% from 2026 to 2033, driven by increasing patient preference for convenient at-home therapy. Oral drugs reduce hospital visits and treatment burden. Improved compliance supports better outcomes. Expansion of homecare oncology services boosts adoption. Growing development of oral targeted therapies supports pipeline growth. Lower administration costs enhance affordability. Telemedicine adoption complements oral therapy usage. Oral therapies offer greater flexibility. Improved safety profiles increase acceptance. Availability through retail and online pharmacies expands reach. Rising chronic disease management trends support growth. Hence, oral administration is growing rapidly.

- By End Users

On the basis of end users, the Sezary Syndrome Treatment market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the largest market revenue share of about 44.3% in 2025, driven by the complexity of disease management and need for multidisciplinary care. Hospitals provide advanced diagnostics and infusion facilities. Severe cases require inpatient monitoring. Availability of oncologists and dermatologists supports dominance. Hospitals manage clinical trials, increasing drug usage. Strong reimbursement structures favor hospital treatment. Access to advanced therapies boosts demand. High patient inflow supports revenue growth. Hospitals ensure comprehensive disease management. Presence of specialized oncology units strengthens adoption. Government and private funding supports infrastructure. Therefore, hospitals remain the leading end user.

The specialty clinics segment is expected to witness the fastest CAGR of approximately 13.1% from 2026 to 2033, driven by growth of dermatology-oncology specialty centers. Clinics offer focused expertise and personalized care. Shorter waiting times attract patients. Outpatient treatment adoption supports growth. Clinics increasingly administer advanced therapies. Rising private investment supports clinic expansion. Improved diagnostic capabilities enhance utilization. Growing patient preference for specialized care boosts demand. Expansion in urban areas supports growth. Integration of telemedicine improves access. Increasing disease awareness fuels clinic visits. Thus, specialty clinics are growing rapidly.

- By Distribution Channel

On the basis of distribution channel, the Sezary Syndrome Treatment market is segmented into hospital pharmacy, online pharmacy, retailers, and others. The hospital pharmacy segment held the largest market revenue share of approximately 49.5% in 2025, driven by high dispensing of specialty oncology drugs. Hospital pharmacies manage storage of biologics. Integration with inpatient services supports dominance. Controlled dispensing ensures safety. High-cost drugs are primarily distributed through hospitals. Strong procurement contracts enhance revenue. Regulatory compliance favors hospital distribution. Close coordination with physicians supports usage. High patient dependency sustains demand. Inventory management efficiency boosts adoption. Reimbursement alignment supports growth. Hence, hospital pharmacies dominate.

The online pharmacy segment is expected to register the fastest CAGR of about 14.4% from 2026 to 2033, driven by increasing digital healthcare adoption. Online platforms improve access to oral medications. Teleconsultation growth supports e-pharmacy usage. Convenience and home delivery attract patients. Price transparency enhances affordability. Expansion in emerging markets fuels growth. Regulatory frameworks are becoming supportive. Improved logistics ensure timely delivery. Rising chronic therapy demand boosts volume. Patient preference for privacy supports adoption. Technology integration improves experience. Consequently, online pharmacies are expanding rapidly.

Sezary Syndrome Treatment Market Regional Analysis

- North America dominated the Sezary syndrome treatment market with the largest revenue share of approximately 41.6% in 2025, supported by a strong oncology research infrastructure, high adoption of novel and targeted therapies, favorable reimbursement frameworks, and the presence of leading pharmaceutical companies

- The region benefits from well-established healthcare systems and advanced diagnostic capabilities, enabling early and accurate identification of rare hematologic malignancies such as Sezary syndrome

- Continuous investments in cancer research, coupled with a high level of awareness among healthcare professionals, further strengthen the market position of North America

U.S. Sezary Syndrome Treatment Market Insight

The U.S. Sezary syndrome treatment market accounted for the majority of the regional demand within North America in 2025, driven by robust clinical research activity and widespread access to advanced treatment options. The country has a strong concentration of specialized oncology and dermatology centers that actively adopt innovative therapies, including monoclonal antibodies and immunomodulatory drugs. Favorable reimbursement policies and strong participation in clinical trials are accelerating the adoption of emerging Sezary syndrome treatments, contributing significantly to market growth.

Europe Sezary Syndrome Treatment Market Insight

The Europe Sezary syndrome treatment market is projected to expand at a substantial CAGR during the forecast period, driven by increasing awareness of cutaneous T-cell lymphomas and rising emphasis on early cancer diagnosis. The region’s well-developed public healthcare systems and growing adoption of advanced oncology therapies are supporting market expansion. Ongoing research initiatives and collaborations between academic institutions and pharmaceutical companies are also enhancing the availability of treatment options across Europe.

U.K. Sezary Syndrome Treatment Market Insight

The U.K. Sezary syndrome treatment market is anticipated to grow at a noteworthy CAGR, supported by increasing focus on rare cancer management and improved access to specialized oncology care. Government-backed healthcare programs and rising awareness among clinicians regarding advanced therapeutic approaches are driving market growth. The expansion of diagnostic services and participation in international clinical trials are further supporting the adoption of innovative treatment options in the country.

Germany Sezary Syndrome Treatment Market Insight

Germany Sezary syndrome treatment market is expected to witness considerable growth in the Sezary syndrome treatment market during the forecast period, fueled by strong healthcare infrastructure and high investment in medical research. The country’s emphasis on precision medicine and oncology innovation is promoting the adoption of targeted therapies for rare hematologic malignancies. In addition, increasing collaboration between research institutions and pharmaceutical manufacturers is supporting the development and availability of advanced treatment options.

Asia-Pacific Sezary Syndrome Treatment Market Insight

Asia-Pacific Sezary syndrome treatment market is expected to be the fastest-growing region in the Sezary syndrome treatment market during the forecast period, registering a CAGR of approximately 18.9%. This rapid growth is driven by improving cancer diagnosis capabilities, expanding access to specialty oncology care, and rising healthcare investments across emerging economies. Increasing awareness of rare lymphomas, coupled with improvements in healthcare infrastructure, is accelerating early diagnosis and treatment adoption across the region.

Japan Sezary Syndrome Treatment Market Insight

Japan’s Sezary syndrome treatment market is gaining momentum due to advancements in oncology research and a growing focus on personalized medicine. The country’s aging population and increasing prevalence of cancer-related conditions are driving demand for effective treatment options. Strong regulatory support and continuous innovation in pharmaceutical development are further enhancing market growth in Japan.

China Sezary Syndrome Treatment Market Insight

China Sezary syndrome treatment market accounted for the largest revenue share in the Asia-Pacific Sezary syndrome treatment market in 2025, supported by rising healthcare expenditure and expanding oncology care infrastructure. Increasing government initiatives to improve cancer diagnosis and treatment access, along with growing participation in clinical research, are driving market growth. The rapid expansion of specialized cancer hospitals and increasing availability of advanced therapies are further strengthening China’s position in the regional market.

Sezary Syndrome Treatment Market Share

The Sezary Syndrome Treatment industry is primarily led by well-established companies, including:

- Johnson & Johnson (U.S.)

- Bristol Myers Squibb (U.S.)

- Merck & Co., Inc. (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Novartis AG (Switzerland)

- AbbVie Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Kyowa Kirin Co., Ltd. (Japan)

- Eisai Co., Ltd. (Japan)

- Seattle Genetics (U.S.)

- Celgene Corporation (U.S.)

- Takeda Pharmaceutical Company (Japan)

- AstraZeneca (U.K.)

- Amgen Inc. (U.S.)

- Incyte Corporation (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories (India)

- Cipla Limited (India)

Latest Developments in Global Sezary Syndrome Treatment Market

- In January 2025, Kyowa Kirin International and Swixx BioPharma announced that the Croatian National Health Insurance Fund and Bulgaria’s Ministry of Health approved reimbursement for POTELIGEO (mogamulizumab) for adults with mycosis fungoides and Sézary syndrome, marking a significant expansion of access to this key biologic therapy in Central and Eastern Europe following earlier inclusion in the Polish Ministry of Health’s Drug Programme. This expansion increased patient access to one of the few approved systemic therapies for Sézary syndrome and reflects broader efforts to improve treatment availability across European markets

- In May 2025, Innate Pharma presented long-term follow-up data from the Phase II TELLOMAK clinical trial evaluating lacutamab in patients with Sézary syndrome and mycosis fungoides at the ASCO Annual Meeting 2025, demonstrating meaningful clinical activity in heavily pretreated Sézary syndrome patients with a global overall response rate of 42.9% and durable responses lasting a median of 25.6 months. These data underpin ongoing development and the potential for lacutamab to address unmet needs in this rare and aggressive form of cutaneous T-cell lymphoma

- In February 2025, the U.S. Food and Drug Administration (FDA) granted Breakthrough Therapy Designation to lacutamab, an anti-KIR3DL2 monoclonal antibody, for the treatment of adult patients with relapsed or refractory Sézary syndrome following at least two prior systemic therapies, a regulatory milestone designed to accelerate lacutamab’s development and review given promising early clinical results in this difficult-to-treat population

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.