Global Short Bowel Syndrome Drugs Market

Market Size in USD Billion

USD

2.51 Billion

USD

7.67 Billion

2025

2033

USD

2.51 Billion

USD

7.67 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.51 Billion | |

| USD 7.67 Billion | |

| % | |

|

Short Bowel Syndrome Drugs Market Overview

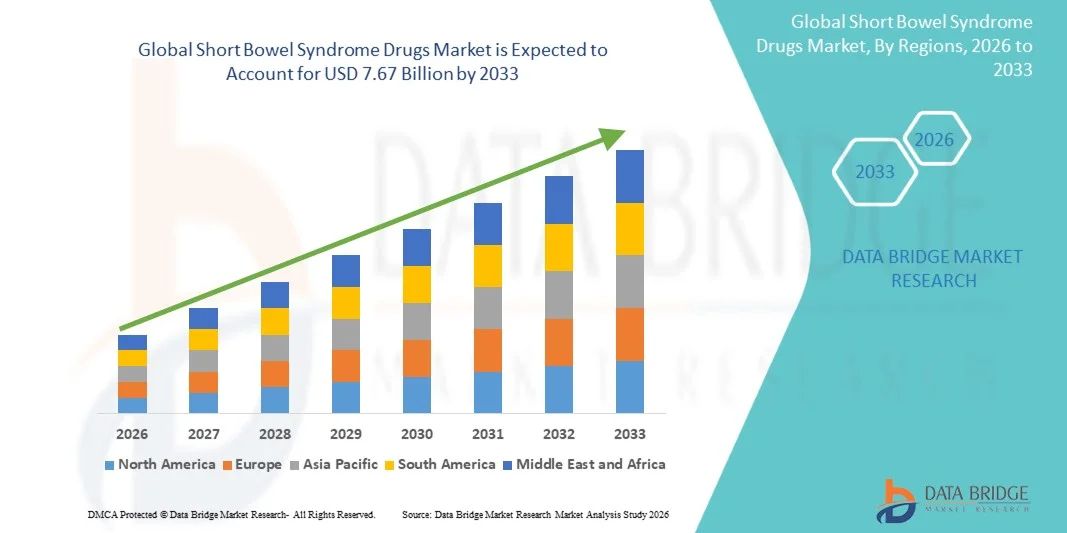

The Short Bowel Syndrome Drugs Market was valued at USD 2.51 billion in 2025 and is projected to reach USD 7.67 billion by 2033, growing at a CAGR of 15.00% from 2026 to 2033. The market is experiencing steady growth driven by the rising prevalence of short bowel syndrome (SBS), increasing awareness of rare gastrointestinal disorders, and ongoing advancements in targeted pharmacological therapies aimed at improving intestinal absorption and reducing dependence on parenteral nutrition.

The growing number of patients undergoing extensive bowel resection due to conditions such as Crohn’s disease, mesenteric ischemia, trauma, and congenital intestinal disorders, combined with improved diagnostic capabilities, is contributing to higher demand for SBS treatments. In addition, favorable regulatory support for orphan drugs, expanding research into glucagon-like peptide-2 (GLP-2) analogs, and increasing healthcare investments are encouraging the adoption of innovative therapies. Novel biologics and long-acting treatment options are increasingly being utilized to enhance nutrient absorption, improve patient quality of life, and reduce long-term healthcare costs associated with chronic nutritional support.

Key Market Trends & Insights

- North America dominated the Short Bowel Syndrome Drugs Market with the largest revenue share of 42.18% in 2025, supported by high diagnosis rates, favorable reimbursement policies, and the presence of leading manufacturers of orphan gastrointestinal therapies.

- The Glucagon-like Peptide segment led the market with a 38.64% share in 2025, driven by its superior ability to enhance intestinal adaptation, improve nutrient absorption, and reduce dependence on parenteral nutrition.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by improving healthcare infrastructure, increasing awareness of rare diseases, and expanding access to specialty biologic treatments.

- Growth Hormone segment are the fastest-growing drug class type, projected to register a CAGR of 8.4%, reflecting the surge in interest in combination therapies aimed at enhancing intestinal absorption and bowel adaptation.

- The Parenteral segment dominated the route of administration category with a 61.27% revenue share in 2025, led by the widespread use of injectable biologics and peptide-based therapies for SBS treatment.

- Adult Patients accounted for 71.26% of the market, preferred by the higher prevalence of SBS resulting from Crohn’s disease, mesenteric ischemia, cancer surgeries, and trauma-related bowel resections.

- The Pediatric Patients segment is the fastest-growing patient type category, with a CAGR of 8.2%, driven by the growing recognition of congenital gastrointestinal disorders and improved neonatal care outcomes.

Market Size & Forecast

- Global Market Value (2025): USD 2.51 Billion

- Expected Market Value (2033): USD 7.67 Billion

- Forecast CAGR (2026–2033): 15.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Short Bowel Syndrome Drugs Market Segmentation

|

Attributes |

Short Bowel Syndrome Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Takeda Pharmaceutical Company (Japan) · Ironwood Pharmaceuticals, Inc. (U.S.) · Pfizer Inc. (U.S.) · AbbVie Inc. (U.S.) · Novo Nordisk A/S (Denmark) · Sanofi (France) · Merck & Co., Inc. (U.S.) · Bristol Myers Squibb (U.S.) · Amgen Inc. (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · AstraZeneca (U.K.) · GSK plc (U.K.) · Eli Lilly and Company (U.S.) · Novartis AG (Switzerland) · Roche Holding AG (Switzerland) · Abbott (U.S.) · Bausch Health (Canada) · Zealand Pharma A/S (Denmark) · Ferring Pharmaceuticals (Switzerland) · Horizon Therapeutics (U.S.) · Recordati Rare Diseases (Italy) |

|

Market Opportunities |

· Expanding development of next-generation GLP-2 analogs and long-acting biologics · Increasing diagnosis and treatment access in emerging markets · Growing investment in intestinal rehabilitation therapies and personalized treatment approaches |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Short Bowel Syndrome Drugs Market Trends

Trend: Increasing Adoption of Long-Acting GLP-2 Therapies

Healthcare providers are increasingly adopting long-acting GLP-2 therapies to improve nutrient absorption, reduce dependence on parenteral nutrition, and enhance quality of life for patients with short bowel syndrome. These therapies stimulate intestinal growth and adaptation, enabling patients to absorb more fluids and nutrients through the remaining functional bowel. The availability of advanced biologic formulations supports less frequent dosing schedules, improved treatment adherence, and reduced healthcare burden compared with conventional supportive care approaches. Specialty intestinal rehabilitation centers are increasingly incorporating these therapies into multidisciplinary treatment programs, while ongoing clinical research is focused on developing next-generation GLP-2 analogs with improved efficacy, safety, and durability.

For instance, in December 2022, Zealand Pharma announced positive phase 3 results for glepaglutide, a long-acting GLP-2 analog developed to reduce parenteral support requirements in patients with short bowel syndrome.

Short Bowel Syndrome Drugs Market Dynamics

Key Market Driver: Rising Prevalence of Intestinal Failure and Dependence on Parenteral Nutrition

The increasing incidence of intestinal failure resulting from Crohn’s disease, mesenteric ischemia, trauma, cancer-related surgeries, and congenital gastrointestinal disorders has created substantial demand for effective short bowel syndrome therapies. Many SBS patients require long-term parenteral nutrition to maintain adequate hydration and nutritional status, creating significant clinical and economic burdens. As awareness of SBS improves and diagnostic capabilities expand, a growing number of patients are being identified and referred to specialized treatment centers. Pharmaceutical companies and healthcare providers are therefore expanding the use of targeted therapies that promote intestinal adaptation and reduce nutritional support dependence.

For instance, in March 2024, Takeda Pharmaceutical Company continued expanding global access initiatives for teduglutide-based therapies, supporting broader treatment availability for adult and pediatric SBS patients who rely on parenteral nutrition.

Key Restraint/Challenge: High Treatment Costs and Limited Patient Accessibility

A significant restraint in the Short Bowel Syndrome Drugs Market is the high cost associated with advanced biologic therapies and comprehensive patient management programs. Modern SBS treatments require sophisticated manufacturing processes, specialized administration protocols, and continuous clinical monitoring, resulting in substantial expenses for healthcare systems and patients. In addition to drug costs, patients often require nutritional counseling, laboratory assessments, imaging studies, and management of treatment-related complications. Reimbursement policies remain inconsistent across countries, and access to specialty care centers is limited in many developing regions. These factors can delay treatment initiation and restrict the adoption of innovative therapies among eligible patients. Consequently, affordability and healthcare infrastructure limitations continue to present major barriers to wider market penetration despite growing clinical demand.

For instance, reimbursement restrictions and premium pricing associated with GLP-2 analog therapies continue to limit treatment accessibility across several emerging markets, particularly where rare disease funding programs remain underdeveloped.

Key Market Opportunity: Expansion of Next-Generation Intestinal Rehabilitation Therapies

The development of next-generation intestinal rehabilitation therapies presents a significant growth opportunity for the short bowel syndrome drugs market. Advances in peptide engineering, biologic drug design, and orphan disease research are enabling the development of therapies that offer longer duration of action, improved efficacy, and enhanced patient convenience. Emerging treatments are being designed to further reduce dependence on parenteral nutrition while improving intestinal function and overall quality of life. In addition, growing regulatory incentives for orphan drug development are encouraging pharmaceutical companies to invest in innovative SBS treatment pipelines. Expanding clinical research activities, increasing collaboration between biotechnology firms and academic institutions, and rising healthcare spending on rare diseases are creating favorable conditions for market expansion

For instance, in December 2022, Zealand Pharma reported positive phase 3 findings for glepaglutide, highlighting the potential of next-generation long-acting intestinal rehabilitation therapies to improve outcomes and reduce parenteral nutrition dependence in SBS patients.

Short Bowel Syndrome Drugs Market Scope

The short bowel syndrome drugs market is segmented on the basis of drug class, route of administration, patient type, end-users, and distribution channel.

- By Drug Class

On the basis of drug class, the Short Bowel Syndrome Drugs Market is segmented into glucagon-like peptide, anti-diarrheal, histamine blockers, proton pump inhibitors, growth hormone, and others. The Glucagon-like Peptide (GLP) segment dominated the market with a 38.64% share in 2025, owing to its superior ability to enhance intestinal adaptation, improve nutrient absorption, and reduce dependence on parenteral nutrition. GLP-2 analogs have become the standard targeted therapy for SBS patients due to their proven clinical efficacy and long-term benefits. Increasing physician preference for disease-modifying treatments over symptomatic management is supporting segment growth. Regulatory approvals for advanced GLP-based therapies have further strengthened market penetration across developed healthcare systems. Growing awareness among healthcare professionals regarding intestinal rehabilitation is accelerating adoption. The segment continues to benefit from ongoing investments in biologic drug development and orphan disease research.

The Growth Hormone segment is projected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by increasing interest in combination therapies aimed at enhancing intestinal absorption and bowel adaptation. Growth hormone therapies are being evaluated for their ability to improve nutrient uptake and reduce complications associated with chronic malabsorption. Expanding clinical studies are supporting their use in selected SBS patient populations. Growing focus on personalized treatment approaches is creating opportunities for broader adoption. Advances in endocrinology-based therapies and supportive care strategies are also contributing to market expansion. Rising investments in innovative gastrointestinal treatment solutions are expected to further accelerate growth within this segment.

- By Route of Administration

On the basis of route of administration, the Short Bowel Syndrome Drugs Market is segmented into oral, parenteral, and others. The Parenteral segment led the market with a 61.27% share in 2025, driven by the widespread use of injectable biologics and peptide-based therapies for SBS treatment. Many advanced SBS drugs require parenteral administration to ensure optimal bioavailability and therapeutic effectiveness. Healthcare providers prefer this route for patients with severe malabsorption conditions where oral absorption remains compromised. The segment also benefits from strong clinical evidence supporting injectable GLP-2 analog therapies. Increasing adoption of specialty biologics in hospital and outpatient settings is further strengthening demand. Continuous development of long-acting injectable formulations is reinforcing the segment’s dominant position.

The Oral segment is expected to witness the fastest growth at a CAGR of 7.9% from 2026 to 2033, supported by rising demand for convenient treatment options and improved patient compliance. Pharmaceutical companies are increasingly investing in oral formulations designed to enhance absorption and therapeutic effectiveness. Oral therapies reduce the burden associated with frequent injections and long-term administration procedures. Advancements in drug delivery technologies are improving the feasibility of oral SBS treatments. Growing patient preference for self-administered medications is further encouraging adoption. Expanding research activities focused on novel oral gastrointestinal therapies are expected to support long-term segment growth.

- By Patient Type

On the basis of patient type, the Short Bowel Syndrome Drugs Market is segmented into adult patients and pediatric patients. The Adult Patients segment dominated the market with a 71.26% share in 2025, owing to the higher prevalence of SBS resulting from Crohn’s disease, mesenteric ischemia, cancer surgeries, and trauma-related bowel resections. Adults account for the majority of diagnosed SBS cases globally and represent the largest treatment population. Increased awareness and availability of specialized therapies are improving treatment access among adult patients. The segment also benefits from higher healthcare spending and stronger reimbursement support in developed countries. Long-term management requirements create sustained demand for advanced SBS therapies. Continuous improvements in clinical care are further contributing to segment dominance.

The Pediatric Patients segment is anticipated to register the fastest growth at a CAGR of 8.2% from 2026 to 2033, driven by growing recognition of congenital gastrointestinal disorders and improved neonatal care outcomes. Advances in pediatric gastroenterology are enabling earlier diagnosis and intervention for children with SBS. Increasing availability of pediatric-specific treatment protocols is improving clinical outcomes. Healthcare providers are placing greater emphasis on nutritional rehabilitation and long-term growth management in pediatric patients. Expanding research efforts focused on child-friendly formulations are supporting market development. Rising awareness among caregivers and clinicians is expected to further boost adoption across this segment.

- By End-Users

On the basis of end-users, the Short Bowel Syndrome Drugs Market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment accounted for the largest market share of 52.83% in 2025, supported by the complex nature of SBS treatment and the need for multidisciplinary patient management. Hospitals provide access to gastroenterologists, nutrition specialists, and advanced supportive care services required for effective disease management. Most biologic therapies and intestinal rehabilitation programs are initiated within hospital settings. The availability of specialized diagnostic and monitoring infrastructure further supports treatment delivery. Hospitals also manage severe SBS cases requiring parenteral nutrition and intensive follow-up. Strong reimbursement frameworks continue to reinforce their leading position.

The Homecare segment is projected to be the fastest-growing segment at a CAGR of 8.1% from 2026 to 2033, driven by increasing efforts to reduce hospitalization costs and improve patient quality of life. Advances in home-based nutritional support and drug administration technologies are enabling safer treatment outside traditional healthcare facilities. Patients increasingly prefer receiving long-term care in familiar home environments. Improved telehealth services and remote monitoring capabilities are supporting this transition. Healthcare systems are encouraging homecare adoption to optimize resource utilization and reduce clinical burden. Growing availability of patient support programs is further accelerating market growth within this segment.

- By Distribution Channel

On the basis of distribution channel, the Short Bowel Syndrome Drugs Market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The Hospital Pharmacy segment dominated the market with a 56.74% share in 2025, owing to the specialized nature of SBS therapies and the requirement for physician-supervised treatment initiation. Most biologic drugs are dispensed through hospital pharmacies due to storage, handling, and monitoring requirements. These facilities ensure appropriate patient education and medication management. Strong integration with hospital treatment pathways further supports segment leadership. Hospital pharmacies also facilitate access to specialty medications through reimbursement and rare disease programs. Their critical role in managing complex therapies continues to sustain market dominance.

The Online Pharmacy segment is expected to witness the fastest growth at a CAGR of 8.3% from 2026 to 2033, driven by increasing digitalization of healthcare services and expanding access to specialty medications. Online platforms offer greater convenience, improved medication availability, and streamlined prescription management for chronic disease patients. Rising adoption of telemedicine is creating favorable conditions for online pharmaceutical distribution. Enhanced home delivery services are improving treatment continuity for SBS patients requiring long-term therapy. Growing internet penetration and digital healthcare infrastructure are further supporting expansion. The segment is also benefiting from increasing patient preference for convenient and contactless healthcare solutions.

Short Bowel Syndrome Drugs Market Regional Analysis

North America dominated the Short Bowel Syndrome Drugs Market with the largest revenue share of 42.18% in 2025, supported by high diagnosis rates, favorable reimbursement policies, and the presence of leading manufacturers of orphan gastrointestinal therapies. The region also benefits from high diagnosis rates, strong awareness of short bowel syndrome, and widespread availability of innovative biologic treatments across specialized care centers and hospitals. Increasing adoption of GLP-2 analog therapies, growing investment in orphan drug development, and expanding intestinal rehabilitation programs continue to drive market growth. Ongoing clinical research activities and regulatory support for novel SBS therapies further strengthen North America’s leadership position in the global market.

U.S. Short Bowel Syndrome Drugs Market Insight

The U.S. short bowel syndrome drugs market is witnessing strong growth due to rising diagnosis rates of intestinal failure, increasing adoption of advanced biologic therapies, and favorable reimbursement support for rare disease treatments. The country’s well-established healthcare infrastructure, along with strong presence of leading pharmaceutical companies and specialized intestinal rehabilitation centers, is driving demand across adult and pediatric patient populations. In addition, growing investment in orphan drug development and increasing awareness regarding long-term SBS management are accelerating the adoption of innovative therapies throughout the United States.

Europe Short Bowel Syndrome Drugs Market Insight

The Europe short bowel syndrome drugs market remains a major contributor to global revenue, driven by strong healthcare systems, supportive regulatory frameworks, and increasing availability of advanced treatment options. The widespread use of biologic therapies and multidisciplinary intestinal rehabilitation programs is supporting market expansion across the region. Increasing investments in rare disease research, coupled with favorable reimbursement policies and growing awareness among healthcare professionals, continue to enhance the adoption of short bowel syndrome drugs throughout Europe.

U.K. Short Bowel Syndrome Drugs Market Insight

The U.K. short bowel syndrome drugs market is experiencing steady growth, supported by rising awareness of rare gastrointestinal disorders, increasing adoption of targeted biologic therapies, and strong access to specialized healthcare services. Growing investments in rare disease management programs and expanding clinical research activities are contributing to market growth. Furthermore, improvements in patient identification, treatment accessibility, and long-term nutritional support strategies are strengthening the country’s position as an important market for SBS therapies.

Germany Short Bowel Syndrome Drugs Market Insight

The Germany short bowel syndrome drugs market is expanding steadily due to the country’s advanced healthcare infrastructure, strong pharmaceutical industry presence, and increasing adoption of innovative treatment approaches. Hospitals and specialty care centers are increasingly utilizing biologic therapies and intestinal rehabilitation programs to improve patient outcomes and reduce dependence on parenteral nutrition. Continuous advancements in rare disease management, along with strong government support for healthcare innovation and research, are further driving market growth in Germany.

Asia-Pacific Short Bowel Syndrome Drugs Market Insight

The Asia-Pacific short bowel syndrome drugs market is expected to witness rapid growth, driven by improving healthcare infrastructure, increasing awareness of rare gastrointestinal disorders, and rising investments in specialty treatment services across countries such as China, India, and Japan. Growing recognition of SBS-related complications, expanding access to advanced biologic therapies, and increasing demand for effective long-term disease management solutions are supporting regional market expansion. In addition, rising healthcare expenditure and improving diagnostic capabilities are accelerating treatment adoption across the region.

Japan Short Bowel Syndrome Drugs Market Insight

The Japan short bowel syndrome drugs market is witnessing consistent growth due to rising investments in rare disease treatment, increasing adoption of advanced biologic therapies, and growing focus on improving patient quality of life. Healthcare providers and research institutions are increasingly utilizing innovative SBS therapies to reduce dependence on parenteral nutrition and enhance intestinal function. Moreover, expanding clinical research activities and the country’s emphasis on advanced healthcare solutions are further contributing to market growth.

China Short Bowel Syndrome Drugs Market Insight

The China short bowel syndrome drugs market is growing rapidly, driven by improving healthcare access, expanding rare disease awareness programs, and increasing government focus on advanced treatment availability. Growing adoption of biologic therapies across hospitals and specialty care centers is significantly boosting market demand. In addition, rising investments in pharmaceutical innovation, increasing diagnosis rates of gastrointestinal disorders, and continuous healthcare modernization efforts are positioning China as one of the fastest-growing markets for short bowel syndrome drugs globally.

Short Bowel Syndrome Drugs Market Share

The short bowel syndrome drugs industry is primarily led by well-established companies, including:

- Takeda Pharmaceutical Company (Japan)

- Ironwood Pharmaceuticals, Inc. (U.S.)

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Novo Nordisk A/S (Denmark)

- Sanofi (France)

- Merck & Co., Inc. (U.S.)

- Bristol Myers Squibb (U.S.)

- Amgen Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- AstraZeneca (U.K.)

- GSK plc (U.K.)

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Roche Holding AG (Switzerland)

- Abbott (U.S.)

- Bausch Health (Canada)

- Zealand Pharma A/S (Denmark)

- Ferring Pharmaceuticals (Switzerland)

- Horizon Therapeutics (U.S.)

- Recordati Rare Diseases (Italy)

Latest Developments in Short Bowel Syndrome Drugs Market

- In February 2025, Ironwood Pharmaceuticals announced progress toward a confirmatory Phase III (STARS-2) clinical trial for apraglutide after discussions with the U.S. FDA. The company aligned on key trial design elements to further evaluate apraglutide, a once-weekly GLP-2 analog being developed for adults with short bowel syndrome dependent on parenteral support. The development highlights continued industry investment in next-generation SBS therapies and reinforces the importance of long-acting treatment options for reducing nutritional support dependence

- In December 2024, Zealand Pharma announced that the U.S. FDA issued a Complete Response Letter for glepaglutide, requesting an additional clinical trial to further confirm safety and efficacy in adults with short bowel syndrome. Despite the setback, the company stated plans to initiate another late-stage study and continue regulatory discussions. This development underscores the rigorous regulatory standards governing SBS drug approvals and the ongoing commitment to advancing innovative treatments

- In February 2024, Ironwood Pharmaceuticals announced positive topline results from its global Phase III STARS trial evaluating apraglutide in adults with short bowel syndrome with intestinal failure (SBS-IF). The once-weekly GLP-2 analog met its primary endpoint by significantly reducing weekly parenteral support volume compared with placebo. The results strengthened apraglutide’s position as a potential new treatment option and represented a major advancement in SBS drug development

- In February 2024, Takeda Pharmaceutical Company announced that teduglutide received approval from China's National Medical Products Administration (NMPA) for the treatment of adult and pediatric patients aged one year and older with short bowel syndrome. The approval introduced the first GLP-2 analog therapy for SBS patients in China and expanded access to long-term intestinal rehabilitation treatment in one of the world's largest healthcare markets

- In September 2022, Zealand Pharma announced positive Phase III EASE-1 trial results for glepaglutide in patients with short bowel syndrome. The study demonstrated that twice-weekly treatment significantly reduced parenteral support requirements, with several patients successfully weaned off parenteral nutrition. The achievement marked one of the most significant late-stage clinical milestones in the SBS market and further validated the therapeutic potential of long-acting GLP-2 analogs

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.