Global Silicon Anode Battery Market

Market Size in USD Billion

USD

97.97 Billion

USD

490.34 Billion

2024

2032

USD

97.97 Billion

USD

490.34 Billion

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 97.97 Billion |

Market Size (Forecast Year) |

USD 490.34 Billion |

CAGR |

% |

Major Markets Players |

|

Silicon Anode Battery Market Size

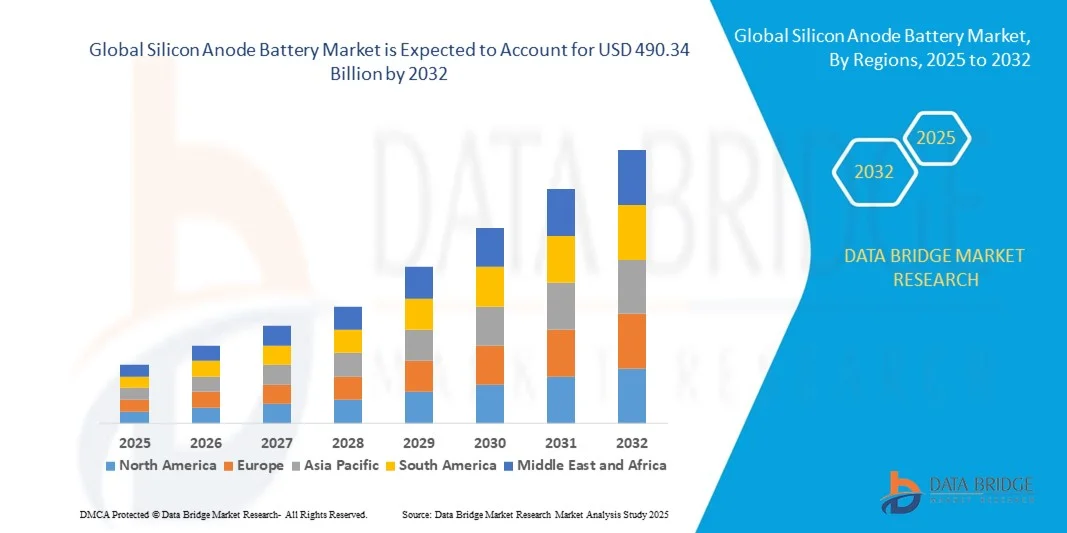

- The global silicon anode battery market size was valued at USD 97.97 billion in 2024 and is expected to reach USD 490.34 billion by 2032, at a CAGR of 22.3% during the forecast period

- The market growth is largely fueled by the rising adoption of electric vehicles, increasing demand for high-capacity consumer electronics, and ongoing advancements in battery technology, which are driving the development and commercialization of silicon anode batteries

- Furthermore, the need for longer-lasting, faster-charging, and higher-energy-density batteries across automotive, industrial, and portable electronics applications is accelerating investment and innovation in silicon anode materials, significantly boosting the industry's growth

Silicon Anode Battery Market Analysis

- Silicon anode batteries utilize silicon-based materials in the anode to replace or supplement traditional graphite, offering higher energy density, longer cycle life, and improved charge/discharge performance. These batteries are increasingly integrated into electric vehicles, portable electronics, and energy storage systems to meet growing performance demands

- The escalating demand for silicon anode batteries is primarily driven by the global shift toward electrification, the rising need for efficient and high-capacity energy storage solutions, and continuous technological innovations in advanced battery materials, which are enhancing performance, reducing charging times, and supporting sustainable energy adoption

- Asia-Pacific dominated the silicon anode battery market with a share of 54.84% in 2024, due to rapid adoption of electric vehicles, growing consumer electronics demand, and strong presence of battery manufacturing hubs

- North America is expected to be the fastest growing region in the silicon anode battery market during the forecast period due to high EV adoption, government incentives, and growing investments in advanced battery technologies

- Less than 1500 mAh segment dominated the market with a market share of 42.74% in 2024, due to rising demand in compact consumer electronics and wearable devices. These batteries offer lightweight, small-form-factor solutions without compromising on performance, catering to the miniaturization trend in electronics. Growing adoption in IoT devices and portable medical instruments also supports their rapid market expansion. Furthermore, improvements in energy efficiency and cost-effective production methods are encouraging manufacturers to integrate smaller silicon anode batteries in emerging product categories

Report Scope and Silicon Anode Battery Market Segmentation

|

Attributes |

Silicon Anode Battery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Silicon Anode Battery Market Trends

Increasing Demand for High-Energy Density Batteries

- The demand for high-energy density batteries is significantly accelerating the growth of the silicon anode battery market, driven by the limitations of conventional lithium-ion technology and the rising need for longer battery life. Silicon anodes offer a much higher lithium storage capacity compared to traditional graphite, creating opportunities for improved energy efficiency and performance

- For instance, companies such as Sila Nanotechnologies have been pioneering the commercialization of silicon-dominant anode materials integrated into consumer electronics and wearables. Their partnership with automakers such as Mercedes-Benz demonstrates how industry leaders are moving toward silicon-based chemistries to enhance vehicle range and charging performance

- A major trend in this market is the increasing adoption of silicon anode batteries in electric vehicles to address range anxiety and enable faster charging. The substitution of graphite with silicon in anodes enhances the energy density, which contributes to extending driving ranges and reducing dependence on frequent charging

- In consumer electronics, silicon anode batteries are showing potential to power devices such as smartphones, laptops, and wearables with longer cycles and reduced charging times. This is increasingly appealing to global technology manufacturers aiming to improve customer satisfaction and meet the rising demand for advanced portable power solutions

- The integration of nanotechnology and composite materials is enabling the development of silicon anodes with improved durability and cyclability, addressing the challenge of volume expansion in pure silicon. Companies are actively exploring silicon-carbon composites and other advanced materials to ensure commercial scalability

- The growing emphasis on higher energy density and longer lifespan is transforming battery innovation, making silicon anode batteries a strategic enabler for EV adoption, consumer electronics growth, and renewable energy storage. This trajectory is expected to reshape the battery materials industry by setting new performance benchmarks across applications

Silicon Anode Battery Market Dynamics

Driver

Government Initiatives and Regulations Promoting Clean Energy

- Global government initiatives aimed at reducing carbon emissions and enabling electrification are driving demand for advanced battery technologies such as silicon anode batteries. Policies promoting electric vehicles, renewable integration, and energy-efficient storage systems make the adoption of high-performance batteries a crucial priority

- For instance, the U.S. Department of Energy has supported research and funding for next-generation battery materials, including silicon anodes, with programs that encourage commercialization and pilot-scale production. Similarly, governments across Europe have introduced strict emission reduction targets, pushing automakers to invest in batteries offering higher energy density to comply with regulatory norms

- The increasing deployment of renewable energy projects globally has created demand for efficient energy storage systems that silicon anode batteries can support with higher energy retention and longer cycle life. This advancement complements national strategies for decarbonization and grid modernization

- In addition, regulatory mandates requiring automakers to accelerate EV adoption are pushing companies to explore higher-capacity batteries that can enable affordable mass-market electrification. Silicon anodes are seen as a breakthrough facilitating compliance with stringent emission rules and sustainability objectives

- Government funding, research incentives, and clean energy regulations are creating favorable conditions for rapid development and adoption of silicon anode batteries. This policy-driven momentum is expected to reinforce the technology’s role in

Restraint/Challenge

Workforce Skill Enhancement and Retraining

- A major challenge in the silicon anode battery market is the technical limitation related to the volume expansion of silicon during charge-discharge cycles, which can cause structural instability, rapid capacity fading, and reduced lifespan of the battery. This scientific drawback slows down widespread commercialization

- For instance, many research projects supported by companies such as Amprius Technologies are focused on developing silicon nanowires and advanced composites to mitigate volume expansion. Despite progress, scalability remains difficult, making it challenging to integrate such solutions at an industrial production level

- The high manufacturing cost of silicon anode materials also acts as a barrier, particularly in comparison to established graphite-based solutions, which are cheaper and more commercially mature. Producers face difficulties in achieving cost parity while ensuring durability and safety in large-scale deployments

- Limited infrastructure for mass production and the lack of standardized manufacturing processes create bottlenecks that slow adoption across industries. Without significant advancements in material development and processing methods, companies may struggle to bring down costs to levels suitable for mass-market applications

- To overcome these challenges, manufacturers are investing in research, strategic collaborations, and pilot-scale facilities aimed at optimizing silicon composites and reducing production costs. Addressing these technical and economic barriers will be essential for silicon anode batteries to transition from niche applications into mainstream commercial adoption

Silicon Anode Battery Market Scope

The market is segmented on the basis of capacity and application.

- By Capacity

On the basis of capacity, the silicon anode battery market is segmented into less than 1500 mAh, 1500 mAh to 2500 mAh, and above 2500 mAh. The less than 1500 mAh segment dominated the largest market revenue share of 42.74% in 2024, driven by rising demand in compact consumer electronics and wearable devices. These batteries offer lightweight, small-form-factor solutions without compromising on performance, catering to the miniaturization trend in electronics. Growing adoption in IoT devices and portable medical instruments also supports their rapid market expansion. Furthermore, improvements in energy efficiency and cost-effective production methods are encouraging manufacturers to integrate smaller silicon anode batteries in emerging product categories.

The above 2500 mAh segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by its superior energy density and longer lifecycle compared to lower-capacity variants. High-capacity silicon anode batteries are increasingly preferred in applications requiring extended battery life, such as electric vehicles and high-performance consumer electronics. Their ability to deliver consistent power output and support fast charging cycles further strengthens their adoption. In addition, advancements in silicon anode formulations have improved cycle stability, making these batteries a reliable choice for both industrial and automotive applications.

- By Application

On the basis of application, the silicon anode battery market is segmented into consumer electronics, automobile, medical devices, industrial, and energy harvesting. The automobile segment dominated the largest market revenue share in 2024, driven by the increasing electrification of vehicles and the push for high-energy-density batteries to extend driving range. Silicon anode batteries provide significant improvements in charge capacity and lifecycle performance, making them ideal for electric vehicles and hybrid models. Automakers are actively investing in these batteries to reduce reliance on traditional lithium-ion chemistries, while meeting stringent environmental regulations and consumer expectations for performance. Integration with battery management systems also enhances safety and efficiency in automotive applications.

The consumer electronics segment is projected to witness the fastest CAGR from 2025 to 2032, fueled by the growing use of smartphones, laptops, and wearable devices requiring compact, high-capacity batteries. Silicon anode batteries enable faster charging, longer battery life, and lighter weight designs, meeting the demands of modern portable devices. Rising consumer preference for seamless, uninterrupted usage of electronic gadgets further drives market growth. Moreover, continuous innovations in electrode materials and scalable manufacturing techniques support the rapid adoption of silicon anode batteries across consumer electronics.

Silicon Anode Battery Market Regional Analysis

- Asia-Pacific dominated the silicon anode battery market with the largest revenue share of 54.84% in 2024, driven by rapid adoption of electric vehicles, growing consumer electronics demand, and strong presence of battery manufacturing hubs

- The region’s cost-effective manufacturing ecosystem, increasing investments in advanced battery technologies, and supportive government policies for EVs and renewable energy storage are accelerating market growth

- Availability of skilled labor, rapid industrialization, and expanding research and development capabilities across developing economies are contributing to higher consumption of silicon anode batteries in automotive, consumer, and industrial applications

China Silicon Anode Battery Market Insight

China held the largest share in the Asia-Pacific silicon anode battery market in 2024, owing to its dominance in electric vehicle production and battery manufacturing. Strong government incentives for EV adoption, extensive supply chain infrastructure, and large-scale production of advanced anode materials are major growth drivers. Continuous investments in R&D for high-capacity batteries and collaborations with global battery manufacturers further strengthen market demand.

India Silicon Anode Battery Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by rising EV adoption, increasing consumer electronics production, and growing focus on renewable energy storage solutions. Government initiatives promoting Make in India and local battery manufacturing are supporting market expansion. In addition, investments in advanced materials and growing industrial applications are driving demand for silicon anode batteries.

Europe Silicon Anode Battery Market Insight

The Europe silicon anode battery market is expanding steadily, supported by stringent environmental regulations, high EV penetration, and investments in advanced battery technologies. The region emphasizes sustainability, energy efficiency, and long-cycle batteries for automotive and industrial applications. Rising R&D activities in materials innovation and collaborations between manufacturers and academic institutions are enhancing market growth.

Germany Silicon Anode Battery Market Insight

Germany’s market is driven by its leadership in EV production, advanced automotive battery research, and strong industrial adoption of high-capacity batteries. The country benefits from robust R&D infrastructure and collaborations between universities and battery manufacturers. Demand is particularly strong for automotive, industrial, and energy storage applications, supported by government incentives for green mobility.

U.K. Silicon Anode Battery Market Insight

The U.K. market is supported by increasing EV adoption, renewable energy initiatives, and government policies encouraging local battery production. Rising focus on research in high-capacity and fast-charging silicon anode batteries, along with academic-industry collaborations, is driving market growth. Demand from consumer electronics and industrial sectors further strengthens the market.

North America Silicon Anode Battery Market Insight

North America is projected to grow at the fastest CAGR from 2025 to 2032, driven by high EV adoption, government incentives, and growing investments in advanced battery technologies. Strong focus on energy storage solutions, technological innovation in high-capacity anodes, and reshoring of battery production are boosting market growth.

U.S. Silicon Anode Battery Market Insight

The U.S. accounted for the largest share in the North American market in 2024, underpinned by its advanced EV industry, substantial R&D infrastructure, and increasing production of silicon anode materials. Government incentives for clean energy, strong collaborations between industry and academia, and the presence of key battery manufacturers are strengthening demand across automotive, industrial, and consumer electronics sectors.

Silicon Anode Battery Market Share

The silicon anode battery industry is primarily led by well-established companies, including:

- Panasonic Corporation (Japan)

- SAMSUNG SDI CO., LTD. (South Korea)

- LG Chem. (South Korea)

- NEXEON LTD. (U.K.)

- Los Angeles Cleantech Incubator (U.S.)

- Enevate Corporation (U.S.)

- Zeptor Corporation (U.S.)

- CONNEXX SYSTEMS Corp. (Japan)

- XGSciences (U.S.)

- California Lithium Battery (U.S.)

- City of Irvine (U.S.)

- Amprius Technologies (U.S.)

- Solid Energy A/S (Denmark)

- ActaCell, Inc. (U.S.)

- OneD Material, Inc. (U.S.)

- Hitachi Chemical Co., Ltd. (Japan)

- Huawei Technologies Co., Ltd. (China)

Latest Developments in Global Silicon Anode Battery Market

- In May 2025, Sila Nanotechnologies commenced the commissioning of its Moses Lake, Washington facility to produce Titan Silicon, a next-generation silicon anode material developed in partnership with Panasonic. This material is designed to enhance electric vehicle battery energy density by up to 25% and significantly reduce charging times. The facility’s production will support mass-market EV deployment, addressing the growing industry demand for high-performance, longer-lasting batteries. This initiative highlights the increasing collaboration between leading battery manufacturers to accelerate commercialization of silicon anode technology and its adoption in both automotive and energy storage applications

- In 2025, Sicona Battery Technologies began developing its first U.S. commercial facility in the southeastern region. The plant will initially produce 6,700 tonnes per annum of silicon-carbon anode material, with plans to scale up to 26,500 tonnes, sufficient to meet battery requirements for over 3.25 million electric vehicles annually. This facility will strengthen domestic supply of high-performance anode materials, reduce dependency on imports, and support the expanding EV ecosystem in the U.S. It also positions Sicona as a key player in the commercialization and mass adoption of silicon anode battery technology across automotive and industrial sectors

- In December 2023, Amprius Technologies inaugurated a state-of-the-art silicon nanowire battery manufacturing line at its Fremont, California facility. This expansion increases production capacity tenfold, enabling the company to meet rising global demand for high-energy-density batteries. The advanced production line will produce batteries with significantly higher energy density than conventional lithium-ion cells, serving high-performance applications such as aerospace, defense, and premium electric vehicles. By scaling production, Amprius is set to drive cost efficiencies, expand market presence, and accelerate adoption of next-generation silicon-based battery solutions

- In June 2023, LG Chem introduced a high-performance silicon anode battery utilizing a silicon-based anode material that substantially increases energy density and overall capacity compared to conventional lithium-ion batteries. This breakthrough addresses the growing need for longer-lasting, faster-charging, and high-power batteries in electric vehicles and portable electronics. By improving battery performance, LG Chem is enabling manufacturers to meet rising consumer and industry expectations, driving market demand and technological adoption in automotive and consumer electronics sectors

- In March 2023, Panasonic Corporation announced the successful development of a high-capacity silicon anode battery offering significantly higher energy storage than traditional graphite anode batteries. This advancement allows for longer battery life, improved efficiency, and enhanced overall performance across multiple applications. By pushing forward silicon anode technology, Panasonic is bridging the gap between conventional lithium-ion limitations and the rising demand for high-capacity, fast-charging energy storage solutions, reinforcing its leadership in next-generation battery innovation

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Silicon Anode Battery Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Silicon Anode Battery Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Silicon Anode Battery Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.