Global Silicon Based Paper Market

Market Size in USD Billion

USD

3.82 Billion

USD

5.26 Billion

2025

2033

USD

3.82 Billion

USD

5.26 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.82 Billion | |

| USD 5.26 Billion | |

| % | |

|

Silicon Based Paper Market Size

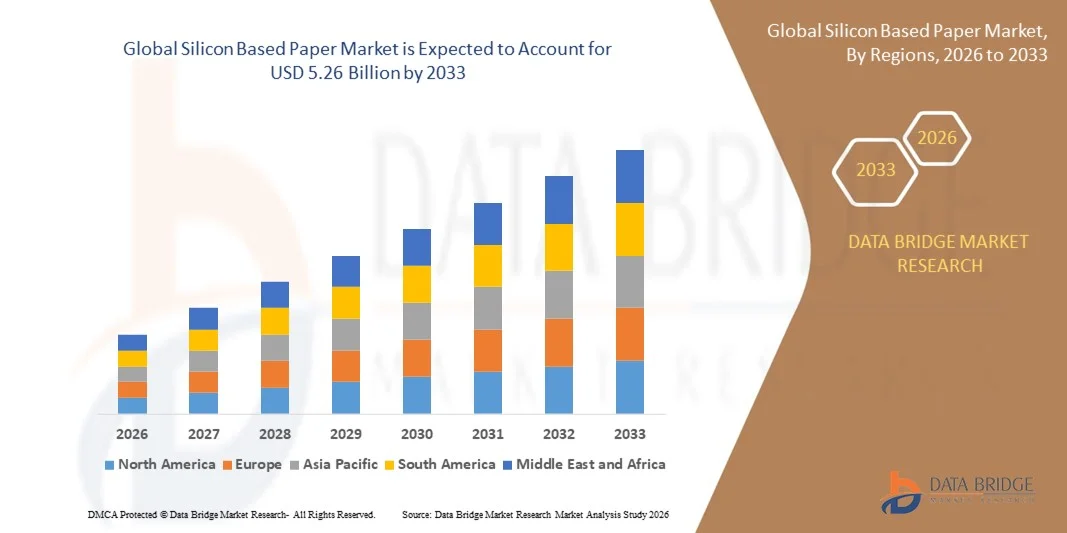

- The global silicon based paper market size was valued at USD 3.82 billion in 2024 and is expected to reach USD 5.26 billion by 2032, at a CAGR of 4.10% during the forecast period

- The market growth is largely driven by increasing demand for sustainable, high-performance packaging and labeling solutions across food, hygiene, cosmetic, and pharmaceutical industries, which is fueling the adoption of silicon-based papers with superior release and non-stick properties

- Furthermore, growing emphasis on eco-friendly and recyclable materials, coupled with technological advancements in silicone coating and paper substrate production, is encouraging manufacturers to integrate silicon-based papers into diverse industrial and commercial applications. These converging factors are accelerating the uptake of silicone-coated papers, thereby significantly boosting the market's growth

Silicon Based Paper Market Analysis

- Silicon-based papers, providing superior release, heat resistance, and durability, are becoming essential in packaging, labeling, and specialty industrial applications. Their ability to improve process efficiency, ensure product safety, and enhance printing and lamination performance is increasing their adoption across multiple end-user industries

- The escalating demand for silicon-based papers is primarily fueled by the rapid growth of the packaged food and personal care sectors, increasing hygiene awareness, and the rising preference for high-quality, non-stick, and reliable paper substrates

- Asia-Pacific dominated the silicon based paper market in 2024, due to expanding packaging, food processing, and hygiene industries across emerging economies

- North America is expected to be the fastest growing region in the silicon based paper market during the forecast period due to increasing use of silicon-coated paper in food packaging, labeling, and hygiene applications

- 61 to 80 GSM segment dominated the market with a market share of 39.1% in 2024, due to its optimal balance between strength, flexibility, and cost-effectiveness. This weight range is widely used in labeling, packaging, and release liner applications due to its superior coating compatibility and durability. Manufacturers prefer this segment for industrial-scale production as it provides consistent silicone coating performance, enhances adhesive properties, and minimizes paper wastage during processing. Its versatility across food packaging, hygiene, and medical-grade applications further solidifies its leading position in the market

Report Scope and Silicon Based Paper Market Segmentation

|

Attributes |

Silicon Based Paper Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Silicon Based Paper Market Trends

Growing Use of Sustainable Silicon-Based Papers

- The silicon based paper market is expanding steadily, driven by increasing demand for sustainable paper solutions that replace traditional plastic liners and packaging materials. The industry is moving toward eco-friendly silicon-based papers with biodegradable and recyclable properties that address stringent environmental regulations and consumer preferences for greener packaging

- For instance, companies such as Ahlstrom-Munksjö and Arjowiggins are pioneering silicon base paper products that combine sustainable raw materials with advanced silicon coating technologies. These products cater primarily to packaging, electronics, and label industries requiring high-performance release liners that are also certified for environmental compliance

- The unique release, heat resistance, and moisture barrier characteristics of silicon based paper make it ideal for flexible packaging, food contact papers, and medical packaging. Ongoing technological advancements are focusing on reducing the carbon footprint associated with production while maintaining durability and usability

- In addition, growing e-commerce and retail sectors are driving demand for silicon based papers used in adhesive labels, tapes, and protective films due to their reliable performance and ease of recycling compared to plastic alternatives. The increasing use of silicon paper in electronics manufacturing also contributes significantly to market growth

- Investments in R&D to improve coating efficiency, transparency, and product customization are supporting market diversification. These innovations enable silicon based paper to serve emerging end-use applications while aligning with circular economy principles

- The trend toward sustainable silicon based papers is expected to continue strengthening as global packaging shifts to eco-friendly solutions balancing functionality with environmental stewardship. This will define long-term growth paths and competitive differentiation in the silicon base paper market

Silicon Based Paper Market Dynamics

Driver

High Demand for Release Liners in Food, Hygiene, and Cosmetics

- Demand for high-quality release liners in the food, hygiene, and cosmetics industries is a critical growth driver for the silicon based paper market. Silicon based papers provide essential release properties that ensure product integrity, hygienic packaging, and ease of use in these sectors

- For instance, major packaging converters such as Nippon Paper Industries and Yupo Corporation supply silicon base papers used in peelable seals for food products, adhesive backings for hygiene items, and cosmetic packaging components. These applications require silicone coatings that offer consistent release behavior and regulatory compliance for direct consumer contact

- The rising global consumption of packaged foods, personal care items, and hygiene products continues to fuel market expansion. Silicon based papers enable manufacturers to meet stringent safety and performance standards while supporting faster production speeds and cost efficiencies

- In addition, growing preference for eco-friendly liners in consumer products encourages the substitution of plastic-backed release liners with silicon coated paper options. This shift is supported by regulations targeting single-use plastics and increasing consumer demand for sustainable packaging

- Technological improvements in silicon coating techniques provide enhanced coating uniformity, printability, and adhesion properties, broadening application possibilities. These features reinforce silicon paper’s position as a preferred release liner material in diverse sectors with evolving packaging needs

- The sustained demand from food, hygiene, and cosmetics end-users is expected to remain a robust market engine, fostering steady innovation and investment in silicon based paper technologies

Restraint/Challenge

High Production Costs and Reliance on Specialized Coatings

- The silicon based paper market is constrained by relatively high production costs stemming from specialized raw materials and complex coating processes required to achieve precise release and barrier properties. These costs limit competitive pricing compared to conventional synthetic alternatives

- For instance, manufacturers such as Ahlstrom-Munksjö and Arjowiggins highlight that the cost-intensive nature of silicone coating operations, including expensive precursors and strict quality control measures, contribute significantly to product pricing. These factors pose adoption barriers in cost-sensitive applications or emerging markets

- The dependency on specialized coating formulations and processes also creates supply chain vulnerabilities, as fluctuations in raw material prices or availability impact production costs and lead times. Maintaining consistent quality in high-volume manufacturing is challenging and often requires ongoing investment in equipment modernization

- In addition, efforts to develop fully biodegradable or compostable silicon papers face technical hurdles due to the inherent stability requirements of silicone coatings. Balancing functionality with environmental goals remains a key innovation challenge facing producers

- Addressing these challenges requires R&D focused on cost reduction, process optimization, and alternative coating chemistries. Enhancing economies of scale and securing sustainable raw material sources will be vital to improving affordability and supporting broader silicon based paper market growth

Silicon Based Paper Market Scope

The market is segmented on the basis of weight and end-user type.

- By Weight

On the basis of weight, the silicon-based paper market is segmented into 40 to 60 GSM, 61 to 80 GSM, 81 to 100 GSM, and more than 100 GSM. The 61 to 80 GSM segment dominated the market with the largest revenue share of 39.1% in 2024, attributed to its optimal balance between strength, flexibility, and cost-effectiveness. This weight range is widely used in labeling, packaging, and release liner applications due to its superior coating compatibility and durability. Manufacturers prefer this segment for industrial-scale production as it provides consistent silicone coating performance, enhances adhesive properties, and minimizes paper wastage during processing. Its versatility across food packaging, hygiene, and medical-grade applications further solidifies its leading position in the market.

The 81 to 100 GSM segment is projected to witness the fastest growth rate from 2025 to 2032, driven by its increasing adoption in high-performance applications requiring enhanced thickness and stability. This segment is favored in the cosmetic and pharmaceutical industries, where strong release liners and superior moisture resistance are critical. The growing trend toward premium and sustainable packaging solutions also boosts demand, as higher GSM silicon papers support efficient printing, lamination, and high-quality finishing. Moreover, technological advancements in coating and curing methods are expanding the use of heavy-weight silicon papers in industrial and specialty label applications.

- By End User Type

On the basis of end user type, the silicon-based paper market is segmented into food industry, hygiene industry, cosmetic industry, pharmaceutical industry, and others. The food industry segment dominated the market in 2024, accounting for the largest revenue share due to the extensive use of silicon-coated paper in baking, packaging, and labeling applications. Its heat resistance, non-stick surface, and grease barrier properties make it indispensable in bakery operations and food wrapping processes. Food manufacturers increasingly prefer silicon-based paper for ensuring hygienic packaging, maintaining product freshness, and meeting regulatory standards on food safety and sustainability. The rapid expansion of quick-service restaurants and packaged food production further strengthens this segment’s dominance.

The cosmetic industry segment is anticipated to record the fastest CAGR from 2025 to 2032, fueled by the rising use of silicon-based paper in release liners for cosmetic labels, self-adhesive packaging, and personal care products. The segment benefits from growing consumer preference for premium and aesthetically appealing packaging solutions. In addition, the adoption of silicon-based paper supports enhanced print quality, resistance to moisture, and eco-friendly material alternatives, aligning with sustainability goals in cosmetic manufacturing. Increasing investment in luxury skincare and beauty brands also propels the demand for specialized silicon-coated release papers to ensure high-end label performance and product differentiation.

Silicon Based Paper Market Regional Analysis

- Asia-Pacific dominated the silicon based paper market with the largest revenue share in 2024, driven by expanding packaging, food processing, and hygiene industries across emerging economies

- The region’s robust manufacturing ecosystem, low production costs, and growing demand for release liners in labels and packaging are fueling market expansion

- Rapid industrialization, coupled with government support for sustainable materials and export-oriented paper production, further strengthens its leadership position in the global market

China Silicon-Based Paper Market Insight

China held the largest share in the Asia-Pacific silicon-based paper market in 2024, supported by its strong paper manufacturing base and extensive adoption in the food and packaging sectors. The country’s advanced coating technologies, large-scale production capacity, and cost competitiveness drive consistent demand. Growth is further supported by increasing applications in hygiene and industrial packaging and ongoing investments in eco-friendly paper coating solutions aligned with national sustainability goals.

India Silicon-Based Paper Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, propelled by rapid expansion in food processing, cosmetics, and healthcare packaging sectors. Rising urbanization, increasing disposable income, and growth in organized retail are boosting the need for silicone-coated release liners and non-stick food-grade papers. In addition, government initiatives promoting domestic paper manufacturing and a shift toward sustainable and recyclable packaging materials are accelerating market development.

Europe Silicon-Based Paper Market Insight

The Europe silicon-based paper market is growing steadily, driven by stringent environmental standards, strong packaging industry presence, and rising use in personal care and pharmaceutical applications. European manufacturers emphasize high-quality, recyclable, and low-emission paper coatings, aligning with the EU’s circular economy goals. The region’s focus on innovation in silicone formulations and bio-based release liners is contributing to consistent market expansion.

Germany Silicon-Based Paper Market Insight

Germany’s market is characterized by its advanced printing, labeling, and packaging industries, which demand high-performance silicone-coated papers. The country’s emphasis on technological innovation, automation in paper processing, and adherence to strict environmental norms drive growth. Strong R&D collaborations and continuous development of durable, sustainable release liners for industrial and commercial applications further support market expansion.

U.K. Silicon-Based Paper Market Insight

The U.K. market is supported by a strong presence of packaging converters, expanding cosmetic and healthcare sectors, and growing focus on sustainability in paper usage. Rising demand for premium and recyclable release liners in the labeling and hygiene industries is boosting market growth. In addition, post-Brexit investments in local manufacturing and increased reliance on eco-friendly paper-based materials are enhancing the U.K.’s role in the European silicon-based paper market.

North America Silicon-Based Paper Market Insight

North America is projected to grow at the fastest CAGR from 2025 to 2032, driven by increasing use of silicon-coated paper in food packaging, labeling, and hygiene applications. The region’s focus on sustainable packaging materials, combined with technological advancements in silicone coating processes, is fueling demand. Strong consumer preference for high-quality, eco-conscious packaging and the presence of leading manufacturers in the U.S. are key contributors to regional growth.

U.S. Silicon-Based Paper Market Insight

The U.S. accounted for the largest share in the North America market in 2024, owing to its developed packaging infrastructure, large-scale food processing industry, and innovation-driven paper manufacturing sector. The country’s emphasis on product safety, recyclability, and premium packaging quality supports strong demand. Presence of major market players and growing investment in sustainable silicone formulations position the U.S. as a major hub for silicon-based paper production and application.

Silicon Based Paper Market Share

The silicon based paper industry is primarily led by well-established companies, including:

- Sappi (South Africa)

- Ivex Speciality Paper, LLC (U.S.)

- KRPA Holding CZ, a.s. (Czech Republic)

- Ahlstrom-Munksjö (Finland)

- Felix Schoeller Group (Germany)

- The Griff Network (U.K.)

- Sona Papers Pvt. Ltd. (India)

- Paper N Films International (U.S.)

- Gascogne (France)

- Savvy Packaging Pvt. Ltd. (India)

- Mehadia Enterprises Private Limited (India)

- Rayven, Inc. (U.S.)

- LINTEC Corporation (Japan)

- Jagannath Industries Pvt. Ltd. (India)

- Spoton Coatings Private Limited (India)

- SAFEPACK INDUSTRIES LTD. (India)

- Fortaok Limited (U.K.)

- MLM India Limited (India)

- ITASA (Brazil)

- Loparex (Netherlands)

Latest Developments in Global Silicon Based Paper Market

- In April 2025, Elkem ASA’s Silicones division launched two additions — SILCOLEASE RE POLY 11362 and RE POLY 368 — which are 100% recycled‑silicone, solvent‑free release coatings for label and liner applications. This development strengthens the sustainability segment of the silicon‑based paper market by providing high-performance alternatives to virgin silicones. It enables manufacturers and converters to reduce carbon footprint significantly while maintaining material quality, encouraging widespread adoption of eco-friendly products in packaging, labeling, and industrial applications. The launch is expected to set a benchmark for circular economy practices in the global release liner marke

- In November 2024, Techlan Ltd introduced an enhanced Re‑Liner™ product featuring a 120 gsm PE‑coated kraft substrate that is fully recycled and suitable for silicone release liner applications. This expansion addresses the growing demand for sustainable paper solutions, particularly in regions emphasizing zero-waste and net-zero goals. By providing a reliable recycled substrate option, the launch facilitates greater use of eco-conscious materials among converters and end-users, expanding the market for recycled silicon-based papers in food, hygiene, and industrial packaging sectors

- In November 2024, the Tag & Label Manufacturers Institute (TLMI) and CELAB North America launched the Liner Recycling Initiative (LRI) to implement recycling programs for silicone‑coated paper release liners across multiple U.S. regions. This initiative enhances the infrastructure for collecting, processing, and reusing silicone-coated paper waste, addressing a key challenge in the market’s sustainability efforts. By creating pathways for recycling previously discarded liners, the program encourages manufacturers to adopt circular supply chain models, driving the long-term growth of the environmentally responsible segment of the silicon-based paper industry

- In November 2024, Elkem ASA commenced operations of a chemical-recycling pilot unit at its Saint-Fons facility in France to recycle silicone waste into high-performance release liner coatings. This innovation addresses one of the market’s critical sustainability challenges — the recycling of silicone coatings themselves — enabling reintegration into new products without compromising performance. The development supports circular economy objectives and also enhances the availability of sustainable, high-quality silicone-coated papers, positioning the company as a leader in advancing environmentally responsible solutions for the global silicon-based paper market

- In January 2023, Mondi plc completed the acquisition of the Duino mill in Italy from Burgo Group and began converting it to produce high-quality recycled containerboard suitable for silicon-coated release liner applications. This strategic acquisition strengthens the upstream supply chain for silicon-based paper, increasing production capacity and securing a reliable source of paper substrates. The move allows Mondi to cater to the rising demand for high-performance, sustainable release liners, reinforcing the company’s market position while supporting the broader growth of eco-friendly silicon-based paper solutions in Europe and beyond

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Silicon Based Paper Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Silicon Based Paper Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Silicon Based Paper Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.