Global Silicone Oil Market

Market Size in USD Billion

USD

4.14 Billion

USD

7.47 Billion

2024

2032

USD

4.14 Billion

USD

7.47 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.14 Billion | |

| USD 7.47 Billion | |

| % | |

|

Silicone Oil Market Size

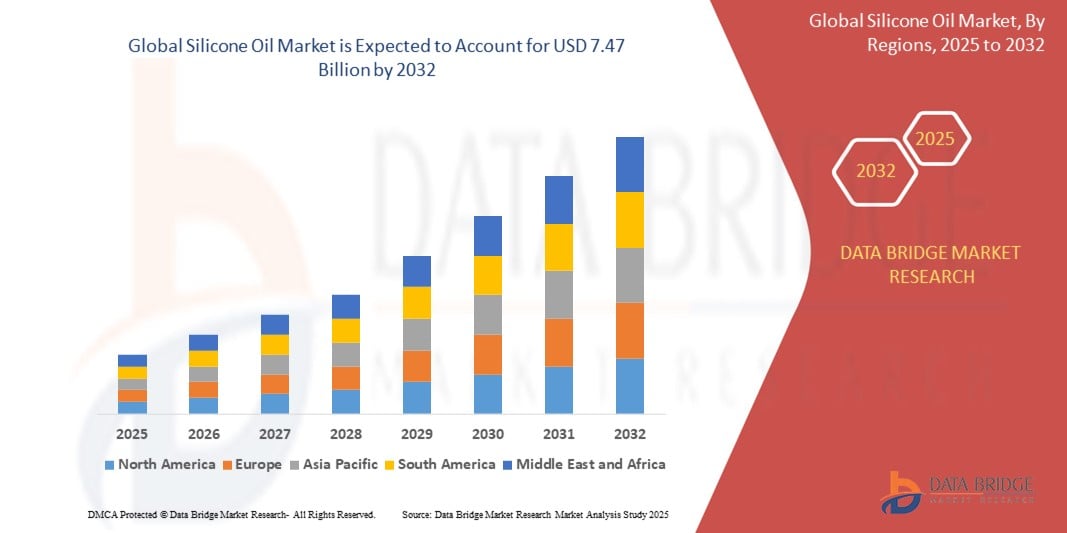

- The global silicone oil market size was valued at USD 4.14 billion in 2024 and is expected to reach USD 7.47 billion by 2032, at a CAGR of 7.65% during the forecast period

- The market growth is driven by increasing demand for silicone oil in diverse industries, including personal care, automotive, and electronics, due to its versatile properties such as thermal stability, low toxicity, and excellent lubricity

- Rising adoption of silicone oil in cosmetics, industrial applications, and advanced manufacturing processes, coupled with technological advancements, is propelling market expansion

Silicone Oil Market Analysis

- Silicone oils, known for their excellent thermal stability, chemical inertness, and versatility, are critical components in applications ranging from lubricants and sealants to personal care products and industrial formulations

- The market is fueled by growing demand in the personal care and cosmetics sector, increasing use in automotive and industrial applications, and the rising need for high-performance materials in electronics and construction

- North America dominated the silicone oil market with the largest revenue share of 38.5% in 2024, driven by advanced industrial infrastructure, high demand in electronics and automotive sectors, and the presence of key market players. The U.S. leads with significant adoption in cosmetics and industrial applications

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, propelled by rapid industrialization, urbanization, and increasing demand for personal care products in countries such as China, India, and Japan

- The straight-chained silicone oil segment dominated the largest market revenue share of 60.2% in 2024, primarily due to its widespread use in applications requiring high thermal stability, low viscosity, and excellent lubricity, such as in automotive, industrial, and personal care sectors. Its simplicity in structure ensures cost-effectiveness and versatility

Report Scope and Silicone Oil Market Segmentation

|

Attributes |

Silicone Oil Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Silicone Oil Market Trends

“Increasing Integration of AI and Big Data Analytics”

- The global silicone oil market is experiencing a notable trend toward the integration of Artificial Intelligence (AI) and Big Data analytics to optimize production, supply chain management, and application development

- These technologies enable advanced data processing, providing insights into manufacturing efficiency, raw material usage, and demand forecasting for silicone oil across industries such as automotive, cosmetics, and electronics

- AI-driven platforms are being developed to monitor production processes in real time, predicting equipment maintenance needs and minimizing downtime, thus improving operational efficiency

- For instances, companies are leveraging AI to analyze market trends and consumer preferences, enabling the formulation of specialized silicone oil products tailored for high-performance applications, such as thermal management in electric vehicles (EVs) or emollients in personal care products

- This trend enhances the precision and sustainability of silicone oil applications, increasing their appeal to manufacturers and end-users

- Big Data analytics helps track usage patterns across industries, identifying opportunities for innovation, such as eco-friendly or high-purity silicone oils for medical and pharmaceutical applications

Silicone Oil Market Dynamics

Driver

“Rising Demand for Advanced Industrial and Consumer Applications”

- Growing demand for silicone oil in diverse sectors, including automotive, personal care, electronics, and renewable energy, is a key driver for the global silicone oil market

- Silicone oil’s unique properties, such as thermal stability, chemical resistance, and low viscosity, make it essential for advanced applications such as EV battery thermal management, solar panel encapsulation, and wind turbine lubrication

- Increasing consumer preference for high-performance personal care products, such as silicone-based skincare and haircare formulations, further fuels market growth

- Government initiatives promoting renewable energy and electric mobility, particularly in regions such as Asia-Pacific and Europe, are boosting the adoption of silicone oil in sustainable technologies

- Manufacturers are increasingly incorporating silicone oil into innovative products to meet industry standards and consumer expectations for durability, efficiency, and eco-friendliness

Restraint/Challenge

“High Production Costs and Environmental Concerns”

- The high cost of producing silicone oil, driven by expensive raw materials such as silicon metal and complex manufacturing processes, poses a significant barrier to market growth, particularly in cost-sensitive regions

- Integrating silicone oil into specialized applications, such as medical-grade or high-purity formulations, requires substantial investment in research, development, and quality control

- Environmental concerns related to silicone oil production, including high energy consumption and greenhouse gas emissions, along with challenges in recycling or disposing of silicone waste, present major challenges

- Stringent environmental regulations, particularly in Europe and North America, regarding volatile organic compounds (VOCs) and waste management, complicate compliance for manufacturers and may increase operational costs

- The rise of bio-based and plant-derived alternatives, which are perceived as more sustainable, adds competitive pressure and could limit market expansion in environmentally conscious markets

Silicone Oil market Scope

The market is segmented on the basis of type, product type, function, and end-use.

- By Type

On the basis of type, the global silicone oil market is segmented into straight-chained silicone oil and modified-chained silicone oil. The straight-chained silicone oil segment dominated the largest market revenue share of 60.2% in 2024, primarily due to its widespread use in applications requiring high thermal stability, low viscosity, and excellent lubricity, such as in automotive, industrial, and personal care sectors. Its simplicity in structure ensures cost-effectiveness and versatility.

The modified-chained silicone oil segment is anticipated to witness the fastest growth rate of 8.1% from 2025 to 2032, driven by its enhanced functional properties, such as improved compatibility with organic materials, water solubility, and specialized applications in textiles, cosmetics, and construction.

- By Product Type

On the basis of product type, the global silicone oil market is segmented into polydimethylsiloxane (PDMS), phenyl methyl silicone oil, polymethyl hydrogen siloxane, amino silicone oil, vinyl silicone oil, hydrogen silicone oil, and others. The polydimethylsiloxane (PDMS) segment dominated with a market revenue share of 36.8% in 2024, owing to its versatility, biocompatibility, and widespread use as a lubricant, anti-foaming agent, and in medical and cosmetic formulations.

The phenyl methyl silicone oil segment is projected to experience the fastest growth rate of 7.9% from 2025 to 2032, fueled by its superior thermal stability and increasing demand in high-temperature applications, such as electrical insulation, high-performance lubricants, and personal care products.

- By Function

On the basis of function, the global silicone oil market is segmented into lubricants, sealant, formulations, water repellants, anti-foam agents, heat carrier, hydraulic fluids, release agent, working media, damping fluid, chemical intermediate, liquid dielectrics, additives, thermal bath fluid, and others. The lubricants segment is expected to hold the largest market revenue share of 38.6% in 2024, driven by silicone oil’s low friction coefficient, thermal stability, and broad application in automotive, industrial, and marine sectors.

The formulations segment is anticipated to witness the fastest growth rate of 8.3% from 2025 to 2032, propelled by rising demand in personal care and cosmetics for non-greasy, lightweight, and smooth-textured products, such as lotions, serums, and hair care formulations.

- By End-Use

On the basis of end-use, the global silicone oil market is segmented into electrical & electronics, automotive/transportation, industrial, building & construction, rubber and plastic industry, oil and gas, pharmaceuticals and medical, home care, consumer goods, aerospace and defence, agriculture, textiles, packaging, energy, paper and pulp, personal care and cosmetics, and others. The personal care and cosmetics segment is expected to dominate with a market revenue share of 32.5% in 2024, attributed to silicone oil’s smooth texture, spreadability, and moisturizing properties, making it a key ingredient in skincare, haircare, and makeup products.

The automotive/transportation segment is projected to witness the fastest growth rate of 8.5% from 2025 to 2032, driven by increasing adoption of silicone oil as lubricants, hydraulic fluids, and anti-foaming agents in vehicle manufacturing and maintenance, supported by the global rise in automotive production.

Silicone Oil Market Regional Analysis

- North America dominated the silicone oil market with the largest revenue share of 38.5% in 2024, driven by advanced industrial infrastructure, high demand in electronics and automotive sectors, and the presence of key market players. The U.S. leads with significant adoption in cosmetics and industrial applications

- Consumers and industries prioritize silicone oil for its thermal stability, lubricity, and versatility, particularly in regions with diverse industrial and climatic conditions

- Growth is supported by advancements in silicone oil formulations, such as high-performance lubricants and eco-friendly variants, alongside rising adoption in both industrial and consumer product segments

U.S. Silicone Oil Market Insight

The U.S. silicone oil market captured the largest revenue share of 81% in 2024 within North America, fueled by strong demand in automotive lubricants, cosmetics, and medical applications. Growing consumer awareness of silicone oil’s benefits, such as durability and heat resistance, drives market expansion. The trend towards sustainable and high-performance products, coupled with stringent quality standards, further boosts market growth.

Europe Silicone Oil Market Insight

The Europe silicone oil market is expected to witness significant growth, supported by regulatory emphasis on sustainable and high-performance materials. Industries seek silicone oils for their excellent thermal and chemical stability, particularly in automotive and industrial applications. Growth is prominent in both manufacturing and aftermarket sectors, with countries such as Germany and France showing significant adoption due to environmental concerns and advanced industrial needs.

U.K. Silicone Oil Market Insight

The U.K. market for silicone oil is expected to witness rapid growth, driven by demand for high-quality lubricants and personal care products in urban and industrial settings. Increased interest in product performance and sustainability encourages adoption. Evolving regulations promoting eco-friendly materials influence consumer and industrial choices, balancing performance with compliance.

Germany Silicone Oil Market Insight

Germany is expected to witness rapid growth in the silicone oil market, attributed to its advanced manufacturing sector and high consumer focus on efficiency and sustainability. German industries prefer technologically advanced silicone oils that enhance performance and reduce environmental impact. The integration of these oils in automotive, industrial, and personal care products supports sustained market growth.

Asia-Pacific Silicone Oil Market Insight

The Asia-Pacific region is expected to witness the fastest growth rate, driven by expanding industrial production and rising disposable incomes in countries such as China, India, and Japan. Increasing awareness of silicone oil’s versatility in automotive, cosmetics, and electronics applications boosts demand. Government initiatives promoting energy efficiency and sustainable materials further encourage the use of advanced silicone oils.

Japan Silicone Oil Market Insight

Japan’s silicone oil market is expected to witness rapid growth due to strong consumer and industrial preference for high-quality, technologically advanced silicone oils that enhance product performance and durability. The presence of major manufacturers and integration of silicone oils in automotive and electronics sectors accelerate market penetration. Rising interest in sustainable solutions also contributes to growth.

China Silicone Oil Market Insight

China holds the largest share of the Asia-Pacific silicone oil market, propelled by rapid industrialization, rising consumer demand, and increasing applications in automotive, personal care, and electronics sectors. The country’s growing middle class and focus on advanced manufacturing support the adoption of high-performance silicone oils. Strong domestic production capabilities and competitive pricing enhance market accessibility.

Silicone Oil Market Share

The silicone oil industry is primarily led by well-established companies, including:

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Elkem ASA (Norway)

- Dow (U.S.)

- FUCHS (Germany)

- Evonik Industries AG (Germany)

- Hoshine Silicon Industry Co., Ltd (China)

- Hubei Xingfa Chemicals Group Co., Ltd (China)

- BRB International B.V. (The Netherlands)

- Aurolab (India)

- Clearco Products Co., Inc. (U.S.)

- D R P Silicone (India)

- CHT Germany GmbH (Germany)

- Momentive (U.S.)

- Siltech Corporation (Canada)

- SiSiB SILICONES (China)

What are the Recent Developments in Global Silicone Oil Market?

- In May 2025, Shin-Etsu Chemical introduced KF-6070W and KF-6080W, two water-soluble silicones designed to enhance feel and texture in cosmetics. These formulations provide a smooth melting and spreading sensation, serving as emulsifiers for O/W formulations in skin care and hair care products. In addition, KSG-16-SF and KSG-19-PF, silicone elastomer gels, were launched with high light-diffusing properties, offering soft-focus effects and acting as alternatives to microplastic beads. Shin-Etsu showcased these innovations at CITE JAPAN 2025, reinforcing its commitment to sustainable beauty solutions

- In January 2025, Wacker Chemie AG inaugurated two new production facilities for specialty silicones in Japan and South Korea, reinforcing its presence in the Asian market. The Tsukuba, Japan site focuses on silicone-based thermal interface materials (TIM) for electromobility, ensuring efficient heat dissipation in electric vehicle batteries. Meanwhile, the Jincheon, South Korea facility expands silicone sealant production, catering to construction and automotive industries. This strategic expansion aligns with Wacker’s specialties strategy, supporting regional demand for high-performance silicones

- In January 2025, KCC Corporation unveiled SeraSense AG 21, an advanced silicone fluid tailored for personal care applications. This innovative formulation, featuring Bis-C16-18 Alkyl Glyceryl Undecyl Dimethicone, offers both hydrophilic and hydrophobic properties, enhancing pigment dispersion, moisture retention, and color vibrancy in cosmetic formulations. The launch underscores KCC’s commitment to innovation, strengthening its footprint in high-demand specialty markets. In addition, KCC showcased SeraSilk PDA 90 and SeraShine EM QSE, reinforcing its technological expertise in cosmetic ingredients

- In July 2024, Trelleborg Group finalized its acquisition of Baron Group, a global leader in precision silicone component manufacturing. This strategic move enhances Trelleborg’s capabilities in producing high-quality silicone solutions, particularly within medical technology applications such as sleep apnea, respiratory care, and chronic obstructive pulmonary disease (COPD). The acquisition expands manufacturing capacity for liquid silicone rubber (LSR) injection molding, reinforcing Trelleborg Medical Solutions’ presence in Asia and Australia. In addition, Baron Group’s expertise in high-volume production strengthens Trelleborg’s global reach

- In September 2023, Univar Solutions expanded its distribution partnership with Dow in Germany, strengthening its portfolio of silicone additives and resins for the paint and coatings markets. This collaboration introduces a wide range of DOWSIL™ Silicone Additives and DOWSIL™ Silicone Resins, enhancing coatings, adhesives, sealants, elastomers (CASE), and industrial products. The partnership aims to provide paint and coatings manufacturers with high-performance silicone solutions, improving weather resistance, gloss retention, and VOC compliance

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDYD

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL SILICONE OIL MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 TYPE LIFE LINE CURVE

2.7 MULTIVARIATE MODELING

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET END-USE COVERAGE GRID

2.11 DBMR MARKET CHALLENGE MATRIX

2.12 DBMR VENDOR SHARE ANALYSIS

2.13 SECONDARY SOURCES

2.14 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTLE ANALYSIS

4.1.1 POLITICAL FACTORS

4.1.2 ECONOMIC FACTORS

4.1.3 SOCIAL FACTORS

4.1.4 TECHNOLOGICAL FACTORS

4.1.5 LEGAL FACTORS

4.1.6 ENVIRONMENTAL FACTORS

4.2 PORTER’S FIVE FORCES

4.2.1 THREAT OF NEW ENTRANTS

4.2.2 THE THREAT OF SUBSTITUTES

4.2.3 SUPPLIERS BARGAINING POWER

4.2.4 BUYERS BARGAINING POWER

4.2.5 INTERNAL COMPETITION (RIVALRY)

4.3 CLIMATE CHANGE SCENARIO

4.3.1 ENVIRONMENTAL CONCERNS

4.3.2 INDUSTRY RESPONSE

4.3.3 GOVERNMENT ROLE

4.3.4 ANALYST RECOMMENDATION

4.4 END USERS INSIGHTS

4.5 RAW MATERIAL COVERAGE

4.6 SUPPLY CHAIN ANALYSIS

4.6.1 OVERVIEW

4.6.2 LOGISTIC COST SCENARIO

4.6.3 IMPORTANCE OF LOGISTICS SERVICE PROVIDERS

4.7 TECHNOLOGICAL ADVANCEMENT BY MANUFACTURERS

4.8 VENDOR SELECTION CRITERIA

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 GROWING USE OF SILICONE OIL IN THE TEXTILE INDUSTRY

5.1.2 GROWING DEMAND FOR SILICONE OIL IN AUTOMOTIVE APPLICATIONS

5.1.3 WIDESPREAD ADOPTION OF SILICONE OIL ACROSS DIVERSE INDUSTRIES, INCLUDING COSMETICS AND PERSONAL CARE

5.1.4 SURGE IN THE DEMAND FOR SILICONE OIL FROM THE HEALTHCARE AND MEDICAL SECTOR

5.2 RESTRAINTS

5.2.1 FLUCTUATIONS IN THE RAW MATERIAL PRICES

5.2.2 INTENSE COMPETITION FROM ALTERNATIVES

5.3 OPPORTUNITIES

5.3.1 EXPANDING EMPHASIS ON RENEWABLE ENERGY

5.3.2 RISING UPTAKE OF SILICONE OIL IN THE AEROSPACE INDUSTRY

5.3.3 INCREASING FOCUS ON RESEARCH AND DEVELOPMENT FOR THE APPLICATION OF SILICONE OIL

5.4 CHALLENGES

5.4.1 STRINGENT ENVIRONMENTAL REGULATIONS

5.4.2 CONCERNS RELATED TO WASTE MANAGEMENT AND RECYCLING

6 GLOBAL SILICONE OIL MARKET, BY TYPE

6.1 OVERVIEW

6.2 STRAIGHT-CHAINED SILICONE OIL

6.3 MODIFIED-CHAINED SILICONE OIL

7 GLOBAL SILICONE OIL MARKET, BY PRODUCT TYPE

7.1 OVERVIEW

7.2 POLYDIMETHYLSILOXANE (PDMS)

7.3 PHENYL METHYL SILICONE OIL

7.4 POLYMETHYL HYDROGEN SILOXANE

7.5 AMINO SILICONE OIL

7.6 VINYL SILICONE OIL

7.7 HYDROGEN SILICONE OIL

7.8 OTHERS

8 GLOBAL SILICONE OIL MARKET, BY FUNCTION

8.1 OVERVIEW

8.2 LUBRICANTS

8.3 SEALANT

8.4 FORMULATIONS

8.5 WATER REPELLANTS

8.6 ANTI- FOAM AGENTS

8.7 HEAT CARRIER

8.8 HYDRAULIC FLUIDS

8.9 RELEASE AGENT

8.1 WORKING MEDIA

8.11 DAMPING FLUID

8.12 CHEMICAL INTERMEDIATE

8.13 LIQUID DIELECTRICS

8.14 ADDITIVES

8.15 THERMAL BATH FLUID

8.16 OTHERS

9 GLOBAL SILICONE OIL MARKET, BY END USE

9.1 OVERVIEW

9.2 ELECTRICAL & ELECTRONICS

9.2.1 ELECTRICAL & ELECTRONICS, BY TYPE

9.2.2 ELECTRICAL & ELECTRONICS, BY PRODUCT TYPE

9.2.3 ELECTRICAL & ELECTRONICS, BY FUNCTION

9.3 AUTOMOTIVE/TRANSPORTATION

9.3.1 AUTOMOTIVE/TRANSPORTATION, BY END-USE

9.3.2 AUTOMOTIVE/TRANSPORTATION, BY TYPE

9.3.3 AUTOMOTIVE/TRANSPORTATION, BY PRODUCT TYPE

9.3.4 AUTOMOTIVE/TRANSPORTATION, BY FUNCTION

9.4 INDUSTRIAL

9.4.1 INDUSTRIAL, BY TYPE

9.4.2 INDUSTRIAL, BY PRODUCT TYPE

9.4.3 INDUSTRIAL, BY FUNCTION

9.5 BUILDING & CONSTRUCTION

9.5.1 BUILDING & CONSTRUCTION, BY END-USE

9.5.2 BUILDING & CONSTRUCTION, BY TYPE

9.5.3 BUILDING & CONSTRUCTION, BY PRODUCT TYPE

9.5.4 BUILDING & CONSTRUCTION, BY FUNCTION

9.6 RUBBER AND PLASTIC INDUSTRY

9.6.1 RUBBER AND PLASTIC INDUSTRY, BY TYPE

9.6.2 RUBBER AND PLASTIC INDUSTRY, BY PRODUCT TYPE

9.6.3 RUBBER AND PLASTIC INDUSTRY, BY FUNCTION

9.7 OIL AND GAS

9.7.1 OIL AND GAS, BY TYPE

9.7.2 OIL AND GAS, BY PRODUCT TYPE

9.7.3 OIL AND GAS, BY FUNCTION

9.8 PHARMACEUTICALS AND MEDICAL

9.8.1 PHARMACEUTICALS AND MEDICAL, BY END-USE

9.8.2 PHARMACEUTICALS AND MEDICAL, BY TYPE

9.8.3 PHARMACEUTICALS AND MEDICAL, BY PRODUCT TYPE

9.8.4 PHARMACEUTICALS AND MEDICAL, BY FUNCTION

9.9 HOME CARE

9.9.1 HOME CARE, BY TYPE

9.9.2 HOME CARE, BY PRODUCT TYPE

9.9.3 HOME CARE, BY FUNCTION

9.1 CONSUMER GOODS

9.10.1 CONSUMER GOODS, BY TYPE

9.10.2 CONSUMER GOODS, BY PRODUCT TYPE

9.10.3 CONSUMER GOODS, BY FUNCTION

9.11 AEROSPACE AND DEFENCE

9.11.1 AEROSPACE AND DEFENCE, BY TYPE

9.11.2 AEROSPACE AND DEFENCE, BY PRODUCT TYPE

9.11.3 AEROSPACE AND DEFENCE, BY FUNCTION

9.12 AGRICULTURE

9.12.1 AGRICULTURE, BY TYPE

9.12.2 AGRICULTURE, BY PRODUCT TYPE

9.12.3 AGRICULTURE, BY FUNCTION

9.13 TEXTILES

9.13.1 TEXTILES, BY TYPE

9.13.2 TEXTILES, BY PRODUCT TYPE

9.13.3 TEXTILES, BY FUNCTION

9.14 PACKAGING

9.14.1 PACKAGING, BY TYPE

9.14.2 PACKAGING, BY PRODUCT TYPE

9.14.3 PACKAGING, BY FUNCTION

9.15 ENERGY

9.15.1 ENERGY, BY TYPE

9.15.2 ENERGY, BY PRODUCT TYPE

9.15.3 ENERGY, BY FUNCTION

9.16 PAPER AND PULP

9.16.1 PAPER AND PULP, BY TYPE

9.16.2 PAPER AND PULP, BY PRODUCT TYPE

9.16.3 PAPER AND PULP, BY FUNCTION

9.17 PERSONAL CARE AND COSMETICS

9.17.1 PERSONAL CARE AND COSMETICS, BY END-USE

9.17.2 PERSONAL CARE AND COSMETICS, BY TYPE

9.17.3 PERSONAL CARE AND COSMETICS, BY PRODUCT TYPE

9.17.4 PERSONAL CARE AND COSMETICS, BY FUNCTION

9.18 OTHERS

9.18.1 OTHERS, BY TYPE

9.18.2 OTHERS, BY PRODUCT TYPE

9.18.3 OTHERS, BY FUNCTION

10 GLOBAL SILICONE OIL MARKET, BY REGION

10.1 OVERVIEW

10.2 NORTH AMERICA

10.2.1 U.S.

10.2.2 CANADA

10.2.3 MEXICO

10.3 EUROPE

10.3.1 GERMANY

10.3.2 U.K.

10.3.3 FRANCE

10.3.4 RUSSIA

10.3.5 ITALY

10.3.6 SPAIN

10.3.7 NETHERLANDS

10.3.8 SWITZERLAND

10.3.9 TURKEY

10.3.10 BELGIUM

10.3.11 REST OF EUROPE

10.4 ASIA-PACIFIC

10.4.1 CHINA

10.4.2 JAPAN

10.4.3 SOUTH KOREA

10.4.4 INDIA

10.4.5 AUSTRALIA & NEW ZEALAND

10.4.6 TAIWAN

10.4.7 SINGAPORE

10.4.8 THAILAND

10.4.9 INDONESIA

10.4.10 MALAYSIA

10.4.11 PHILIPPINES

10.4.12 HONG KONG

10.4.13 REST OF ASIA-PACIFIC

10.5 MIDDLE EAST AND AFRICA

10.5.1 SAUDI ARABIA

10.5.2 UNITED ARAB EMIRATES

10.5.3 SOUTH AFRICA

10.5.4 EGYPT

10.5.5 ISRAEL

10.5.6 REST OF MIDDLE EAST AND AFRICA

10.6 SOUTH AMERICA

10.6.1 BRAZIL

10.6.2 ARGENTINA

10.6.3 REST OF SOUTH AMERICA

11 GLOBAL SILICONE OIL MARKET: COMPANY LANDSCAPE

11.1 COMPANY SHARE ANALYSIS: GLOBAL

11.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

11.3 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

11.4 COMPANY SHARE ANALYSIS: EUROPE

11.5 NEW PRODUCTION PLANTS

11.6 ANNOUNCEMENT

11.7 PRODUCT LAUNCHES

12 SWOT ANALYSIS

13 COMPANY PROFILES

13.1 DOW

13.1.1 COMPANY SNAPSHOT

13.1.2 REVENUE ANALYSIS

13.1.3 COMPANY SHARE ANALYSIS

13.1.4 PRODUCT PORTFOLIO

13.1.5 RECENT DEVELOPMENTS

13.2 HUBEI XINGFA CHEMICALS GROUP CO., LTD

13.2.1 COMPANY SNAPSHOT

13.2.2 COMPANY SHARE ANALYSIS

13.2.3 PRODUCT PORTFOLIO

13.2.4 RECENT DEVELOPMENTS

13.3 EVONIK INDUSTRIES AG

13.3.1 COMPANY SNAPSHOT

13.3.2 REVENUE ANALYSIS

13.3.3 COMPANY SHARE ANALYSIS

13.3.4 PRODUCT PORTFOLIO

13.3.5 RECENT DEVELOPMENTS

13.4 WACKER CHEMIE AG

13.4.1 COMPANY SNAPSHOT

13.4.2 REVENUE ANALYSIS

13.4.3 COMPANY SHARE ANALYSIS

13.4.4 PRODUCT PORTFOLIO

13.4.5 RECENT DEVELOPMENTS

13.5 FUCHS

13.5.1 COMPANY SNAPSHOT

13.5.2 REVENUE ANALYSIS

13.5.3 COMPANY SHARE ANALYSIS

13.5.4 PRODUCT PORTFOLIO

13.5.5 RECENT DEVELOPMENTS

13.6 ALSTONE INDUSTRIES PVT. LTD

13.6.1 COMPANY SNAPSHOT

13.6.2 PRODUCT PORTFOLIO

13.6.3 RECENT DEVELOPMENTS

13.7 ARIHANT SOLVENTS AND CHEMICALS

13.7.1 COMPANY SNAPSHOT

13.7.2 PRODUCT PORTFOLIO

13.7.3 RECENT DEVELOPMENTS

13.8 AUROLAB

13.8.1 COMPANY SNAPSHOT

13.8.2 PRODUCT PORTFOLIO

13.8.3 RECENT DEVELOPMENTS

13.9 BRB INTERNATIONAL B.V. (A SUBSIDIARY OF PETRONAS CHEMICALS GROUP BERHAD)

13.9.1 COMPANY SNAPSHOT

13.9.2 PRODUCT PORTFOLIO

13.9.3 RECENT DEVELOPMENTS

13.1 CHT GERMANY GMBH

13.10.1 COMPANY SNAPSHOT

13.10.2 PRODUCT PORTFOLIO

13.10.3 RECENT DEVELOPMENTS

13.11 CLEARCO PRODUCTS CO., INC.

13.11.1 COMPANY SNAPSHOT

13.11.2 PRODUCT PORTFOLIO

13.11.3 RECENT DEVELOPMENTS

13.12 D R P SILICONE

13.12.1 COMPANY SNAPSHOT

13.12.2 PRODUCT PORTFOLIO

13.12.3 RECENT DEVELOPMENTS

13.13 ELECTROLUBE

13.13.1 COMPANY SNAPSHOT

13.13.2 PRODUCT PORTFOLIO

13.13.3 RECENT DEVELOPMENTS

13.14 ELKEM ASA

13.14.1 COMPANY SNAPSHOT

13.14.2 REVENUE ANALYSIS

13.14.3 PRODUCT PORTFOLIO

13.14.4 RECENT DEVELOPMENTS

13.15 HOSHINE SILICON INDUSTRY CO., LTD

13.15.1 COMPANY SNAPSHOT

13.15.2 PRODUCT PORTFOLIO

13.15.3 RECENT DEVELOPMENTS

13.16 IOTA SILICONE

13.16.1 COMPANY SNAPSHOT

13.16.2 PRODUCT PORTFOLIO

13.16.3 RECENT DEVELOPMENTS

13.17 MOMENTIVE

13.17.1 COMPANY SNAPSHOT

13.17.2 PRODUCT PORTFOLIO

13.17.3 RECENT DEVELOPMENTS

13.18 SHIN-ETSU CHEMICAL CO., LTD

13.18.1 COMPANY SNAPSHOT

13.18.2 REVENUE ANALYSIS

13.18.3 PRODUCT PORTFOLIO

13.18.4 RECENT DEVELOPMENTS

13.19 SILTECH CORPORATION

13.19.1 COMPANY SNAPSHOT

13.19.2 PRODUCT PORTFOLIO

13.19.3 RECENT DEVELOPMENTS

13.2 SISIB SILICONES (SUBSIDIARY OF PCC GROUP)

13.20.1 COMPANY SNAPSHOT

13.20.2 PRODUCT PORTFOLIO

13.20.3 RECENT DEVELOPMENTS

14 QUESTIONNAIRE

15 RELATED REPORTS

Global Silicone Oil Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Silicone Oil Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Silicone Oil Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.