Global Silicone Textile Chemicals Market

Market Size in USD Billion

USD

1.84 Billion

USD

3.19 Billion

2024

2032

USD

1.84 Billion

USD

3.19 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.84 Billion | |

| USD 3.19 Billion | |

| % | |

|

Silicone Textile Chemicals Market Size

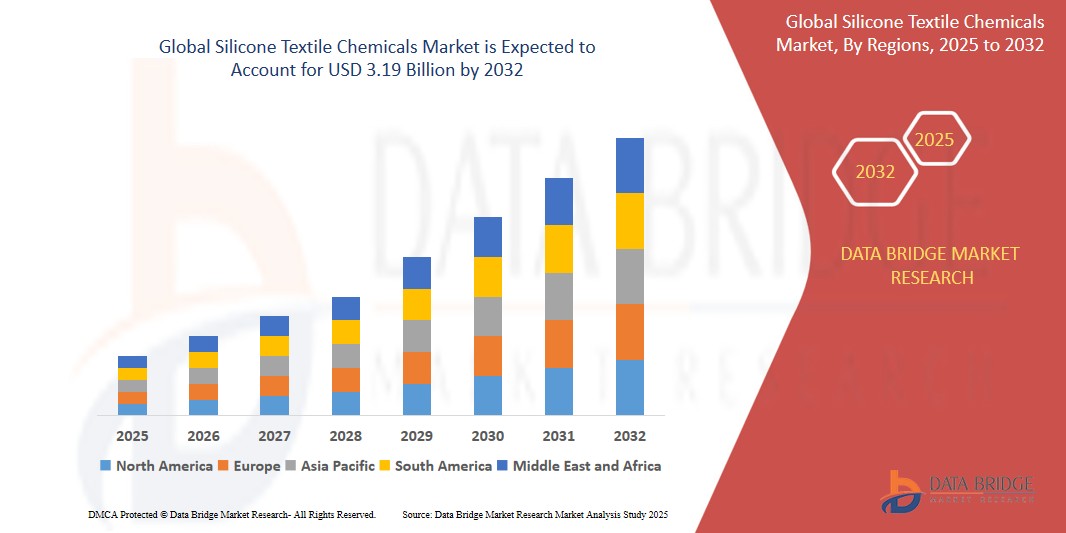

- The Global Silicone Textile Chemicals Market size was valued at USD 1.84 billion in 2024 and is expected to reach USD 3.19 billion by 2032, at a CAGR of 6.3% during the forecast period

- The market growth is largely fueled by the rising shift in consumer inclination towards foreign textile brands

- Furthermore, the rising research and development proficiencies on green or bio-based chemicals that are prepared from renewable resources, rising adoption of green chemicals and growth and expansion of various end user verticals such as chemicals and materials industry especially in the developing economies is further anticipated to propel the growth of the silicone textile chemicals market

Silicone Textile Chemicals Market Analysis

- The rise in the use of silicone textile chemicals for a wide range of end user applications such as apparel, home and office furnishing, technical textiles and others, strong influence of social media and surge in industrialization especially in the developing countries is escalating the growth of silicone textile chemicals market

- Silicone technology has brought in a revolution in the textile industry. Silicone textile chemicals are high purity silicone-based chemicals that are usually added in the pre-treatment of textiles. Some of the commonly used textile chemicals silicone textile chemicals are used in the form of fluids, emulsions, oils and antifoams

- North America dominates the Silicone Textile Chemicals market with the largest revenue share of 44.16% in 2025, characterized by high demand for premium textiles, technological advancements, and strong R&D infrastructure.

- Asia-Pacific is expected to be the fastest growing region in the Silicone Textile Chemicals market during the forecast period due to rising textile production, export growth, and regulatory improvements. Countries like China, India, Bangladesh, and Vietnam are leading in textile exports

- Silicon softeners segment is expected to dominate the Silicone Textile Chemicals market with a market share of 40.21% in 2025, driven by its cost-effectiveness, ease of formulation, and broad applicability across textile types

Report Scope and Silicone Textile Chemicals Market Segmentation

|

Attributes |

Silicone Textile Chemicals Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

|

Silicone Textile Chemicals Market Trends

“Growing Integration of Smart Finishing Technologies in Textile Processing”

- A notable trend in the Global Silicone Textile Chemicals Market is the increasing use of smart finishing technologies to enhance textile properties such as softness, elasticity, water repellency, and durability. Advanced silicone-based finishes are enabling manufacturers to offer high-performance textiles for various end-use applications.

- For instance, new-generation amino-functional silicones provide better compatibility with synthetic and natural fibers, leading to improved hand feel and fabric resilience, especially in sportswear and home textiles.

- The trend also includes the development of multifunctional silicones that combine benefits such as anti-pilling, wrinkle resistance, and antimicrobial features, reducing the need for multiple chemical treatments.

- In parallel, the adoption of silicone-based softeners and hydrophobes that align with eco-certifications is rising, addressing both performance and sustainability criteria.

- These advancements are reshaping the Silicone Textile Chemicals landscape, supporting innovation in sustainable fabric enhancement while meeting evolving consumer and industry expectations.

Silicone Textile Chemicals Market Dynamics

Driver

“Rising Demand for Sustainable and High-Performance Textile Finishes”

- The growing demand for textile products with enhanced comfort, stretchability, and environmental compatibility is a major driver of the Silicone Textile Chemicals market. Silicone-based finishes offer superior softness, fabric protection, and long-lasting effects compared to conventional chemicals.

- Increasing consumer preference for eco-friendly and premium-quality garments is pushing textile manufacturers to adopt silicone solutions that meet both performance standards and regulatory compliance.

- Additionally, the shift toward water-efficient and low-VOC formulations is aligning with global sustainability trends, further boosting the market for silicone-based textile chemicals.

Restraint/Challenge

“Cost Sensitivity and Limited Adoption in Price-Conscious Markets”

- The relatively higher cost of silicone-based chemicals compared to traditional textile finishes remains a key restraint, particularly in price-sensitive markets such as Southeast Asia and parts of Africa.

- Smaller textile mills may hesitate to invest in silicone solutions due to budget constraints and uncertainty over immediate ROI, slowing adoption in emerging regions.

- Addressing this challenge requires pricing strategies, technological simplification, and awareness campaigns to demonstrate the long-term benefits and sustainability advantages of silicone textile chemicals.

Silicone Textile Chemicals Market Scope

The market is segmented on the basis of type, form, silicone technology, silicone modifications, textile type, and application.

- By Type

On the basis of type, the silicone textile chemicals market is segmented into silicon softeners, micro emulsion silicon, and others. The silicon softeners segment dominates the largest market revenue share of 40.21% in 2025, driven by its cost-effectiveness, ease of formulation, and broad applicability across textile types. Manufacturers favor silicon softeners due to their compatibility with traditional and modern textile finishes, and their ability to impart softness, flexibility, and enhanced hand-feel to fabrics. The market also sees rising demand due to environmentally compliant formulations and their proven performance in bulk dyeing and finishing operations.

The micro emulsion silicon segment is anticipated to witness the fastest growth rate of 21.7% from 2025 to 2032, fueled by its superior penetration, smoother surface finish, and versatility in blending with other softeners. Increasing use in high-end garments and technical fabrics supports this growth, along with the demand for sustainable, high-performance finishes in premium textile products.

- By Form

On the basis of form, the silicone textile chemicals market is segmented into fluids, emulsions, and antifoams. The fluids held the largest market revenue share in 2025 of, driven by their easy integration into manufacturing lines, stable performance under various processing conditions, and strong demand from the apparel and home furnishing sectors. These fluid forms allow high efficiency in the treatment process and are often tailored for specific textile properties like softness, drape, and static control.

The emulsions segment is expected to witness the fastest CAGR from 2025 to 2032, supported by increasing demand for cost-effective and water-based alternatives to conventional oils. Emulsions offer environmental compliance and versatility across applications, making them a favorable choice for textile processors seeking enhanced finishing results with reduced environmental impact.

- By Silicone Technology

On the basis of silicone technology, the meat testing market is segmented into polydimethylsiloxanes and special silicone fluids. The polydimethylsiloxanes segment accounted for the largest market revenue share in 2025, attributed to their well-established safety profile, cost-efficiency, and broad compatibility with textile formulations. Their consistent performance in imparting softness and improved tear strength positions them as a preferred base for a wide range of fabric softeners.

The special silicone fluids segment is projected to witness the fastest CAGR from 2025 to 2032, driven by growing demand in niche markets such as technical and medical textiles. These fluids offer enhanced durability, resistance to washing, and hydrophobicity, making them ideal for advanced textile finishes and high-performance fabrics.

- By Silicone Modifications

On the basis of silicone modifications, the meat testing market is segmented into methyl group, amino group, hydrophilic group, hydrogen group, and other organo modifications. The amino group segment dominates the largest market revenue share in 2025, due to its superior softening effects, fabric smoothness, and excellent compatibility with various textile chemistries. It is highly preferred in cotton and synthetic finishing processes for its long-lasting soft feel.

The hydrophilic group segment is expected to register the fastest CAGR from 2025 to 2032, owing to increasing demand for breathable, quick-drying, and moisture-managing fabrics in sportswear and technical textiles. Enhanced wearer comfort and rising consumer preference for functional garments further fuel this growth.

- By Textile Type

On the basis of textile type, the meat testing market is segmented into component fibers, synthetic fibers, and inorganic fibers. The synthetic fibers segment accounted for the largest market revenue share in 2025, owing to the high usage of polyester and nylon in mass textile manufacturing. The compatibility of silicone finishes with synthetic substrates enhances fabric softness, dye uptake, and aesthetic value.

The inorganic fibers segment is anticipated to witness the fastest CAGR from 2025 to 2032, supported by growing adoption in protective clothing, insulation materials, and specialty applications. These fibers benefit from silicone treatments for thermal stability and enhanced surface functionality, crucial in high-performance end-uses.

- By Application

On the basis of application, the meat testing market is segmented into apparel, home and office furnishing, technical textiles, and others. The apparel segment accounted for the largest market revenue share in 2025, driven by rising fashion trends, increased disposable income, and demand for comfortable, durable clothing. Silicone treatments are widely used to enhance softness, stretch, and wrinkle resistance in garments.

The technical textiles segment is projected to experience the fastest CAGR from 2025 to 2032, fueled by its growing importance in automotive, medical, and industrial sectors. The demand for performance-enhancing finishes, such as water repellency, antimicrobial effects, and thermal resistance, positions silicone treatments as essential in this high-growth category.

Silicone Textile Chemicals Market Regional Analysis

- North America dominates the Silicone Textile Chemicals Market with the largest revenue share of 44.16% in 2024, driven by high demand for premium textiles, technological advancements, and strong R&D infrastructure.

- The region is home to leading manufacturers and is characterized by a preference for sustainable and performance-enhancing chemicals.

- The U.S. textile industry’s focus on innovation, functional fabrics, and eco-label certifications significantly contributes to regional dominance. Silicone chemicals are widely adopted for softeners, water repellents, and antifoaming agents across diverse textile applications such as sportswear, medical fabrics, and automotive interiors.

U.S. Silicone Textile Chemicals Market Insight

The U.S. Silicone Textile Chemicals Market captured the largest revenue share of 81.24% within North America in 2025, fueled by the consumer demand for soft, high-performance fabrics and rapid adoption of eco-friendly solutions. U.S. manufacturers are incorporating silicone-based treatments to improve durability, stretch, and comfort in textiles. Growing awareness about sustainable production and the expansion of technical textile applications further supports market growth.

Europe Silicone Textile Chemicals Market Insight

The European silicone textile chemicals market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by EU regulations promoting sustainable chemical use and rising demand for functional apparel. Europe’s mature textile industry emphasizes compliance with REACH guidelines, pushing demand for low-VOC, non-toxic silicone finishes. Innovation in smart textiles and premium home furnishing fabrics also contributes to growth.

U.K. Silicone Textile Chemicals Market Insight

The U.K. silicone textile chemicals market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by demand for eco-labeled and skin-safe textile finishes. Post-Brexit regulatory transitions have encouraged manufacturers to upgrade chemical formulations for better compliance. Consumer preference for breathable, soft-touch fabrics and water-repellent treatments is supporting steady silicone chemical adoption in domestic production.

Germany Silicone Textile Chemicals Market Insight

The German Silicone Textile Chemicals market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s strong technical textiles sector and export-driven textile manufacturing. Silicone chemicals are increasingly used for high-performance fabrics in industries like automotive, healthcare, and industrial wear. Additionally, growing investment in sustainable processing technologies is accelerating the shift toward silicone-based alternatives.

Asia-Pacific Silicone Textile Chemicals Market Insight

The Asia-Pacific Silicone Textile Chemicals market is poised to grow at the fastest CAGR of over 25.26% in 2025, driven by rising textile production, export growth, and regulatory improvements. Countries like China, India, Bangladesh, and Vietnam are leading in textile exports and are increasingly adopting silicone chemicals for better quality and compliance. The region benefits from lower production costs and a surge in domestic demand for functional and comfortable textiles.

Japan Silicone Textile Chemicals Market Insight

The Japan Silicone Textile Chemicals market is gaining momentum due to growing demand for smart textiles, high-quality apparel, and long-lasting fabric treatments. Japan’s reputation for innovation and precision in textile manufacturing supports the integration of silicone chemicals that improve softness, durability, and thermal comfort. Sustainability targets and consumer expectations for product performance further contribute to the market’s positive outlook.

China Silicone Textile Chemicals Market Insight

The China Silicone Textile Chemicals Market accounted for the largest market revenue share in Asia Pacific in 2025, driven by rapid industrialization and the country’s position as a global textile manufacturing hub. Rising environmental regulations, investments in clean technologies, and the shift toward high-value-added textiles are pushing demand for silicone chemicals. Domestic manufacturers are increasingly using silicone-based softeners, finishes, and emulsions to meet both domestic and export standards.

Silicone Textile Chemicals Market Share

The Silicone Textile Chemicals industry is primarily led by well-established companies, including:

- Mitsubishi Chemical Corporation (Japan)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Huntsman International LLC (U.S.)

- Wacker Chemie AG (Germany)

- Momentive (U.S.)

- Evonik Industries AG (Germany)

- Elkem ASA (Norway)

- NICCA U.S.A. Inc. (U.S.)

- Piedmont Chemical Industries (U.S.)

- CHT Germany GmbH (Germany)

- Weifang Ruiguang Chemical Co., Ltd. (China)

- zxchem group (China)

- Dow (U.S.)

- Nouryon (Netherlands)

Latest Developments in Global Silicone Textile Chemicals Market

- In July 2024, JAY Chemical Industries Private Limited established a cutting-edge manufacturing facility in Saykha, near Dahej, focused on producing ethylene oxide and propylene oxide-based derivatives, along with formulated products primarily used in textile auxiliaries. These derivatives play a vital role in lowering surface and interfacial tension, thereby improving the stability and longevity of various substances.

- In February 2024, Birla Cellulose introduced Birla Viscose – Intellicolor, an innovative textile solution unveiled at Bharat Tex. This breakthrough addresses long-standing challenges in traditional reactive dyeing by incorporating basic and cationic dyes, achieving over 95% dye exhaustion. The result is more vibrant colors, reduced chemical usage, enhanced fabric durability, and significantly faster production processes.

- In 2023, leading chemical firms such as Dow, Arkema, and BASF intensified their adoption of digital technologies to boost operational efficiency. This shift has been critical for improving the productivity of textile chemicals, including silicone-based formulations, amid volatile raw material prices and ongoing supply chain issues.

- In 2022, the industry witnessed a strong shift toward sustainable and eco-friendly silicone solutions. Companies like Wacker Chemie and Momentive ramped up investments in developing greener alternatives to conventional textile chemicals, largely in response to increasing environmental awareness and tighter global regulatory standards.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Silicone Textile Chemicals Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Silicone Textile Chemicals Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Silicone Textile Chemicals Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.