Global Single Lead Ecg Equipment Market

Market Size in USD Billion

USD

413.16 Billion

USD

620.73 Billion

2025

2033

USD

413.16 Billion

USD

620.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 413.16 Billion | |

| USD 620.73 Billion | |

| % | |

|

Single Lead Electrocardiogram (ECG) Equipment Market Overview

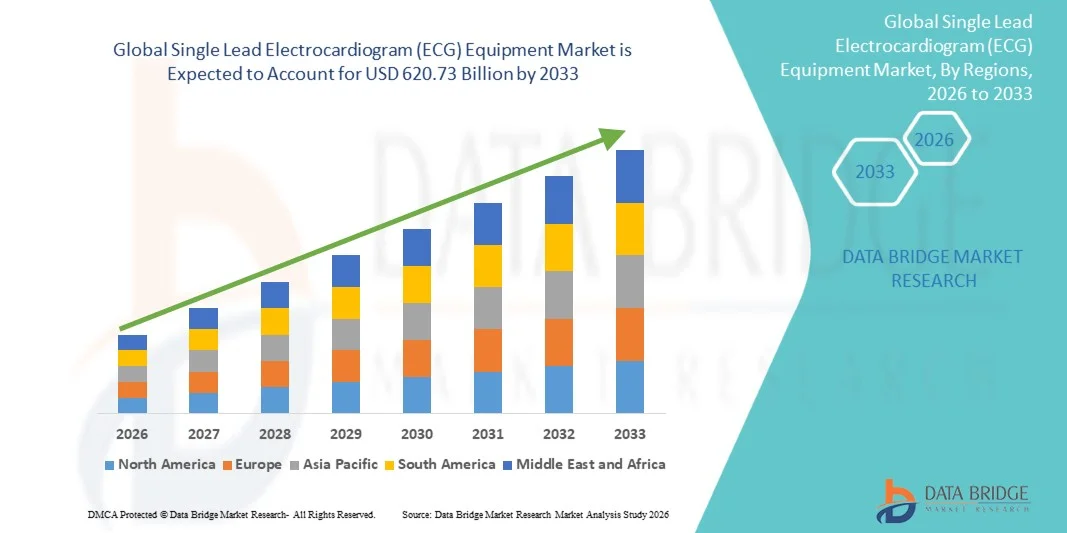

The Single Lead Electrocardiogram (ECG) Equipment Market was valued at USD 413.16 billion in 2025 and is projected to reach USD 620.73 billion by 2033, growing at a CAGR of 5.22% from 2026 to 2033. The Single Lead Electrocardiogram (ECG) Equipment Market is experiencing steady growth driven by rising prevalence of cardiovascular diseases, increasing demand for portable and home-based cardiac monitoring solutions, and rapid advancements in digital health technologies. The growing burden of heart-related disorders, including arrhythmias and atrial fibrillation, is significantly increasing the need for early diagnosis and continuous cardiac monitoring, especially outside traditional hospital settings.

The increasing adoption of remote patient monitoring, wearable health devices, and telemedicine platforms is further accelerating market expansion. Single lead ECG devices, being compact, cost-effective, and easy to use, are widely utilized in ambulatory care, emergency response, and home healthcare settings. Growing awareness about preventive healthcare and early cardiac screening, combined with the integration of AI-powered diagnostic algorithms and smartphone connectivity, is enabling real-time heart monitoring and faster clinical decision-making. Additionally, expanding healthcare infrastructure, rising geriatric population, and increasing focus on reducing hospital readmission rates are further supporting the adoption of single lead ECG equipment across both developed and emerging markets.

Key Market Trends & Insights

- North America dominated the Single Lead Electrocardiogram (ECG) Equipment Market with the largest revenue share of 38.91% in 2025, supported by high prevalence of cardiovascular diseases, advanced healthcare infrastructure, and strong adoption of remote patient monitoring and wearable cardiac devices. The region benefits from widespread use of AI-enabled ECG interpretation tools, strong telemedicine penetration, and increasing focus on preventive cardiac care across hospitals and home-care settings.

- The Arrhythmia segment dominated the market with a 46.32% share in 2025 due to the high global prevalence of atrial fibrillation, cardiac rhythm disorders, and increasing incidence of cardiovascular diseases.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.9% from 2026 to 2033, fueled by rising cardiovascular disease burden, expanding healthcare infrastructure, increasing awareness of early cardiac screening, and growing adoption of portable and wearable ECG devices in China, India, and Japan.

- The Home-Care segment is expected to be the fastest-growing end-use category, projected to register a CAGR of 8.1%, driven by increasing adoption of remote patient monitoring, wearable ECG patches, and rising preference for at-home cardiac care solutions supported by telehealth expansion.

- The Syncope segment is expected to grow steadily, driven by increasing cases of unexplained fainting episodes requiring continuous ECG monitoring and improved diagnostic accuracy through portable single lead ECG systems.

- Hospitals and Clinics dominate the end-use category with a 52.18% revenue share in 2025, supported by high patient inflow, advanced diagnostic infrastructure, and widespread use of ECG devices for emergency cardiac assessment and routine monitoring.

Market Size & Forecast

- Global Market Value (2025): USD 413.16 Billion

- Expected Market Value (2033): USD 620.73 Billion

- Forecast CAGR (2026–2033): 5.22%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Single Lead Electrocardiogram (ECG) Equipment Market Segmentation

|

Attributes |

Single Lead Electrocardiogram (ECG) Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• AliveCor Inc. (U.S.) |

|

Market Opportunities |

· Rising adoption of remote patient monitoring (RPM) and telehealth platforms · Growing demand for wearable and patch-based ECG devices creates strong opportunities · Expansion of preventive healthcare programs and early cardiac screening initiatives |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Single Lead Electrocardiogram (ECG) Equipment Market Trends

Trend: Growth in Remote Patient Monitoring & Wearable Cardiac Devices

The Single Lead Electrocardiogram (ECG) Equipment Market is witnessing strong growth due to increasing adoption of wearable and remote cardiac monitoring devices for continuous heart health assessment. Devices such as patch-based ECG monitors and smartwatch-integrated ECG systems are increasingly used for real-time arrhythmia detection and long-term cardiac tracking. Companies such as AliveCor (KardiaMobile) and iRhythm Technologies (Zio Patch) are leading this transformation, enabling continuous ambulatory ECG monitoring outside traditional hospital settings. Clinical studies indicate that continuous ECG monitoring can improve atrial fibrillation detection rates by up to 30–40% compared to standard short-term ECG testing, significantly improving early diagnosis and treatment outcomes. The integration of cloud connectivity and mobile health platforms is further enabling remote physician access to patient cardiac data, strengthening digital healthcare adoption globally.

Single Lead Electrocardiogram (ECG) Equipment Market Dynamics

Key Market Driver: Rising Cardiovascular Disease Burden and Expansion of Digital Cardiac Monitoring

The increasing prevalence of cardiovascular diseases, including arrhythmia, atrial fibrillation, and syncope-related conditions, is a major driver for the Single Lead ECG equipment market. According to global health estimates, cardiovascular diseases account for nearly 17.9 million deaths annually worldwide, creating strong demand for early detection and continuous monitoring solutions. Single lead ECG devices are increasingly preferred for their portability, affordability, and ease of use in both clinical and home-care settings. Companies such as Apple Inc. (Apple Watch ECG feature), Samsung Electronics, and Omron Healthcare are integrating ECG functionality into wearable devices, enabling large-scale population screening. Hospitals and cardiology centers are adopting AI-enabled ECG interpretation systems to improve diagnostic accuracy and reduce physician workload. Increasing telemedicine adoption, especially in the U.S., Europe, and Japan, is further accelerating demand for remote cardiac monitoring solutions. Government initiatives promoting preventive healthcare and digital diagnostics are also strengthening market expansion. Rising geriatric population and lifestyle-related risk factors such as obesity and hypertension are further contributing to market growth globally.

Key Restraint/Challenge: Accuracy Limitations and Regulatory Compliance Barriers

A key challenge in the global Single Lead ECG equipment market is the limitation in diagnostic accuracy compared to multi-lead ECG systems, particularly in complex cardiac conditions. Single lead devices may not always provide comprehensive cardiac electrical activity mapping, which can lead to diagnostic limitations in certain clinical scenarios. Additionally, stringent regulatory approval processes by agencies such as the U.S. FDA and European CE authorities can delay product commercialization. Concerns regarding data privacy and cybersecurity in connected ECG devices also pose challenges, especially with cloud-based monitoring systems. The cost of advanced AI integration and continuous software validation increases product development expenses for manufacturers. Furthermore, variability in healthcare infrastructure across emerging markets limits widespread adoption. Limited awareness among patients regarding wearable ECG capabilities also slows penetration in rural and low-income regions. These factors collectively restrain rapid market expansion despite strong underlying demand.

Key Market Opportunity: Integration of AI, Wearables, and Remote Cardiac Care Ecosystems

The integration of artificial intelligence, wearable technology, and cloud-based healthcare platforms presents a significant opportunity in the Single Lead ECG market. AI-powered ECG interpretation systems are improving early detection of arrhythmias with reported diagnostic accuracy improvements of up to 90–95% in some clinical applications, enhancing clinical decision-making efficiency. Companies such as BioTelemetry (Philips), Preventice Solutions (Boston Scientific), and Fitbit (Google) are expanding digital cardiac monitoring ecosystems. The growth of remote patient monitoring (RPM) programs, particularly in the U.S. Medicare system, is accelerating reimbursement-supported adoption of ECG devices. Expanding use of smartphone-connected ECG devices in emerging markets such as India and China is improving accessibility and affordability. Increasing investment in digital health startups and medtech innovation is further driving product development. Medical tourism hubs such as South Korea and Thailand are also adopting advanced ECG monitoring technologies for preventive cardiac screening programs. The convergence of AI analytics, wearable biosensors, and telehealth platforms is expected to significantly expand market accessibility and clinical utility worldwide.

Single Lead Electrocardiogram (ECG) Equipment Market Scope

The Single Lead Electrocardiogram (ECG) Equipment market is segmented on the basis of indication and end use.

- By Indication

On the basis of indication, the Single Lead Electrocardiogram (ECG) Equipment Market is segmented into syncope, arrhythmia, and other indications. The Arrhythmia segment dominated the market with a 46.32% share in 2025 due to the high global prevalence of atrial fibrillation, cardiac rhythm disorders, and increasing incidence of cardiovascular diseases. Rising geriatric population, lifestyle-related risks such as hypertension and obesity, and growing demand for early detection of heart rhythm abnormalities are significantly driving segment growth. Single lead ECG devices are widely used in continuous cardiac monitoring for early diagnosis and preventive healthcare. Increasing adoption of wearable ECG devices such as patch monitors and smartwatches is further strengthening segment dominance. Integration of AI-based arrhythmia detection algorithms is improving diagnostic accuracy and clinical outcomes. Hospitals and cardiology clinics are increasingly relying on real-time ECG monitoring systems for emergency care and long-term observation. Expanding telemedicine and remote patient monitoring programs are also boosting adoption. Strong clinical evidence supporting early arrhythmia detection is further enhancing demand. Continuous technological advancements in portable ECG systems are improving usability and patient compliance. The segment remains the primary revenue contributor due to its high disease burden and diagnostic necessity.

The Syncope segment is expected to register the fastest CAGR of 7.4% from 2026 to 2033, driven by increasing cases of unexplained fainting episodes requiring continuous cardiac monitoring. Growing awareness of hidden cardiac conditions linked to syncope is boosting demand for long-term ECG tracking solutions. Single lead ECG devices are increasingly used in ambulatory and home-care settings for continuous rhythm observation. Rising adoption of wearable ECG patches is enabling real-time detection of transient cardiac abnormalities. Increasing emergency admissions related to syncope are further supporting market growth. Expansion of outpatient monitoring services is improving accessibility. Integration of AI-powered analytics is enhancing early detection accuracy. Growing preference for remote patient monitoring is accelerating adoption in home-care environments. Expanding healthcare infrastructure in emerging economies is further driving demand. Increasing focus on preventive cardiology is strengthening segment expansion globally.

- By End Use

On the basis of end use, the Single Lead Electrocardiogram (ECG) Equipment Market is segmented into hospitals and clinics, home-care, and ambulatory surgical centers (ASCs). The Hospitals and Clinics segment dominated the market with a 52.18% share in 2025 due to high patient inflow, advanced diagnostic infrastructure, and widespread use of ECG devices in emergency and routine cardiac monitoring. Hospitals rely heavily on single lead ECG systems for rapid detection of arrhythmias and continuous cardiac assessment. Increasing burden of cardiovascular diseases globally is driving higher hospital admissions. Integration of ECG devices with electronic health records (EHR) systems is improving workflow efficiency and data management. Availability of skilled healthcare professionals ensures accurate diagnosis and effective device utilization. Strong investment in hospital infrastructure across developed and developing regions is supporting market growth. Growing implementation of preventive screening programs is further boosting demand. Continuous technological advancements in portable ECG systems are improving clinical efficiency. Hospitals remain the largest revenue-generating segment due to their critical role in cardiac care delivery. High adoption of AI-assisted ECG interpretation tools is further strengthening hospital usage. The segment continues to dominate due to centralized diagnostic capabilities and high procedural volume.

The Home-Care segment is expected to register the fastest CAGR of 8.1% from 2026 to 2033, driven by rising adoption of remote patient monitoring and wearable cardiac devices. Increasing preference for at-home healthcare solutions is significantly boosting demand for portable ECG equipment. Aging population and growing prevalence of chronic cardiovascular diseases are key growth drivers. Integration of telemedicine platforms is enabling real-time ECG data sharing with healthcare providers. AI-powered ECG interpretation tools are improving patient self-monitoring capabilities. Rising healthcare costs are encouraging shift toward home-based care models. Expanding digital health ecosystems are supporting remote cardiac diagnostics. Increasing awareness of preventive heart health is further driving adoption. Wearable ECG patches and smartphone-connected devices are gaining strong traction globally. Convenience, affordability, and continuous monitoring capabilities are major factors supporting segment growth. The segment is expected to witness strong expansion across both developed and emerging markets.

Single Lead Electrocardiogram (ECG) Equipment Market Regional Analysis

North America dominated the Single Lead Electrocardiogram (ECG) Equipment Market with the largest revenue share of 38.91% in 2025, supported by high prevalence of cardiovascular diseases, advanced healthcare infrastructure, and strong adoption of remote patient monitoring and wearable cardiac devices. The region benefits from widespread use of AI-enabled ECG interpretation tools and strong telemedicine penetration across hospitals and home-care settings. The United States is the key contributor in the region, driven by high healthcare expenditure, strong presence of companies such as iRhythm Technologies, AliveCor, GE HealthCare, and Medtronic, and rapid adoption of digital health solutions. Canada also contributes significantly due to expanding remote patient monitoring programs and increasing geriatric population. Rising incidence of arrhythmia and atrial fibrillation, along with strong reimbursement policies, is further driving demand across the region. Continuous innovation in wearable ECG devices and smartphone-based monitoring systems is strengthening market leadership.

U.S. Single Lead Electrocardiogram (ECG) Equipment Market Insight

The U.S. Single Lead Electrocardiogram (ECG) Equipment market is witnessing strong growth due to rising burden of cardiovascular diseases, increasing adoption of wearable cardiac monitoring devices, and rapid expansion of telehealth services. Strong penetration of AI-based ECG analysis platforms and remote patient monitoring systems is improving early diagnosis and continuous cardiac care. Hospitals, ambulatory care centers, and home-care settings are increasingly adopting portable ECG devices for real-time monitoring of arrhythmia and syncope cases. Additionally, strong presence of key players such as iRhythm Technologies, AliveCor, Apple Inc. (ECG-enabled wearable ecosystem), and GE HealthCare is accelerating innovation. High healthcare spending and favorable reimbursement frameworks further support market expansion. The U.S. continues to lead in digital cardiac health transformation.

Europe Single Lead Electrocardiogram (ECG) Equipment Market Insight

The Europe Single Lead Electrocardiogram (ECG) Equipment market remains a major contributor to global revenue, driven by strong healthcare systems, rising cardiovascular disease prevalence, and increasing adoption of digital health technologies. Countries such as Germany, the United Kingdom, France, Italy, and Spain are key contributors. Germany leads due to advanced hospital infrastructure and strong medical device penetration, while the U.K. is witnessing rapid growth in remote cardiac monitoring and AI-based diagnostics. France and Italy are increasingly adopting wearable ECG devices in preventive healthcare programs. The region benefits from strong presence of companies such as Philips Healthcare, Schiller AG, and Biotronik. Expanding telemedicine services, aging population, and strict regulatory frameworks are further supporting adoption. Europe continues to strengthen its position in clinical innovation and preventive cardiology.

U.K. Single Lead Electrocardiogram (ECG) Equipment Market Insight

The U.K. Single Lead Electrocardiogram (ECG) Equipment market is experiencing steady growth, driven by rising cardiovascular disease burden, increasing adoption of remote patient monitoring, and expansion of digital healthcare infrastructure. The National Health Service (NHS) is actively promoting wearable ECG devices and home-based cardiac monitoring solutions to reduce hospital burden. AI-integrated ECG interpretation and cloud-based monitoring platforms are improving diagnostic efficiency and early detection of heart rhythm disorders. Increasing partnerships between healthcare providers and medtech companies are accelerating adoption. Growing focus on preventive healthcare and aging population further support market expansion. The U.K. is emerging as a key hub for digital cardiac innovation in Europe.

Germany Single Lead Electrocardiogram (ECG) Equipment Market Insight

The Germany Single Lead Electrocardiogram (ECG) Equipment market is expanding steadily due to strong healthcare infrastructure, high adoption of advanced diagnostic technologies, and rising prevalence of cardiovascular diseases. Hospitals and cardiology clinics are increasingly deploying wearable ECG devices for continuous monitoring and early diagnosis of arrhythmia conditions. Germany benefits from strong presence of medical device manufacturers and digital health innovators. Integration of AI-based ECG analysis and telemedicine platforms is improving clinical decision-making and patient outcomes. Government support for digital healthcare transformation is further accelerating adoption. Germany remains a leading market in Europe for precision cardiac monitoring technologies.

Asia-Pacific Single Lead Electrocardiogram (ECG) Equipment Market Insight

The Asia-Pacific Single Lead Electrocardiogram (ECG) Equipment market is expected to witness rapid growth, driven by rising cardiovascular disease burden, expanding healthcare infrastructure, and increasing awareness of early cardiac screening. Countries such as China, India, Japan, South Korea, and Australia are key contributors. China leads due to large patient population and rapid adoption of digital health technologies, while India is witnessing strong growth in telemedicine and affordable wearable ECG devices. Japan and South Korea are advancing in AI-integrated cardiac monitoring and high-precision wearable devices. Expanding middle-class population and improving access to healthcare services are strengthening market penetration. Asia-Pacific is emerging as the fastest-growing regional market globally.

Japan Single Lead Electrocardiogram (ECG) Equipment Market Insight

The Japan Single Lead Electrocardiogram (ECG) Equipment market is witnessing consistent growth due to rising aging population, high prevalence of cardiovascular disorders, and strong adoption of advanced medical technologies. Healthcare providers are increasingly using wearable ECG devices for long-term cardiac monitoring and early detection of arrhythmia. Integration of AI-based diagnostics and compact wearable technologies is enhancing clinical efficiency. Japan’s strong focus on preventive healthcare and smart medical devices is driving innovation. Hospitals and research institutions are actively adopting remote monitoring solutions. Japan continues to be a technologically advanced market for cardiac monitoring solutions.

China Single Lead Electrocardiogram (ECG) Equipment Market Insight

The China Single Lead Electrocardiogram (ECG) Equipment market is growing rapidly, driven by increasing cardiovascular disease prevalence, expanding healthcare infrastructure, and strong government focus on digital health transformation. Widespread adoption of AI-enabled ECG monitoring systems and wearable cardiac devices is improving early diagnosis and disease management. Hospitals and home-care users are increasingly using portable ECG solutions for continuous monitoring. Strong presence of domestic manufacturers and growing investment in medtech innovation are supporting market expansion. Rising awareness of preventive healthcare and large patient base further accelerate demand. China is emerging as one of the fastest-growing ECG equipment markets globally.

Single Lead Electrocardiogram (ECG) Equipment Market Share

The Single Lead Electrocardiogram (ECG) Equipment industry is primarily led by well-established companies, including:

- AliveCor Inc. (U.S.)

- iRhythm Technologies Inc. (U.S.)

- Apple Inc. (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- Fitbit LLC (Google LLC) (U.S.)

- BioTelemetry Inc. (Philips Healthcare) (U.S.)

- GE HealthCare Technologies Inc. (U.S.)

- Medtronic plc (Ireland)

- Abbott Laboratories (U.S.)

- Omron Healthcare Co., Ltd. (Japan)

- BPL Medical Technologies (India)

- Schiller AG (Switzerland)

- Nihon Kohden Corporation (Japan)

- Hillrom (Baxter International Inc.) (U.S.)

- Shenzen Comen Medical Instruments Co., Ltd. (China)

- Contec Medical Systems Co., Ltd. (China)

- Bittium Corporation (Finland)

- VivaLNK Inc. (U.S.)

- Spacelabs Healthcare (OSI Systems) (U.S.)

- Cardiac Insight Inc. (U.S.)

- Preventice Solutions (Boston Scientific) (U.S.)

- GE Healthcare (Portable ECG Solutions Division) (U.S.)

- BPL Cardiovascular Devices (India)

- Lepu Medical Technology (China)

- Schiller Americas Inc. (U.S.)

- Mindray Medical International (China)

- HealForce Bio-Meditech Holdings (China)

- Cardioline S.p.A. (Italy)

- Alive Technologies Pty Ltd. (Australia)

- SmartCardia SA (Switzerland)

- Vivalnk Medical Systems (U.S.)

Latest Developments in Single Lead Electrocardiogram (ECG) Equipment Market

- In August 2021, Apple expanded the clinical capabilities of its ECG ecosystem integrated into Apple Watch, enabling broader single-lead ECG-based atrial fibrillation detection across additional geographies following regulatory approvals. The ECG app uses a single-lead (Lead I equivalent) configuration to capture cardiac rhythm data and support early detection of irregular heart rhythms. This expansion strengthened the adoption of consumer-grade single-lead ECG devices in preventive healthcare and remote monitoring applications

- In January 2022, iRhythm Technologies announced continued scaling of its Zio patch-based single-lead ECG monitoring platform across the U.S. healthcare system, supported by increasing adoption from cardiology networks and hospitals. The Zio system, which captures continuous single-lead ECG data for extended monitoring periods, gained further traction due to its high diagnostic yield for arrhythmia detection, reinforcing its position in ambulatory cardiac monitoring

- In February 2023, AliveCor announced expanded FDA clearances and enhanced AI-enabled capabilities for its KardiaMobile single-lead ECG platform, improving detection accuracy for atrial fibrillation and other cardiac irregularities. The device enables real-time single-lead ECG recording via smartphone integration, strengthening its role in home-based cardiac monitoring and telehealth ecosystems globally

- In October 2023, researchers introduced advanced artificial intelligence models such as CarDS-Plus, designed to interpret single-lead ECG signals from wearable and portable devices in real time. The platform demonstrated efficient processing of ECG data from devices such as Apple Watch and KardiaMobile, highlighting the growing integration of AI in single-lead ECG diagnostics and supporting rapid clinical decision-making in digital healthcare systems

- In May 2024, clinical research studies published on large-scale datasets demonstrated that deep learning models applied to single-lead ECG recordings could accurately detect clinically significant conditions such as QT prolongation and arrhythmias with high sensitivity. These developments reinforced the reliability of single-lead ECG systems in supporting remote diagnosis and expanding their clinical utility beyond traditional hospital-based ECG monitoring

- In March 2025, wearable ECG device manufacturers including Apple, iRhythm Technologies, and Fitbit ecosystem partners continued expanding AI-driven single-lead ECG capabilities focused on continuous monitoring, early arrhythmia detection, and integration with telemedicine platforms. These advancements reflected the increasing shift toward preventive cardiology, where single-lead ECG systems are embedded into wearable and mobile health technologies for real-time cardiovascular risk assessment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.