Global Single Use Filtration Assemblies Market

Market Size in USD Billion

USD

3.69 Billion

USD

8.66 Billion

2025

2033

USD

3.69 Billion

USD

8.66 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 3.69 Billion |

Market Size (Forecast Year) |

USD 8.66 Billion |

CAGR |

% |

Major Markets Players |

|

Single-Use Filtration Assemblies Market Size

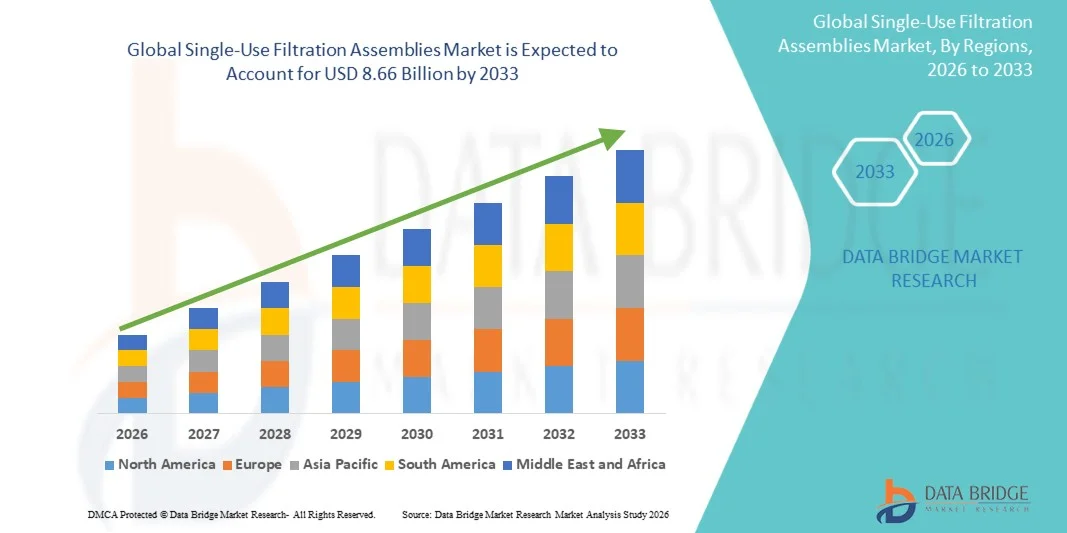

- The global single-use filtration assemblies market size was valued at USD 3.69 billion in 2025 and is expected to reach USD 8.66 billion by 2033, at a CAGR of 11.26% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced biopharmaceutical manufacturing processes and the need for efficient, contamination-free production systems, leading to enhanced process efficiency and reduced risk of cross-contamination in both clinical and commercial settings

- Furthermore, rising demand for flexible, scalable, and cost-effective filtration solutions in biologics, vaccines, and other sterile manufacturing processes is driving the uptake of Single-Use Filtration Assemblies solutions, thereby significantly boosting the industry's growth

Single-Use Filtration Assemblies Market Analysis

- Single-use filtration assemblies, offering disposable filtration solutions for biopharmaceutical and biotechnology processes, are increasingly vital components of modern bioprocessing systems in both research and commercial manufacturing due to their efficiency, sterility, and ease of integration

- The escalating demand for single-use filtration assemblies is primarily fueled by the widespread adoption of biologics manufacturing, growing regulatory focus on contamination control, and a rising preference for flexible, scalable filtration solutions

- North America dominated the single-use filtration assemblies market with the largest revenue share of 42% in 2025, characterized by strong biopharmaceutical manufacturing infrastructure, high adoption of advanced filtration technologies, and a robust presence of key industry players, with the U.S. contributing the majority of this share due to increasing biologics production and regulatory support for single-use technologies

- Asia-Pacific is expected to be the fastest growing region in the single-use filtration assemblies market during the forecast period, registering a CAGR of 9.1% from 2026 to 2033, driven by rising biologics manufacturing, expanding contract manufacturing organizations (CMOs), and increasing investments in flexible filtration systems in countries such as China and India

- The bioprocessing/biopharmaceutical segment accounted for the largest market revenue share of 51% in 2025, fueled by the increasing global demand for monoclonal antibodies, vaccines, cell therapies, and recombinant proteins

Report Scope and Single-Use Filtration Assemblies Market Segmentation

|

Attributes |

Single-Use Filtration Assemblies Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Single-Use Filtration Assemblies Market Trends

“Rising Adoption of Single-Use Technology in Biopharmaceutical Processes”

- A major trend in the global single-use filtration assemblies market is the increasing adoption of single-use technology in biopharmaceutical manufacturing and laboratory processes

- For instance, in 2023, Sartorius launched a modular single-use filtration system for vaccine production, emphasizing faster changeover and reduced contamination risk. Single-use assemblies are replacing traditional stainless-steel filtration systems due to their reduced risk of cross-contamination, faster changeover times, and lower cleaning requirements

- Biopharmaceutical manufacturers are increasingly utilizing single-use filtration systems for critical processes such as sterile filtration, clarification, and virus removal, ensuring higher operational efficiency and compliance with regulatory standards

- Single-use systems provide flexibility in scaling up or down production volumes, which is particularly beneficial for clinical trials, contract manufacturing organizations (CMOs), and small-scale biologics production

- The trend toward disposable filtration assemblies is reinforced by the growing focus on biologics, vaccines, cell therapies, and personalized medicines, which demand adaptable and cost-effective filtration solutions

- Companies such as Sartorius, Pall Corporation, and Merck are developing modular single-use filtration systems that can be easily integrated into existing processes, facilitating streamlined production and minimizing downtime

- The increasing emphasis on contamination-free manufacturing and reducing operational costs is expected to drive the continued adoption of single-use filtration assemblies across research, pharmaceutical, and bioprocessing facilities worldwide

Single-Use Filtration Assemblies Market Dynamics

Driver

“Growing Biopharmaceutical Production and Need for Efficient Filtration”

- The expanding global biopharmaceutical sector is a key driver for the Single-Use Filtration Assemblies market, fueled by increasing demand for monoclonal antibodies, vaccines, and other biologics

- For instance, in 2022, Merck reported a surge in orders for single-use assemblies from CMOs producing COVID-19 vaccines

- Manufacturers are prioritizing process efficiency and product safety, leading to widespread replacement of conventional filtration systems with single-use alternatives that offer rapid deployment and lower maintenance requirements

- The rising prevalence of chronic diseases and the increasing need for innovative biologic therapies further push the demand for reliable, scalable filtration systems that maintain product integrity

- Government support for vaccine production, especially during public health emergencies, is boosting investments in single-use filtration technologies

- Contract manufacturing organizations (CMOs) are adopting single-use assemblies to provide flexible production solutions for multiple clients while minimizing cleaning validation efforts, reducing turnaround time, and controlling operational costs

- The adoption of single-use filtration assemblies is also supported by their ability to comply with stringent regulatory requirements such as FDA and EMA guidelines, ensuring higher reproducibility and safety in biopharmaceutical products

- Overall, the combined demand for flexibility, efficiency, and compliance in modern biomanufacturing processes is driving strong growth in the Single-Use Filtration Assemblies market

Restraint/Challenge

“Concerns Regarding Material Compatibility and Operational Costs”

- One of the primary challenges in the Single-Use Filtration Assemblies market is material compatibility with diverse biological products and process fluids

- For instance, in 2021, a small biotech firm reported reduced protein yield when using an incompatible polymer membrane in a monoclonal antibody filtration process

- Inappropriate selection of membrane materials can result in reduced filtration efficiency, product loss, or contamination risks

- In addition, while single-use systems reduce cleaning and sterilization costs, the initial procurement cost of disposable assemblies can be higher than conventional filtration systems, particularly for large-scale production facilities

- The recurring need for consumables also contributes to operational expenditures, which may be a barrier for smaller organizations or low-volume manufacturers

- Disposal and environmental considerations related to single-use assemblies, including proper waste management and sustainability concerns, can also pose challenges in widespread adoption

- Manufacturers must balance operational efficiency with environmental responsibility by implementing recycling programs or biodegradable materials in assembly design

- Addressing these concerns through careful material selection, cost optimization, and regulatory compliance is essential to encourage broader adoption of single-use filtration assemblies across research and industrial biopharmaceutical applications

Single-Use Filtration Assemblies Market Scope

The market is segmented on the basis of type, application, and product.

• By Type

On the basis of type, the Single-Use Filtration Assemblies market is segmented into membrane filtration, depth filtration, centrifugation, and others. The membrane filtration segment dominated the largest market revenue share of 46% in 2025, driven by its high efficiency in removing impurities, versatility across different bioprocesses, and compatibility with both large-scale and small-scale manufacturing. Membrane filtration is widely used in critical processes such as sterile filtration, virus removal, and protein clarification, providing reliable and consistent performance. Pharmaceutical and biopharmaceutical manufacturers favor membrane filters due to their regulatory compliance, reproducibility, and reduced risk of cross-contamination. The availability of different membrane types, such as PVDF, PES, and cellulose, allows customization for specific applications. Companies such as Sartorius, Pall Corporation, and Merck have enhanced membrane technology to improve filtration capacity and reduce processing time. Membrane filtration also offers lower operational costs compared to traditional stainless-steel systems by minimizing cleaning and validation requirements. Increasing adoption in vaccines, monoclonal antibodies, and cell therapies further reinforces its market dominance. The segment’s strong demand in North America and Europe is attributed to well-established biopharma infrastructure and stringent quality standards. Membrane filtration continues to be the preferred choice for both research laboratories and commercial production facilities globally.

The depth filtration segment is expected to witness the fastest CAGR of 10.5% from 2026 to 2033, driven by its ability to handle high particulate loads and reduce fouling in upstream and downstream processes. Depth filtration is increasingly utilized in clarification of cell cultures and removal of large impurities during protein purification. Manufacturers prefer depth filters for flexible batch processing, ease of scalability, and reduced downtime. Emerging biopharmaceutical companies in Asia-Pacific are adopting depth filtration solutions due to their cost-effectiveness and adaptability to small-volume production. Depth filtration cassettes and cartridges allow quick integration into existing processes without significant infrastructure modification. The segment is also gaining traction due to innovations in filter media, enhancing particle retention efficiency while maintaining high flow rates. Regulatory compliance, including adherence to FDA and EMA guidelines, drives trust and adoption in commercial processes. Depth filtration is particularly favored in vaccine manufacturing, biologics production, and therapeutic protein processing. Companies such as Merck and Pall have introduced advanced depth filtration products to improve productivity. The increasing focus on contamination-free processing and rapid production cycles is expected to sustain strong growth for depth filtration over the forecast period.

• By Application

On the basis of application, the Single-Use Filtration Assemblies market is segmented into pharmaceuticals manufacturing, bioprocessing or biopharmaceuticals, and laboratory use. The bioprocessing/biopharmaceutical segment accounted for the largest market revenue share of 51% in 2025, fueled by the increasing global demand for monoclonal antibodies, vaccines, cell therapies, and recombinant proteins. This segment benefits from the growing trend of outsourcing manufacturing to contract manufacturing organizations (CMOs) and the need for flexible, scalable filtration systems that ensure sterility and process efficiency. Biopharmaceutical processes often require multiple filtration steps including sterilization, virus removal, and clarification, where single-use assemblies provide high reliability. Leading pharmaceutical companies are incorporating single-use filtration to reduce cross-contamination risks, speed up changeovers, and minimize cleaning validation. Regulatory compliance with FDA, EMA, and other guidelines ensures consistent product quality. The segment’s dominance is also driven by adoption in developed regions with advanced biologics manufacturing infrastructure, such as North America and Europe. Technological innovations in filtration media and modular assemblies further strengthen its position. Growing investments in vaccine production, cell and gene therapies, and personalized medicines also drive the segment. Bioprocessing filtration systems allow quick scale-up or scale-down to meet variable batch sizes, enhancing operational efficiency. Continuous improvements in membrane and depth filtration technologies further consolidate biopharmaceutical dominance in this market.

The laboratory use segment is expected to witness the fastest CAGR of 11.2% from 2026 to 2033, attributed to the expanding number of research laboratories and increasing adoption of single-use filtration in analytical, diagnostic, and experimental workflows. Single-use assemblies in laboratories enable contamination-free sample handling, rapid processing, and minimal downtime between experiments. This segment benefits from rising demand in academic research, contract research organizations (CROs), and diagnostic companies for vaccines, biologics, and therapeutic testing. Innovations such as pre-sterilized, ready-to-use filtration devices and modular setups enhance operational convenience and reproducibility. Laboratory filtration applications include sample clarification, virus removal, protein purification, and cell culture processing. Emerging economies in Asia-Pacific are increasingly investing in research facilities, boosting laboratory filtration adoption. Disposable filtration assemblies also minimize risk of cross-contamination and reduce cleaning requirements, critical for high-throughput labs. Companies such as Sartorius and Merck offer laboratory-focused single-use assemblies optimized for small-volume, high-precision workflows. Regulatory compliance and ease of integration with automated systems drive broader acceptance. The flexibility, efficiency, and safety provided by single-use assemblies make the laboratory segment one of the fastest-growing application areas in the market.

• By Product

On the basis of product, the Single-Use Filtration Assemblies market is segmented into filters, cartridges, membranes, manifolds, cassettes, syringes, and others. The membranes segment held the largest market revenue share of 48% in 2025, as membranes form the critical component of most filtration systems, offering precise separation, sterility assurance, and high throughput for biopharmaceutical and laboratory processes. Membranes are used across virus removal, sterile filtration, protein purification, and clarification applications. The adoption of high-performance membranes made of PVDF, PES, and cellulose acetate has enhanced reliability and process efficiency. Leading manufacturers provide modular membrane systems suitable for both large-scale production and small batch research workflows. The segment benefits from regulatory acceptance, ease of validation, and reduced risk of cross-contamination. Membrane filters also offer versatility across multiple bioprocessing applications, including cell culture, vaccine production, and therapeutic protein manufacturing. The membranes segment continues to see strong demand from North America and Europe due to mature biologics and pharmaceutical industries. Continuous innovation in pore size, flow rate, and chemical compatibility ensures its market leadership. The segment’s high adoption in both pharmaceutical and laboratory workflows consolidates its dominant position globally.

The cartridges segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, owing to its adaptability in upstream and downstream filtration processes and ease of integration into existing manufacturing lines. Cartridges are widely used in clarification, sterilization, and removal of particulates in biologics production. Manufacturers favor cartridges for their modularity, consistent performance, and reduced downtime. The segment also benefits from increasing adoption in small-scale manufacturing, research labs, and emerging biopharma facilities in Asia-Pacific. Innovations in cartridge design, including pre-sterilized, disposable, and high-capacity options, are driving adoption. Cartridges allow rapid changeover between batches, improving operational efficiency. Regulatory compliance, reproducibility, and low risk of contamination contribute to their growing preference. Companies such as Pall and Sartorius are introducing advanced cartridge systems for virus removal, protein purification, and sterile filtration. Cartridges provide flexibility, scalability, and reliable performance, establishing themselves as a key growth driver in the single-use filtration assemblies market.

Single-Use Filtration Assemblies Market Regional Analysis

- North America dominated the single-use filtration assemblies market with the largest revenue share of 42% in 2025

- Characterized by strong biopharmaceutical manufacturing infrastructure, high adoption of advanced filtration technologies, and a robust presence of key industry players

- The market contributed the majority of this share due to increasing biologics production and regulatory support for single-use technologies

U.S. Single-Use Filtration Assemblies Market Insight

The U.S. single-use filtration assemblies market captured the largest revenue share in 2025 within North America, driven by expanding biologics production, rising adoption of single-use technologies in contract manufacturing organizations (CMOs), and ongoing investments in flexible, contamination-free filtration systems. The presence of advanced laboratory infrastructure, skilled workforce, and favorable government initiatives for biologics manufacturing are further accelerating market growth.

Europe Single-Use Filtration Assemblies Market Insight

The Europe single-use filtration assemblies market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by growing biopharmaceutical production, increasing adoption of disposable technologies, and stringent regulatory standards for contamination control. Countries such as Germany, France, and Switzerland are witnessing rising investments in biopharma facilities and contract manufacturing capabilities.

U.K. Single-Use Filtration Assemblies Market Insight

The U.K. single-use filtration assemblies market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by expanding biologics manufacturing, investments in advanced filtration systems, and the growing trend of outsourcing production to CMOs. Regulatory frameworks supporting single-use adoption are also encouraging market expansion.

Germany Single-Use Filtration Assemblies Market Insight

The Germany single-use filtration assemblies market is expected to expand at a considerable CAGR during the forecast period, driven by a strong presence of biopharma companies, increasing focus on contamination-free production, and rising investments in single-use technologies. The integration of advanced filtration assemblies in vaccine and biologics manufacturing is further boosting growth.

Asia-Pacific Single-Use Filtration Assemblies Market Insight

The Asia-Pacific single-use filtration assemblies market is poised to grow at the fastest CAGR of 9.1% during the forecast period of 2026 to 2033, driven by increasing biologics manufacturing, expanding contract manufacturing organizations, and rising investments in flexible filtration systems in countries such as China, India, and Japan. Growing government support and adoption of single-use technologies in emerging markets are further fueling market expansion.

Japan Single-Use Filtration Assemblies Market Insight

The Japan single-use filtration assemblies market is gaining momentum due to the country’s strong biopharma sector, increasing demand for biologics, and adoption of single-use technologies for efficient and contamination-free production. Investments in advanced filtration assemblies and continuous process improvement are supporting market growth.

China Single-Use Filtration Assemblies Market Insight

The China single-use filtration assemblies market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid expansion in biologics manufacturing, a growing number of CMOs, and increasing adoption of single-use filtration systems. The push for domestic biologics production and supportive regulatory initiatives are key factors driving market growth.

Single-Use Filtration Assemblies Market Share

The Single-Use Filtration Assemblies industry is primarily led by well-established companies, including:

- GE Healthcare Life Sciences (U.S.)

- Sartorius AG (Germany)

- Merck KGaA (Germany)

- Pall Corporation (U.S.)

- Thermo Fisher Scientific (U.S.)

- Cytiva (U.S.)

- Repligen Corporation (U.S.)

- 3M Company (U.S.)

- Eppendorf AG (Germany)

- DiaSorin S.p.A (Italy)

- HydroDyne Biofiltration (U.S.)

- Asahi Kasei Corporation (Japan)

- Membrane Solutions (U.S.)

- Porex Corporation (U.S.)

- SP Industries (U.S.)

- Franz Ziel GmbH (Germany)

- Avantec BioSystems (U.S.)

- MilliporeSigma (U.S.)

- Corning Inc. (U.S.)

- Watson-Marlow Fluid Technology Group (U.K.)

Latest Developments in Global Single-Use Filtration Assemblies Market

- In June 2021, 3M Health Care introduced the 3M Harvest RC clarifier, a single‑stage purification solution designed for recombinant protein therapeutics — streamlining the traditional multi‑stage harvest and clarification process for biologics manufacturers

- In September 2022, Pall Corporation (a subsidiary of Danaher Corporation) expanded its bioprocessing product line with three new Allegro Connect Systems, which combine virus‑filtration, depth filtration, and buffer‑management capabilities — helping biomanufacturers automate critical downstream filtration workflows

- In January 2024, Repligen Corporation opened a new 50,000-square-foot manufacturing facility in Sweden, dedicated to producing single-use filtration assemblies for the European market — a move reflecting growing demand for disposable filtration components in biologics and vaccine production

- In July 2024, the market research firm Spherical Insights & Consulting published a forecast projecting the global Single‑Use Filtration Assemblies market to grow from USD 2.43 billion in 2023 to USD 10.09 billion by 2033 (CAGR ~ 15.3%), highlighting increasing adoption of single‑use systems in biopharma manufacturing

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.