Global Skin Closure Devices Market

Market Size in USD Billion

USD

15.39 Billion

USD

25.10 Billion

2025

2033

USD

15.39 Billion

USD

25.10 Billion

2025

2033

| 2026 - 2033 | |

| USD 15.39 Billion | |

| USD 25.10 Billion | |

| % | |

|

Skin Closure Devices Market Overview

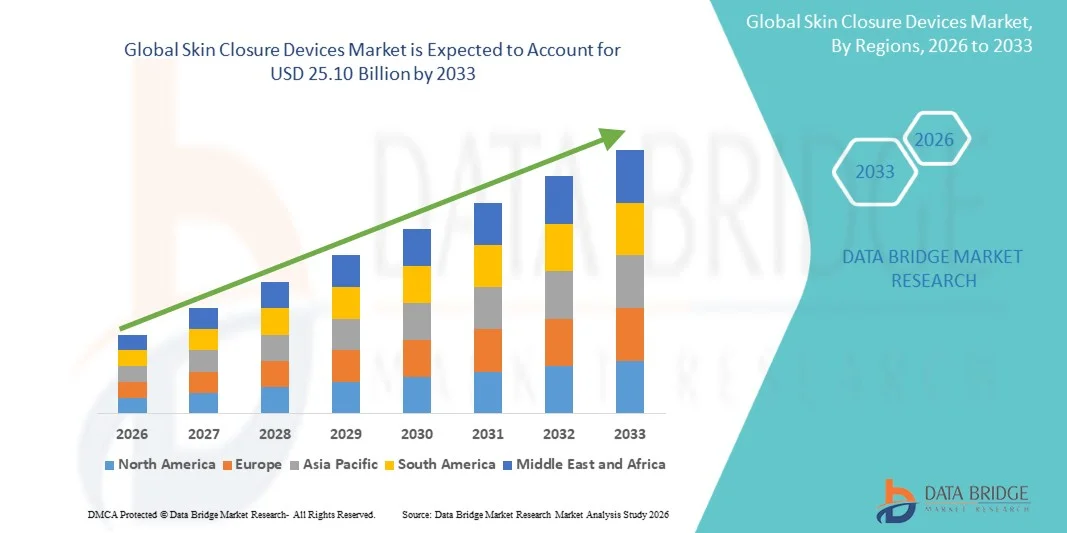

The Skin Closure Devices Market was valued at USD 15.39 billion in 2025 and is projected to reach USD 25.10 billion by 2033, growing at a CAGR of 6.31% from 2026 to 2033. The market is experiencing steady growth driven by the rising volume of surgical procedures worldwide, increasing prevalence of traumatic injuries and chronic wounds, and continuous advancements in wound management technologies.

The growing emphasis on minimizing surgical site infections, improving cosmetic outcomes, and accelerating patient recovery is encouraging healthcare providers to adopt advanced skin closure solutions such as sutures, staples, adhesive strips, tissue adhesives, and surgical sealants. In addition, the expansion of ambulatory surgical centers, increasing healthcare expenditure, and the rising demand for minimally invasive and outpatient procedures are supporting market growth. Technological innovations in absorbable materials, antimicrobial-coated closure products, and bioengineered adhesives are further enhancing clinical efficiency and patient outcomes across hospitals, specialty clinics, and emergency care settings.

Key Market Trends & Insights

- North America dominated the Skin Closure Devices Market with the largest revenue share of 38.42% in 2025, supported by high surgical procedure volumes, advanced healthcare infrastructure, and strong adoption of innovative wound closure technologies.

- The Surgical Wounds segment led the market with a 46.82% share in 2025, driven by the continuously rising number of surgical procedures performed globally across general surgery, orthopedics, cardiovascular, cosmetic, and trauma care settings

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.1% from 2026 to 2033, fueled by expanding healthcare access, rising surgical interventions, and increasing investments in hospital infrastructure across China, India, and Southeast Asia.

- Diabetic Ulcers are the fastest-growing application type, projected to register a CAGR of 7.5%, reflecting the surge in demand for global prevalence of diabetes and associated chronic wound complications.

- The Acute Wound segment dominated the wound type category with a 68.47% revenue share in 2025, led by the high incidence of surgical incisions, traumatic injuries, lacerations, and accident-related wounds requiring immediate closure.

- Sutures accounted for 44.18% of the market, preferred by their extensive use across a wide range of surgical procedures and wound management applications.

- The Adhesives segment is the fastest-growing device category, with a CAGR of 7.4%, driven by increasing demand for non-invasive, faster, and cosmetically superior wound closure solutions

Market Size & Forecast

- Global Market Value (2025): USD 15.39 Billion

- Expected Market Value (2033): USD 25.10 Billion

- Forecast CAGR (2026–2033): 6.31%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Skin Closure Devices Market Segmentation

|

Attributes |

Skin Closure Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Ethicon, Inc. (U.S.) · Medtronic (Ireland) · B. Braun SE (Germany) · Baxter (U.S.) · Smith & Nephew (U.K.) · Stryker (U.S.) · Cardinal Health (U.S.) · Medline Industries, LP (U.S.) · DeRoyal Industries, Inc. (U.S.) · DermaRite Industries, LLC (U.S.) · Advanced Medical Solutions Group plc (U.K.) · Healthium Medtech Limited (India) · Meril Life Sciences Pvt. Ltd. (India) · Terumo Corporation (Japan) · Riverpoint Medical LLC (U.S.) · Corza Medical (U.S.) · DemeTECH Corporation (U.S.) · Aspen Surgical Products, Inc. (U.S.) · Mölnlycke Health Care AB (Sweden) · Paul Hartmann AG (Germany) |

|

Market Opportunities |

· Growing adoption of bioengineered tissue adhesives and surgical sealants · Rising demand for advanced wound closure products in outpatient and ambulatory surgical centers · Increasing volume of minimally invasive and robotic-assisted surgeries worldwide |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Skin Closure Devices Market Trends

Trend: Rising Adoption of Advanced Tissue Adhesives and Surgical Sealants

Healthcare providers are increasingly adopting advanced tissue adhesives and surgical sealants to improve wound closure efficiency, reduce procedure times, and enhance cosmetic outcomes compared to conventional suturing methods. These products offer improved patient comfort, lower infection risks, and faster healing, making them particularly attractive for minimally invasive surgeries, emergency care, and outpatient procedures. Continuous innovation in bio-compatible materials and antimicrobial formulations is further expanding their use across a wide range of surgical specialties and wound management applications.

For instance, in February 2024, Ethicon expanded its portfolio of advanced wound closure solutions, highlighting the growing industry focus on products that improve healing outcomes while reducing postoperative complications.

Skin Closure Devices Market Dynamics

Key Market Driver: Increasing Global Volume of Surgical Procedures

The growing number of surgical procedures worldwide is a major factor driving demand for skin closure devices across hospitals, ambulatory surgical centers, and specialty clinics. Rising prevalence of chronic diseases, expanding access to healthcare services, and increasing adoption of elective and minimally invasive surgeries are generating consistent demand for reliable wound closure products. Healthcare providers are prioritizing solutions that minimize surgical site infections, improve recovery times, and deliver better cosmetic results, further supporting market expansion.

For instance, in January 2025, Medtronic continued expanding its surgical solutions portfolio to address increasing procedural volumes and the need for efficient wound management technologies across diverse healthcare settings.

Key Restraint/Challenge: Risk of Surgical Site Infections and Product-Related Complications

A significant challenge in the Skin Closure Devices Market is the risk of surgical site infections, wound dehiscence, allergic reactions, and other closure-related complications. Improper application techniques, patient-specific factors, and variability in product performance can negatively affect healing outcomes and increase healthcare costs. Regulatory scrutiny surrounding product safety and clinical effectiveness also requires manufacturers to invest heavily in testing, compliance, and post-market surveillance activities, creating additional operational challenges.

For instance, ongoing regulatory evaluations by agencies such as the U.S. Food and Drug Administration continue to emphasize the importance of safety, efficacy, and quality standards for wound closure products used in surgical settings.

Key Market Opportunity: Development of Antimicrobial and Bioengineered Closure Technologies

The development of antimicrobial-coated sutures, bioengineered adhesives, and next-generation wound closure materials presents a significant growth opportunity for market participants. These innovations are designed to reduce infection risks, accelerate tissue healing, and improve overall patient outcomes while addressing growing demand for advanced surgical care. Expanding adoption of minimally invasive procedures and value-based healthcare models is creating favorable conditions for manufacturers offering differentiated and clinically effective closure technologies.

For instance, in 2024, Baxter International Inc. continued advancing surgical care and wound management innovations, reflecting broader industry efforts to develop next-generation solutions that enhance healing performance and procedural efficiency.

Skin Closure Devices Market Scope

The skin closure devices market is segmented on the basis of application, wound type, device type, and end user.

- By Application

On the basis of application, the Skin Closure Devices Market is segmented into burns, ulcer, surgical wounds, pressure ulcers, diabetic ulcers, and arterial ulcers. The Surgical Wounds segment dominated the market with an estimated 46.82% share in 2025, owing to the continuously rising number of surgical procedures performed globally across general surgery, orthopedics, cardiovascular, cosmetic, and trauma care settings. Surgical wounds require reliable closure solutions to minimize infection risks, accelerate healing, and improve cosmetic outcomes. The growing adoption of minimally invasive and outpatient procedures is further increasing demand for advanced closure products. Hospitals and surgical centers extensively utilize sutures, staples, and tissue adhesives for postoperative wound management. Rising healthcare expenditure and improved access to surgical services in emerging economies are supporting segment growth. Continuous innovations in absorbable and antimicrobial closure technologies further strengthen the segment’s market leadership.

The Diabetic Ulcers segment is projected to register the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by the increasing global prevalence of diabetes and associated chronic wound complications. Diabetic foot ulcers often require advanced wound management and specialized closure techniques to prevent infections and amputations. Growing awareness regarding early wound care intervention is supporting adoption of innovative closure devices. Healthcare providers are increasingly focusing on reducing hospitalization duration and improving healing outcomes for diabetic patients. Advancements in bioactive dressings and tissue repair technologies are complementing closure device utilization. Expanding diabetic patient populations across Asia-Pacific, North America, and the Middle East are expected to accelerate segment growth significantly.

- By Wound

On the basis of wound, the Skin Closure Devices Market is segmented into acute wound and chronic wound. The Acute Wound segment dominated the market with an estimated 68.47% share in 2025, primarily due to the high incidence of surgical incisions, traumatic injuries, lacerations, and accident-related wounds requiring immediate closure. Acute wounds typically undergo faster treatment cycles and represent a significant proportion of hospital and emergency department cases. The widespread use of sutures, staples, and adhesives for rapid wound management contributes substantially to segment revenue. Growing numbers of surgical interventions worldwide continue to increase demand for acute wound closure products. Technological advancements aimed at reducing healing time and infection rates further support market expansion. The segment also benefits from established clinical protocols and broad product availability.

The Chronic Wound segment is expected to witness the fastest growth at a CAGR of 7.0% from 2026 to 2033, driven by the increasing prevalence of diabetes, obesity, vascular diseases, and aging populations worldwide. Chronic wounds often require prolonged treatment and specialized closure approaches to facilitate healing and prevent complications. Rising healthcare costs associated with chronic wound management are encouraging the adoption of advanced closure technologies. Growing awareness regarding effective wound care and preventive healthcare measures is supporting market penetration. Innovations in antimicrobial and bioengineered closure products are improving treatment outcomes for chronic wound patients. Increasing investments in wound care infrastructure are further accelerating segment growth globally.

- By Device

On the basis of device, the Skin Closure Devices Market is segmented into adhesives, staples, sutures, and mechanical devices. The Sutures segment led the market with an estimated 44.18% share in 2025, owing to their extensive use across a wide range of surgical procedures and wound management applications. Sutures remain the preferred closure method due to their reliability, versatility, and ability to provide strong wound approximation. Both absorbable and non-absorbable variants are widely utilized in hospitals and ambulatory surgical centers. Continuous product innovations, including antimicrobial-coated and synthetic sutures, are improving clinical outcomes. Their cost-effectiveness and familiarity among healthcare professionals further support widespread adoption. The segment continues to benefit from growing surgical volumes worldwide.

The Adhesives segment is projected to be the fastest-growing segment at a CAGR of 7.4% from 2026 to 2033, driven by increasing demand for non-invasive, faster, and cosmetically superior wound closure solutions. Tissue adhesives reduce procedure time and eliminate the need for suture removal, enhancing patient comfort and convenience. Their growing application in minimally invasive surgeries and pediatric procedures is supporting market expansion. Technological advancements in bio-compatible and antimicrobial formulations are improving product performance. Rising preference for outpatient surgical procedures is further encouraging adhesive adoption. Expanding use across emergency care and cosmetic surgery settings is expected to accelerate future growth.

- By End User

On the basis of end user, the Skin Closure Devices Market is segmented into hospitals, community healthcare service providers, ambulatory surgical centers, and home care. The Hospitals segment dominated the market with an estimated 61.35% share in 2025, supported by the large volume of surgical procedures, trauma cases, and inpatient treatments conducted in hospital settings. Hospitals serve as primary centers for complex surgeries requiring advanced wound closure products and specialized clinical expertise. The availability of skilled healthcare professionals and comprehensive postoperative care further supports segment dominance. Increasing healthcare investments and hospital infrastructure development are driving product adoption globally. Hospitals also benefit from access to advanced closure technologies and favorable reimbursement frameworks. Their central role in surgical care continues to maintain strong market leadership.

The Ambulatory Surgical Centers (ASCs) segment is anticipated to register the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by the increasing shift toward outpatient surgical procedures and cost-effective healthcare delivery models. ASCs offer shorter patient stays, lower treatment costs, and improved operational efficiency compared to traditional hospital settings. Growing adoption of minimally invasive surgeries is creating significant demand for efficient wound closure solutions within these facilities. Healthcare systems are increasingly promoting outpatient care to reduce hospital burden and improve resource utilization. Technological advancements in skin closure products are enhancing suitability for same-day discharge procedures. Rising patient preference for convenient and affordable surgical services is expected to fuel rapid segment growth.

Skin Closure Devices Market Regional Analysis

North America dominated the Skin Closure Devices Market with the largest revenue share of 38.42% in 2025, supported by high surgical procedure volumes, advanced healthcare infrastructure, and strong adoption of innovative wound closure technologies. The region also benefits from favorable reimbursement frameworks, the presence of leading medical device manufacturers, and increasing demand for minimally invasive surgical procedures. Growing prevalence of chronic wounds, rising incidence of traumatic injuries, and expanding use of antimicrobial and bioengineered closure products are further driving market growth. Continuous investments in surgical innovation, wound care management, and infection prevention strategies continue to strengthen North America’s leadership position in the global market.

U.S. Skin Closure Devices Market Insight

The U.S. skin closure devices market is witnessing strong growth due to rising surgical procedure volumes, increasing prevalence of chronic wounds, and growing adoption of advanced wound management technologies. The country’s well-established healthcare infrastructure, favorable reimbursement environment, and strong presence of leading medical device manufacturers are driving demand across hospitals, ambulatory surgical centers, and specialty clinics. In addition, growing emphasis on reducing surgical site infections and improving postoperative outcomes is accelerating the adoption of innovative sutures, staples, tissue adhesives, and surgical sealants across healthcare facilities.

Europe Skin Closure Devices Market Insight

The Europe skin closure devices market remains a major contributor to global revenue, driven by advanced healthcare systems, technological innovation, and high demand for effective wound management solutions. The widespread use of skin closure devices in surgical procedures, trauma care, and chronic wound treatment is supporting market expansion across the region. Increasing investments in healthcare modernization, coupled with stringent patient safety regulations and growing adoption of minimally invasive surgeries, continue to enhance the utilization of skin closure devices throughout Europe.

U.K. Skin Closure Devices Market Insight

The U.K. skin closure devices market is experiencing steady growth, supported by rising surgical intervention rates, increasing demand for advanced wound care products, and expanding healthcare investments. Growing adoption of innovative closure technologies designed to improve healing outcomes and reduce infection risks is contributing to market growth. Furthermore, the integration of antimicrobial-coated sutures, tissue adhesives, and bioengineered wound closure products is improving clinical effectiveness and patient recovery, positioning the U.K. as a key market within the European skin closure devices industry.

Germany Skin Closure Devices Market Insight

The Germany skin closure devices market is expanding steadily due to the country’s advanced healthcare infrastructure, strong medical technology sector, and increasing adoption of innovative surgical products. Hospitals, specialty clinics, and surgical centers are increasingly utilizing advanced skin closure solutions to improve procedural efficiency and patient outcomes. Continuous advancements in absorbable sutures, surgical adhesives, and infection prevention technologies, along with strong healthcare expenditure and emphasis on quality care, are further driving market growth in Germany.

Asia-Pacific Skin Closure Devices Market Insight

The Asia-Pacific skin closure devices market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising surgical procedure volumes, and increasing investments in wound care services across countries such as China, India, and Japan. Growing awareness regarding infection prevention, rising adoption of advanced closure technologies, and increasing demand for cost-effective healthcare solutions are supporting regional market expansion. In addition, the growing burden of chronic diseases and expanding access to surgical treatments are accelerating the adoption of skin closure devices across healthcare facilities.

Japan Skin Closure Devices Market Insight

The Japan skin closure devices market is witnessing consistent growth due to rising healthcare expenditure, increasing surgical procedures, and growing demand for advanced wound management technologies. Hospitals, surgical centers, and healthcare providers are increasingly adopting high-performance skin closure products to improve healing outcomes and reduce postoperative complications. Moreover, increasing integration of bioengineered materials and the country’s focus on high-quality patient care are further contributing to market growth.

China Skin Closure Devices Market Insight

The China skin closure devices market is growing rapidly, driven by expanding healthcare infrastructure, increasing surgical volumes, and rising government focus on improving healthcare quality and accessibility. Growing adoption of advanced wound closure technologies across hospitals and specialty clinics is significantly boosting market demand. In addition, rising investments in healthcare modernization, increasing prevalence of chronic wounds, and rapid advancements in medical device technologies are positioning China as one of the fastest-growing markets for skin closure devices globally.

Skin Closure Devices Market Share

The skin closure devices industry is primarily led by well-established companies, including:

- Ethicon, Inc. (U.S.)

- Medtronic (Ireland)

- Braun SE (Germany)

- Baxter (U.S.)

- Smith & Nephew (U.K.)

- Stryker (U.S.)

- Cardinal Health (U.S.)

- Medline Industries, LP (U.S.)

- DeRoyal Industries, Inc. (U.S.)

- DermaRite Industries, LLC (U.S.)

- Advanced Medical Solutions Group plc (U.K.)

- Healthium Medtech Limited (India)

- Meril Life Sciences Pvt. Ltd. (India)

- Terumo Corporation (Japan)

- Riverpoint Medical LLC (U.S.)

- Corza Medical (U.S.)

- DemeTECH Corporation (U.S.)

- Aspen Surgical Products, Inc. (U.S.)

- Mölnlycke Health Care AB (Sweden)

- Paul Hartmann AG (Germany)

Latest Developments in Skin Closure Devices Market

- In December 2024, BRIJ Medical announced that its Brijjit® BP-100 and BP-75 Force Modulating Tissue Bridges received a Breakthrough Technology Agreement from Premier in the non-invasive skin closure category. The agreement enables broader access to the technology across Premier member healthcare facilities and recognizes its potential to improve patient safety, clinical outcomes, and operational efficiency. This development highlights the growing adoption of innovative non-invasive skin closure solutions in surgical care

- In August 2024, Resivant Medical received U.S. FDA 510(k) clearance for its Cutiva™ Topical Skin Adhesive and Cutiva™ PLUS Skin Closure System. The products utilize a novel high-viscosity cyanoacrylate technology designed for surgical incision and traumatic laceration closure. The company described the launch as one of the most significant advances in tissue adhesive technology in more than two decades, strengthening innovation within the skin closure devices market

- In December 2023, BD (Becton, Dickinson and Company) expanded its surgical solutions portfolio following the integration of Tissuemed Ltd., acquired to strengthen its position in advanced surgical sealants. The acquisition added Tissuepatch™, a self-adhesive surgical sealant technology used to support tissue sealing and wound management during surgical procedures. The move reinforced BD’s presence in the growing market for advanced closure and sealing technologies

- In October 2023, Sylke Inc. launched SYLKE™, a silk-based surgical dressing and adhesive wound closure technology designed to reduce skin injuries, infections, and scarring associated with traditional closure methods. Clinical data released alongside the launch demonstrated improved outcomes compared with conventional closure approaches, reflecting increasing innovation in post-surgical wound closure and healing solutions

- In April 2023, Corza Medical announced the direct U.S. commercialization and distribution of TachoSil®, a fibrin sealant patch used to support tissue sealing, hemostasis, and surgical wound management. The transition to direct distribution strengthened the product’s market presence and expanded access to advanced surgical closure technologies for healthcare providers across the United States

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.