Global Sleep Disorder Treatment Market

Market Size in USD Billion

USD

12.02 Billion

USD

23.77 Billion

2025

2033

USD

12.02 Billion

USD

23.77 Billion

2025

2033

| 2026 - 2033 | |

| USD 12.02 Billion | |

| USD 23.77 Billion | |

| % | |

|

Sleep Disorder Treatment Market Size

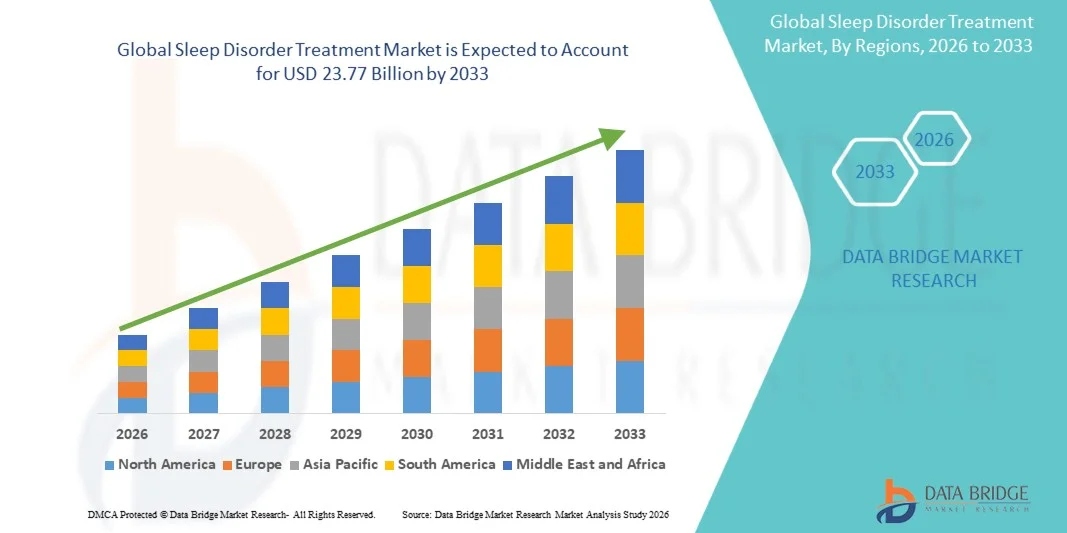

- The global sleep disorder treatment market size was valued at USD 12.02 billion in 2025 and is expected to reach USD 23.77 billion by 2033, at a CAGR of 8.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of sleep disorders such as insomnia, sleep apnea, and restless leg syndrome, along with rising awareness about the importance of sleep health, leading to higher demand for effective diagnosis and treatment solutions

- Furthermore, growing adoption of advanced treatment options including CPAP devices, medications, and behavioral therapies, coupled with increasing focus on mental health and lifestyle-related disorders, is establishing sleep disorder treatment as a critical component of modern healthcare. These converging factors are accelerating the uptake of Sleep Disorder Treatment solutions, thereby significantly boosting the market growth

Sleep Disorder Treatment Market Analysis

- Sleep disorder treatment solutions, including therapies, devices, and medications used to manage conditions such as insomnia, sleep apnea, and narcolepsy, are becoming increasingly vital in modern healthcare due to rising awareness of sleep health and its impact on overall well-being

- The escalating demand for sleep disorder treatment is primarily fueled by increasing prevalence of lifestyle-related disorders, growing stress levels, and rising geriatric population, along with advancements in diagnostic technologies such as sleep studies and wearable monitoring devices

- North America dominated the sleep disorder treatment market with the largest revenue share of approximately 42.6% in 2025, characterized by advanced healthcare infrastructure, high awareness of sleep health, and strong adoption of CPAP devices and prescription therapies, with the U.S. leading in diagnosis and treatment rates

- Asia-Pacific is expected to be the fastest growing region in the sleep disorder treatment market during the forecast period due to increasing healthcare expenditure, rising awareness of sleep disorders, and expanding access to diagnostic and treatment facilities

- The adults segment accounted for the largest market revenue share of 72.3% in 2025, driven by the high prevalence of sleep disorders among working professionals and the aging population

Report Scope and Sleep Disorder Treatment Market Segmentation

|

Attributes |

Sleep Disorder Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Sleep Disorder Treatment Market Trends

“Enhanced Convenience Through AI and Voice Integration”

- A significant and accelerating trend in the global Sleep Disorder Treatment market is the increasing adoption of digital therapeutics and non-pharmacological treatment approaches

- These solutions are gaining traction as patients and healthcare providers seek safer and more sustainable alternatives to long-term medication use

- For instance, cognitive behavioral therapy for insomnia (CBT-I) is being widely adopted as a first-line treatment for chronic insomnia, supported by digital platforms and mobile-based therapy programs

- The growing use of wearable devices and sleep tracking technologies is enabling individuals to monitor sleep patterns, identify disturbances, and take corrective measures

- Furthermore, increased awareness regarding the side effects of prolonged use of sleep medications is driving demand for behavioral and lifestyle-based interventions

- Healthcare providers are also emphasizing holistic treatment approaches, including stress management, sleep hygiene education, and relaxation techniques

- This shift toward personalized and non-invasive treatment solutions is significantly shaping the global Sleep Disorder Treatment market

Sleep Disorder Treatment Market Dynamics

Driver

“Rising Prevalence of Sleep Disorders and Increasing Mental Health Awareness”

- The increasing global prevalence of sleep disorders such as insomnia, sleep apnea, and restless leg syndrome is a major driver for the growth of the Sleep Disorder Treatment market

- For instance, rising stress levels, changing lifestyles, excessive screen time, and work-related pressures are contributing to a significant increase in sleep-related issues across various age groups worldwide

- Growing awareness of the link between sleep health and overall well-being, including mental health, cardiovascular health, and productivity, is encouraging individuals to seek treatment

- In addition, increasing diagnosis rates and improved access to sleep clinics and specialized healthcare services are supporting market expansion

- The expansion of healthcare infrastructure and rising healthcare expenditure, particularly in emerging economies, is further boosting access to treatment options

- The growing focus on preventive healthcare and quality of life improvement is also contributing to the increasing demand for effective sleep disorder treatments globally

Restraint/Challenge

“High Treatment Costs and Underdiagnosis of Sleep Disorders”

- The high cost associated with certain sleep disorder treatments, particularly advanced diagnostic procedures and long-term therapies, remains a key challenge for market growth

- A significant portion of individuals with sleep disorders remains undiagnosed due to lack of awareness and limited access to sleep specialist

- For instance, in many developing regions, patients often ignore symptoms such as chronic insomnia or sleep apnea, or attribute them to lifestyle factors, leading to delayed diagnosis and treatment

- In addition, the cost of sleep studies, such as polysomnography, and specialized equipment can limit access for many patients

- Social stigma and lack of awareness regarding mental health and sleep-related conditions can further discourage individuals from seeking medical help

- Variability in treatment response and the need for long-term management can also affect patient adherence

- Addressing these challenges through increased awareness, affordable diagnostic solutions, and expansion of sleep healthcare services will be essential for sustained market growth

Sleep Disorder Treatment Market Scope

The market is segmented on the basis of type, treatment, route of administration, drug type, population type, end user, and distribution channel.

• By Type

On the basis of type, the Sleep Disorder Treatment market is segmented into insomnia, sleep apnea, restless legs syndrome (RLS), narcolepsy, and others. The insomnia segment dominated the largest market revenue share of 39.8% in 2025, driven by its high global prevalence and increasing association with stress, anxiety, and lifestyle changes. Insomnia is widely reported across both developed and emerging regions, making it the most commonly diagnosed sleep condition. Rising awareness about sleep health and growing diagnosis rates further contribute to segment growth. Increasing adoption of pharmacological and behavioral therapies also supports demand. The expansion of digital health platforms and sleep tracking technologies is improving diagnosis and treatment adherence. In addition, urbanization and hectic work schedules are increasing the burden of sleep disturbances. The availability of over-the-counter and prescription medications enhances accessibility. Growing healthcare expenditure and physician recommendations further drive this segment.

The sleep apnea segment is expected to witness the fastest CAGR of 11.7% from 2026 to 2033, driven by increasing obesity rates and rising awareness about obstructive sleep apnea (OSA). Sleep apnea is often underdiagnosed, but improved screening technologies and home sleep testing are accelerating diagnosis rates. The growing adoption of advanced treatment devices such as CPAP machines is further boosting segment growth. Increasing geriatric population and cardiovascular risk factors also contribute to rising prevalence. Healthcare providers are focusing on early intervention to prevent complications. Technological advancements in wearable sleep monitoring devices are enhancing detection. Expanding reimbursement policies for sleep apnea treatments further support growth. As awareness improves, this segment is expected to expand rapidly.

• By Treatment

On the basis of treatment, the Sleep Disorder Treatment market is segmented into pharmacological therapy, mechanical therapy, mandibular advancement devices, hypoglossal nerve stimulators, surgery, and others. The pharmacological therapy segment dominated the largest market revenue share of 42.5% in 2025, driven by the widespread use of medications such as sedatives, hypnotics, and antidepressants for managing sleep disorders. These therapies are commonly prescribed for conditions like insomnia and anxiety-related sleep disturbances. The ease of administration and quick symptom relief further support segment dominance. Increasing patient preference for medication-based treatment options also contributes to growth. Pharmaceutical companies are continuously developing new drugs with improved safety profiles. Growing awareness among healthcare professionals regarding treatment options enhances adoption. In addition, strong distribution networks ensure widespread availability of medications.

The mechanical therapy segment is expected to witness the fastest CAGR of 12.3% from 2026 to 2033, driven by increasing adoption of non-invasive devices such as CPAP and BiPAP machines for sleep apnea treatment. These therapies offer long-term solutions without the side effects associated with medications. Rising awareness about device-based treatment options is boosting demand. Technological advancements in portable and user-friendly devices are improving patient compliance. Increasing prevalence of sleep apnea and respiratory disorders further supports growth. Healthcare providers are increasingly recommending mechanical therapies for moderate to severe cases. Expanding insurance coverage for sleep devices also contributes to adoption. As patient preference shifts toward non-pharmacological treatments, this segment is expected to grow rapidly.

• By Route of Administration

On the basis of route of administration, the Sleep Disorder Treatment market is segmented into oral, parenteral, and others. The oral segment held the largest market revenue share of 64.1% in 2025, driven by the widespread use of tablets and capsules for treating sleep disorders. Oral medications are convenient, cost-effective, and easy to administer, making them the preferred choice for both patients and healthcare providers. Increasing availability of over-the-counter sleep aids further supports segment dominance. High patient compliance and accessibility through retail pharmacies also contribute to growth. Pharmaceutical companies are introducing improved formulations with fewer side effects. Rising prevalence of insomnia and anxiety disorders further boosts demand. The strong presence of oral drugs in both prescription and OTC categories strengthens this segment.

The parenteral segment is expected to witness the fastest CAGR of 8.5% from 2026 to 2033, driven by its use in acute care settings and severe cases requiring immediate intervention. Parenteral administration ensures rapid onset of action and higher bioavailability. It is commonly used in hospital environments for patients with severe sleep disorders or comorbid conditions. Increasing hospital admissions and advancements in injectable therapies further support growth. Healthcare providers prefer this route for critical care management. As demand for rapid and effective treatment increases, this segment is expected to expand steadily.

• By Drug Type

On the basis of drug type, the Sleep Disorder Treatment market is segmented into branded and generics. The branded segment dominated the largest market revenue share of 58.6% in 2025, driven by strong clinical efficacy, brand trust, and continuous innovation by pharmaceutical companies. Branded drugs are widely prescribed due to their proven safety, reliability, and regulatory approvals. These medications often undergo extensive clinical trials, ensuring higher physician confidence and patient adherence. The availability of advanced formulations with improved pharmacokinetics further enhances their adoption. Pharmaceutical companies are investing heavily in research and development to introduce novel therapies with fewer side effects. In addition, aggressive marketing strategies and strong brand positioning contribute to their widespread usage. Hospitals and specialty clinics often prefer branded medications for critical and chronic cases. The presence of patented drugs limits competition, strengthening market share. Increasing healthcare expenditure and patient preference for quality treatments further support segment dominance. Growing awareness about sleep health also drives demand for effective branded therapies.

The generics segment is expected to witness the fastest CAGR of 10.4% from 2026 to 2033, driven by cost-effectiveness and increasing demand for affordable treatment options. Generic drugs provide similar therapeutic benefits at significantly lower costs, making them accessible to a broader population. Patent expirations of major branded drugs are opening opportunities for generic manufacturers. Governments across various regions are promoting generic drug adoption to reduce healthcare expenditure. Increasing awareness among patients about cost savings is also boosting demand. Retail pharmacies are actively stocking generic alternatives due to high consumer preference. Expanding healthcare access in emerging economies further accelerates growth. In addition, improvements in manufacturing quality and regulatory approvals are enhancing trust in generics. As affordability becomes a key factor in treatment decisions, this segment is expected to expand rapidly.

• By Population Type

On the basis of population type, the Sleep Disorder Treatment market is segmented into children and adults. The adults segment accounted for the largest market revenue share of 72.3% in 2025, driven by the high prevalence of sleep disorders among working professionals and the aging population. Adults are more susceptible to sleep disorders due to lifestyle factors such as stress, long working hours, and irregular sleep schedules. Chronic conditions such as obesity, cardiovascular diseases, and mental health disorders further contribute to sleep disturbances. Increasing awareness about sleep health and growing diagnosis rates are supporting market growth. The availability of a wide range of treatment options, including medications and devices, enhances adoption. In addition, higher healthcare spending among adults contributes to increased treatment uptake. Corporate wellness programs and health initiatives also promote sleep disorder management. The growing geriatric population globally further strengthens demand. Technological advancements in sleep monitoring devices are improving diagnosis and treatment adherence.

The children segment is expected to witness the fastest CAGR of 9.7% from 2026 to 2033, driven by rising awareness of pediatric sleep disorders and increasing diagnosis rates. Growing concerns among parents regarding sleep-related issues such as insomnia and sleep apnea are supporting early intervention. Pediatric healthcare providers are increasingly focusing on identifying and managing sleep disorders at an early stage. Advancements in pediatric-friendly treatment options and diagnostic tools are enhancing care delivery. Increasing prevalence of behavioral and neurological conditions also contributes to sleep disturbances in children. Schools and healthcare organizations are promoting awareness about the importance of healthy sleep patterns. In addition, improved access to pediatric healthcare services supports growth. As awareness and diagnosis improve, this segment is expected to grow steadily.

• By End User

On the basis of end user, the Sleep Disorder Treatment market is segmented into hospitals, specialty clinics, home healthcare, ambulatory surgical centers, and others. The hospitals segment dominated the largest market revenue share of 47.5% in 2025, driven by advanced diagnostic facilities and the availability of comprehensive treatment options. Hospitals serve as primary centers for conducting sleep studies and managing complex sleep disorders. The presence of skilled healthcare professionals ensures accurate diagnosis and effective treatment planning. Increasing patient admissions for sleep-related issues further contribute to segment growth. Hospitals are equipped with advanced technologies such as polysomnography systems for detailed sleep analysis. Government investments in healthcare infrastructure also support hospital-based treatment. In addition, integrated care services and multidisciplinary approaches enhance patient outcomes. Rising awareness and referral rates from primary care physicians further strengthen this segment.

The home healthcare segment is expected to witness the fastest CAGR of 12.8% from 2026 to 2033, driven by increasing adoption of home-based sleep monitoring and treatment devices. Patients are increasingly preferring convenient and cost-effective treatment options outside hospital settings. The availability of portable CPAP devices and wearable sleep trackers is supporting this trend. Advancements in telemedicine and remote monitoring technologies further enhance patient care. Home healthcare reduces the need for frequent hospital visits, improving patient comfort and compliance. Increasing prevalence of chronic sleep disorders also supports long-term home-based management. In addition, healthcare providers are encouraging home care solutions to reduce hospital burden. As digital healthcare continues to expand, this segment is expected to grow rapidly.

• By Distribution Channel

On the basis of distribution channel, the Sleep Disorder Treatment market is segmented into direct tender, hospital pharmacy, retail pharmacy, online pharmacy, and others. The retail pharmacy segment held the largest market revenue share of 41.9% in 2025, driven by easy accessibility of sleep medications and over-the-counter products. Retail pharmacies serve as the primary distribution point for both prescription and non-prescription sleep aids. Strong distribution networks ensure availability across urban and rural areas. Increasing consumer awareness about sleep disorders and self-medication trends further support growth. Pharmacists also play a key role in guiding patients regarding medication usage. The availability of multiple brands and formulations enhances consumer choice. In addition, rising demand for OTC sleep aids contributes to segment expansion. Convenient store locations and immediate product availability strengthen market presence.

The online pharmacy segment is expected to witness the fastest CAGR of 13.2% from 2026 to 2033, driven by the rapid growth of e-commerce and digital healthcare platforms. Online pharmacies offer convenience, home delivery, and competitive pricing, attracting a large customer base. Increasing internet penetration and smartphone usage are key growth drivers. Patients benefit from access to a wide range of products and detailed information online. The expansion of telemedicine services further supports online prescription fulfillment. Secure payment systems and improved logistics enhance consumer trust. In addition, the preference for contactless purchasing has increased significantly post-pandemic. As digital healthcare adoption rises, this segment is expected to grow substantially.

Sleep Disorder Treatment Market Regional Analysis

- North America dominated the Sleep Disorder Treatment market with the largest revenue share of approximately 42.6% in 2025, characterized by advanced healthcare infrastructure, high awareness of sleep health, and strong adoption of CPAP devices and prescription therapies

- The region benefits from well-established sleep clinics, widespread diagnostic capabilities such as polysomnography, and increasing focus on managing sleep-related conditions

- Rising prevalence of disorders such as insomnia, sleep apnea, and restless leg syndrome is further driving demand. In addition, continuous advancements in treatment technologies and strong reimbursement frameworks are supporting market growth across North America

U.S. Sleep Disorder Treatment Market Insight

The U.S. sleep disorder treatment market captured the largest revenue share within North America in 2025, driven by high diagnosis and treatment rates. The country has a strong network of sleep centers and advanced healthcare facilities enabling early detection and effective management of sleep disorders. Increasing adoption of CPAP devices, oral appliances, and digital sleep monitoring solutions is improving patient outcomes. Furthermore, growing awareness campaigns and physician recommendations are accelerating market expansion.

Europe Sleep Disorder Treatment Market Insight

The Europe sleep disorder treatment market is projected to expand at a substantial CAGR during the forecast period, supported by increasing awareness of sleep health and growing prevalence of sleep-related conditions. Government initiatives and healthcare programs promoting early diagnosis and treatment are boosting market growth. In addition, advancements in sleep diagnostic technologies and expanding access to treatment options are contributing to regional expansion.

U.K. Sleep Disorder Treatment Market Insight

The U.K. sleep disorder treatment market is anticipated to grow at a noteworthy CAGR, driven by rising awareness of sleep disorders and strong public healthcare support. Increasing diagnosis rates and adoption of therapeutic devices such as CPAP machines are supporting market growth. Moreover, ongoing public health initiatives and research activities are enhancing patient care and treatment accessibility.

Germany Sleep Disorder Treatment Market Insight

The Germany sleep disorder treatment market is expected to expand at a considerable CAGR, fueled by advanced healthcare infrastructure and increasing focus on sleep medicine. Germany’s strong medical device industry and emphasis on innovation are encouraging adoption of modern diagnostic and therapeutic solutions. The growing use of sleep monitoring technologies and treatment devices is further supporting market growth.

Asia-Pacific Sleep Disorder Treatment Market Insight

The Asia-Pacific sleep disorder treatment market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare expenditure, rising awareness of sleep disorders, and expanding access to diagnostic and treatment facilities. Rapid urbanization, stressful lifestyles, and growing prevalence of sleep disorders are contributing to rising demand. Government efforts to improve healthcare infrastructure are further accelerating market expansion.

Japan Sleep Disorder Treatment Market Insight

The Japan sleep disorder treatment market is gaining momentum due to increasing awareness of sleep health and a rapidly aging population. Growing adoption of advanced diagnostic tools and therapeutic devices is improving treatment outcomes. In addition, Japan’s focus on healthcare innovation and quality care is supporting the development and adoption of sleep disorder treatments.

China Sleep Disorder Treatment Market Insight

The China Sleep Disorder Treatment market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rising healthcare investments, increasing prevalence of sleep disorders, and expanding access to medical services. Growing awareness of sleep health and the adoption of diagnostic technologies are improving detection rates. Furthermore, government support and rapid development of healthcare infrastructure are key factors driving market growth in China.

Sleep Disorder Treatment Market Share

The Sleep Disorder Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Sanofi S.A. (France)

- GlaxoSmithKline plc (U.K.)

- AstraZeneca plc (U.K.)

- Merck & Co., Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Mylan N.V. (U.S.)

- ResMed Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Fisher & Paykel Healthcare Corporation Limited (New Zealand)

- Inspire Medical Systems, Inc. (U.S.)

- SomnoMed Limited (Australia)

- Natus Medical Incorporated (U.S.)

- BMC Medical Co., Ltd. (China)

- Compumedics Limited (Australia)

- Drive DeVilbiss Healthcare (U.S.)

- Itamar Medical Ltd. (Israel)

Latest Developments in Global Sleep Disorder Treatment Market

- In August 2021, the U.S. Food and Drug Administration approved Xywav (Jazz Pharmaceuticals) for the treatment of idiopathic hypersomnia, marking the first FDA-approved therapy specifically for this rare sleep disorder. This approval expanded treatment options for patients suffering from excessive daytime sleepiness and highlighted growing innovation in sleep disorder therapeutics

- In January 2022, the U.S. Food and Drug Administration approved QUVIVIQ (daridorexant), developed by Idorsia Pharmaceuticals, for the treatment of adult patients with insomnia. The drug, a dual orexin receptor antagonist (DORA), introduced a novel mechanism targeting wakefulness pathways rather than sedation, representing a significant advancement in insomnia treatment

- In August 2024, Big Health received U.S. FDA clearance for SleepioRx, a prescription digital therapeutic for chronic insomnia. This marked a major step toward non-drug treatment approaches, using cognitive behavioral therapy delivered digitally to improve sleep outcomes and expand access to care

- In December 2024, the U.S. Food and Drug Administration approved Zepbound (tirzepatide) for the treatment of moderate to severe obstructive sleep apnea in adults with obesity, making it the first drug specifically indicated for sleep apnea. This breakthrough introduced a pharmacological alternative to traditional device-based therapies such as CPAP

- In October 2024, the U.S. FDA expanded the approval of Lumryz (Avadel Pharmaceuticals) to include pediatric patients aged 7 years and older with narcolepsy, broadening access to treatment and strengthening its position in the sleep disorder therapeutics market

- In June 2025, the U.S. FDA granted orphan drug designation to Lumryz for the treatment of idiopathic hypersomnia, supporting ongoing clinical development and providing incentives for further innovation in rare sleep disorder therapies

- In August 2025, Nyxoah received U.S. FDA approval for its Genio hypoglossal nerve stimulation system for the treatment of moderate to severe obstructive sleep apnea. This implantable device offers an alternative to CPAP therapy by stimulating airway muscles to prevent obstruction during sleep

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.