Global Smart Implantable Biosensor Devices Market

Market Size in USD Billion

USD

1.27 Billion

USD

5.14 Billion

2025

2033

USD

1.27 Billion

USD

5.14 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.27 Billion | |

| USD 5.14 Billion | |

| % | |

|

Smart Implantable Biosensor Devices Market Size

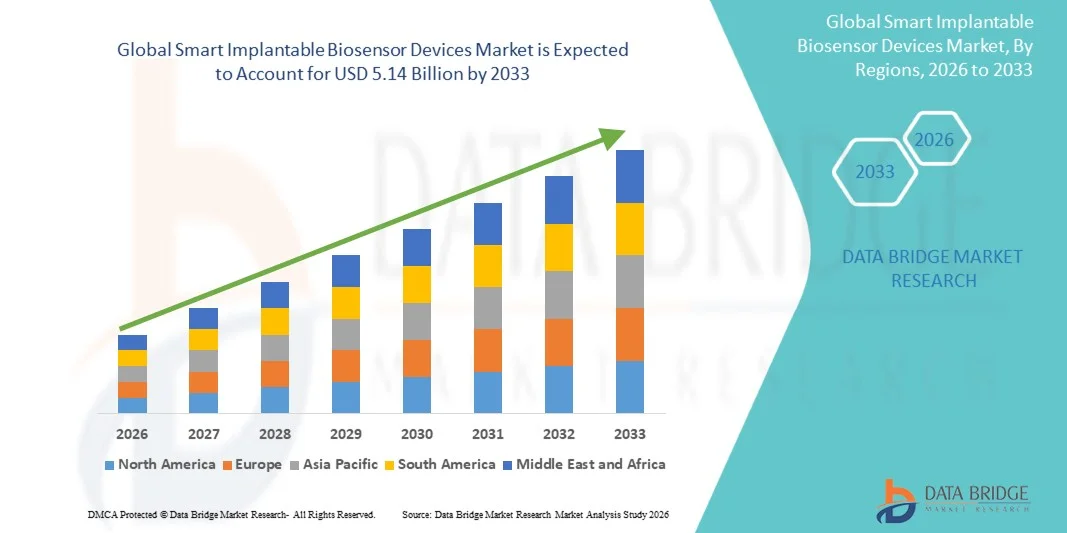

- The global Smart Implantable Biosensor Devices market size was valued at USD 1.27 billion in 2025 and is expected to reach USD 5.14 billion by 2033, at a CAGR of 19.10% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases such as diabetes, cardiovascular disorders, and neurological conditions, driving the adoption of smart implantable biosensor devices for continuous and real-time monitoring

- Furthermore, rising demand for connected, minimally invasive, and remote patient monitoring solutions is establishing smart implantable biosensor devices as essential tools for early detection, personalized treatment, and improved patient outcomes, thereby significantly boosting the market’s growth

Smart Implantable Biosensor Devices Market Analysis

- Smart implantable biosensor devices, which provide continuous monitoring of physiological parameters such as glucose levels, cardiac activity, and neurological signals, are increasingly becoming essential in both clinical and homecare settings due to the growing prevalence of chronic diseases and demand for real-time health monitoring

- The escalating demand for smart implantable biosensor devices is primarily driven by advancements in wireless connectivity, AI integration, and minimally invasive device design, enabling remote patient monitoring, early disease detection, and personalized treatment plans

- North America dominated the smart implantable biosensor devices market with the largest revenue share of 39.2% in 2025, supported by advanced healthcare infrastructure, high adoption of connected medical devices, and a strong presence of key industry players, with the U.S. witnessing significant growth in clinical and home-based deployments

- Asia-Pacific is expected to be the fastest growing region in the smart implantable biosensor devices market during the forecast period, owing to increasing healthcare awareness, rising prevalence of chronic diseases, and growing investments in medical technology in countries such as China, India, and Japan

- The glucose monitoring sensors segment dominated the largest market revenue share of 48.5% in 2025, driven by the high prevalence of diabetes and growing demand for continuous glucose monitoring (CGM) systems

Report Scope and Smart Implantable Biosensor Devices Market Segmentation

|

Attributes |

Smart Implantable Biosensor Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Medtronic plc (Ireland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Smart Implantable Biosensor Devices Market Trends

“Enhanced Patient Monitoring and Real-Time Health Insights Through Smart Implantable Biosensors”

- A key trend in the global smart implantable biosensor devices market is the integration of advanced sensor technology with wireless connectivity, enabling continuous real-time monitoring of physiological parameters such as glucose, cardiac rhythm, or blood pressure

- For instance, some next-generation biosensors now allow data to be transmitted securely to physicians or caregivers via smartphones or cloud platforms, providing timely alerts for anomalies and reducing the need for frequent hospital visits

- These devices are increasingly incorporating AI-driven analytics to predict health events, personalize treatment regimens, and improve patient outcomes. Predictive algorithms can detect early deviations from normal ranges and provide actionable insights to clinicians, enhancing preventive care

- Furthermore, trends in minimally invasive implantation techniques and biocompatible materials are making these devices more patient-friendly, supporting long-term adoption for chronic disease management and post-operative monitoring

Smart Implantable Biosensor Devices Market Dynamics

Driver

“Growing Need for Personalized, Remote, and Continuous Healthcare Monitoring”

- The rising prevalence of chronic conditions, cardiovascular diseases, diabetes, and other lifestyle-related disorders is driving the demand for continuous and personalized monitoring solutions through smart implantable biosensors

- For instance, in March 2025, Medtronic announced the launch of its next-generation cardiac implantable sensor capable of continuous hemodynamic monitoring and remote data transmission to clinicians. Such innovations are expected to significantly propel market growth

- Continuous monitoring allows patients to maintain normal daily activities while enabling physicians to track therapy effectiveness, detect complications early, and adjust interventions without repeated hospital visits

- Increasing awareness and adoption of telehealth platforms, coupled with integration of biosensor data into electronic health records (EHRs), further facilitate remote patient management

- Rising patient preference for minimally invasive, self-managed healthcare solutions, combined with healthcare providers’ emphasis on preventive care and early intervention, is strengthening the adoption of smart implantable biosensors globally

Restraint/Challenge

“Concerns Regarding Data Security, Device Reliability, and High Costs”

- Data privacy and cybersecurity concerns remain major barriers, as implantable devices collect sensitive physiological data and transmit it over wireless networks. Unauthorized access or breaches can compromise patient confidentiality and safety

- For instance, past reports of vulnerabilities in medical IoT devices have made hospitals and patients cautious about adopting connected implantable solutions. Leading companies like Abbott and Medtronic are addressing these issues through robust encryption, secure authentication, and frequent software updates

- In addition, the high initial cost of advanced smart implantable biosensors may restrict adoption among price-sensitive patients or smaller healthcare facilities. Devices offering multi-parameter monitoring or advanced analytics often carry premium pricing

- Device reliability and long-term performance are also critical concerns, as implantable sensors must maintain accuracy over years while remaining biocompatible. Malfunction or calibration drift can undermine trust in these technologies

- Overcoming these challenges through stronger cybersecurity protocols, patient and provider education, development of cost-effective device variants, and improving device longevity will be essential for sustained market growth

Smart Implantable Biosensor Devices Market Scope

The Smart Implantable Biosensor Devices market is segmented on the basis of device type and end user.

• By Device Type

On the basis of device type, the Smart Implantable Biosensor Devices market is segmented into glucose monitoring sensors, cardiac monitoring sensors, neurostimulators, and other implantable biosensors. The glucose monitoring sensors segment dominated the largest market revenue share of 48.5% in 2025, driven by the high prevalence of diabetes and growing demand for continuous glucose monitoring (CGM) systems. Hospitals and clinics widely adopt these devices for inpatients and high-risk diabetic patients to maintain real-time glucose level tracking. Continuous improvements in sensor accuracy, miniaturization, and integration with smartphones and cloud platforms enhance adoption. Patients benefit from real-time alerts, data analytics, and remote monitoring. Insurance coverage for diabetes management devices and reimbursement policies strengthen the segment’s revenue share. Hospitals, homecare, and specialty clinics increasingly rely on these devices for personalized treatment plans. Awareness campaigns for early diabetes detection also support adoption. CGM devices are widely validated in clinical trials, boosting physician confidence. Integration with telemedicine platforms further reinforces usage. Device compatibility with insulin pumps increases treatment efficiency. The segment also benefits from technological partnerships between device manufacturers and digital health platforms.

The cardiac monitoring sensors segment is expected to witness the fastest CAGR of 20.8% from 2026 to 2033, fueled by increasing prevalence of cardiovascular diseases and demand for continuous remote cardiac monitoring. Hospitals, homecare providers, and research institutes adopt implantable cardiac monitors to detect arrhythmias, heart failure, and ischemic events. Technological advancements in miniaturized sensors, wireless transmission, and AI-based alert systems drive adoption. Patients increasingly prefer wearable or implantable cardiac solutions for early detection and remote supervision. Growth is further supported by telemedicine expansion, home monitoring programs, and rising awareness of cardiovascular risk factors. Research and academic institutions are exploring multifunctional biosensors integrating cardiac monitoring with other vital parameters. Regulatory approvals for next-generation cardiac devices facilitate adoption. Aging populations in developed and emerging markets further boost demand. Integration with cloud-based health platforms improves real-time data access for physicians. Cardiac sensor adoption in post-operative care enhances hospital workflow efficiency. Partnerships between device manufacturers and healthcare providers accelerate deployment.

• By End User

On the basis of end user, the market is segmented into hospitals & clinics, research & academic institutes, homecare settings, and other healthcare facilities. The hospitals & clinics segment dominated the largest market revenue share of 56.2% in 2025, driven by the availability of skilled staff, advanced implantable device infrastructure, and high patient volumes. Hospitals adopt biosensor devices for chronic disease management, continuous monitoring, and post-surgical patient care. Regulatory approvals, reimbursement policies, and clinical guidelines reinforce hospital adoption. The segment benefits from established physician networks, multi-disciplinary care teams, and clinical trials conducted in hospital settings. Integration of data from implantable sensors with electronic medical records (EMR) enhances patient care efficiency. Hospitals also act as training and demonstration centers for device usage. High prevalence of diabetes and cardiovascular disorders ensures sustained demand. Telemedicine and remote monitoring programs complement hospital-based monitoring. Patient awareness campaigns conducted by hospitals improve adoption. Hospital pharmacies and in-house clinical support further strengthen usage.

The homecare settings segment is expected to witness the fastest CAGR of 21.5% from 2026 to 2033, fueled by increasing demand for remote monitoring, convenience, and patient-centered care. Implantable biosensors in homecare enable patients to track glucose levels, cardiac activity, or neurological signals without frequent hospital visits. Integration with smartphones, mobile apps, and telehealth platforms enhances real-time monitoring and physician intervention. Rising awareness of chronic disease management and aging populations support adoption. Technological advancements in battery life, wireless connectivity, and miniaturization further drive growth. Patients prefer home-based monitoring for long-term convenience and reduced healthcare costs. Collaboration between homecare providers and device manufacturers accelerates distribution. Emerging markets are witnessing rapid adoption due to improving homecare infrastructure. Insurance coverage for home monitoring devices reinforces growth. Educational programs for patients and caregivers enhance compliance. Homecare adoption allows integration with other remote health monitoring platforms, supporting holistic patient care.

Smart Implantable Biosensor Devices Market Regional Analysis

- North America dominated the smart implantable biosensor devices market with the largest revenue share of 39.2% in 2025

- Supported by advanced healthcare infrastructure, high adoption of connected medical devices, and a strong presence of key industry players. The U.S. is witnessing significant growth in clinical and home-based deployments of biosensor devices for continuous monitoring of cardiac, glucose, and other physiological parameters

- The rising focus on preventive care, early detection of chronic diseases, and integration with telehealth platforms is further fueling market expansion

U.S. Smart Implantable Biosensor Devices Market Insight

The U.S. smart implantable biosensor devices market captured the largest revenue share within North America in 2025, driven by increasing adoption of implantable biosensors in hospitals, clinics, and home healthcare settings. Advancements in minimally invasive implantation techniques and biocompatible sensor materials are making these devices more accessible and patient-friendly. Furthermore, integration with cloud platforms and remote monitoring solutions enables healthcare providers to track patient health in real time, improving outcomes while reducing hospital readmissions.

Europe Smart Implantable Biosensor Devices Market Insight

The Europe smart implantable biosensor devices market is expected to grow at a notable CAGR over the forecast period, driven by increasing healthcare expenditure, a rising geriatric population, and regulatory support for digital health innovations. Countries such as Germany, France, and the U.K. are witnessing the adoption of smart biosensors in both clinical and home-based monitoring. Investments in telehealth infrastructure and electronic health records (EHRs) facilitate real-time data access for clinicians, strengthening the market’s expansion.

U.K. Smart Implantable Biosensor Devices Market Insight

The U.K. smart implantable biosensor devices market is projected to experience significant growth, fueled by an increasing prevalence of chronic diseases such as cardiovascular conditions and diabetes. The government’s focus on remote patient monitoring and home-based care solutions is encouraging the adoption of implantable biosensors. In addition, growing patient awareness and healthcare provider initiatives aimed at personalized therapy and early intervention are supporting market expansion.

Germany Smart Implantable Biosensor Devices Market Insight

Germany’s smart implantable biosensor devices market is expanding steadily, driven by its well-developed healthcare infrastructure, advanced research in medical devices, and emphasis on preventive healthcare. The integration of implantable biosensor data into hospital systems and telemedicine platforms is enhancing patient monitoring and disease management. Rising patient acceptance of minimally invasive monitoring devices further strengthens the market’s growth prospects.

Asia-Pacific Smart Implantable Biosensor Devices Market Insight

The Asia-Pacific market is poised to grow at the fastest CAGR during 2026–2033, owing to increasing healthcare awareness, rising prevalence of chronic diseases, and growing investments in medical technology in countries such as China, India, and Japan. Government initiatives promoting digital health and telemedicine, coupled with expanding healthcare infrastructure, are accelerating the adoption of smart implantable biosensors. The region is also benefiting from lower manufacturing costs, making devices more affordable and accessible to a larger patient population.

Japan Smart Implantable Biosensor Devices Market Insight

Japan’s market is gaining momentum due to its high-tech healthcare ecosystem, rapidly aging population, and focus on preventive care. Smart implantable biosensors are increasingly used in home-based monitoring for chronic conditions, supported by advanced hospital networks and integration with digital health platforms. Growing demand for personalized therapy and continuous patient monitoring is fueling the market.

China Smart Implantable Biosensor Devices Market Insight

China smart implantable biosensor devices market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by rapid urbanization, rising middle-class population, and increasing healthcare investments. The prevalence of chronic diseases, along with government support for digital health initiatives and telemedicine, is boosting the adoption of implantable biosensors. Domestic manufacturers and innovations in minimally invasive devices are enhancing accessibility and affordability, further propelling market growth.

Smart Implantable Biosensor Devices Market Share

The Smart Implantable Biosensor Devices industry is primarily led by well-established companies, including:

• Medtronic plc (Ireland)

• Abbott Laboratories (U.S.)

• Dexcom, Inc. (U.S.)

• Boston Scientific Corporation (U.S.)

• Roche Diagnostics (Switzerland)

• BioTelemetry, Inc. (U.S.)

• Senseonics Holdings, Inc. (U.S.)

• Johnson & Johnson (U.S.)

• Edwards Lifesciences Corporation (U.S.)

• Terumo Corporation (Japan)

• Proteus Digital Health, Inc. (U.S.)

• iRhythm Technologies, Inc. (U.S.)

• Philips Healthcare (Netherlands)

• Siemens Healthineers AG (Germany)

• GE Healthcare (U.S.)

• Stryker Corporation (U.S.)

• Abbott Vascular (U.S.)

• Nipro Corporation (Japan)

• Boston Scientific Neuromodulation (U.S.)

• Becton, Dickinson and Company (U.S.)

Latest Developments in Global Smart Implantable Biosensor Devices Market

- In April 2024, Innovar Health introduced smart implantable biosensors integrated with artificial intelligence (AI) capabilities, designed for real‑time tracking of physiological parameters and personalized healthcare monitoring, marking a significant step forward in smart implantable sensor technology for continuous patient data collection

- In September 2024, Medtrix Solutions completed its acquisition of BioSense Technologies, a move aimed at expanding its portfolio in the implantable biosensors market, particularly for continuous disease monitoring solutions, and strengthening its position in the smart biosensor device sector

- In October 2024, Medtronic announced its acquisition of CardioMEMS, enhancing its portfolio of implantable sensors focused on chronic disease management and remote physiological monitoring, supporting expanded use of smart implantable biosensor technologies in cardiovascular care

- In December 2024, Sensotrix launched next‑generation implantable biosensors featuring advanced wireless connectivity and improved operational longevity, aimed at supporting continuous health monitoring and expanding clinical applications of implantable biosensor devices

- In March 2025, Dexcom announced a strategic partnership with Philips Healthcare to co‑develop implantable biosensor technologies for continuous physiological monitoring and seamless data integration into remote patient management platforms, advancing the integration of smart biosensors with broader healthcare systems

- In July 2025, Abbott Laboratories launched a new implantable biosensor platform designed for cardiovascular monitoring, backed by significant hospital contract deployments, reflecting growing clinical adoption of smart implantable biosensors in cardiovascular care settings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.