Global Smart Medical Devices Market

Market Size in USD Billion

USD

88.70 Billion

USD

512.00 Billion

2025

2033

USD

88.70 Billion

USD

512.00 Billion

2025

2033

| 2026 - 2033 | |

| USD 88.70 Billion | |

| USD 512.00 Billion | |

| % | |

|

Smart Medical Devices Market Overview

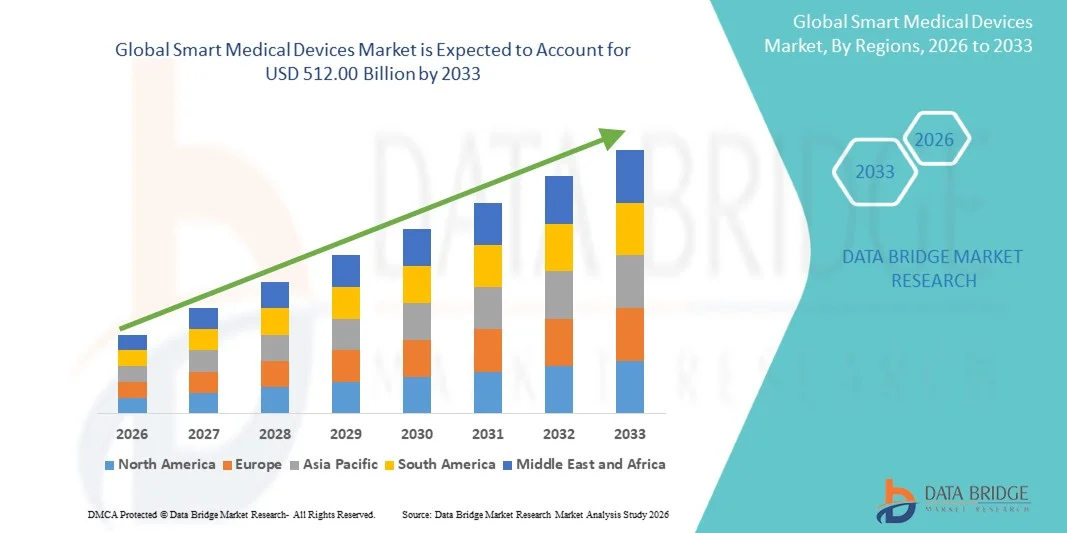

The Smart Medical Devices Market was valued at USD 88.70 billion in 2025 and is projected to reach USD 512.00 billion by 2033, growing at a CAGR of 24.50% from 2026 to 2033. The market is witnessing steady expansion driven by the rising adoption of connected healthcare technologies, increasing prevalence of chronic diseases, and growing demand for remote patient monitoring and personalized treatment solutions. Integration of IoT, AI, and cloud-based analytics into medical devices is significantly enhancing diagnostic accuracy and real-time health tracking capabilities.

The growing aging population, coupled with the surge in hospital-at-home care models and telehealth services, is accelerating the deployment of smart medical devices across hospitals, clinics, and homecare settings. In addition, increasing healthcare digitization initiatives and supportive government policies for digital health infrastructure are further encouraging the adoption of wearable devices, smart implants, and connected diagnostic equipment. These advancements are reshaping traditional healthcare delivery by improving efficiency, reducing costs, and enabling proactive disease management.

Key Market Trends & Insights

- North America dominated the Smart Medical Devices Market with the largest revenue share of 36.42% in 2025, supported by strong healthcare digitization, high adoption of connected care solutions, and presence of leading medtech companies.

- The Diagnostics and Monitoring Devices segment led the market with a 42.05% share in 2025, driven by increasing demand for real-time health tracking, early disease detection, and continuous patient monitoring solutions.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by expanding healthcare infrastructure, increasing chronic disease burden, and rapid adoption of digital health technologies in China, India, and Japan.

- Therapeutic Devices are the fastest-growing product type, projected to register a CAGR of 7.8%, reflecting the surge in demand for adoption of smart insulin pumps, connected drug delivery systems, and implantable therapeutic devices.

- The On-Body (Adhesive Patch) segment dominated the type category with a 39.64% revenue share in 2025, led by increasing demand for continuous, non-invasive health monitoring solutions.

- Motor-Driven technology accounted for 37.28% of the market, preferred by widespread use in insulin pumps, infusion systems, and automated drug delivery devices.

- The Non-Wearable segment is the fastest-growing modality category, with a CAGR of 7.5%, driven by increasing use of smart hospital equipment, connected diagnostic systems, and remote monitoring stations.

Market Size & Forecast

- Global Market Value (2025): USD 88.70 Billion

- Expected Market Value (2033): USD 512.00 Billion

- Forecast CAGR (2026–2033): 24.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Smart Medical Devices Market Segmentation

|

Attributes |

Smart Medical Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Abbott (U.S.) · Medtronic (Ireland) · Dexcom, Inc. (U.S.) · Koninklijke Philips N.V. (Netherlands) · GE HealthCare (U.S.) · Siemens Healthineers AG (Germany) · Boston Scientific Corporation (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · ResMed Inc. (U.S.) · Masimo Corporation (U.S.) · Omron Healthcare Co., Ltd. (Japan) · iRhythm Technologies, Inc. (U.S.) · Insulet Corporation (U.S.) · Tandem Diabetes Care, Inc. (U.S.) · Biotronik SE & Co. KG (Germany) · AliveCor, Inc. (U.S.) · Apple Inc. (U.S.) · Baxter (U.S.) · F. Hoffmann-La Roche Ltd (Switzerland) · BD (U.S.) |

|

Market Opportunities |

· Expansion of AI-powered predictive diagnostics integrated into smart medical devices · Growing demand for interoperable remote patient monitoring ecosystems · Rising adoption of smart implantable devices |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Smart Medical Devices Market Trends

Trend: Expansion of Remote Patient Monitoring and Wearable Ecosystems

Healthcare providers and consumers are increasingly adopting wearable and connected medical devices that enable continuous monitoring of vital signs such as heart rate, glucose levels, and blood oxygen in real time outside clinical settings. The integration of cloud platforms and mobile health applications allows seamless data transmission between patients and physicians, enabling faster clinical decision-making and proactive disease management. Artificial intelligence-driven analytics further enhances predictive insights, while interoperability across devices and healthcare systems is improving overall care coordination. For instance, wearable ECG patches and connected insulin monitors are widely used in chronic disease management programs across advanced healthcare systems.

Smart Medical Devices Market Dynamics

Key Market Driver: Rising Burden of Chronic Diseases and Demand for Continuous Monitoring

The increasing prevalence of chronic conditions such as diabetes, cardiovascular disorders, and respiratory diseases is driving strong demand for smart medical devices that enable long-term patient monitoring and timely intervention. Healthcare systems are shifting from reactive treatment models to preventive and value-based care approaches supported by real-time health data collection and remote diagnostics. The integration of AI and IoT technologies into medical devices is enhancing diagnostic accuracy and enabling personalized treatment pathways across hospitals and homecare settings. For instance, connected glucose monitoring systems and smart cardiac implants are increasingly deployed in chronic care management programs across global healthcare networks.

Key Restraint/Challenge: Data Privacy Concerns and High Device Cost Barriers

A significant restraint in the smart medical devices market is the growing concern over patient data privacy and cybersecurity risks associated with continuous health data transmission across connected platforms. In addition, the high cost of advanced smart devices and supporting digital infrastructure limits adoption in low- and middle-income regions, creating disparities in access to connected healthcare solutions. Regulatory complexities and lack of standardized interoperability frameworks further slowdown large-scale deployment across fragmented healthcare systems. For instance, hospitals in emerging markets often face challenges in implementing integrated wearable monitoring systems due to budget constraints and data security compliance requirements.

Key Market Opportunity: Expansion of AI-Enabled Predictive Healthcare and Smart Implant Ecosystems

The integration of artificial intelligence with smart medical devices is creating strong opportunities for predictive healthcare, enabling early diagnosis, risk stratification, and personalized treatment planning based on continuous patient data streams. Growing adoption of smart implantable devices such as connected cardiac monitors, neurostimulators, and insulin delivery systems is further expanding long-term therapeutic monitoring capabilities. In addition, the shift toward cloud-based healthcare platforms and interoperable digital ecosystems is opening new opportunities for scalable remote care solutions across hospitals and homecare settings. For instance, AI-enabled cardiac monitoring patches and smart insulin pumps are increasingly being deployed in chronic disease management programs across advanced healthcare systems.

Smart Medical Devices Market Scope

The smart medical devices market is segmented on the basis of product type, type, technology, modality, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the Smart Medical Devices Market is segmented into diagnostics and monitoring devices and therapeutic devices. The Diagnostics and Monitoring Devices segment dominated the market with a 42.05% share in 2025, driven by increasing demand for real-time health tracking, early disease detection, and continuous patient monitoring solutions. These devices include smart ECG monitors, glucose tracking systems, and connected imaging tools widely used in hospitals and homecare settings. Rising prevalence of chronic diseases such as diabetes and cardiovascular disorders is significantly boosting adoption. Integration of AI and IoT technologies enhances diagnostic accuracy and enables predictive healthcare insights. Strong hospital digitization and remote monitoring programs further strengthen segment dominance. The segment benefits from high clinical reliability and widespread reimbursement support in developed healthcare systems.

The Therapeutic Devices segment is expected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by rising adoption of smart insulin pumps, connected drug delivery systems, and implantable therapeutic devices. These systems enable automated and personalized treatment delivery, improving patient adherence and outcomes. Increasing demand for minimally invasive and home-based treatment solutions is accelerating adoption. Continuous advancements in bioelectronics and closed-loop therapeutic systems are enhancing treatment precision. Growing preference for self-managed care among chronic patients is further supporting expansion. Integration with mobile apps and cloud platforms enables real-time therapy adjustments and remote physician monitoring.

- By Type

On the basis of type, the market is segmented into on-body (adhesive patch), off-body (belt clip), and handheld devices. The On-Body (Adhesive Patch) segment dominated the market with a 39.64% share in 2025, driven by increasing demand for continuous, non-invasive health monitoring solutions. These patches are widely used for ECG monitoring, glucose tracking, and temperature sensing in chronic care management. Their lightweight design and ease of use make them highly suitable for long-term patient monitoring outside hospitals. Growing adoption in elderly care and post-surgical monitoring is further strengthening demand. Advancements in flexible electronics and sensor miniaturization are improving device performance. Increasing preference for wearable convenience and real-time data transmission supports sustained dominance.

The Off-Body (Belt Clip) segment is expected to witness the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing use in specialized clinical monitoring and rehabilitation applications. These devices offer higher processing capacity and extended battery life compared to compact wearables. They are widely used in hospital-based monitoring systems and high-risk patient care environments. Rising demand for hybrid monitoring systems combining portability and accuracy is supporting growth. Integration with wireless communication technologies enhances mobility and data accessibility. Expanding use in sports medicine and physical therapy programs is further accelerating adoption.

- By Technology

On the basis of technology, the market is segmented into spring-based, motor-driven, rotary pump, expanding battery, pressurized gas, and others. The Motor-Driven technology segment dominated the market with a 37.28% share in 2025, driven by widespread use in insulin pumps, infusion systems, and automated drug delivery devices. These systems provide precise and controlled medication dosing, improving treatment accuracy and patient safety. Increasing prevalence of chronic diseases requiring long-term therapy is boosting adoption. Strong integration with digital monitoring systems enables real-time dosage adjustments. Continuous improvements in micro-motor efficiency are enhancing device reliability. The segment benefits from high clinical acceptance and strong hospital adoption rates.

The Expanding Battery technology segment is expected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by rising demand for compact, long-lasting, and energy-efficient smart medical devices. These batteries enable extended device operation in wearable and implantable applications without frequent replacement. Increasing use in continuous monitoring devices and portable diagnostic systems is fueling demand. Advancements in flexible energy storage and biocompatible materials are supporting innovation. Growing preference for miniaturized medical devices is accelerating adoption. Expanding use in remote healthcare and home-based monitoring systems further supports growth.

- By Modality

On the basis of modality, the market is segmented into wearable and non-wearable devices. The Wearable segment dominated the market with a 53.66% share in 2025, driven by strong adoption of fitness trackers, smart patches, and continuous health monitoring devices. Increasing consumer awareness about preventive healthcare and wellness management is boosting demand. These devices enable real-time tracking of vital signs such as heart rate, oxygen levels, and physical activity. Integration with smartphones and cloud platforms enhances usability and data accessibility. Rising adoption in chronic disease management programs is further strengthening growth. Continuous innovation in sensor technology and device miniaturization supports market leadership.

The Non-Wearable segment is expected to witness the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by increasing use of smart hospital equipment, connected diagnostic systems, and remote monitoring stations. These systems provide high-precision clinical data and are widely used in intensive care and surgical environments. Growing hospital digitization and smart infrastructure development are accelerating adoption. Integration with AI-based analytics improves diagnostic efficiency and patient outcomes. Rising demand for centralized monitoring systems in healthcare facilities supports expansion. Expanding deployment in telehealth-supported hospital networks further drives growth.

- By Application

On the basis of application, the market is segmented into oncology, diabetes, auto-immune disorders, infectious diseases, sports & fitness, sleep disorders, and others. The Diabetes segment dominated the market with a 34.91% share in 2025, driven by increasing global prevalence of diabetes and strong adoption of continuous glucose monitoring systems. Smart insulin pumps and connected glucose sensors enable real-time blood sugar tracking and automated insulin delivery. Rising lifestyle-related disorders and obesity rates are further boosting demand. Strong integration with mobile health apps enhances patient compliance and monitoring. Expanding insurance coverage for diabetes management devices supports adoption. Continuous innovation in non-invasive glucose monitoring technologies strengthens dominance.

The Oncology segment is expected to register the fastest growth at a CAGR of 8.3% from 2026 to 2033, driven by increasing use of smart diagnostic and monitoring systems in cancer treatment. These devices enable continuous monitoring of patient vitals, treatment response, and drug delivery accuracy. Rising global cancer burden is significantly driving demand for advanced monitoring solutions. Integration of AI-powered diagnostic tools improves early detection and treatment planning. Growing adoption of personalized oncology care is accelerating device usage. Expanding clinical trials and precision medicine initiatives further support growth.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, home care, sports clubs, and others. The Hospitals segment dominated the market with a 46.37% share in 2025, driven by high adoption of advanced monitoring systems, diagnostic tools, and therapeutic devices. Hospitals require integrated smart ecosystems for critical care, surgery, and patient monitoring. Strong infrastructure and high patient inflow support large-scale deployment of smart medical technologies. Increasing digitization of hospital operations is further enhancing efficiency and care coordination. Government investments in smart hospital infrastructure are boosting adoption. Continuous need for real-time clinical decision support systems strengthens dominance.

The Home Care segment is expected to register the fastest growth at a CAGR of 8.0% from 2026 to 2033, driven by rising demand for decentralized healthcare and patient-centric treatment models. Increasing aging population and chronic disease burden are encouraging home-based monitoring solutions. Wearable and connected devices enable continuous health tracking outside clinical settings. Telehealth integration allows remote physician consultation and treatment adjustments. Cost-effective home care solutions are gaining strong acceptance globally. Expanding adoption of digital health platforms further accelerates growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into pharmacies, online channels, and others. The Pharmacies segment dominated the market with a 51.12% share in 2025, driven by strong accessibility, trusted purchasing environments, and immediate availability of medical devices. Pharmacies play a key role in distributing glucose monitors, wearable patches, and diagnostic tools. Strong physician-pharmacy linkage supports device recommendation and adoption. Increasing presence of retail pharmacy chains enhances market reach. Consumers prefer pharmacies for verified and regulated medical products. Continuous expansion of pharmacy-based healthcare services supports segment leadership.

The Online Channel segment is expected to witness the fastest growth at a CAGR of 8.5% from 2026 to 2033, driven by rising e-commerce adoption and increasing demand for convenient healthcare purchasing. Online platforms offer wide product variety, competitive pricing, and doorstep delivery. Growing digital literacy and smartphone penetration are boosting adoption. Integration of telehealth platforms with e-commerce channels enhances accessibility. Increasing preference for direct-to-consumer medical device sales is further accelerating growth. Expanding regulatory support for online medical device sales strengthens market expansion.

Smart Medical Devices Market Regional Analysis

North America dominated the Smart Medical Devices Market with the largest revenue share of 36.42% in 2025, supported by strong healthcare digitization, high adoption of connected care solutions, and presence of leading medtech companies. The region also benefits from widespread integration of IoT- and AI-enabled medical devices, favorable reimbursement frameworks, and strong government initiatives promoting telehealth and remote patient monitoring. Increasing prevalence of chronic diseases and rising demand for home-based healthcare solutions continue to strengthen North America’s leadership position in the global market.

U.S. Smart Medical Devices Market Insight

The U.S. smart medical devices market is witnessing strong growth due to rising healthcare digitization, increasing prevalence of chronic diseases, and rapid adoption of AI-enabled remote patient monitoring systems. The country’s advanced healthcare infrastructure, along with strong presence of leading medtech and digital health companies, is driving demand across hospitals, homecare, and ambulatory settings. In addition, growing emphasis on value-based care, telehealth expansion, and personalized medicine is accelerating adoption of wearable devices and connected therapeutic systems across the healthcare ecosystem.

Europe Smart Medical Devices Market Insight

The Europe smart medical devices market remains a key contributor to global revenue, driven by strong regulatory frameworks, high healthcare standards, and increasing investments in digital health technologies. The widespread adoption of wearable monitoring devices, smart diagnostic systems, and hospital-based connected platforms is supporting market expansion across the region. Increasing focus on aging population care, chronic disease management, and interoperable healthcare systems continues to strengthen the adoption of smart medical technologies throughout Europe.

U.K. Smart Medical Devices Market Insight

The U.K. smart medical devices market is experiencing steady growth, supported by rising adoption of remote monitoring technologies, increasing NHS digital transformation initiatives, and growing demand for home-based healthcare solutions. Expanding use of wearable health trackers, connected diagnostic tools, and AI-powered patient monitoring systems is contributing to market development. Furthermore, integration of cloud-based healthcare platforms and data-driven clinical decision systems is improving efficiency and positioning the U.K. as a key innovation hub in digital health technologies.

Germany Smart Medical Devices Market Insight

The Germany smart medical devices market is expanding steadily due to strong medical engineering capabilities, advanced healthcare infrastructure, and increasing adoption of digital health solutions in clinical practice. Hospitals, diagnostic centers, and homecare providers are increasingly utilizing connected monitoring systems and smart therapeutic devices for improved patient outcomes. Continuous innovation in medical technology, strong regulatory support for digital health adoption, and rising focus on precision medicine are further driving market growth in Germany.

Asia-Pacific Smart Medical Devices Market Insight

The Asia-Pacific smart medical devices market is expected to witness rapid growth, driven by increasing healthcare expenditure, rising chronic disease burden, and expanding adoption of digital health technologies across emerging economies such as China, India, and Japan. Growing investments in healthcare infrastructure, rising awareness of preventive healthcare, and increasing penetration of wearable and connected devices are supporting regional market expansion. In addition, the growing presence of telehealth platforms and government-led digital health initiatives is accelerating adoption across both urban and rural populations.

Japan Smart Medical Devices Market Insight

The Japan smart medical devices market is witnessing consistent growth due to rising aging population, increasing demand for remote healthcare monitoring, and strong focus on advanced medical technology innovation. Healthcare providers and medical device manufacturers are increasingly adopting wearable monitoring systems, smart diagnostic tools, and AI-powered healthcare platforms. Moreover, integration of robotics, IoT, and digital health solutions is enhancing care efficiency and supporting the country’s emphasis on high-quality, technology-driven healthcare delivery.

China Smart Medical Devices Market Insight

The China smart medical devices market is growing rapidly, driven by expanding healthcare infrastructure, increasing chronic disease prevalence, and strong government support for digital healthcare transformation. Rising adoption of wearable health devices, smart hospital systems, and AI-enabled diagnostic platforms is significantly boosting market demand. In addition, growing investments in healthcare innovation, increasing consumer awareness of preventive health management, and rapid technological advancements are positioning China as one of the fastest-growing markets for smart medical devices globally.

Smart Medical Devices Market Share

The smart medical devices industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Medtronic (Ireland)

- Dexcom, Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- Boston Scientific Corporation (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- ResMed Inc. (U.S.)

- Masimo Corporation (U.S.)

- Omron Healthcare Co., Ltd. (Japan)

- iRhythm Technologies, Inc. (U.S.)

- Insulet Corporation (U.S.)

- Tandem Diabetes Care, Inc. (U.S.)

- Biotronik SE & Co. KG (Germany)

- AliveCor, Inc. (U.S.)

- Apple Inc. (U.S.)

- Baxter (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- BD (U.S.)

Latest Developments in Smart Medical Devices Market

- In September 2023, Medtronic, a global medical device company, expanded its smart insulin delivery ecosystem with enhanced connected diabetes management technologies. The expansion integrates insulin pumps with continuous glucose monitoring systems and mobile applications to provide automated insulin adjustments and real-time diabetes insights. It improves glycemic control and reduces manual intervention for patients with chronic diabetes. The system supports remote physician monitoring and data-driven treatment optimization. It reflects the growing trend toward closed-loop automated insulin delivery systems. The development highlights increasing adoption of AI-enabled therapeutic smart medical devices

- In December 2022, Dexcom, a global leader in continuous glucose monitoring, received FDA clearance for its Dexcom G7 system. The Dexcom G7 is an advanced smart wearable medical device that integrates the sensor and transmitter into a single compact unit, improving usability and patient comfort. It provides real-time glucose data with improved accuracy and a faster warm-up time compared to previous generations. The system is widely used in diabetes care and is integrated with digital health ecosystems for automated insights. It also supports remote monitoring and enhanced physician connectivity

- In August 2022, Apple, a global technology company expanding into digital health, enhanced its Apple Watch with FDA-cleared atrial fibrillation monitoring features. The update allows users to track AFib burden over time, providing deeper insights into heart rhythm irregularities through continuous wearable monitoring. This smart medical capability enables early detection of cardiovascular risks and supports preventive healthcare management. It integrates with Apple’s Health ecosystem, allowing data sharing with healthcare providers for clinical evaluation. The innovation strengthens the convergence of consumer electronics and medical-grade health monitoring

- In April 2022, Abbott, a global healthcare leader, announced FDA clearance of its FreeStyle Libre 3 continuous glucose monitoring system in the United States. The FreeStyle Libre 3 is a next-generation wearable glucose monitoring device that delivers real-time glucose readings directly to smartphones without the need for manual scanning. It is designed to improve diabetes management through continuous, highly accurate, and needle-free monitoring. The device is significantly smaller than previous versions, enhancing patient comfort and compliance. It also enables seamless integration with digital health platforms for better clinical decision-making and remote monitoring

- In March 2021, Philips, a global health technology company, received FDA clearance for its wearable biosensor designed for continuous patient monitoring. The Philips wearable biosensor enables real-time tracking of vital signs such as heart rate, respiratory rate, and patient movement in hospital and remote care settings. It supports early detection of patient deterioration and reduces clinical workload through automated monitoring. The device is widely used in acute care and hospital-at-home models. It also enhances digital transformation in healthcare delivery systems.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.