Global Smart Medical Implants Market

Market Size in USD Billion

USD

5.39 Billion

USD

18.76 Billion

2024

2032

USD

5.39 Billion

USD

18.76 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.39 Billion | |

| USD 18.76 Billion | |

| % | |

|

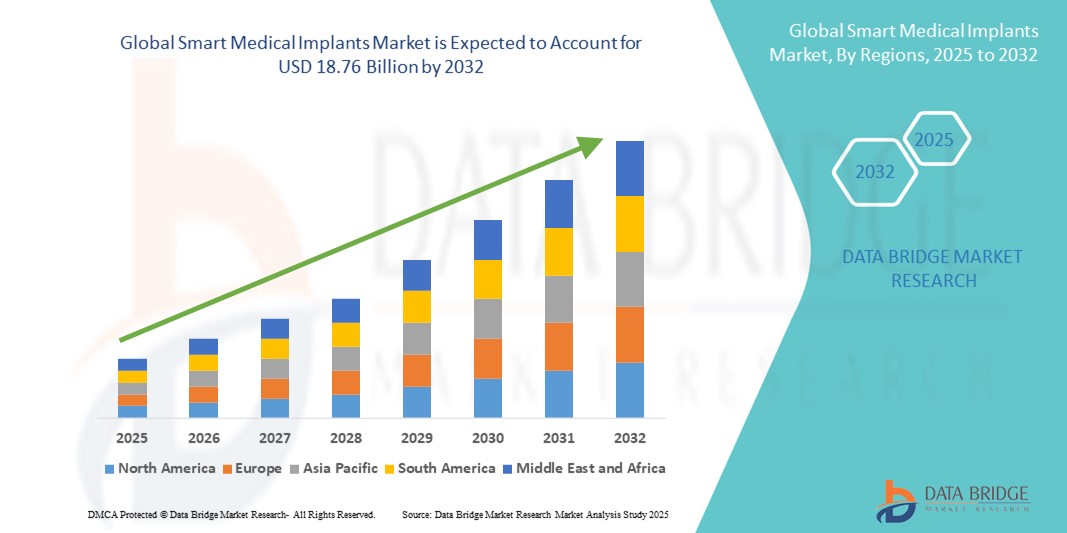

Smart Medical Implants Market Size

- The global smart medical implants market size was valued at USD 5.39 billion in 2024 and is expected to reach USD 18.76 billion by 2032, at a CAGR of 16.85% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced implantable medical devices equipped with sensors, wireless connectivity, and AI-driven monitoring capabilities, enabling real-time health data tracking and personalized treatment. Rising prevalence of chronic diseases, aging populations, and the demand for minimally invasive surgical procedures are further driving the uptake of these smart solutions across various medical specialties

- Furthermore, growing emphasis on improving patient outcomes, reducing hospital readmissions, and enabling remote patient monitoring is establishing smart medical implants as a vital component of modern healthcare delivery. These converging factors are accelerating adoption rates, thereby significantly boosting the market’s expansion

Smart Medical Implants Market Analysis

- Smart medical implants are technologically enhanced implantable devices designed to monitor, record, and transmit physiological data while supporting therapeutic functions. They integrate sensors, microprocessors, and wireless communication systems to enable seamless connectivity with healthcare platforms, facilitating real-time monitoring and predictive diagnostics in fields such as orthopedics, cardiology, neurology, and dentistry

- The escalating demand for smart medical implants is primarily fueled by advancements in biomedical engineering, growing healthcare digitalization, and rising patient preference for devices that combine therapeutic efficacy with continuous health monitoring

- North America dominated the smart medical implants market with a share of 42.3% due to the increasing prevalence of chronic diseases, advancements in implantable device technology, and the growing emphasis on personalized and preventive healthcare

- Asia-Pacific is expected to be the fastest growing region in the smart medical implants market during the forecast period due to rapid urbanization, rising healthcare expenditure, and technological advancements in countries such as China, Japan, and India

- Orthopedic smart implants segment dominated the market with a market share of 42% due to the rising prevalence of musculoskeletal disorders, growing aging population, and increasing demand for post-operative monitoring solutions. These implants integrate sensors and wireless communication technologies to track healing progress, load distribution, and implant performance, enabling personalized rehabilitation plans. Orthopedic smart implants are widely adopted due to their ability to provide real-time data to healthcare providers, improving surgical outcomes and reducing the risk of complications. Their compatibility with remote patient monitoring systems and integration with hospital information systems further strengthens their market dominance

Report Scope and Smart Medical Implants Market Segmentation

|

Attributes |

Smart Medical Implants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Smart Medical Implants Market Trends

Rising Technological Advancements

- Rapid innovations in smart medical implant technology are reshaping healthcare through integration of advanced sensors, microprocessors, AI-driven diagnostics, wireless communication, and real-time data analytics, enabling continuous monitoring and tailored intervention for patients with chronic or acute conditions

- For instance, market leaders are launching implants that combine sophisticated pressure, strain, and temperature sensors with embedded AI and IoT connectivity, supporting applications in cardiology, orthopedics, neurology, and dental surgery, while facilitating remote diagnosis, cloud-based updates, and adaptive therapy through personalized feedback mechanisms

- Product development trends include blockchain-enabled data management to secure patient records and advancements in biocompatible materials enhancing the longevity, safety, and functionality of implants, such as those used in joint replacements and neurostimulators

- Wireless smart implants with capabilities for external adjustment and remote follow-up are advancing minimally invasive procedural possibilities, reducing hospital stay durations and improving patient comfort

- The integration of smart implant systems with hospital information platforms and wearable health devices promotes more holistic patient care and supports rapid decision making in critical care and rehabilitation settings

- AI-powered predictive monitoring in smart implants is facilitating proactive management of postoperative risks and complications, supporting earlier intervention and reducing adverse event rates in high-risk patient populations

Smart Medical Implants Market Dynamics

Driver

Rise in Shift Towards Minimally Invasive Procedures

- Growing global preference for minimally invasive surgeries is a major force behind smart medical implant market expansion, as these techniques offer reduced pain, quicker recovery, minimal scarring, and lower risk of complications compared to traditional open surgeries

- For instance, smart implants enable real-time feedback and remote adjustment during and after minimally invasive procedures in fields such as orthopedics, cardiovascular medicine, and dentistry, contributing to improved accuracy, faster recovery, and fewer follow-up interventions

- Surge in chronic disease prevalence, aging populations, and higher rates of sports injuries and accidents further elevate demand for advanced implants designed for rapid diagnosis and intervention with minimal invasiveness

- Growing investment in healthcare technologies and surgical training fosters greater proficiency among clinicians, accelerating the incorporation of smart implants in routine and complex medical procedures

- Patient-centric care models and integration of personalized medicine approaches with smart implants supports broad-based market momentum by facilitating tailored therapy and risk reduction

Restraint/Challenge

Privacy and Data Security Concerns

- Widespread use of connected smart medical implants raises significant concerns regarding patient data privacy, cybersecurity threats, and compliance with health data protection regulations

- For instance, the growing sophistication of implant sensors and cloud integration introduces risks around hacking, unauthorized data access, and integrity of remote monitoring platforms, challenging manufacturers, hospitals, and regulators to maintain robust security protocols and transparency

- Evolving standards such as HIPAA, GDPR, and local health information guidelines require regular updates to data management and protection strategies, increasing operational and legal complexity for device makers and providers

- Patient mistrust due to potential breaches or privacy violations can slow adoption rates and reduce willingness to use connected smart implants, while adverse publicity around security incidents may impact market reputation

- Balancing seamless data integration for clinical efficacy with privacy safeguards requires ongoing investment in regulatory compliance, technology upgrades, and industry collaboration to ensure safe and ethical deployment of smart medical implants

Smart Medical Implants Market Scope

The market is segmented on the basis of product type and end-user.

- By Product Type

On the basis of product type, the smart medical implants market is segmented into orthopedic smart implants, cardiovascular smart implants, ophthalmic smart implants, dental smart implants, cosmetics smart implants, and others. The orthopedic smart implants segment dominated the largest market revenue share of 42% in 2024, driven by the rising prevalence of musculoskeletal disorders, growing aging population, and increasing demand for post-operative monitoring solutions. These implants integrate sensors and wireless communication technologies to track healing progress, load distribution, and implant performance, enabling personalized rehabilitation plans. Orthopedic smart implants are widely adopted due to their ability to provide real-time data to healthcare providers, improving surgical outcomes and reducing the risk of complications. Their compatibility with remote patient monitoring systems and integration with hospital information systems further strengthens their market dominance.

The cardiovascular smart implants segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing incidence of cardiac disorders, advancements in miniaturized biosensors, and demand for continuous heart health monitoring. These devices, including smart pacemakers and defibrillators, offer features such as wireless diagnostics, automated alerts, and AI-powered data analysis, enabling early intervention in critical cases. Growing patient awareness about proactive cardiac care, coupled with favorable reimbursement policies and technological innovation in battery life and device longevity, is accelerating adoption. In addition, the integration of cloud-based analytics for predictive health insights makes cardiovascular smart implants an attractive choice for both patients and clinicians.

- By End-User

On the basis of end-user, the smart medical implants market is segmented into hospitals, ambulatory surgical centers, specialty centers, and others. The hospitals segment held the largest market revenue share in 2024, driven by their advanced infrastructure, access to specialized surgical expertise, and the ability to manage complex implant procedures. Hospitals often serve as primary centers for the implantation of high-tech medical devices, with dedicated post-operative care units and integrated digital health systems that enhance the efficiency of patient monitoring. The increasing adoption of smart implants in hospitals is also supported by higher patient inflow, access to skilled surgeons, and strong partnerships with medical device manufacturers for early technology adoption.

The specialty centers segment is projected to witness the fastest CAGR from 2025 to 2032, attributed to their focused expertise in specific therapeutic areas and personalized patient care. These centers are increasingly adopting smart implants to offer niche, high-precision treatments, especially in orthopedics, cardiology, and ophthalmology. Specialty centers often provide shorter wait times, customized surgical approaches, and enhanced patient follow-up protocols, making them attractive to patients seeking tailored treatment options. The rising number of outpatient surgeries, coupled with advancements in minimally invasive procedures, is boosting the role of specialty centers in driving future market growth.

Smart Medical Implants Market Regional Analysis

- North America dominated the smart medical implants market with the largest revenue share of 42.3% in 2024, driven by the increasing prevalence of chronic diseases, advancements in implantable device technology, and the growing emphasis on personalized and preventive healthcare

- Healthcare providers in the region highly value the real-time monitoring, data integration, and diagnostic capabilities offered by smart implants, enabling improved patient management and outcomes

- This strong adoption is further supported by favorable reimbursement policies, high healthcare expenditure, and a technologically advanced medical infrastructure, establishing smart implants as a critical tool in both surgical and post-surgical care

U.S. Smart Medical Implants Market Insight

The U.S. smart medical implants market captured the largest revenue share in 2024 within North America, fueled by rapid adoption of connected healthcare devices and the growing trend of personalized medicine. Patients and healthcare professionals increasingly prioritize implants with integrated sensors for continuous health monitoring and early detection of complications. Strong collaborations between medical device manufacturers, research institutions, and healthcare providers, coupled with FDA approvals for next-generation implants, are further propelling market growth. In addition, the integration of AI-powered analytics and remote patient monitoring platforms is significantly enhancing treatment efficiency and outcomes.

Europe Smart Medical Implants Market Insight

The Europe smart medical implants market is projected to expand at a substantial CAGR during the forecast period, primarily driven by stringent medical device regulations, growing prevalence of cardiovascular and orthopedic conditions, and the rising demand for high-precision healthcare solutions. Increasing aging populations and the adoption of advanced implantable devices for chronic disease management are fostering growth. The region is experiencing notable adoption across hospitals, specialty centers, and outpatient facilities, with smart implants becoming a critical component of integrated healthcare delivery systems.

U.K. Smart Medical Implants Market Insight

The U.K. smart medical implants market is anticipated to grow at a noteworthy CAGR, driven by the country’s focus on digital health innovation, early adoption of medical technology, and rising healthcare investments. Increasing cases of orthopedic injuries, cardiovascular disorders, and dental issues are fueling the need for advanced implant solutions. The National Health Service’s (NHS) digital transformation initiatives, combined with growing collaborations between medtech firms and research bodies, are expected to support the adoption of smart medical implants.

Germany Smart Medical Implants Market Insight

The Germany smart medical implants market is expected to expand at a considerable CAGR, supported by the country’s strong medtech manufacturing base, emphasis on innovation, and high healthcare standards. Demand is driven by the need for technologically advanced, durable, and sustainable implant solutions, especially in orthopedic and cardiac care. Germany’s focus on integrating smart implants with hospital IT systems for real-time patient monitoring aligns with its preference for secure and efficient healthcare solutions.

Asia-Pacific Smart Medical Implants Market Insight

The Asia-Pacific smart medical implants market is poised to grow at the fastest CAGR from 2025 to 2032, fueled by rapid urbanization, rising healthcare expenditure, and technological advancements in countries such as China, Japan, and India. Increasing prevalence of lifestyle-related diseases, government initiatives promoting healthcare modernization, and expanding access to advanced treatments are key drivers. APAC’s growing role as a manufacturing hub for medical devices also contributes to the affordability and accessibility of smart implants across the region.

Japan Smart Medical Implants Market Insight

The Japan smart medical implants market is gaining momentum due to its advanced healthcare infrastructure, high adoption of IoT-based medical solutions, and demand for convenience in patient care. The country’s aging population is a significant driver, boosting demand for orthopedic, cardiovascular, and ophthalmic smart implants. Integration of these devices with other health monitoring systems, such as wearable trackers, is further accelerating adoption.

China Smart Medical Implants Market Insight

The China smart medical implants market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s rapidly growing middle class, expanding healthcare infrastructure, and strong domestic manufacturing base. Government-led healthcare reforms and initiatives promoting advanced medical technologies are fostering market expansion. The availability of cost-effective yet technologically advanced implant solutions is making adoption more widespread across both urban and rural areas

Smart Medical Implants Market Share

The smart medical implants industry is primarily led by well-established companies, including:

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

- Medical Device Business Services, Inc. (U.S.)

- IQ IMPLANTS USA (U.S.)

- Canary Medical Inc. (U.S.)

- Medtronic (U.S.)

- NuVasive Inc. (U.S.)

- SIS (Spain)

- Rejoint srl (Italy)

- CONMED Corporation (U.S.)

Latest Developments in Global Smart Medical Implants Market

- In July 2025, Teleflex completed the EUR 760 million acquisition of BIOTRONIK’s vascular intervention unit, securing the Freesolve resorbable scaffold platform. This strategic acquisition positions Teleflex as a stronger player in the vascular implant segment by adding cutting-edge bioresorbable technology to its portfolio. The Freesolve platform offers significant advantages over traditional stents, such as improved vessel healing and reduced long-term complications, aligning with the global shift towards minimally invasive and patient-friendly solutions. This move broadens Teleflex’s cardiovascular product range and also strengthens its competitive presence in both hospital and specialty cardiovascular centers, catering to rising global demand for innovative vascular intervention products

- In July 2025, Cochlear received FDA clearance for its Nucleus Nexa upgradable cochlear implant system, which features on-board memory and lighter processors for enhanced user comfort and performance. This next-generation auditory implant allows for seamless upgrades without the need for invasive replacement surgeries, significantly extending the device’s lifespan and patient value. The lighter design improves wearability, especially for pediatric and elderly patients, while the enhanced memory enables more advanced sound processing features. With growing awareness of hearing health and a rising prevalence of hearing loss worldwide, this innovation is expected to boost adoption rates, reinforce Cochlear’s market leadership, and expand the global smart hearing implant market

- In July 2024, Stryker completed the acquisition of Artelon, significantly enhancing its orthopedic and surgical implant portfolio. Artelon’s proprietary biomaterial technologies are designed to restore soft tissue and ligament functionality, making them highly relevant in sports medicine, trauma, and reconstructive surgery. By integrating these solutions, Stryker can address the rising demand for durable, biocompatible implants that promote faster healing and reduce complications. This acquisition strengthens Stryker’s competitive advantage in the orthopedic implant market and also aligns with its strategy to deliver advanced, patient-focused surgical solutions, supporting long-term growth in the musculoskeletal segment

- In May 2024, Exactech introduced its latest ligament-driven balancing technology, ExactechGPS, featuring new software and modern alignment philosophies for total knee replacement surgeries. This innovation provides surgeons with advanced intraoperative guidance, allowing for greater precision, optimized joint alignment, and personalized implant placement. By integrating real-time data into the surgical process, ExactechGPS enhances patient outcomes, reduces revision rates, and improves long-term joint function. The launch is expected to drive strong adoption in orthopedic centers that are increasingly seeking digital, data-supported surgical tools, thereby expanding Exactech’s footprint in the smart knee implant segment and reinforcing its role as a leader in orthopedic innovation

- In 2022, INTEGRUM, a Swedish-based company, partnered with 20 leading hospitals in the U.S. to introduce its OPRA™ Implant System, a breakthrough solution that accelerates prosthetic limb surgery. The system has achieved a 45% increase in the number of procedures performed since its introduction, reflecting strong clinical acceptance and patient demand. By directly anchoring prosthetic limbs to the skeleton, the OPRA™ system offers improved limb control, faster rehabilitation, and enhanced patient comfort compared to conventional prosthetics. This innovation is transforming the field of prosthetic implants by significantly improving quality of life for amputees, strengthening INTEGRUM’s position as a pioneer in osseointegration technologies, and expanding opportunities in the advanced orthopedic implant market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.