Global Sme Force Automation Market

Market Size in USD Billion

USD

27.64 Billion

USD

85.73 Billion

2025

2033

USD

27.64 Billion

USD

85.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 27.64 Billion | |

| USD 85.73 Billion | |

| % | |

|

What is the Global SME Force Automation Market Size and Growth Rate?

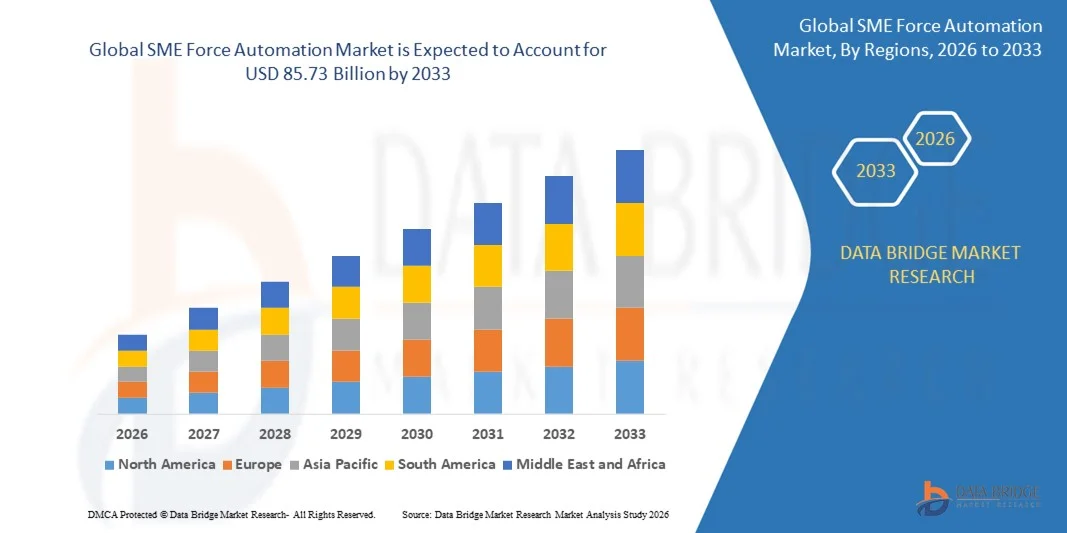

- The global SME force automation market size was valued at USD 27.64 billion in 2025 and is expected to reach USD 85.73 billion by 2033, at a CAGR of15.20% during the forecast period

- The rise in demand for sales forecasting applications in the banking, IT and telecom sectors and retail and growing adoption of cloud sales force automation (SFA) software are the major factors driving the SME force automation market

- The utilization of artificial intelligence (AI) and machine learning (ML) and high deployment of cloud technology and the rising trend of artificial intelligence in sales automation process accelerate the SME force automation market growth

What are the Major Takeaways of SME Force Automation Market?

- The increase in demand for AI for sales management by automating, expanding, and supercharging the way deals are conducted and the utilization of SFA software to collect large amount of data from multiple customer touch points which could be accessed several devices in a cloud deployment also boost the SME force automation market

- In addition, the implementation of rules and regulations including General Data Protection Regulation (GDPR) to strengthen the regulatory framework, concerns regarding data security concerns and launch of updated automation solutions positively affect the SME force automation market. Furthermore, integration of AI and ML capabilities for streamlining field operations and emergence of IoT for improved automation extend profitable opportunities to the SME force automation market players

- North America dominated the SME force automation market with a 39.55% revenue share in 2025, driven by rapid adoption of CRM automation, sales acceleration platforms, and cloud-driven workflow solutions across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 8.6% from 2026 to 2033, driven by rapid digitization, expanding SME base, strong mobile-first business ecosystems, and increasing adoption of cloud CRM and sales automation platforms

- The Solution segment dominated the market with a 62.3% share in 2025, driven by extensive adoption of CRM platforms, workflow automation tools, and integrated analytics solutions

Report Scope and SME Force Automation Market Segmentation

|

Attributes |

SME Force Automation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the SME Force Automation Market?

Rising Adoption of Portable, High-Speed, and Software-Defined SME Force Automation Systems

- The SME force automation market is witnessing robust growth driven by compact, USB-powered, and PC-integrated analyzers designed for microcontrollers, FPGA debugging, IoT devices, and high-speed digital communication validation

- Manufacturers are introducing multi-channel, high-bandwidth analyzers with deep memory buffers, advanced triggering, and software-defined interfaces to support modern embedded systems and rapid prototyping

- Increasing demand for lightweight, portable, and field-deployable instruments is expanding adoption in electronics design labs, academic institutions, and repair/maintenance facilities

- For instance, companies such as Saleae (U.S.), Tektronix (U.S.), Keysight (U.S.), RIGOL (China), and Yokogawa (Japan) upgraded their analyzers in 2024–2025 with enhanced protocol decoding (SPI, I2C, UART, CAN) and cloud-enabled data visualization

- The growing need for real-time testing, multi-device validation, and high-speed debugging is accelerating the shift toward compact, software-driven SME Force Automation systems

- As embedded electronics, IoT, and digital circuits continue to evolve, SME Force Automations remain critical for efficient development, testing, and validation of high-performance systems

What are the Key Drivers of SME Force Automation Market?

- Rising demand for affordable, accurate, and easy-to-use logic analyzers is fueling adoption across microcontroller, FPGA, and digital system development environments

- For instance, in 2025, leading companies such as Saleae (U.S.), Yokogawa (Japan), and Good Will Instrument (Taiwan) enhanced their product portfolios with higher sampling rates, advanced protocol decoding, and flexible software interfaces

- Widespread deployment of IoT devices, EV systems, robotics, consumer electronics, and smart automation solutions is boosting demand for digital signal acquisition and validation tools across North America, Europe, and Asia-Pacific

- Technological advancements in waveform compression, memory depth, high-speed sampling, and USB-powered architectures have improved portability, accuracy, and performance of analyzers

- Rising complexity of high-speed serial interfaces, AI chips, and mixed-signal communication protocols is increasing the need for multi-channel, high-resolution, portable SME Force Automation systems

- Sustained investment in semiconductor R&D, electronics testing infrastructure, and embedded system development supports long-term growth in the SME Force Automation market

Which Factor is Challenging the Growth of the SME Force Automation Market?

- High prices of premium, multi-channel, and high-bandwidth analyzers limit adoption among small engineering teams, startups, and academic labs

- For instance, during 2024–2025, component shortages, rising semiconductor costs, and long lead times increased production expenses for several global vendors

- Complexity in analyzing high-speed digital protocols, mixed-signal circuits, and timing sequences requires specialized technical expertise, limiting broader adoption

- Limited awareness of advanced analyzer features, protocol support, and debugging best practices in emerging regions slows market penetration

- Competition from digital oscilloscopes with built-in logic analyzer features, software debuggers, and protocol analyzers exerts pricing pressure and reduces differentiation

- To overcome these challenges, companies are focusing on cost-effective designs, enhanced software integration, cloud-based analytics, and comprehensive training programs to expand global adoption of SME Force Automation systems

How is the SME Force Automation Market Segmented?

The market is segmented on the basis of components, deployment, application, and end-use.

- By Components

On the basis of components, the SME force automation market is segmented into Solution and Services. The Solution segment dominated the market with a 62.3% share in 2025, driven by extensive adoption of CRM platforms, workflow automation tools, and integrated analytics solutions. Solutions enable companies to manage leads, track opportunities, and streamline sales pipelines, offering measurable improvements in productivity and operational efficiency. Cloud-connected and on-premise solutions provide real-time visibility, multi-device access, and enhanced collaboration across departments, reinforcing their market dominance.

The Services segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing demand for system integration, customization, maintenance, and professional consulting services. Organizations, particularly SMEs, are investing in expert support to optimize platform deployment, enhance user adoption, and integrate CRM with ERP, marketing automation, and analytics tools.

- By Deployment

On the basis of deployment, the market is segmented into Cloud and On-Premise. The Cloud segment dominated the market with a 54.6% share in 2025, supported by its low upfront costs, scalability, real-time updates, and remote accessibility. Cloud-based platforms allow multi-location teams to collaborate effectively, improve data centralization, and leverage AI-driven analytics for sales and customer insights. Organizations increasingly prefer SaaS offerings due to ease of integration, rapid deployment, and automatic software updates.

The On-Premise segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by industries requiring high data security, compliance with local regulations, and control over system customization. Large enterprises, BFSI, and healthcare organizations continue to adopt on-premise deployments to meet regulatory and privacy requirements while maintaining operational control.

- By Application

On the basis of application, the market is segmented into Lead Management, Sales Forecasting, Order & Invoices Management, Opportunity Management, and Others. The Lead Management segment dominated the market with a 38.1% share in 2025, fueled by the growing need to track, nurture, and convert prospects efficiently across multiple channels. Companies leverage automated lead scoring, email campaigns, and pipeline analytics to increase conversion rates and drive revenue growth.

The Sales Forecasting segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by demand for predictive analytics, AI-driven sales projections, and data-informed decision-making. Advanced forecasting tools enable sales teams to optimize resource allocation, anticipate market trends, and align strategies with revenue goals, enhancing competitive advantage.

- By End Use

On the basis of end-use, the SME force automation market is segmented into BFSI, Retail, Healthcare, IT & Telecom, Manufacturing, and Others. The BFSI segment dominated the market with a 32.7% share in 2025, driven by high adoption of CRM systems to manage client relationships, regulatory reporting, and digital banking solutions. Banking, insurance, and investment firms increasingly leverage automated workflows, AI insights, and customer segmentation to improve service quality and efficiency.

The Retail segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by the rapid adoption of digital sales tools, loyalty program management, omnichannel integration, and personalized customer engagement. Expanding e-commerce, high competition, and demand for superior customer experience are driving retailers to deploy advanced SME Force Automation solutions globally.

Which Region Holds the Largest Share of the SME Force Automation Market?

- North America dominated the SME force automation market with a 39.55% revenue share in 2025, driven by rapid adoption of CRM automation, sales acceleration platforms, and cloud-driven workflow solutions across the U.S. and Canada

- Strong growth in digital transformation, rising implementation of AI-enabled sales tools, and increasing investment in workforce automation continue to fuel market expansion. Enterprises across BFSI, retail, healthcare, IT & telecom, and manufacturing are integrating SME automation platforms to streamline pipelines, improve forecasting accuracy, enhance lead qualification, and reduce operational inefficiencies

- Leading companies in the region are launching advanced CRM suites with predictive analytics, automated lead scoring, omnichannel customer engagement, and cloud-native architectures, further strengthening North America’s technological leadership. High digital maturity, strong SaaS adoption, and sustained investment in enterprise IT modernization reinforce the region’s dominant position

U.S. SME Force Automation Market Insight

The U.S. is the largest contributor in North America, driven by strong adoption of cloud CRM systems, AI-powered sales automation tools, and advanced customer engagement platforms. Demand is further supported by growth in e-commerce, fintech, digital healthcare, and B2B technology sectors. Enterprises increasingly rely on automated workflows, predictive lead scoring, and integrated analytics to optimize sales cycles and enhance revenue performance. High concentration of software vendors, innovation hubs, and tech startups accelerates deployment across SMEs and large enterprises.

Canada SME Force Automation Market Insight

Canada contributes significantly to regional growth, supported by expanding digital transformation programs, rising adoption of cloud-based CRM systems, and growing investment in AI, fintech, and e-commerce ecosystems. SMEs and enterprises increasingly deploy automation tools for customer management, sales pipeline tracking, and omnichannel engagement. Government-supported digitization initiatives, strong IT infrastructure, and rising enterprise spending on cloud applications further accelerate adoption.

Asia-Pacific SME Force Automation Market

Asia-Pacific is projected to register the fastest CAGR of 8.6% from 2026 to 2033, driven by rapid digitization, expanding SME base, strong mobile-first business ecosystems, and increasing adoption of cloud CRM and sales automation platforms. High-volume sectors such as retail, BFSI, manufacturing, telecom, and e-commerce are accelerating deployment of automated sales tools to streamline operations and manage large customer datasets. Rising digital payments, SaaS adoption, and enterprise process automation across China, India, Japan, South Korea, and Southeast Asia continue to drive strong market growth.

China SME Force Automation Market Insight

China is the largest contributor to Asia-Pacific due to large-scale enterprise digitization, strong SaaS adoption, and extensive investments in e-commerce, fintech, and manufacturing automation. CRM and sales automation tools are increasingly used for customer lifecycle management, omnichannel marketing, and workflow automation. Government-backed digital economy initiatives and growth in cloud-native enterprises further support robust market expansion.

Japan SME Force Automation Market Insight

Japan shows stable growth supported by high enterprise IT adoption, strong demand for precision-driven sales tools, and modernization across retail, manufacturing, and telecom sectors. Companies rely on automation platforms to enhance forecasting accuracy, manage complex customer relationships, and improve operational efficiencies. Rising focus on AI-powered analytics and customer experience optimization fuels further adoption.

India SME Force Automation Market Insight

India is emerging as one of the fastest-growing markets due to rapid expansion of SMEs, increasing digital adoption, and government-backed initiatives such as Digital India and Make in India. High growth in SaaS startups, rising e-commerce penetration, and strong demand for lead management, workflow automation, and cloud CRM tools significantly boost market adoption across industries.

South Korea SME Force Automation Market Insight

South Korea contributes strongly due to high digital maturity, strong enterprise tech infrastructure, and rapid expansion of e-commerce, fintech, and electronics sectors. Companies increasingly adopt advanced automation platforms for customer analytics, sales optimization, and omnichannel engagement. Strong innovation ecosystems and tech-driven business models support sustained long-term growth.

Which are the Top Companies in SME Force Automation Market?

The SME force automation industry is primarily led by well-established companies, including:

- Salesforce.com, Inc. (U.S.)

- Microsoft (U.S.)

- SAP (Germany)

- Oracle (U.S.)

- Creatio (U.S.)

- Aptean (U.S.)

- Zoho Corporation Pvt. Ltd. (India)

- Infor (U.S.)

- CRMNEXT (India)

- SugarCRM (U.S.)

- Infusion Software, Inc. (U.S.)

- Pegasystems Inc. (U.S.)

- Trimble Inc. (U.S.)

- Accruent (U.S.)

- Acumatica, Inc. (U.S.)

- LeadSquared (India)

- Kloudq Technologies Limited (India)

- Nimap Infotech (India)

What are the Recent Developments in Global SME Force Automation Market?

- In November 2023, Salesforce introduced Service Intelligence, an advanced analytics application for Service Cloud aimed at enhancing agent productivity, reducing operational costs, and improving customer satisfaction. Powered by Data Cloud, it enables users to access real-time unified data directly within Service Cloud, eliminating the need to switch between multiple screens. This launch significantly strengthens Salesforce’s intelligent service management ecosystem

- In September 2023, Oracle Corporation unveiled the Fusion Data Intelligence Platform for its Oracle Fusion Cloud Application users, evolving from the Oracle Fusion Analytics Warehouse. The platform delivers business data-as-a-service with automated pipelines, 360-degree data models, interactive analytics, and integrated AI/ML capabilities. This development marks a major step forward in Oracle’s strategy to simplify enterprise data and analytics workflows

- In June 2023, Aptean Inc. announced the acquisition of TOTALogistix, a prominent provider of cloud-based transportation management systems (TMS) for manufacturers, retailers, and distributors across North America. This acquisition strengthens Aptean’s logistics and supply chain offerings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.