Global Soil Health Management Market

Market Size in USD Billion

USD

9.50 Billion

USD

17.71 Billion

2025

2033

USD

9.50 Billion

USD

17.71 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.50 Billion | |

| USD 17.71 Billion | |

| % | |

|

What is the Soil Health Management Market Size and Overview?

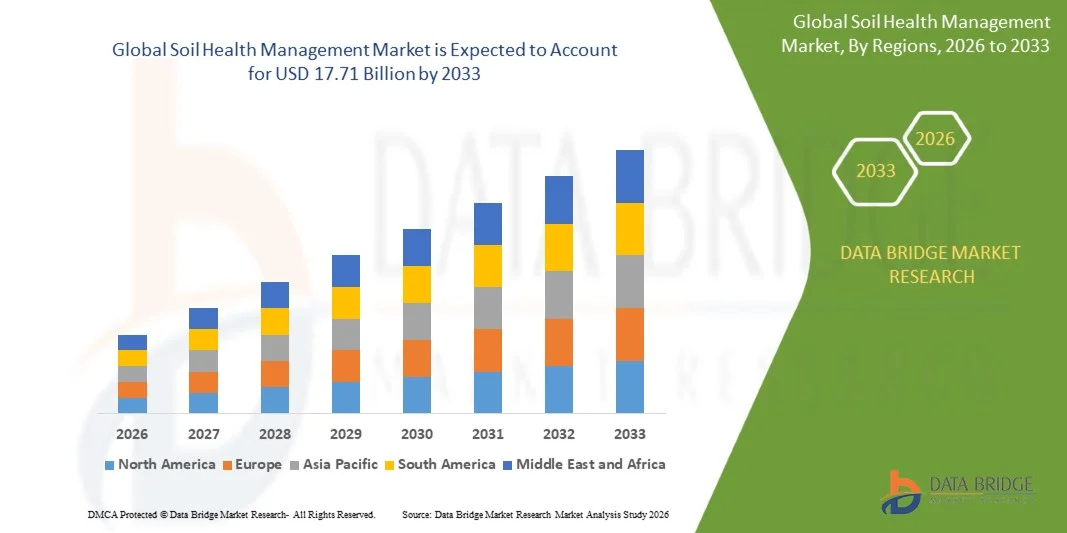

As per Data Bridge Market Research market analysis, the soil health management market was valued at USD 9.5 billion in 2025 and is expected to reach USD 17.71 billion by 2033, growing at a CAGR of 8.10% from 2025 to 2033. The market is witnessing significant expansion due to increasing concerns regarding soil degradation, nutrient depletion, declining soil fertility, and the global shift toward sustainable and regenerative agriculture. Increasing adoption of organic amendments, biological soil health products, precision agriculture technologies, and government initiatives promoting sustainable land management are further driving market growth.

Rapid population growth and increasing food demand have intensified pressure on agricultural land, making soil health management a critical component of global food security. Farmers and agricultural enterprises are increasingly adopting organic soil amendments, biofertilizers, microbial inoculants, soil conditioners, and precision soil monitoring technologies to improve nutrient availability, enhance water retention, restore soil biodiversity, and increase crop productivity while reducing environmental impacts.

Growing awareness regarding carbon sequestration, climate-smart agriculture, and sustainable land management has accelerated investments in digital agriculture solutions such as IoT-enabled soil sensors, artificial intelligence (AI)-based nutrient management systems, remote sensing technologies, and GIS-enabled soil mapping. These technologies enable farmers to optimize fertilizer application, reduce production costs, improve soil fertility, and achieve long-term sustainability.

Furthermore, favorable government policies supporting regenerative agriculture, increasing investments in precision farming technologies, expansion of organic farming, and rising adoption of biological crop inputs are expected to create substantial growth opportunities for market participants throughout the forecast period.

Market Size and Forecast

- Global Market Value (2026): USD 9.50 Billion

- Expected Market Value (2033): USD 17.71 Billion

- Forecast CAGR (2025–2033): 8.10%

- Leading Region: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends and Insights

- North America dominated the global soil health management market with the largest revenue share of 34.6% in 2024, supported by advanced agricultural practices, strong government initiatives, and widespread adoption of precision farming, soil testing, diagnostics, and bio-based inputs.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 12.5% during the forecast period, driven by rising agricultural production, increasing concerns regarding soil degradation, supportive government programs, and growing adoption of digital soil monitoring tools and biofertilizers across China, India, and Australia.

- The organic amendments segment led the market with a 37.6% revenue share in 2024, driven by increasing use of compost, manure, and biochar to improve soil structure, moisture retention, microbial activity, organic carbon content, and nutrient balance.

- The biological products segment is the fastest-growing product category, projected to register a CAGR of 12.4% during the forecast period, reflecting growing demand for biofertilizers, biostimulants, and microbial inoculants that improve nutrient uptake, restore microbial diversity, and reduce dependence on synthetic inputs.

- The agriculture segment dominated the application category with a 55.8% revenue share in 2024, supported by increasing use of soil testing, soil conditioners, biological products, and precision agriculture technologies to improve soil fertility, nutrient management, and crop productivity.

- The research and environmental monitoring segment is the fastest-growing application category, projected to register a CAGR of 13.7% from 2025 to 2033, driven by increasing assessment of soil composition, pollution levels, ecosystem health, carbon sequestration, and soil biodiversity.

Report Scope and Soil Health Management Market Segmentation

|

Attributes |

Soil Health Management Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Soil Health Management Market?

Trend: Rapid Adoption of Regenerative Agriculture and Biological Soil Health Solutions

The global agricultural sector is witnessing a significant transition from conventional input-intensive farming toward regenerative agriculture practices that prioritize long-term soil productivity, biodiversity conservation, and environmental sustainability. Farmers are increasingly adopting organic amendments, microbial inoculants, biofertilizers, compost, cover cropping, reduced tillage, and crop rotation practices to improve soil structure, increase microbial activity, enhance nutrient cycling, and reduce dependence on synthetic fertilizers. Governments across North America, Europe, and Asia-Pacific are supporting these practices through subsidy programs, carbon farming initiatives, and sustainable agriculture policies. Simultaneously, advancements in precision agriculture technologies—including AI-powered soil analytics, IoT-enabled sensors, satellite monitoring, and GIS-based soil mapping—are enabling farmers to make data-driven nutrient management decisions. These innovations are improving fertilizer use efficiency, increasing crop productivity, reducing greenhouse gas emissions, and strengthening long-term soil resilience, thereby driving sustained growth in the global Soil Health Management market.

Soil Health Management Market Dynamics

Key Market Driver: Rising Adoption of Sustainable and Regenerative Agriculture Practices

The increasing emphasis on sustainable agriculture and regenerative farming is one of the primary factors driving the global Soil Health Management market. Rapid population growth, climate change, soil degradation, and declining arable land have intensified the need for efficient soil management solutions that enhance productivity while preserving natural resources. According to the Food and Agriculture Organization (FAO), nearly one-third of the world's soils are moderately to highly degraded due to erosion, nutrient depletion, salinization, compaction, acidification, and chemical contamination. This has prompted governments, agricultural organizations, and farmers to adopt biological soil health products, organic amendments, precision nutrient management systems, and conservation agriculture practices.

Furthermore, increasing consumer preference for sustainably produced food has encouraged agricultural producers to minimize excessive chemical fertilizer usage and adopt environmentally friendly soil management practices. Precision agriculture technologies, including IoT-enabled soil sensors, artificial intelligence (AI), satellite imagery, GIS-based soil mapping, and digital nutrient management platforms, are enabling farmers to monitor soil conditions in real time and optimize fertilizer application, thereby improving crop productivity while reducing environmental impact. Government initiatives such as the European Green Deal, USDA Soil Health Initiative, India's Soil Health Card Scheme, and regenerative agriculture incentive programs are expected to further strengthen market growth throughout the forecast period.

Key Restraint/Challenge: High Cost of Precision Soil Monitoring Technologies and Limited Farmer Awareness

Despite increasing adoption, the Soil Health Management market continues to face several challenges, particularly in developing economies. The high initial investment associated with advanced soil monitoring technologies, including IoT-based soil sensors, GIS mapping systems, remote sensing equipment, drones, and AI-enabled farm management software, limits adoption among small and marginal farmers. Many agricultural producers continue to rely on conventional farming practices due to financial constraints, lack of technical expertise, and inadequate access to digital agricultural infrastructure.

In addition, limited awareness regarding soil biological health, improper fertilizer application practices, fragmented land holdings, and insufficient extension services continue to restrict the adoption of integrated soil health management practices. Variability in soil characteristics across regions further complicates implementation, requiring location-specific recommendations and continuous soil testing. These factors collectively present challenges to the widespread commercialization of advanced soil health management solutions, particularly across emerging agricultural economies.

Key Market Opportunity: Integration of Digital Agriculture and Carbon Farming Initiatives

The growing integration of digital agriculture technologies with soil health management presents significant opportunities for market expansion. Artificial intelligence, machine learning, remote sensing, blockchain-enabled traceability, cloud computing, and Internet of Things (IoT)-based soil monitoring systems are enabling precision nutrient management, predictive soil analytics, and real-time decision support for farmers. These technologies improve fertilizer efficiency, reduce operational costs, and enhance overall farm productivity.

Simultaneously, increasing global interest in carbon sequestration and carbon credit markets is creating new revenue opportunities for farmers adopting regenerative agricultural practices. Healthy soils play a critical role in storing atmospheric carbon, and governments are increasingly introducing carbon farming programs that financially reward sustainable land management practices. Private organizations and food companies are also investing in regenerative agriculture initiatives to achieve climate commitments and improve supply chain sustainability. These developments are expected to accelerate investments in biological soil amendments, microbial products, precision agriculture technologies, and digital farm management platforms over the coming decade.

Soil Health Management Market Scope

The soil health management market is segmented on the basis of product type, technology type, application type, end user type, distribution channel type, deployment type.

- By Product Type

On the basis of product type, the soil health management market is segmented into organic amendments, biofertilizers, soil conditioners, specialty fertilizers, soil testing and diagnostic products, and biological soil health products. Organic amendments dominated with a 37.6% share in 2024 due to their role in improving soil structure and nutrient availability. Biofertilizers support nutrient uptake through beneficial microorganisms, while Soil Conditioners improve moisture retention and physical soil properties. Specialty Fertilizers provide targeted and efficient nutrient delivery, whereas Soil testing and diagnostic products help assess nutrient levels, pH, and overall soil condition. Biological soil health products are expected to grow fastest at a CAGR of 12.4%, supported by rising demand for microbial and bio-based solutions.

- By Technology

On the basis of technology, the market is segmented into precision agriculture, AI-based soil analytics, GIS, remote sensing, and IoT-enabled soil monitoring. Precision Agriculture improves fertilizer and irrigation efficiency using field data. AI-based soil analytics helps predict nutrient needs and identify soil risks, while GIS supports mapping of soil variations across farms. Remote Sensing monitors soil and crop conditions over large areas, whereas IoT-enabled soil monitoring provides real-time data on moisture, temperature, and other soil parameters.

- By End User

On the basis of end user, the market is segmented into farmers, commercial farms, agricultural cooperatives, government agencies, and research institutions and universities. Farmers use soil products and testing services to improve productivity and control input costs. Commercial farms increasingly adopt advanced digital and precision technologies, while agricultural cooperatives improve access to products, testing, and technical services. Government agencies support soil conservation and land management programs, whereas Research Institutions and Universities focus on soil research, technology development, and field validation.

- By Application

On the basis of application, the market is segmented into agriculture, horticulture, forestry, turf and landscaping, and environmental restoration. Agriculture dominated with a 55.8% revenue share in 2024, driven by widespread demand for soil fertility and crop productivity solutions. Horticulture requires precise nutrient and moisture management for high-value crops, while Forestry focuses on long-term soil quality and ecosystem health. Turf and Landscaping uses soil products for maintaining sports fields, parks, and gardens, whereas environmental restoration supports degraded land recovery, biodiversity improvement, and soil rehabilitation.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct sales, agricultural distributors, cooperatives, and online platforms. Direct sales mainly serve large farms and institutional customers requiring customized solutions. Agricultural Distributors remain important due to their established local networks and technical support. Cooperatives provide collective access to products and services, while Online Platforms are gaining adoption by offering convenient access to soil management products and information.

- By Deployment

On the basis of deployment, the market is segmented into on-premise digital platforms and cloud-based farm management platforms. On-premise digital platforms are preferred by large farms and institutions requiring greater control over data and internal systems. Cloud-based farm management platforms are expected to lead and grow faster, supported by remote accessibility, scalability, lower infrastructure requirements, and integration with IoT sensors and satellite technologies.

Soil Health Management Market Regional Analysis

North America dominated the global soil health management market with a 34.6% revenue share in 2024, supported by advanced agricultural practices, strong soil testing infrastructure, and widespread adoption of precision farming and bio-based inputs. The U.S. leads the region, while government programs promoting regenerative agriculture, cover cropping, nutrient management, and rotational grazing are further supporting market growth across the U.S. and Canada.

U.S. Soil Health Management Market Trends

The U.S. leads the North America soil health management industry, supported by strong federal programs, such as the USDA’s conservation initiatives, and the widespread adoption of precision agriculture. The presence of major agritech companies and active soil research networks ensures continuous innovation in soil testing, biologicals, and sustainable inputs.

Asia Pacific Soil Health Management Market Trends

The Asia Pacific soil health management industry is expected to grow at the fastest CAGR of 12.5% during the forecast period. This growth is fueled by rising agricultural output, challenges related to soil degradation, and supportive government programs. Nations such as China, India, and Australia are implementing large-scale soil rejuvenation initiatives and promoting the use of organic amendments. Rapid adoption of digital soil monitoring tools and biofertilizers is further strengthening market growth across the region.

China soil health management market is expected to grow during the forecast period. China plays a central role in the Asia Pacific market, with its growth driven by large-scale agricultural production and government-backed soil fertility improvement programs. National initiatives focused on restoring organic matter and reducing synthetic fertilizer use are driving strong demand for biofertilizers and organic amendments.

Europe Soil Health Management Market Trends

Europe’s growth is supported by stringent environmental regulations and policy frameworks that promote sustainable land use. The European Union’s Green Deal and Common Agricultural Policy (CAP) emphasize the conservation of soil fertility and reduced chemical dependency. Countries such as Germany, France, and the Netherlands are leading adopters of biological soil enhancers and monitoring technologies, driving steady regional growth.

The Germany soil health management market is at the forefront of Europe’s soil health management efforts, emphasizing sustainable farming and technological innovation. The country’s advanced research ecosystem and strict environmental regulations promote the adoption of soil testing, microbial products, and organic soil conditioners. Germany’s focus on carbon sequestration and regenerative agriculture continues to shape market growth.

Latin America Soil Health Management Market Trends

Latin America is an emerging market with moderate growth, driven by expanding agricultural production and increasing awareness of soil fertility management. Brazil and Argentina are key contributors, with initiatives promoting soil conservation and reduced reliance on chemical inputs. The growing adoption of sustainable farming and crop rotation practices is expected to gradually boost demand for biological and organic soil health products.

Middle East and Africa Soil Health Management Market

The Middle East and Africa showcase steady demand, with growing interest in soil health management due to challenges such as soil salinity, arid conditions, and desertification. Countries like Saudi Arabia, the UAE, and South Africa are investing in soil remediation, water conservation, and controlled-environment agriculture. Government-led sustainability programs and partnerships with international agritech firms are helping strengthen market development in this region.

Which are the Top Companies in Soil Health Management Market?

The soil health management industry is primarily led by well-established companies, including:

- Syngenta AG (Switzerland)

- Corteva Agriscience (U.S.)

- Nutrien Ltd. (Canada)

- Yara International ASA (Norway)

- UPL Limited (India)

- FMC Corporation (U.S.)

- Novonesis A/S (Denmark)

- Koppert Biological Systems (Netherlands)

- ICL Group Ltd. (Israel)

- Haifa Group (Israel)

- Bioceres Crop Solutions Corp. (Argentina)

- Indigo Ag Inc. (U.S.)

- Pivot Bio Inc. (U.S.)

- Lallemand Plant Care (Canada)

- Rizobacter Argentina S.A. (Argentina)

- Eurofins Agro Testing (Netherlands)

- SGS SA (Switzerland)

- ALS Limited (Australia)

- The Mosaic Company (U.S.)

- K+S AG (Germany)

- Coromandel International Ltd. (India)

- National Fertilizers Limited (India)

Latest Developments in Market

- In May 2026, BASF Agricultural Solutions commissioned its new BioHub fermentation facility in Ludwigshafen, expanding the company’s production capacity for biological and biotechnology-based agricultural solutions. The high double-digit million-euro investment supports commercial production of biological fungicides and biological seed treatments, including products based on beneficial microorganisms. The facility also strengthens production flexibility and supply chain resilience while supporting the wider use of biological solutions in sustainable and integrated crop management. This development reflects the growing industry shift toward scalable biological technologies that can support healthier and more resilient agricultural systems.

- In January 2026, Indigo Ag entered into a 12-year agreement with Microsoft for the purchase of 2.85 million soil carbon removal credits, representing one of the largest soil carbon transactions announced to date. The credits will be generated through Indigo’s regenerative agriculture program, which supports practices that improve soil health, crop resilience, water infiltration, and carbon storage across millions of U.S. acres. The agreement also uses remote sensing, machine learning, and advanced soil carbon modelling to improve measurement and verification. This development highlights the increasing commercial value of soil health improvement and regenerative land management.

- In August 2025, Biome Makers partnered with Midwest Laboratories to expand access to microbiome-based soil intelligence across the U.S. Under the partnership, Midwest Laboratories began offering the BeCrop Test alongside traditional soil chemistry analysis, enabling growers to assess microbial activity and biological soil functions. The technology uses next-generation DNA sequencing to provide information on nutrient bioavailability, bacteria-to-fungi ratios, disease risks, and overall soil health. This collaboration strengthens the integration of biological diagnostics with conventional soil testing and supports more precise soil and input management decisions.

- In March 2025, Pivot Bio unveiled PROVEN G3, its third-generation microbial nitrogen solution for corn, combining proprietary gene-edited nitrogen-fixing technology with an additional microbial blend designed to improve nutrient uptake and nitrogen-use efficiency. The product is designed to complement existing fertility programs and help crops obtain nitrogen more efficiently under different soil and field conditions. Pivot Bio also announced a large-scale demonstration program across more than 300 locations to evaluate the technology under commercial farming conditions. This launch reflects growing investment in microbial solutions for more efficient nutrient and soil fertility management.

- In February 2025, Syngenta and Ceres Biotics signed a global agreement to expand farmer access to VIXERAN, a microbial biostimulant designed to improve nitrogen-use efficiency. The solution is based on the beneficial bacterium Azotobacter salinestris and helps plants access nitrogen from the environment through both leaves and roots while complementing conventional fertilizer programs. The partnership aims to introduce the technology into additional global markets and support more sustainable nutrient management practices. This development strengthens the role of microbial biostimulants in improving crop productivity, nutrient efficiency, and soil health.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.