Global Solar Cell Paste Market

Market Size in USD Billion

USD

8.88 Billion

USD

55.06 Billion

2025

2033

USD

8.88 Billion

USD

55.06 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.88 Billion | |

| USD 55.06 Billion | |

| % | |

|

Solar Cell Paste Market Overview

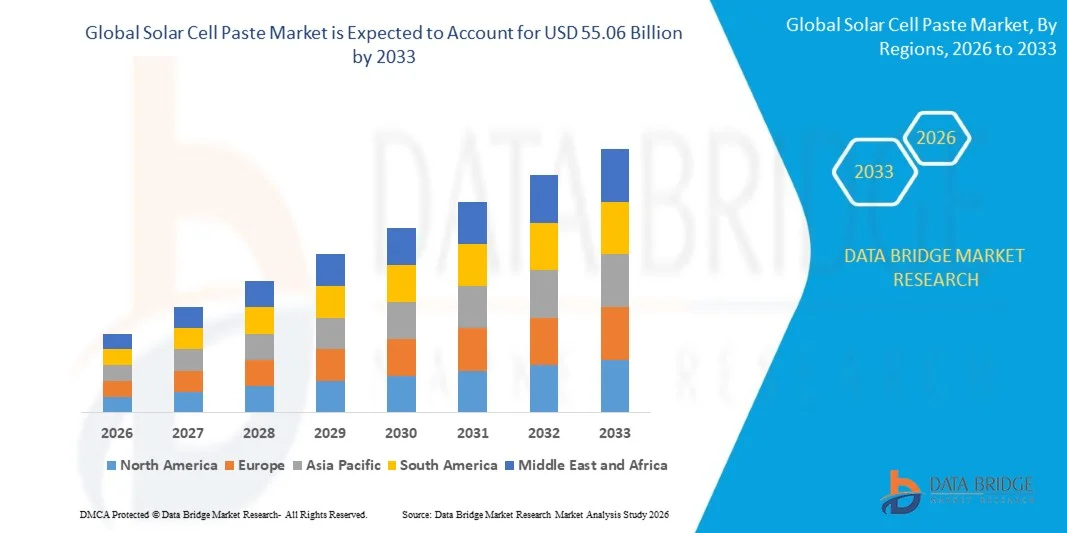

The Solar Cell Paste Market was valued at USD 8.88 Billion in 2025 and is projected to reach USD 55.06 Billion by 2033, growing at a CAGR of 25.62% from 2026 to 2033. The market is experiencing consistent growth driven by increasing global solar photovoltaic installations, rising demand for high-efficiency solar cells, and expanding investments in renewable energy infrastructure. Growing adoption of advanced solar technologies such as TOPCon, HJT, and bifacial solar cells, along with continuous innovations in conductive paste formulations, is further supporting market expansion across major photovoltaic manufacturing regions.

The increasing global focus on clean energy generation and carbon reduction targets, combined with supportive government policies promoting solar energy deployment, is accelerating demand for solar cell paste materials. High-performance silver and aluminum pastes play a critical role in improving electrical conductivity, conversion efficiency, and long-term reliability of photovoltaic cells. Solar manufacturers are increasingly investing in advanced metallization technologies to enhance cell performance while reducing material consumption and production costs, further driving market growth.

Key Market Trends & Insights

- Asia-Pacific dominated the Solar Cell Paste Market with the largest revenue share of 62.8% in 2025, supported by the region’s strong photovoltaic manufacturing base, large-scale solar module production, and extensive investments in renewable energy infrastructure

- The monocrystalline solar cell segment led the market with a 67.4% share in 2025, driven by the global transition toward high-efficiency solar energy systems

- North America is expected to be the fastest-growing region at a CAGR of 6.8% from 2026 to 2033, fueled by increasing investments in domestic solar manufacturing, rising deployment of utility-scale photovoltaic projects, and supportive clean energy policies

- Polycrystalline solar cell is the fastest-growing application type, projected to register a CAGR of 13.5% from 2026 to 2033, supported by increasing demand for cost-effective solar power solutions across emerging economies and large-scale utility projects

- The front side silver paste segment dominated the type category with a 48.7% revenue share in 2025, led by its critical role in forming conductive gridlines that directly influence solar cell efficiency and power output

- The back-side silver solar cell paste segment is the fastest-growing type category, with a CAGR of 12.8% from 2026 to 2033, driven by increasing adoption of high-efficiency cell technologies such as TOPCon and heterojunction solar cells

Market Size & Forecast

- Global Market Value (2025): USD 8.88 Billion

- Expected Market Value (2033): USD 55.06 Billion

- Forecast CAGR (2026–2033): 25.62%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Solar Cell Paste Market Segmentation

|

Attributes |

Solar Cell Paste Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Toyo Aluminium K.K. (Japan) · ANP Co., Ltd. (South Korea) · Samsung Electronics Co., Ltd. (South Korea) · Daejoo Electronic Materials Co., Ltd. (South Korea) · Targray Technology International Inc. (Canada) · NAMICS Corporation (Japan) · Giga Solar Materials Corp. (Taiwan) · Noritake Co., Limited (Japan) · Heraeus Holding GmbH (Germany) · DuPont de Nemours, Inc. (U.S.) · Murata Manufacturing Co., Ltd. (Japan) · Thintech Limited (Taiwan) · Deere & Company (U.S.) · Monocrystal LLC (Russia) · XO Global LLC (U.S.) · Cermet Resistronics Pvt. Ltd. (India) · Changzhou EGing Photovoltaic Technology Co., Ltd. (China) · Jiangsu Hoyi Technology Co., Ltd. (China) |

|

Market Opportunities |

· Expansion of TOPCon and Heterojunction Solar Cell Manufacturing · Increasing Commercialization of Copper-Based Conductive Paste Solutions · Growth of Domestic Solar Manufacturing Capacity Across Emerging Economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Solar Cell Paste Market Trends

Trend: Growing Adoption of Low-Silver and Silver-Free Metallization Technologies

Solar cell manufacturers are increasingly adopting low-silver and alternative metallization technologies to reduce production costs and improve supply chain resilience amid fluctuating silver prices. The industry is witnessing a transition toward copper-based conductive pastes, copper plating technologies, and advanced low-silver formulations, particularly in TOPCon and heterojunction solar cell production. Continuous innovation in paste chemistry is helping manufacturers maintain conductivity and efficiency while lowering precious metal consumption. This trend is becoming increasingly important as global photovoltaic deployment scales and material cost optimization remains a key competitive factor.

Companies such as Daejoo Electronic Materials Co., Ltd. launched mass production of high-copper paste products in October 2025, while Aiko Solar confirmed copper plating deployment on a 5 GW production line in July 2025, highlighting the industry's shift toward reduced silver consumption and next-generation metallization technologies.

Solar Cell Paste Market Dynamics

Key Market Driver: Rising Global Deployment of High-Efficiency Solar Photovoltaic Systems

The rapid expansion of solar energy installations worldwide is significantly driving demand for advanced solar cell paste materials. High-efficiency photovoltaic technologies such as TOPCon, heterojunction (HJT), and bifacial solar cells require specialized conductive pastes to maximize electrical performance, conversion efficiency, and long-term reliability. Governments across major economies are accelerating renewable energy deployment through supportive policies, incentives, and clean energy targets, increasing demand for high-performance solar manufacturing materials. Growing investments in utility-scale solar projects and domestic photovoltaic manufacturing are further strengthening market growth.

According to the International Energy Agency, global renewable capacity additions reached record levels in recent years, with solar photovoltaics accounting for the largest share of new power generation capacity. Companies such as JinkoSolar, LONGi Green Energy Technology, and Trina Solar continue expanding high-efficiency TOPCon cell production, directly supporting demand for advanced solar cell paste products.

Key Restraint/Challenge: Volatility in Silver Prices and Raw Material Supply Constraints

A major challenge in the Solar Cell Paste market is the volatility of silver prices and the increasing cost pressure associated with precious metal consumption. Silver remains a critical raw material for front-side and back-side conductive pastes used in photovoltaic cells, making manufacturers vulnerable to fluctuations in commodity markets. Rising global solar deployment is increasing silver demand, creating concerns regarding long-term supply availability and production economics. Manufacturers must continuously balance efficiency improvements with material cost reductions, which can impact profitability and product pricing.

The September 2024 launch of the PV6NL low solid-content rear silver paste by Solamet Electronic Materials demonstrated the industry's efforts to reduce silver consumption by approximately 5% to 10% per cell while maintaining performance standards, reflecting the growing challenge of managing raw material costs within photovoltaic manufacturing.

Key Market Opportunity: Expansion of TOPCon and Heterojunction Solar Cell Manufacturing

The rapid expansion of TOPCon and heterojunction solar cell manufacturing is creating significant growth opportunities for the Solar Cell Paste market. These advanced photovoltaic technologies require highly specialized metallization materials capable of delivering superior conductivity, lower resistive losses, and improved cell efficiency. Increasing investments in next-generation solar manufacturing facilities across Asia-Pacific, Europe, and North America are accelerating demand for premium silver, copper, and hybrid conductive paste solutions. Ongoing technological advancements are also enabling development of customized paste formulations tailored for emerging high-efficiency cell architectures.

Companies such as LONGi Green Energy Technology, JinkoSolar, and Canadian Solar are expanding TOPCon and advanced n-type solar cell production capacities, while the June 2025 acquisition of a majority stake in Solamet Electronic Materials by Wuxi DK Electronic Materials Co., Ltd. further strengthened research and development capabilities for metallization solutions supporting next-generation photovoltaic technologies.

Solar Cell Paste Market Scope

The solar cell paste market is segmented on the basis of type and application.

- By Type

On the basis of type, the Solar Cell Paste Market is segmented into Front Side Silver Paste, Rear Side Silver Paste, Aluminum Paste, and Back-Side Silver Solar Cell Paste. The Front Side Silver Paste segment dominated the market with the largest share of 48.7% in 2025, driven by its critical role in forming conductive gridlines that directly influence solar cell efficiency and power output. The segment benefits from widespread adoption across high-efficiency photovoltaic technologies, particularly monocrystalline and advanced cell architectures. Continuous advancements in silver paste formulations have improved conductivity while reducing material consumption. Growing investments in premium solar modules and higher conversion efficiency targets further support demand. Strong deployment of utility-scale and commercial solar projects reinforces the segment’s leading position globally.

The Back-Side Silver Solar Cell Paste segment is projected to register the fastest growth at a CAGR of 12.8% from 2026 to 2033, driven by increasing adoption of high-efficiency cell technologies such as TOPCon and heterojunction solar cells. These advanced solar cell designs require enhanced rear-side electrical conductivity and optimized current collection performance. Rising demand for bifacial modules is creating significant opportunities for specialized back-side silver paste applications. Technological innovations focused on improving cell efficiency and durability are further accelerating market penetration. Expanding manufacturing capacities for next-generation photovoltaic modules across Asia-Pacific, Europe, and North America continue to support rapid segment growth.

- By Application

On the basis of application, the Solar Cell Paste Market is segmented into Monocrystalline Solar Cell and Polycrystalline Solar Cell. The Monocrystalline Solar Cell segment dominated the market with the largest share of 67.4% in 2025, driven by the global transition toward high-efficiency solar energy systems. Monocrystalline cells require advanced paste materials to maximize conductivity, reduce energy losses, and enhance overall conversion efficiency. The segment benefits from strong deployment in utility-scale, commercial, and residential solar installations where performance optimization is a key priority. Continuous improvements in cell technologies, including TOPCon and PERC, have further increased demand for specialized solar cell pastes. Growing investments in premium photovoltaic manufacturing strengthen the segment’s market leadership.

The Polycrystalline Solar Cell segment is also projected to register the fastest growth at a CAGR of 13.5% from 2026 to 2033, driven by increasing demand for cost-effective solar power solutions across emerging economies and large-scale utility projects. Polycrystalline solar cells offer a favorable balance between performance and manufacturing cost, making them suitable for price-sensitive markets. Expanding solar installation programs in developing regions are supporting adoption. Continuous improvements in cell efficiency and production technologies are enhancing competitiveness. Growing investments in renewable energy infrastructure and rising electricity demand are expected to accelerate segment growth during the forecast period.

Solar Cell Paste Market Regional Analysis

Asia-Pacific dominated the solar cell paste market and accounted for the largest revenue share of 62.8% in 2025, supported by the region’s strong photovoltaic manufacturing base, large-scale solar module production, and extensive investments in renewable energy infrastructure. The region benefits from the presence of leading solar cell manufacturers, well-established supply chains for photovoltaic materials, and cost-effective production capabilities. Rising installation of utility-scale solar projects, increasing government incentives for clean energy adoption, and growing demand for high-efficiency solar modules are accelerating regional market expansion. Continuous capacity additions in solar cell manufacturing and advancements in next-generation photovoltaic technologies further strengthen the region’s leadership.

China Solar Cell Paste Market Insight

China held the largest share in the Asia-Pacific Solar Cell Paste market in 2025, supported by its dominant position in global solar cell and photovoltaic module manufacturing. The country has a highly integrated solar supply chain that supports large-scale production of silver and aluminum pastes required for advanced solar cell technologies. Strong investments in TOPCon, heterojunction, and bifacial solar cell manufacturing are further driving demand for high-performance paste materials. In addition, expanding domestic solar installations and significant export activities across global photovoltaic markets are reinforcing China's leadership position.

India Solar Cell Paste Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by expanding solar power generation capacity, increasing domestic photovoltaic manufacturing initiatives, and supportive government policies promoting renewable energy self-sufficiency. Rising investments in solar parks, rooftop solar systems, and utility-scale renewable projects are significantly increasing demand for solar cell materials. The country is also benefiting from production-linked incentive programs aimed at strengthening local solar manufacturing capabilities. In addition, growing focus on energy security and clean energy transition is accelerating long-term market growth.

Europe Solar Cell Paste Market Insight

The Europe Solar Cell Paste market is expanding steadily, supported by increasing investments in renewable energy projects, growing adoption of high-efficiency photovoltaic technologies, and strong decarbonization targets across the region. Rising demand for locally manufactured solar components and increasing emphasis on energy independence are strengthening regional market development. Solar module manufacturers are increasingly focusing on advanced cell architectures that require specialized conductive paste materials. In addition, favorable government policies and expanding solar deployment programs are supporting sustained market growth.

Germany Solar Cell Paste Market Insight

Germany accounted for the largest share in the Europe Solar Cell Paste market in 2025, driven by its advanced solar energy sector, strong photovoltaic research capabilities, and growing deployment of high-efficiency solar installations. The country benefits from extensive adoption of premium solar technologies that require advanced silver and conductive paste formulations. Strong investments in renewable energy infrastructure and increasing modernization of solar manufacturing facilities are further supporting demand. In addition, supportive regulatory frameworks and sustainability initiatives continue to reinforce Germany’s leading market position.

U.K. Solar Cell Paste Market Insight

The U.K. market is supported by increasing solar energy deployment, rising investments in renewable electricity generation, and growing demand for efficient photovoltaic technologies. Expanding commercial and residential solar installations are contributing to higher consumption of advanced solar cell materials. The country is also witnessing growing interest in energy transition initiatives and carbon reduction strategies, which are supporting market development. In addition, increasing investment in domestic clean energy infrastructure is further accelerating growth.

North America Solar Cell Paste Market Insight

North America is projected to grow at the fastest CAGR of 6.8% from 2026 to 2033, driven by increasing investments in domestic solar manufacturing, rising deployment of utility-scale photovoltaic projects, and supportive clean energy policies. Growing efforts to strengthen regional solar supply chains and reduce dependence on imported solar components are significantly supporting market expansion. Demand for advanced solar cell technologies with higher energy conversion efficiency is further accelerating adoption of premium conductive paste materials. In addition, expanding government incentives and corporate renewable energy commitments are boosting regional market growth.

U.S. Solar Cell Paste Market Insight

The U.S. accounted for the largest share in the North America Solar Cell Paste market in 2025, supported by strong investments in solar energy infrastructure, increasing domestic photovoltaic manufacturing capacity, and growing adoption of high-efficiency solar technologies. The country benefits from expanding utility-scale solar projects and favorable policy initiatives encouraging clean energy deployment. Rising focus on advanced solar cell architectures and local production of photovoltaic components is further strengthening demand for specialized paste materials. In addition, increasing public and private sector investments in renewable energy are reinforcing the U.S. leadership position in the regional market.

Solar Cell Paste Market Share

The solar cell paste industry is primarily led by well-established companies, including:

- Toyo Aluminium K.K. (Japan)

- ANP Co., Ltd. (South Korea)

- Samsung Electronics Co., Ltd. (South Korea)

- Daejoo Electronic Materials Co., Ltd. (South Korea)

- Targray Technology International Inc. (Canada)

- NAMICS Corporation (Japan)

- Giga Solar Materials Corp. (Taiwan)

- Noritake Co., Limited (Japan)

- Heraeus Holding GmbH (Germany)

- DuPont de Nemours, Inc. (U.S.)

- Murata Manufacturing Co., Ltd. (Japan)

- Thintech Limited (Taiwan)

- Deere & Company (U.S.)

- Monocrystal LLC (Russia)

- XO Global LLC (U.S.)

- Cermet Resistronics Pvt. Ltd. (India)

- Changzhou EGing Photovoltaic Technology Co., Ltd. (China)

- Jiangsu Hoyi Technology Co., Ltd. (China)

Latest Developments in Solar Cell Paste Market

- In October 2025, DK Electronic Materials commenced mass production of its newly developed high-copper paste products, strengthening the transition of the Solar Cell Paste market toward low-silver and silver-free metallization technologies. The products successfully passed validation with major solar cell manufacturers and demonstrated compatibility with advanced TOPCon 3.0 cell architectures. The establishment of gigawatt-scale manufacturing lines enhanced commercial readiness and is expected to accelerate industry-wide adoption of cost-efficient conductive paste solutions while reducing dependence on expensive silver materials

- In July 2025, Aiko Solar confirmed the rollout of copper plating technology on a 5 GW production line, significantly influencing the evolution of metallization processes within the Solar Cell Paste market. The initiative is targeted to reduce rear-side paste consumption by nearly 90% by mid-2026, supporting lower manufacturing costs and improved resource efficiency. This advancement is expected to encourage wider adoption of alternative metallization technologies and reshape demand patterns for traditional silver paste products

- In June 2025, Wuxi DK Electronic Materials Co., Ltd. acquired a 60% equity stake in Solamet Electronic Materials for CNY 696 million, enhancing consolidation within the Solar Cell Paste market. The acquisition combined Solamet’s intellectual property portfolio and global customer relationships with DKEM’s manufacturing expertise, strengthening innovation capabilities in silver paste solutions for TOPCon and HJT solar cells. The transaction is expected to improve technological competitiveness and support the development of advanced metallization materials amid increasing industry margin pressures

- In January 2025, LPKF Laser & Electronics SE collaborated with Fraunhofer Institute for Solar Energy Systems to develop an advanced metallization process utilizing Laser Induced Deep Etching (LIDE) technology. The breakthrough enabled the printing of ultra-fine contact fingers below 10 micrometers, reducing shading losses and lowering silver paste consumption in photovoltaic cells. This innovation supports the market’s focus on improving solar cell efficiency while advancing material optimization and sustainability objectives

- In September 2024, Solamet Electronic Materials launched the PV6NL series of low solid-content rear silver pastes for TOPCon solar cells, contributing to cost optimization across the Solar Cell Paste market. The new formulation reduced rear-side silver consumption by approximately 5% to 10% per cell while maintaining conductivity and adhesion performance. The product also improved cell efficiency, helping manufacturers enhance the economic viability and competitiveness of next-generation n-type solar technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Solar Cell Paste Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Solar Cell Paste Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Solar Cell Paste Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.