Global Solid Organ Transplantation Market

Market Size in USD Billion

CAGR :

%

USD

7.88 Billion

USD

11.55 Billion

2025

2033

USD

7.88 Billion

USD

11.55 Billion

2025

2033

| 2026 –2033 | |

| USD 7.88 Billion | |

| USD 11.55 Billion | |

| % | |

|

Solid Organ Transplantation Market Size

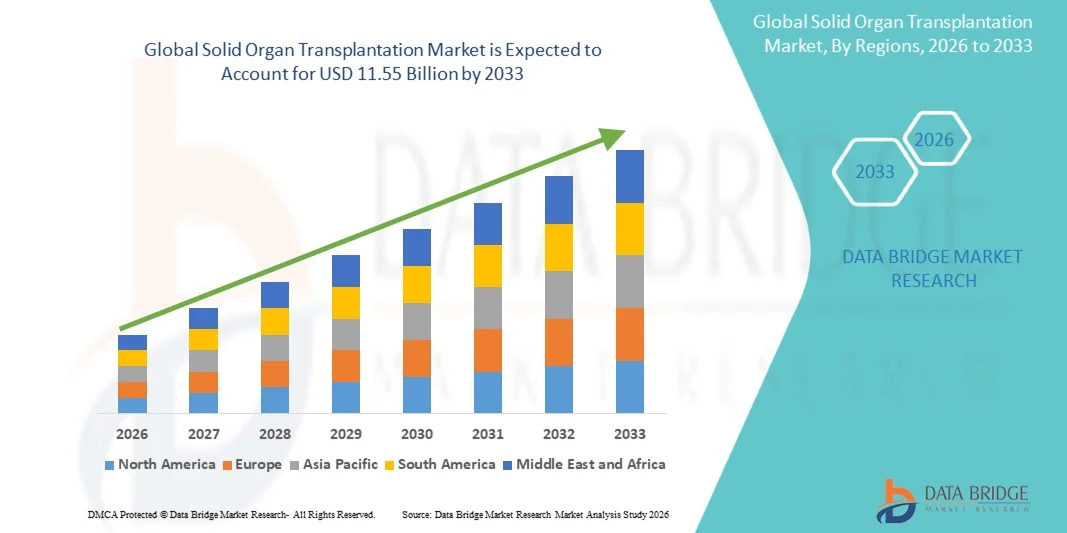

- The global solid organ transplantation market size was valued at USD 7.88 billion in 2025 and is expected to reach USD 11.55 billion by 2033, at a CAGR of 4.90% during the forecast period

- The market growth is largely fueled by the rising prevalence of end-stage organ failure, increasing chronic disease burden, and continuous technological progress in transplant procedures and organ preservation systems, leading to improved treatment outcomes across hospitals and specialty healthcare centers

- Furthermore, growing demand for life-saving treatment options, rising adoption of advanced immunosuppressive therapies, and increasing investments in healthcare infrastructure are establishing Solid Organ Transplantation solutions as a critical component of modern healthcare systems. These converging factors are accelerating the uptake of Solid Organ Transplantation solutions, thereby significantly boosting the industry's growth

Solid Organ Transplantation Market Analysis

- Solid Organ Transplantation solutions, including transplant procedures, organ preservation systems, immunosuppressive therapies, and post-transplant monitoring services, are increasingly vital components of modern healthcare systems across hospitals and specialty transplant centers due to their critical role in treating end-stage organ failure and improving patient survival outcomes

- The escalating demand for Solid Organ Transplantation solutions is primarily fueled by the rising prevalence of chronic kidney disease, liver cirrhosis, heart failure, diabetes-related complications, and growing awareness regarding advanced life-saving treatment options, along with improvements in donor management and surgical success rates

- North America dominated the solid organ transplantation market with the largest revenue share of approximately 41.8% in 2025, characterized by advanced healthcare infrastructure, favorable reimbursement systems, high transplant procedure volumes, and the presence of major industry players, with the U.S. experiencing substantial growth in kidney, liver, heart, and lung transplantation supported by technological innovations and strong organ donation networks

- Asia-Pacific is expected to be the fastest growing region in the solid organ transplantation market during the forecast period due to expanding healthcare infrastructure, rising disposable incomes, growing chronic disease burden, increasing medical tourism, and improving awareness regarding organ donation across China, India, Japan, South Korea, and Southeast Asia

- The immunosuppressive segment accounted for the largest market revenue share of 64.2% in 2025, driven by its foundational role in preventing acute and chronic graft rejection after transplantation

Report Scope and Solid Organ Transplantation Market Segmentation

|

Attributes |

Solid Organ Transplantation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Solid Organ Transplantation Market Trends

“Enhanced Clinical Outcomes Through AI Integration and Advanced Organ Preservation Technologies”

- A significant and accelerating trend in the global solid organ transplantation market is the growing adoption of artificial intelligence (AI), digital transplant monitoring tools, and advanced organ preservation systems to improve donor-recipient matching, surgical outcomes, and post-transplant care. These innovations are enhancing efficiency across the transplant value chain

- AI-powered analytics are increasingly being used to optimize donor organ allocation, predict rejection risks, and support transplant decision-making based on clinical data

- For instance, transplant centers in the U.S. and Europe are using AI-assisted matching models to improve compatibility assessments for kidney and liver transplantation candidates

- The increasing use of machine perfusion and next-generation organ preservation technologies is also transforming transplantation by extending organ viability and improving utilization rates of marginal donor organs

- Another important trend is the rising adoption of remote patient monitoring and digital adherence tools for post-transplant recipients, enabling clinicians to track vital signs, immunosuppressant compliance, and early complications. For instance, leading hospitals are deploying mobile transplant care platforms to monitor kidney and heart transplant patients after discharge

- In addition, ongoing advancements in xenotransplantation research, regenerative medicine, and bioengineered organs are creating long-term opportunities to address donor shortages globally

- This shift toward intelligent, technology-enabled, and outcome-focused transplant care is fundamentally reshaping expectations in organ replacement therapy and driving demand for innovative solutions

Solid Organ Transplantation Market Dynamics

Driver

“Rising Organ Failure Cases and Expanding Transplant Infrastructure”

- The increasing prevalence of end-stage organ failure caused by chronic kidney disease, liver cirrhosis, heart failure, and lung disorders is a major driver for the Solid Organ Transplantation market. Growing disease burden is significantly increasing demand for life-saving transplant procedures worldwide

- Expanding transplant programs, improved surgical success rates, and better reimbursement support are further accelerating market growth

- For instance, countries such as the U.S., Spain, India, and Saudi Arabia are investing in national transplant networks and donor awareness programs to increase procedure volumes

- Advancements in immunosuppressive therapies have also improved long-term graft survival, making transplantation a more viable treatment option for many patients

- Furthermore, rising awareness regarding organ donation and increasing use of deceased donor registries are helping expand donor pools in several markets

- The continued modernization of hospitals, transplant centers, and critical care infrastructure is expected to sustain market expansion over the forecast period

Restraint/Challenge

“Donor Shortage, High Procedure Costs, and Rejection Risks”

- One of the major challenges restraining the Solid Organ Transplantation market is the persistent shortage of donor organs relative to the growing number of patients on transplant waiting lists. This supply-demand gap significantly limits procedure volumes globally

- High transplantation and lifelong post-operative care costs also remain a barrier, particularly in lower-income and underinsured populations

- For instance, procedures such as heart, liver, and lung transplantation often involve substantial surgical expenses, ICU care, and long-term immunosuppressive drug costs

- Risk of graft rejection, infection, and other post-transplant complications continues to create clinical uncertainty and increase healthcare burden

- In addition, regulatory complexity, ethical concerns, and limited transplant infrastructure in developing regions may restrict broader market access

- Overcoming these barriers through donor pool expansion, cost-effective care pathways, advanced rejection monitoring, and continued innovation in organ preservation will be essential for sustained market growth

Solid Organ Transplantation Market Scope

The market is segmented on the basis of organ, product, treatment, end-users, and distribution channel.

• By Organ

On the basis of organ, the Solid Organ Transplantation market is segmented into kidney, liver, pancreas, heart, lung, small bowel, kidney/pancreas, and others. The kidney segment dominated the largest market revenue share of 46.5% in 2025, driven by the high global prevalence of end-stage renal disease, diabetes, hypertension, and chronic kidney disorders. Kidney transplantation remains the most commonly performed solid organ transplant procedure due to strong clinical success rates and significant improvement in patient survival compared with long-term dialysis. Increasing awareness regarding living donor transplantation further supported segment growth. Government reimbursement programs and expansion of transplant registries also improved access in major markets. Hospitals continue to prioritize kidney transplant programs because of established surgical protocols and post-operative care pathways. Rising elderly populations with renal complications further increased patient demand. Advancements in donor-recipient matching technologies enhanced success outcomes. Improved immunosuppressive regimens reduced rejection risk and supported long-term graft survival. Emerging economies are also expanding nephrology and transplant infrastructure. Strong demand for replacement therapies sustained procedure volumes globally. These factors collectively ensured kidney segment dominance in 2025.

The lung segment is anticipated to witness the fastest growth rate of 9.8% from 2026 to 2033, fueled by increasing incidence of chronic obstructive pulmonary disease, pulmonary fibrosis, cystic fibrosis, and advanced respiratory failure. Lung transplantation is gaining importance as a life-saving option for patients unresponsive to conventional therapies. Improvements in donor lung preservation systems and ex vivo lung perfusion technologies are expanding transplant eligibility. Growing clinical expertise in thoracic surgery is improving procedural outcomes. Rising awareness regarding transplant options among pulmonologists is also increasing referrals. Specialized centers are expanding advanced respiratory transplant programs. Better post-transplant infection management supports survival rates. Increased investments in critical care infrastructure further aid adoption. Research into chronic rejection prevention is strengthening long-term confidence. Several countries are enhancing organ donation awareness campaigns. Technological progress in monitoring systems also supports growth. These factors position lung transplantation as the fastest-growing organ segment.

• By Product

On the basis of product, the Solid Organ Transplantation market is segmented into tissue products, immunosuppressive drugs, and preservation solution. The immunosuppressive drugs segment held the largest market revenue share of 58.7% in 2025, driven by the lifelong need for rejection prevention following transplant procedures. Drugs such as tacrolimus, cyclosporine, mycophenolate mofetil, corticosteroids, and newer agents remain essential in post-transplant management. Continuous therapy requirements generate recurring revenue streams throughout graft lifespan. Physicians rely heavily on individualized immunosuppressive regimens to balance rejection control and infection risk. Increasing transplant volumes directly expanded prescription demand worldwide. Strong reimbursement support in developed healthcare systems sustained access. Ongoing innovation in safer and more targeted therapies further strengthened segment growth. Hospital pharmacies and specialty centers remain major dispensing channels. Rising patient survival rates after transplantation extended long-term medication use. Monitoring technologies improved dose optimization and adherence. Generic product availability also widened market penetration. These factors maintained segment dominance.

The preservation solution segment is expected to witness the fastest CAGR of 10.3% from 2026 to 2033, driven by increasing focus on extending organ viability during transport and improving graft outcomes. Preservation solutions are critical for minimizing ischemic injury in kidney, liver, heart, and lung transplantation. Rising cross-border and long-distance organ sharing programs are increasing demand for advanced storage media. Technological improvements in hypothermic and machine perfusion systems are supporting solution usage. Hospitals are adopting premium formulations for high-risk donor organs. Growing organ shortage concerns are encouraging better utilization of marginal donors through preservation innovation. Clinical evidence linking better preservation to reduced complications supports adoption. Emerging markets are investing in transplant logistics infrastructure. Manufacturers are launching organ-specific solutions with improved efficacy. Demand from multi-organ transplant centers is also increasing. Better cold-chain systems further support growth. These factors make preservation solution the fastest-growing product segment.

• By Treatment

On the basis of treatment, the Solid Organ Transplantation market is segmented into immunosuppressive, monoclonal antibodies, and others. The immunosuppressive segment accounted for the largest market revenue share of 64.2% in 2025, driven by its foundational role in preventing acute and chronic graft rejection after transplantation. Standard maintenance regimens typically include calcineurin inhibitors, antiproliferative agents, and corticosteroids. These therapies are administered immediately after surgery and often continued for life. Increasing global transplant procedure volumes significantly supported treatment demand. Clinical protocols across hospitals strongly depend on established immunosuppressive combinations. Advancements in therapeutic drug monitoring improved treatment precision and safety. Long-term follow-up programs increased adherence rates. Rising awareness regarding graft preservation further strengthened uptake. Availability of branded and generic medicines supported affordability. Strong physician familiarity sustained prescribing confidence. Expanded transplant coverage in emerging markets also added demand. These factors ensured leadership of the immunosuppressive segment.

The monoclonal antibodies segment is projected to witness the fastest CAGR of 11.1% from 2026 to 2033, fueled by growing use in induction therapy and treatment of resistant rejection episodes. Agents targeting specific immune pathways offer precision-based suppression with improved outcomes in selected patients. Hospitals increasingly use monoclonal antibodies in high-risk recipients and sensitized patients. Advances in biologics manufacturing are improving product availability. Clinical trials continue evaluating next-generation antibody therapies with better safety profiles. Rising demand for personalized transplant medicine supports adoption. Physicians value targeted mechanisms that may reduce dependence on conventional drugs. Specialty centers are expanding biologic-based protocols. Strong investment by pharmaceutical companies in transplant immunology is another driver. Improved reimbursement for biologics in some regions supports access. Better survival outcomes strengthen long-term confidence. These factors position monoclonal antibodies as the fastest-growing treatment segment.

• By End-Users

On the basis of end-users, the Solid Organ Transplantation market is segmented into hospitals, homecare, speciality centres, and others. The hospitals segment dominated the largest market revenue share of 61.8% in 2025, driven by their role as primary centers for transplant surgery, donor matching, intensive care, and post-operative monitoring. Hospitals house multidisciplinary teams including surgeons, nephrologists, hepatologists, cardiologists, anesthesiologists, and transplant coordinators. Complex infrastructure requirements make hospitals essential for solid organ procedures. High patient inflow for evaluation and follow-up sustained service demand. Availability of ICUs and emergency care strengthened hospital leadership. Government-approved transplant programs are mostly concentrated in tertiary hospitals. Strong procurement of surgical devices and medicines supported revenues. Hospitals also manage complications such as rejection and infection. Training and research activities further reinforce their dominance. Public trust in accredited transplant centers supports patient preference. Continuous expansion of transplant units added growth. These factors ensured segment leadership.

The speciality centres segment is anticipated to witness the fastest CAGR of 9.7% from 2026 to 2033, fueled by rising demand for dedicated transplant-focused care pathways. Specialty centers provide streamlined services including evaluation, surgery coordination, immunology testing, and long-term monitoring. Patients increasingly prefer centers with concentrated expertise and shorter waiting times. Advanced diagnostics and personalized treatment models support adoption. Collaborations with hospitals improve referral networks and donor access. These centers often deliver higher procedural efficiency and targeted patient education. Increasing private investment in specialty healthcare infrastructure boosts capacity. International medical tourism for transplantation also supports growth. Digital follow-up systems improve long-term outcomes. Experienced multidisciplinary teams enhance confidence among patients. Expansion in urban healthcare hubs is accelerating. These factors drive rapid future growth.

• By Distribution Channel

On the basis of distribution channel, the Solid Organ Transplantation market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment accounted for the largest market revenue share of 54.6% in 2025, driven by the need for controlled dispensing of high-value immunosuppressants, biologics, and perioperative medicines. Most transplant recipients receive medications directly through hospital systems immediately after surgery. Hospitals ensure accurate dosing, monitoring, and management of drug interactions. Centralized procurement contracts supported consistent product supply. Complex cold-chain products are commonly handled through hospital pharmacies. Inpatient and outpatient transplant clinics generate recurring prescription volumes. Integration with electronic medical records improves compliance and safety. Specialty pharmacists also counsel patients on lifelong medication adherence. Large tertiary centers remain major purchasers globally. Reimbursement frameworks often favor institutional dispensing. Continuous follow-up visits support repeat demand. These factors maintained dominance in 2025.

The online pharmacy segment is expected to witness the fastest CAGR of 12.4% from 2026 to 2033, fueled by increasing demand for convenient long-term refill services for transplant patients. Recipients require lifelong medication adherence, making home delivery highly attractive. Online platforms offer auto-refill reminders, prescription uploads, and price comparison tools. Growing telemedicine use is accelerating prescription-to-order conversion rates. Patients in remote areas gain better access to specialty medicines. Subscription programs improve continuity of care. Enhanced cold-chain logistics are supporting sensitive drug delivery. Smartphone penetration is expanding digital pharmacy adoption worldwide. Cost-saving offers and loyalty programs attract recurring users. Regulatory frameworks for e-pharmacy operations are improving gradually. Rising preference for contactless healthcare purchasing adds momentum. These drivers make online pharmacy the fastest-growing distribution channel segment.

Solid Organ Transplantation Market Regional Analysis

- North America dominated the solid organ transplantation market with the largest revenue share of approximately 41.8% in 2025, driven by advanced healthcare infrastructure, favorable reimbursement systems, and high transplant procedure volumes across the region. The presence of major industry players and well-established transplant centers significantly supports market growth. Increasing prevalence of end-stage organ failure, chronic kidney disease, liver disorders, and heart failure is boosting demand for transplantation procedures

- Strong organ donation networks and efficient allocation systems further enhance transplant accessibility. Continuous technological advancements in surgical techniques and immunosuppressive therapies are improving patient outcomes

- Rising adoption of precision medicine and post-transplant monitoring solutions is strengthening clinical success rates. Government support for organ donation awareness campaigns also contributes to market expansion. High healthcare spending and robust insurance coverage ensure broad patient access to advanced transplant care. North America is expected to maintain its leading position throughout the forecast period

U.S. Solid Organ Transplantation Market Insight

The U.S. solid organ transplantation market captured the largest revenue share in 2025 within North America, driven by a high volume of kidney, liver, heart, and lung transplant procedures. The country benefits from a highly organized organ donation and allocation system that improves transplant efficiency. Strong presence of leading transplant centers and specialized hospitals supports advanced surgical outcomes. Increasing prevalence of chronic diseases such as diabetes, hypertension, and liver cirrhosis is driving demand for organ replacement therapies. Technological innovations in organ preservation, robotic-assisted surgeries, and immunosuppressive drugs are further enhancing success rates. Strong reimbursement frameworks and insurance coverage improve patient access to transplant procedures. Growing awareness regarding organ donation is increasing donor participation. Continuous clinical research and innovation in regenerative medicine and bioengineered organs are also contributing to market growth. The U.S. remains the key revenue contributor in the regional market.

Europe Solid Organ Transplantation Market Insight

The Europe solid organ transplantation market is projected to expand at a substantial CAGR throughout the forecast period, driven by strong public healthcare systems and well-established transplant networks. Rising prevalence of chronic diseases such as renal failure, cardiovascular diseases, and liver disorders is increasing demand for transplantation procedures. Government-supported organ donation programs and cross-border organ sharing agreements are improving transplant availability. Advanced surgical capabilities and increasing adoption of immunosuppressive therapies support positive patient outcomes. Countries such as Germany, France, Spain, and the U.K. are major contributors to regional growth. Rising healthcare investments and increasing awareness regarding organ donation further strengthen the market. Expanding use of digital health platforms for post-transplant monitoring is improving patient management. Continuous research in transplant immunology and regenerative medicine is supporting innovation. Europe maintains a strong and stable transplant ecosystem.

U.K. Solid Organ Transplantation Market Insight

The U.K. solid organ transplantation market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong NHS-backed transplant programs and increasing organ donation awareness. The country has a well-structured organ donation registry system that supports efficient matching and allocation. Rising prevalence of end-stage renal disease and liver disorders is increasing transplant demand. Advanced surgical expertise and specialized transplant centers improve clinical outcomes. Government initiatives promoting opt-out organ donation policies are expanding donor availability. Increasing use of immunosuppressive therapies and post-operative monitoring enhances patient survival rates. Research institutions are actively contributing to innovations in transplant medicine. Growing public awareness campaigns are encouraging higher donor participation. The U.K. continues to strengthen its position in the European transplant market.

Germany Solid Organ Transplantation Market Insight

The Germany solid organ transplantation market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced hospital infrastructure and strong clinical expertise. Germany has one of the most developed healthcare systems in Europe, supporting high-quality transplant procedures. Rising incidence of chronic kidney disease, heart failure, and liver disorders is driving demand. Strong regulatory frameworks ensure safe and efficient organ allocation processes. Increasing adoption of innovative surgical technologies is improving transplant success rates. Well-established organ donation programs support steady supply availability. Growing investment in post-transplant care and immunosuppressive therapies enhances long-term patient outcomes. Research in regenerative medicine and bioengineered organs is further supporting market development. Germany remains a key contributor to the European transplant landscape.

Asia-Pacific Solid Organ Transplantation Market Insight

The Asia-Pacific solid organ transplantation market is poised to grow at the fastest CAGR due to expanding healthcare infrastructure, rising chronic disease burden, and increasing awareness regarding organ donation. Growing disposable incomes and improving access to advanced medical care are supporting transplant adoption. Increasing incidence of kidney, liver, and cardiovascular diseases is significantly driving demand for organ replacement therapies. Governments across China, India, Japan, South Korea, and Southeast Asia are investing in transplant infrastructure and donor awareness programs. Expanding medical tourism in countries like India and Thailand is further boosting transplant procedures. Improvements in hospital capabilities and surgical technologies are enhancing outcomes. Rising adoption of insurance coverage for transplant procedures is improving affordability. Increasing collaboration with global transplant networks is strengthening capabilities. Asia-Pacific is expected to remain the fastest-growing region during the forecast period.

Japan Solid Organ Transplantation Market Insight

The Japan solid organ transplantation market is gaining momentum due to the country’s advanced healthcare system, aging population, and increasing prevalence of organ failure cases. Japan has strong expertise in complex surgical procedures and post-transplant care. Rising demand for kidney and liver transplants is supporting market expansion. Government policies are gradually improving organ donation awareness and registration rates. Increasing use of advanced immunosuppressive therapies enhances transplant success. Strong integration of medical technology and precision medicine supports better patient outcomes. Research in regenerative medicine and artificial organs is further strengthening the market. Japan’s focus on elderly healthcare significantly contributes to demand. Continuous innovation in surgical techniques supports long-term market growth.

China Solid Organ Transplantation Market Insight

The China solid organ transplantation market accounted for the largest market revenue share in Asia Pacific in 2025, driven by a large patient population and rapidly improving healthcare infrastructure. Increasing prevalence of chronic kidney disease, liver disorders, and cardiovascular diseases is fueling demand for transplants. Government investments in hospital expansion and transplant centers are improving access to advanced procedures. Rising awareness regarding organ donation is gradually improving donor availability. Strong domestic healthcare system development and medical training programs support clinical expertise. Expanding insurance coverage is improving affordability of transplant procedures. Growth in medical technology adoption, including minimally invasive and robotic-assisted surgeries, enhances outcomes. Increasing collaboration with international transplant organizations is improving standards. China is expected to remain a key growth driver in the region throughout the forecast period.

Solid Organ Transplantation Market Share

The Solid Organ Transplantation industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Novartis AG (Switzerland)

- Sanofi S.A. (France)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson (U.S.)

- AbbVie Inc. (U.S.)

- Bristol Myers Squibb (U.S.)

- Astellas Pharma Inc. (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- GlaxoSmithKline plc (U.K.)

- Bayer AG (Germany)

- Amgen Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Viatris Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Cipla Ltd. (India)

- Lupin Limited (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

Latest Developments in Global Solid Organ Transplantation Market

- In March 2021, the U.S. Food and Drug Administration (FDA) authorized the world’s first gene-edited pig-to-human kidney transplant research procedure conducted by NYU Langone Health. The transplanted kidney functioned normally for several days in a brain-dead recipient without immediate rejection, marking a major milestone in xenotransplantation and opening a new frontier for addressing global organ shortages

- In July 2022, researchers from Massachusetts General Hospital reported successful development and validation of ex vivo lung perfusion (EVLP) techniques to recondition marginal donor lungs prior to transplantation. The advancement significantly expanded the usable donor organ pool and improved transplant success rates by enabling assessment and repair of donor organs outside the body before implantation

- In March 2023, MediGO and LiveOnNY launched a real-time organ tracking and logistics platform in the United States to improve transparency and efficiency in organ procurement and transplantation. The system enabled end-to-end tracking of donor organs during transport, reducing delays and improving coordination between procurement organizations and transplant centers

- In August 2023, TransMedics Group announced the acquisition of Bridge to Life Ltd., including its LifeCradle Heart Preservation Transport System. This strategic acquisition expanded TransMedics’ organ preservation technology portfolio and strengthened its position in portable organ perfusion and transplantation logistics solutions

- In January 2024, the U.S. Organ Procurement and Transplantation Network (OPTN) reported a record-breaking milestone, with organ transplants in the United States exceeding 46,000 procedures in 2023, reflecting continued growth in transplantation activity and improved donor utilization efficiency across kidney, liver, heart, and lung transplants

- In June 2024, Fortune Business Insights reported that the global transplantation market surpassed USD 10.11 billion in 2023 and was projected to grow steadily through 2032, driven by rising organ failure cases, increasing donor programs, and advancements in immunosuppressive therapies and preservation technologies

- In August 2024, Fact.MR reported that the solid organ transplantation market was valued at approximately USD 4.9 billion in 2024 and is expected to grow steadily through 2034, supported by innovations such as ex vivo organ perfusion, 3D bioengineered tissues, and xenotransplantation research aimed at addressing global organ shortages

- In January 2025, the United States Organ Procurement and Transplantation Network (OPTN) announced that more than 48,000 solid organ transplants were performed in 2024, marking a new record high and a 3.3% increase compared to 2023. This growth reflected rising donor utilization efficiency and continued expansion of transplant infrastructure

- In October 2025, researchers reported advancements in enzyme-based organ conversion technology enabling the transformation of donor kidneys into universal blood-type-compatible organs. This breakthrough is expected to significantly reduce organ rejection risk and expand transplant compatibility across patient populations, representing a major innovation in transplantation science

- In December 2025, NYU Langone Health and collaborators advanced clinical trials in gene-edited pig kidney xenotransplantation in living patients. The study marked one of the most significant steps toward clinical-scale xenotransplantation, aiming to address chronic organ shortages by using genetically modified animal organs for human transplantation

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.