Global Solid Tumor Testing Market

Market Size in USD Billion

CAGR :

%

USD

30.71 Billion

USD

48.57 Billion

2025

2033

USD

30.71 Billion

USD

48.57 Billion

2025

2033

| 2026 –2033 | |

| USD 30.71 Billion | |

| USD 48.57 Billion | |

| % | |

|

Solid Tumor Testing Market Size

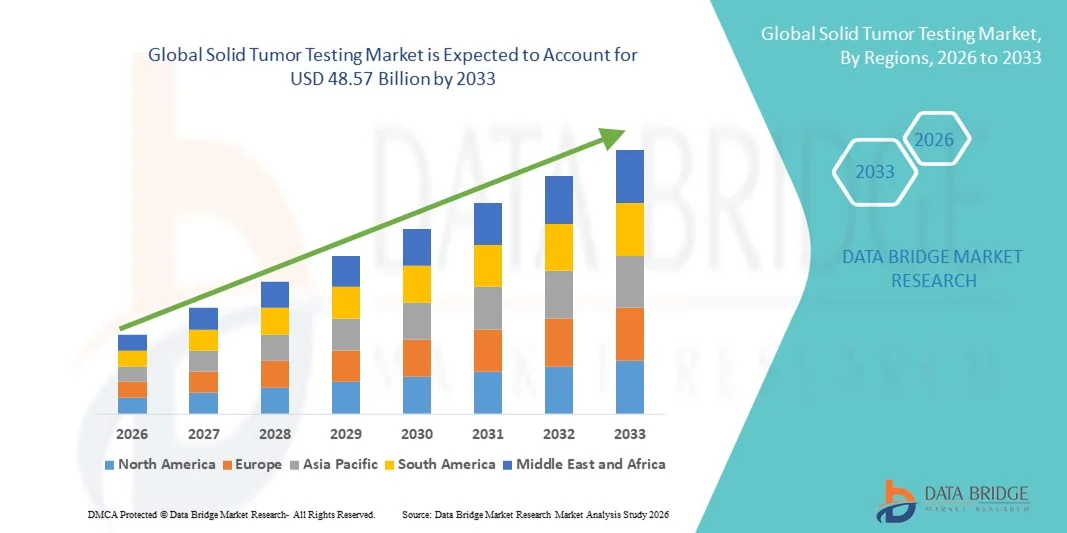

- The global solid tumor testing market size was valued at USD 30.71 billion in 2025 and is expected to reach USD 48.57 billion by 2033, at a CAGR of 5.90% during the forecast period

- The market growth is largely fueled by rapid advancements in molecular diagnostics, next-generation sequencing (NGS), and imaging technologies, which are enhancing the accuracy, speed, and reliability of solid tumor detection in clinical and research settings

- Furthermore, increasing demand for early cancer diagnosis, personalized medicine, and targeted therapy selection is accelerating the adoption of solid tumor testing solutions, thereby significantly boosting the overall growth of the industry

Solid Tumor Testing Market Analysis

- Solid Tumor Testing — advanced diagnostic procedures including molecular profiling, next‑generation sequencing (NGS), immunohistochemistry, FISH, and biomarker testing — are increasingly vital for accurate detection, personalized oncology treatment planning, and disease monitoring across clinical and research settings

- The escalating demand for solid tumor testing is primarily driven by rising cancer incidence globally, increased adoption of precision medicine and genomic diagnostics, and growing awareness of early detection’s impact on better patient outcomes

- North America dominated the solid tumor testing market with the largest revenue share of approximately 42.3% in 2025, supported by advanced healthcare infrastructure, strong reimbursement frameworks, leading diagnostic laboratories, and high adoption of molecular and genomic testing technologies

- Asia‑Pacific is expected to be the fastest‑growing region in the solid tumor testing market during the forecast period, with a notable CAGR driven by expanding healthcare systems, increasing cancer screening programs, rising reimbursement support, and accelerated uptake of advanced diagnostics in emerging economies

- The Clinical segment dominated the largest market revenue share of approximately 65% in 2025, driven by the increasing number of hospital diagnostic procedures, oncology treatment programs, and routine patient screening

Report Scope and Solid Tumor Testing Market Segmentation

|

Attributes |

Solid Tumor Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Solid Tumor Testing Market Trends

Rising Incidence of Cancer and Early Detection Demand

- The increasing prevalence of solid tumors, particularly breast, lung, colorectal, and prostate cancers, is driving demand for advanced solid tumor testing technologies globally

- For instance, in 2025, the International Agency for Research on Cancer (IARC) reported a significant rise in new cancer cases, prompting hospitals and diagnostic centers to invest in comprehensive molecular and genomic testing solutions

- The demand for early and accurate detection is critical to improve patient outcomes and enable personalized treatment strategies, fueling growth in the solid tumor testing market

- Hospitals and diagnostic labs are expanding testing capacities and adopting high-throughput testing platforms to address rising patient loads

- The ability to detect mutations, biomarkers, and tumor-specific signatures enables precision oncology, increasing the relevance of solid tumor tests in clinical decision-making

- Patient awareness campaigns and routine screening programs further accelerate adoption, particularly in regions with well-established healthcare infrastructure

- The integration of next-generation sequencing (NGS) and multiplex assays is expanding the scope of testing to cover multiple cancer types simultaneously

- Advanced analytics for tumor profiling support oncology specialists in selecting targeted therapies, enhancing the clinical value of solid tumor testing

- Clinical adoption is also driven by supportive reimbursement policies in developed markets, enabling wider access to testing

- Regional epidemiological trends in North America and Europe highlight increasing demand due to aging populations and higher cancer incidence rates

Solid Tumor Testing Market Dynamics

Driver

Increasing Healthcare Infrastructure and Awareness

- The expansion of hospital and diagnostic infrastructure in emerging markets is driving demand for solid tumor testing solutions

- For instance, in India and China, increasing government initiatives and investments in oncology care centers are enhancing testing availability

- Rising awareness among physicians and patients regarding early cancer detection and treatment monitoring is contributing to market expansion

- Educational programs and campaigns are promoting routine cancer screenings, particularly for high-risk populations

- Private diagnostic chains and hospital networks are investing in modern laboratory equipment to offer comprehensive tumor testing services

- Regional growth in Asia-Pacific is supported by increasing hospital capacities and the establishment of specialized oncology centers

- Medical tourism in countries like Singapore and Thailand is also contributing to adoption, as international patients seek advanced cancer diagnostics

- Outreach and telemedicine programs are enabling wider access to solid tumor testing in remote regions

- Availability of trained personnel and molecular pathology labs is supporting market growth in emerging economies

Restraint/Challenge

High Cost and Regulatory Hurdles

- The high cost of advanced solid tumor testing technologies, including NGS panels and multiplex assays, remains a significant barrier to widespread adoption, particularly in price-sensitive markets

- For instance, in developing regions, hospitals may limit testing to selected high-risk patients due to financial constraints, slowing market penetration

- Complex regulatory requirements and varying approvals across countries delay commercialization and increase compliance costs

- Laboratory accreditation standards, including CLIA, CAP, and ISO, must be met before implementing new tests, which can extend timelines and costs

- Reimbursement limitations in certain markets discourage adoption among healthcare providers

- Variability in test interpretation and lack of standardization across labs may reduce clinician confidence in some regions

- Operational challenges, such as shortage of trained molecular diagnosticians, impact deployment in emerging markets

- Infrastructure limitations in smaller hospitals can impede installation of high-throughput testing platforms

- Price sensitivity among patients in low- and middle-income countries affects the affordability of advanced testing

Solid Tumor Testing Market Scope

The market is segmented on the basis of type, cancer type, and application.

- By Type

On the basis of type, the Global Solid Tumor Testing market is segmented into Conventional Testing and Non-Conventional Testing. The Conventional Testing segment dominated the largest market revenue share of approximately 57% in 2025, driven by its established presence in clinical workflows, proven accuracy, and wide adoption among hospitals, diagnostic labs, and research institutes. Conventional testing methods, including histopathology, immunohistochemistry (IHC), and fluorescence in situ hybridization (FISH), are considered gold-standard techniques for tumor diagnosis, staging, and treatment planning. These tests are widely integrated into hospital diagnostic systems and support oncologists in treatment decision-making. Strong adoption in North America and Europe is supported by robust healthcare infrastructure, skilled personnel, and regulatory compliance standards. High clinical reliability, reproducibility, and accessibility of conventional methods further reinforce market dominance. Continuous R&D in reagents, imaging, and automation enhances throughput and efficiency. Hospitals and research centers prefer conventional testing for well-established cancer types such as breast, lung, and colorectal cancers. Integration with electronic medical records (EMR) and laboratory information systems (LIS) improves workflow efficiency. Large-scale clinical trials continue to validate the accuracy and reliability of conventional methods. The segment also benefits from strong reimbursement coverage in key markets.

The Non-Conventional Testing segment is expected to witness the fastest CAGR of 22.4% from 2026 to 2033, driven by technological advancements in molecular diagnostics, next-generation sequencing (NGS), liquid biopsy, and AI-based image analysis. Non-conventional testing enables early detection, real-time monitoring, and personalized treatment strategies for solid tumors. Increasing adoption in emerging markets, rising demand for minimally invasive procedures, and expansion of precision oncology programs fuel growth. Non-conventional tests are gaining traction for monitoring treatment response and detecting recurrence in breast, lung, and colorectal cancers. Integration with bioinformatics platforms and AI-enhanced analytics provides higher sensitivity and faster results. Rising investment from pharmaceutical and biotech companies for companion diagnostics further supports adoption. The segment’s flexibility, high throughput, and ability to detect multiple biomarkers simultaneously make it attractive for research and clinical applications. Continuous innovation, decreasing costs of NGS, and increasing awareness among clinicians enhance adoption globally. Regulatory approvals for liquid biopsy and multiplex testing panels are accelerating market penetration. Non-conventional testing also supports clinical trials for novel targeted therapies, expanding its application scope.

- By Cancer Type

On the basis of cancer type, the Global Solid Tumor Testing market is segmented into Breast Cancer, Lung Cancer, Colorectal Cancer, Prostate Cancer, and Cervical Cancer. The Breast Cancer segment dominated the largest market revenue share of approximately 29% in 2025, driven by high prevalence rates globally and well-established screening and diagnostic programs. Breast cancer testing is widely performed using histopathology, IHC, and imaging-guided biopsies, supporting early detection and precision treatment decisions. Awareness campaigns, routine screening initiatives, and insurance coverage in North America and Europe support segment leadership. Technological advances, such as 3D mammography, molecular profiling, and multigene panels, further enhance diagnostic accuracy. Hospitals, diagnostic labs, and research institutes heavily invest in breast cancer testing infrastructure. Early detection and personalized treatment strategies are key drivers of adoption. Integration with EMR and hospital LIS improves data management and clinical decision-making. Research funding and clinical trials continue to validate testing methods and support growth. Collaboration between academic institutions and biotech firms strengthens the adoption of advanced diagnostic methods. Patient-centric approaches, including minimally invasive sampling and liquid biopsy, enhance clinical acceptance. Continuous R&D improves sensitivity, specificity, and turnaround time.

The Lung Cancer segment is expected to witness the fastest CAGR of 21.2% from 2026 to 2033, fueled by increasing prevalence of lung cancer, rising awareness about early detection, and adoption of liquid biopsy and NGS technologies. Lung cancer testing benefits from technological advances in ctDNA detection, multiplex PCR, and AI-powered imaging analysis. Emerging markets in Asia-Pacific, including China and India, show significant growth due to expanding oncology infrastructure and rising smoking-related disease prevalence. Non-invasive and precision testing solutions drive adoption in both clinical and research settings. Government initiatives promoting early cancer detection and personalized medicine programs further support growth. Collaboration between hospitals, research centers, and biotech companies enables faster clinical validation and adoption of new assays. Increasing investment in companion diagnostics and targeted therapies accelerates lung cancer testing demand. Workflow automation, integration with bioinformatics platforms, and digital reporting tools improve efficiency. Rising patient awareness and proactive screening programs also contribute to the segment’s rapid growth.

- By Application

On the basis of application, the Global Solid Tumor Testing market is segmented into Clinical and Research. The Clinical segment dominated the largest market revenue share of approximately 65% in 2025, driven by the increasing number of hospital diagnostic procedures, oncology treatment programs, and routine patient screening. Clinical applications include diagnosis, staging, treatment monitoring, and recurrence detection, which are critical for personalized oncology care. Strong adoption in North America and Europe is supported by robust healthcare infrastructure, reimbursement coverage, and regulatory frameworks. Hospitals and diagnostic labs prefer validated testing platforms to ensure high accuracy and reproducibility. Integration with EMR, LIS, and decision support systems improves workflow and patient management. The segment benefits from the adoption of both conventional and non-conventional testing technologies. Growing awareness among oncologists and patients about precision medicine further strengthens adoption. Clinical trials and validation studies reinforce the reliability of testing methods. Expansion of cancer treatment centers and screening programs globally drives sustained demand. Continuous R&D in diagnostic reagents, automation, and imaging enhances workflow efficiency.

The Research segment is expected to witness the fastest CAGR of 20.8% from 2026 to 2033, fueled by the increasing use of solid tumor testing in biomarker discovery, immunotherapy development, and clinical trial programs. Research applications leverage NGS, liquid biopsy, AI-based image analysis, and multiplex assays for experimental studies and novel drug development. Academic and biotech institutions are investing heavily in advanced testing platforms to accelerate translational oncology research. The segment benefits from increasing government grants, funding for cancer research, and collaborations between pharmaceutical companies and research centers. Rising demand for early-stage drug efficacy studies, companion diagnostics development, and precision oncology trials supports growth. Integration with bioinformatics and data analytics platforms improves reproducibility and throughput. Emerging markets in Asia-Pacific show rapid adoption due to growing research investments. Regulatory support for clinical research and trial standardization further drives growth. Innovation in sample preparation, assay sensitivity, and automation strengthens segment adoption globally.

Solid Tumor Testing Market Regional Analysis

- North America dominated the solid tumor testing market with the largest revenue share of approximately 42.3% in 2025, supported by advanced healthcare infrastructure, strong reimbursement frameworks, leading diagnostic laboratories, and high adoption of molecular and genomic testing technologies

- The region’s healthcare providers are increasingly integrating conventional and non-conventional testing methods, including next-generation sequencing (NGS) and liquid biopsy, to enhance diagnostic accuracy and treatment planning

- Rising patient awareness, robust clinical research, and precision oncology programs further drive adoption. Technological advancements, workflow integration with EMR systems, and automated diagnostic platforms strengthen market growth

U.S. Solid Tumor Testing Market Insight

The U.S. solid tumor testing market captured the largest revenue share within North America in 2025, fueled by high adoption of advanced diagnostics, early cancer detection programs, and strong precision oncology initiatives. Hospitals, diagnostic centers, and research institutes prioritize both conventional histopathology and non-conventional molecular testing, including liquid biopsy and multigene panels. Favorable reimbursement policies, government support for precision medicine, and growing patient awareness accelerate market adoption. Integration with EMR and laboratory information systems enhances clinical efficiency. Rising incidence of breast, lung, and colorectal cancers and increased investment in R&D further support market expansion.

Europe Solid Tumor Testing Market Insight

The Europe solid tumor testing market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong adoption of molecular diagnostics, well-established healthcare infrastructure, and reimbursement policies for advanced testing. Increasing research collaborations and precision oncology programs support growth across hospital and laboratory settings.

U.K. Solid Tumor Testing Market Insight

The U.K. solid tumor testing market is anticipated to grow at a noteworthy CAGR, driven by national cancer screening programs, rising patient awareness, and adoption of advanced molecular testing platforms. Hospitals and diagnostic labs increasingly deploy NGS, liquid biopsy, and AI-assisted imaging to support early detection and treatment monitoring. Government funding and reimbursement for advanced diagnostics further stimulate growth.

Germany Solid Tumor Testing Market Insight

Germany solid tumor testing market is expected to expand at a considerable CAGR during the forecast period, fueled by adoption of advanced molecular diagnostics, regulatory support, and integration with hospital EMR systems. Hospitals and research institutes increasingly use NGS and liquid biopsy for early detection, personalized therapy, and research. Strong academic-industry collaborations and national cancer screening programs further drive market adoption.

Asia-Pacific Solid Tumor Testing Market Insight

Asia-Pacific solid tumor testing market is expected to be the fastest-growing region in the Solid Tumor Testing market during the forecast period, with a notable CAGR driven by expanding healthcare systems, increasing cancer screening programs, rising reimbursement support, and accelerated uptake of advanced diagnostics in emerging economies. Rapid urbanization, growing middle-class populations, and government-led initiatives support adoption.

China Solid Tumor Testing Market Insight

China solid tumor testing market accounted for the largest revenue share in Asia-Pacific in 2025, supported by the rapid expansion of healthcare infrastructure, adoption of NGS and liquid biopsy technologies, and national cancer screening programs. Partnerships between local diagnostic companies and global firms enhance accessibility and affordability.

Japan Solid Tumor Testing Market Insight

Japan solid tumor testing market is gaining momentum due to its high-tech healthcare ecosystem, aging population, and demand for precision oncology diagnostics. Hospitals and research institutes adopt minimally invasive testing and AI-integrated platforms. Strong government support, private healthcare investment, and increasing prevalence of solid tumors drive growth.

Solid Tumor Testing Market Share

The Solid Tumor Testing industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific (U.S.)

- Roche Diagnostics (Switzerland)

- Agilent Technologies (U.S.)

- Illumina (U.S.)

- QIAGEN (Germany)

- F. Hoffmann-La Roche (Switzerland)

- PerkinElmer (U.S.)

- Bio-Rad Laboratories (U.S.)

- Myriad Genetics (U.S.)

- Guardant Health (U.S.)

- Foundation Medicine (U.S.)

- Sysmex Corporation (Japan)

- BioMérieux (France)

- Beckman Coulter (U.S.)

- Genomic Health (U.S.)

- Nanostring Technologies (U.S.)

- SOPHiA GENETICS (Switzerland)

- Exact Sciences (U.S.)

- PathAI (U.S.)

- Fulgent Genetics (U.S.)

Latest Developments in Global Solid Tumor Testing Market

- In April 2024, Labcorp announced the commercial availability of Labcorp Plasma Detect, a clinically validated whole‑genome tumor‑informed assay for liquid biopsy that detects circulating tumor DNA (ctDNA) to guide solid tumor monitoring and recurrence assessments in precision oncology

- In April 2025, PGDx elio plasma focus Dx, a pan‑solid tumor liquid biopsy test, received De Novo authorization from the U.S. Food and Drug Administration (FDA), making it the first FDA‑authorized liquid biopsy assay enabling clinical laboratories and hospitals to analyze ctDNA for a broad range of solid tumors

- In May 2025, Labcorp expanded its precision oncology portfolio with new solid tumor and hematologic cancer test offerings, including expanded NGS panels and enhancements to its OmniSeq INSIGHT pan‑solid tumor profiling test with homologous recombination deficiency (HRD) testing, plus broader digital pathology capabilities to support clinical trials and diagnostic workflows globally

- In July 2025, Labcorp Holdings launched a CE‑marked cancer test in Europe aimed at expanding its solid tumor diagnostic footprint across EU markets, enhancing patient access and clinical decision support for solid tumor genomic profiling

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.