Global Somatostatin Analogs Market

Market Size in USD Billion

CAGR :

%

USD

8.71 Billion

USD

14.74 Billion

2025

2033

USD

8.71 Billion

USD

14.74 Billion

2025

2033

| 2026 –2033 | |

| USD 8.71 Billion | |

| USD 14.74 Billion | |

| % | |

|

Somatostatin Analogs Market Size

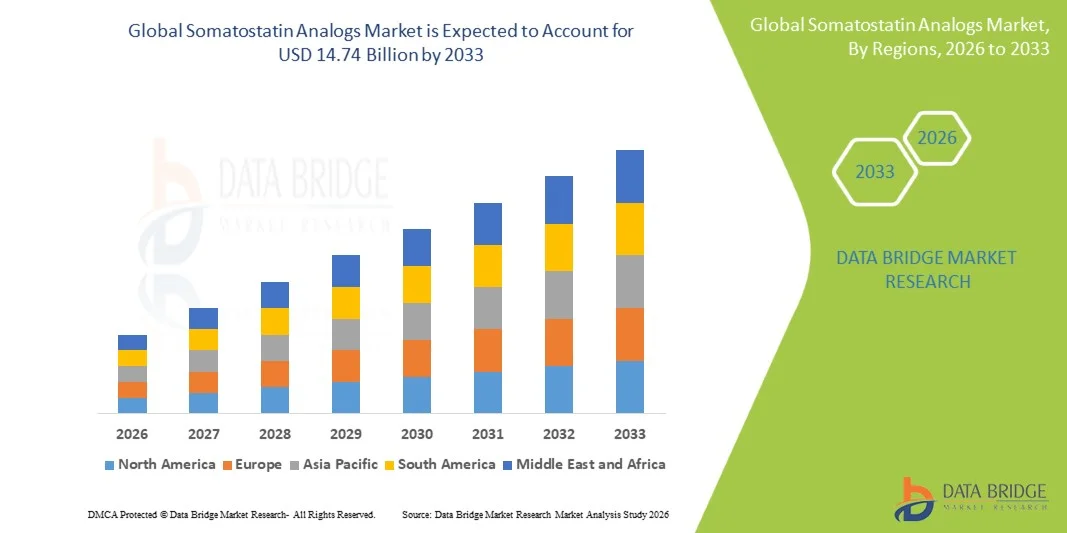

- The global somatostatin analogs market size was valued at USD 8.71 billion in 2025 and is expected to reach USD 14.74 billion by 2033, at a CAGR of 6.80% during the forecast period

- The market growth is largely fueled by the rising incidence of conditions such as acromegaly, neuroendocrine tumors (NETs), and other hormone‑related disorders, alongside broader adoption of long‑acting formulations and improved diagnosis rates, reflecting heightened clinical and research activity

- Furthermore, advancements in drug delivery mechanisms, strong R&D investments by pharmaceutical companies, and expanded access to specialty care and reimbursement programs are supporting innovation and uptake of somatostatin analog therapies across hospitals and clinics, bolstering the market’s expansion

Somatostatin Analogs Market Analysis

- Somatostatin analogs, used to inhibit hormone secretion and manage conditions such as acromegaly, neuroendocrine tumors (NETs), and other endocrine disorders, are increasingly critical in modern therapeutic regimens due to their targeted action, long-acting formulations, and integration with personalized treatment plans in both hospital and outpatient settings

- The rising demand for somatostatin analogs is primarily driven by the growing prevalence of endocrine and neuroendocrine disorders, enhanced diagnostic capabilities, and increasing awareness of effective treatment options, along with a preference for therapies that provide improved patient compliance and quality of life

- North America dominated the somatostatin analogs market with the largest revenue share of 40.5% in 2025, attributed to advanced healthcare infrastructure, early adoption of novel therapeutics, high healthcare spending, and strong presence of leading pharmaceutical companies actively investing in R&D and launching innovative analog therapies

- Asia-Pacific is expected to be the fastest-growing region in the somatostatin analogs market during the forecast period due to rising healthcare accessibility, increasing patient awareness, expanding specialty care facilities, and improving reimbursement policies

- The Octreotide segment dominated the market with a market share of 42.9% in 2025, driven by its established clinical efficacy in treating acromegaly and neuroendocrine tumors

Report Scope and Somatostatin Analogs Market Segmentation

|

Attributes |

Somatostatin Analogs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Somatostatin Analogs Market Trends

“Expansion of Long-Acting and Targeted Formulations”

- A notable and growing trend in the global somatostatin analogs market is the development of long-acting and targeted formulations, which allow for sustained hormone suppression and reduced dosing frequency, improving patient adherence and therapeutic outcomes

- For instance, Lanreotide Autogel enables monthly dosing for acromegaly and neuroendocrine tumor patients, minimizing clinic visits while maintaining consistent drug efficacy

- Advancements in formulation technologies are also supporting the creation of personalized treatment plans, including extended-release and depot injections tailored to patient-specific needs, enhancing clinical convenience

- The integration of these long-acting therapies into standard treatment protocols is helping healthcare providers optimize patient management, improve quality of life, and reduce the burden of frequent hospital visits

- This trend towards more efficient, patient-centric, and clinically effective analog formulations is redefining therapy expectations in endocrine and neuroendocrine disease management

- The demand for long-acting and tailored somatostatin analogs is rising globally, as both hospitals and specialty clinics seek therapies that maximize efficacy while minimizing patient inconvenience

- Collaboration between pharmaceutical companies and specialty care centers is facilitating co-development of combination therapies with somatostatin analogs, broadening their clinical applications and market potential

Somatostatin Analogs Market Dynamics

Driver

“Increasing Prevalence of Endocrine and Neuroendocrine Disorders”

- The growing incidence of acromegaly, neuroendocrine tumors, and other hormone-related disorders is a major driver for the heightened demand for somatostatin analogs

- For instance, rising diagnosis rates due to improved imaging and biochemical testing have expanded the patient pool eligible for targeted analog therapy

- As awareness of effective treatment options increases among healthcare providers and patients, adoption of somatostatin analogs for chronic disease management is accelerating

- Furthermore, the integration of these therapies into comprehensive care pathways for tumor and hormone disorders supports better clinical outcomes and patient compliance

- Increasing investment in R&D and launch of new analog formulations by pharmaceutical companies are further propelling market growth, enhancing accessibility and efficacy

- For instance, government and private healthcare initiatives in Europe and North America are supporting early screening programs for NETs, driving higher adoption of somatostatin analogs

- Growing off-label applications and clinical trials exploring additional endocrine and tumor indications are creating new opportunities for market expansion

Restraint/Challenge

“High Cost and Access Barriers in Emerging Regions”

- The relatively high price of somatostatin analogs compared to conventional therapies poses a significant challenge, limiting accessibility for patients in price-sensitive and emerging markets

- For instance, in countries with limited reimbursement or insurance coverage, the cost of long-acting Lanreotide or Octreotide injections can restrict patient adoption

- In addition, logistical challenges related to cold-chain storage and specialized administration requirements create barriers in resource-limited healthcare settings

- These cost and access limitations can hinder widespread uptake despite the clinical benefits of somatostatin analog therapies for endocrine and neuroendocrine disorders

- Addressing these challenges through patient assistance programs, generic alternatives, and improved healthcare infrastructure is crucial for sustaining market growth

- For instance, limited awareness among healthcare providers in emerging markets about the full benefits of somatostatin analogs can delay adoption, affecting market penetration

- Regulatory approval delays and complex clinical trial requirements in certain regions can also slow the introduction of new analog formulations, constraining market expansion

Somatostatin Analogs Market Scope

The market is segmented on the basis of type, indication, product, route of administration, end-user, and distribution channel.

- By Type

On the basis of type, the somatostatin analogs market is segmented into octreotide, lanreotide, pasireotide diseases, immunological disorders, respiratory diseases, cardiovascular diseases, neurological disorders, and others. The Octreotide segment dominated the market with the largest revenue share of 42.9% in 2025, primarily due to its long-established clinical efficacy in treating acromegaly and neuroendocrine tumors. Octreotide’s widespread adoption in hospitals and specialty clinics, along with its availability in both short-acting and long-acting formulations, makes it a preferred choice for physicians and patients alike. Its compatibility with parenteral administration further enhances patient compliance. The segment also benefits from robust awareness among endocrinologists and oncologists regarding dosing regimens, safety profile, and monitoring. Furthermore, Octreotide has been extensively studied in clinical trials, strengthening physician confidence in its therapeutic outcomes. The consistent demand from both developed and emerging markets contributes to sustaining its leading position in the market.

The Pasireotide segment is expected to witness the fastest growth during the forecast period, driven by its expanded indication for Cushing’s disease and acromegaly, and ongoing clinical research exploring additional applications. Pasireotide’s advanced mechanism of action offers improved efficacy for patients who are resistant to first-generation analogs. The growth is further supported by increasing awareness of rare endocrine disorders and adoption in specialty clinics. Its introduction as a long-acting formulation with enhanced patient convenience is attracting new users. Moreover, patent-protected products and limited competition in certain regions are maintaining high market value. Emerging healthcare infrastructure in Asia-Pacific and Latin America is also contributing to the rising uptake of Pasireotide therapies.

- By Indication

On the basis of indication, the market is segmented into tumor, acromegaly, and others. The tumor segment dominated in 2025 with the largest revenue share due to the widespread use of somatostatin analogs in managing neuroendocrine tumors and other hormone-secreting tumors. Hospitals and specialty clinics prescribe these analogs for their proven efficacy in tumor growth inhibition and symptom management. Strong clinical evidence, long-term patient follow-up data, and established treatment protocols contribute to high adoption rates. Reimbursement policies in developed countries further support the segment. Integration into multidisciplinary treatment regimens enhances patient compliance and outcomes. The segment benefits from continuous innovation in long-acting and depot formulations, maintaining physician preference.

The acromegaly segment is expected to witness the fastest growth during the forecast period, driven by increased diagnosis rates through advanced imaging and biochemical testing. Specialty clinics are increasingly managing acromegaly patients with somatostatin analogs due to improved efficacy and convenience of long-acting formulations. Rising patient awareness about effective therapy options contributes to adoption. The segment is supported by ongoing clinical research exploring combination therapies and novel analog formulations. Emerging markets with rising healthcare access are fueling market growth. Physician confidence in analog therapy for long-term disease management further accelerates adoption.

- By Product

On the basis of product, the market is segmented into Lanreotide, Octreotide, Pasireotide, and others. The Octreotide product segment dominated the market in 2025 due to its established clinical track record, wide availability, and diverse formulation options. Hospitals and specialty clinics prefer Octreotide for its predictable pharmacokinetics and safety profile. Long-acting formulations reduce dosing frequency, enhancing patient adherence. Physician familiarity and robust clinical guidelines further drive adoption. Developed markets contribute significantly to revenue due to strong healthcare infrastructure. Continuous R&D ensures product reliability and sustained market leadership.

The Pasireotide product segment is expected to grow at the fastest rate during the forecast period, supported by its novel mechanism of action and approval for multiple rare endocrine disorders. Specialty clinics are increasingly adopting Pasireotide for patients resistant to first-generation analogs. Clinical trials exploring off-label and combination use are expanding its market reach. Limited competition in certain regions allows higher pricing and revenue potential. Emerging markets with increasing awareness are driving adoption. The introduction of long-acting and patient-friendly formulations further accelerates market growth.

- By Route of Administration

On the basis of route of administration, the market is segmented into parenteral and others. The parenteral segment dominated in 2025 with the largest market share due to the need for controlled, sustained drug delivery, ensuring therapeutic efficacy and safety. Hospitals and specialty clinics widely utilize parenteral administration for long-acting formulations, reducing hospital visits. Physician familiarity and clinical guidelines support routine use. Reimbursement coverage for injectable therapies in developed regions facilitates adoption. Long-term safety and efficacy data strengthen physician preference. The segment benefits from robust demand in both chronic and rare endocrine disorders.

The others segment (oral or subcutaneous alternatives) is expected to witness the fastest growth during the forecast period, due to ongoing research into oral and minimally invasive delivery systems that improve patient convenience and adherence. Emerging formulations are gaining interest in specialty clinics. Reduced administration burden encourages adoption in homecare settings. Clinical trials validating efficacy and safety are increasing confidence among healthcare providers. Accessibility in emerging markets is improving with novel delivery mechanisms. The trend toward patient-centric therapy drives accelerated uptake globally.

- By End-User

On the basis of end-user, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated in 2025 due to high patient volumes, advanced treatment facilities, and the availability of specialist endocrinologists and oncologists. Hospitals provide access to long-acting formulations under controlled conditions, ensuring patient safety. Reimbursement coverage in developed regions encourages hospital-based therapy. Hospitals also serve as referral centers for rare disease management, supporting analog adoption. Continuous monitoring and follow-up capabilities enhance treatment outcomes. This segment remains the largest revenue contributor globally.

The specialty clinics segment is expected to witness the fastest growth during the forecast period, driven by increasing focus on personalized care for endocrine and neuroendocrine disorders. Clinics offer patient-centric services, including therapy administration, monitoring, and counseling. Growing awareness among patients about specialized treatment options accelerates adoption. Emerging markets are witnessing expansion of specialty clinics with improved healthcare infrastructure. Collaboration with pharmaceutical companies for educational and support programs boosts clinic-based adoption. Convenient access to therapy in outpatient settings supports faster growth than traditional hospital-based care.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated in 2025 due to direct supply to hospitals and specialty clinics, ensuring reliable access to high-cost analog therapies and adherence to storage and handling requirements. Hospital pharmacies facilitate seamless administration within healthcare settings, improving patient compliance. Strong relationships with pharmaceutical manufacturers support steady supply. Reimbursement and insurance coverage are more straightforward in hospital settings. Trained staff ensure proper administration and monitoring. Hospitals remain the primary point of access for long-acting somatostatin analogs.

The online pharmacy segment is expected to witness the fastest growth during the forecast period, driven by increasing patient preference for home delivery, improved e-commerce infrastructure, and patient support programs. Online platforms provide access to analogs for patients in remote or underserved areas. Homecare patients benefit from convenience and reduced travel to hospitals. Telemedicine integration and patient counseling enhance therapy adherence. Digital awareness campaigns by pharmaceutical companies support adoption. Regulatory approval of online dispensing in key regions further fuels growth.

Somatostatin Analogs Market Regional Analysis

- North America dominated the somatostatin analogs market with the largest revenue share of 40.5% in 2025, attributed to advanced healthcare infrastructure, early adoption of novel therapeutics, high healthcare spending, and strong presence of leading pharmaceutical companies actively investing in R&D and launching innovative analog therapies

- Patients and healthcare providers in the region highly value the proven efficacy, long-acting formulations, and safety profile of somatostatin analogs, which facilitate improved disease management and patient adherence

- This widespread adoption is further supported by strong reimbursement policies, high healthcare expenditure, advanced diagnostic facilities, and the presence of leading pharmaceutical companies investing in R&D and launching innovative therapies, establishing somatostatin analogs as a standard treatment choice for tumors, acromegaly, and other endocrine disorders

U.S. Somatostatin Analogs Market Insight

The U.S. somatostatin analogs market captured the largest revenue share of 80% in 2025 within North America, driven by the high prevalence of endocrine and neuroendocrine disorders and widespread adoption of advanced therapies. Hospitals and specialty clinics are increasingly relying on long-acting analog formulations to improve patient adherence and reduce clinic visits. The growing focus on early diagnosis of neuroendocrine tumors and acromegaly, coupled with strong reimbursement coverage and insurance support, further propels market growth. Moreover, ongoing R&D by leading pharmaceutical companies and the integration of analog therapy into clinical treatment protocols are significantly contributing to market expansion.

Europe Somatostatin Analogs Market Insight

The Europe somatostatin analogs market is projected to expand at a significant CAGR during the forecast period, driven by increasing awareness of rare endocrine disorders, well-established healthcare infrastructure, and favorable reimbursement policies. Hospitals and specialty clinics are adopting analog therapies for tumor and acromegaly management, supported by clinical guidelines and physician familiarity. The increasing demand for patient-centric treatment options and advancements in long-acting formulations are fostering growth. Countries such as Germany, France, and Italy are witnessing higher adoption across both hospital and specialty clinic settings. Regulatory support and ongoing clinical research further enhance market expansion in Europe.

U.K. Somatostatin Analogs Market Insight

The U.K. somatostatin analogs market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by rising diagnosis rates of acromegaly and neuroendocrine tumors. Hospitals and specialty clinics are increasingly integrating long-acting analogs into standard care regimens to improve treatment outcomes and patient convenience. In addition, favorable reimbursement frameworks and government initiatives promoting rare disease management encourage adoption. Physician awareness and patient preference for therapies that reduce dosing frequency contribute to market growth. The country’s focus on advanced healthcare delivery and specialty care strengthens overall market momentum.

Germany Somatostatin Analogs Market Insight

The Germany somatostatin analogs market is expected to expand at a considerable CAGR during the forecast period, driven by high healthcare expenditure, strong physician adoption, and rising prevalence of neuroendocrine and endocrine disorders. Hospitals and specialty clinics actively prescribe long-acting analogs for tumor and acromegaly management. The country’s advanced diagnostic infrastructure facilitates early detection, enabling timely treatment initiation. Increasing awareness among patients about effective analog therapies and ongoing pharmaceutical innovations are further driving growth. In addition, regulatory support for novel therapies and integration into hospital formularies enhance market penetration.

Asia-Pacific Somatostatin Analogs Market Insight

The Asia-Pacific somatostatin analogs market is poised to grow at the fastest CAGR during the forecast period, driven by rising awareness of endocrine and neuroendocrine disorders, improving healthcare infrastructure, and increasing access to specialty treatments in countries such as China, Japan, and India. Hospitals and specialty clinics are expanding their use of long-acting analog formulations to improve patient adherence and reduce hospital visits. Government initiatives promoting rare disease diagnosis and treatment support market growth. Moreover, the growing presence of pharmaceutical companies, affordability of therapy, and expansion of specialty clinics are increasing accessibility in both urban and semi-urban areas.

Japan Somatostatin Analogs Market Insight

The Japan somatostatin analogs market is gaining momentum due to the country’s advanced healthcare system, rising prevalence of neuroendocrine tumors, and increasing focus on patient convenience. Specialty clinics and hospitals are adopting long-acting formulations to enhance therapy adherence and reduce dosing frequency. The integration of analog therapy into multidisciplinary treatment approaches is driving growth. In addition, government initiatives supporting rare disease management and early diagnosis are fueling adoption. Patient awareness programs and technological advancements in drug delivery further contribute to the market expansion in Japan.

India Somatostatin Analogs Market Insight

The India somatostatin analogs market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising prevalence of endocrine disorders, expanding healthcare infrastructure, and increasing patient awareness. Specialty clinics and hospitals are adopting long-acting analogs to improve adherence and minimize hospital visits. The emergence of domestic pharmaceutical manufacturers and availability of cost-effective analog options are supporting market growth. In addition, government programs promoting rare disease diagnosis and improved access to specialty care are facilitating adoption. Urbanization, growing middle-class population, and increasing access to modern healthcare facilities are key factors propelling the market in India.

Somatostatin Analogs Market Share

The Somatostatin Analogs industry is primarily led by well-established companies, including:

- Crinetics Pharmaceuticals, Inc. (U.S.)

- Ipsen (France)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Camurus AB (Sweden)

- Midatech Pharma PLC (U.K.)

- Peptron Inc (South Korea)

- Amryt Pharma plc (U.K.)

- Crinetics Oncology (U.S.)

- Dauntless Pharmaceuticals (U.S.)

- Eli Lilly and Company (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Sunovion Pharmaceuticals Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Sanofi (France)

- Bristol Myers Squibb (U.S.)

- Alkermes plc (Ireland)

- Helsinn Healthcare SA (Switzerland)

What are the Recent Developments in Global Somatostatin Analogs Market?

- In September 2025, the U.S. Food and Drug Administration (FDA) approved Palsonify (paltusotine) a once‑daily oral somatostatin analog for the treatment of acromegaly, marking a shift toward more convenient oral therapy options beyond injectable analogs for rare endocrine disorders

- In July 2025, multiple biosimilar versions of lanreotide and octreotide were approved in Europe, expanding competitive treatment options and potentially improving affordability and access across key markets

- In April 2025, the European Medicines Agency’s (EMA) CHMP issued a positive opinion for Oczyesa (CAM2029), a long‑acting subcutaneous octreotide depot formulation for maintenance treatment of adult patients with acromegaly indicating strong regulatory support for next‑generation somatostatin analog delivery systems in the EU

- In February 2025, Crinetics Pharmaceuticals announced FDA acceptance of the paltusotine NDA for adult acromegaly maintenance therapy, signaling key regulatory progress toward broader availability of oral somatostatin analog therapies in the U.S.

- In October 2024, the U.S. FDA issued a Complete Response Letter (CRL) to Camurus for CAM2029, an extended‑release octreotide treatment intended for acromegaly, citing manufacturing facility deficiencies; the company committed to resolving these to advance approval

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.