Global Spasticity Treatment Market

Market Size in USD Billion

USD

15.30 Billion

USD

33.03 Billion

2025

2033

USD

15.30 Billion

USD

33.03 Billion

2025

2033

| 2026 - 2033 | |

| USD 15.30 Billion | |

| USD 33.03 Billion | |

| % | |

|

Spasticity Treatment Market Size

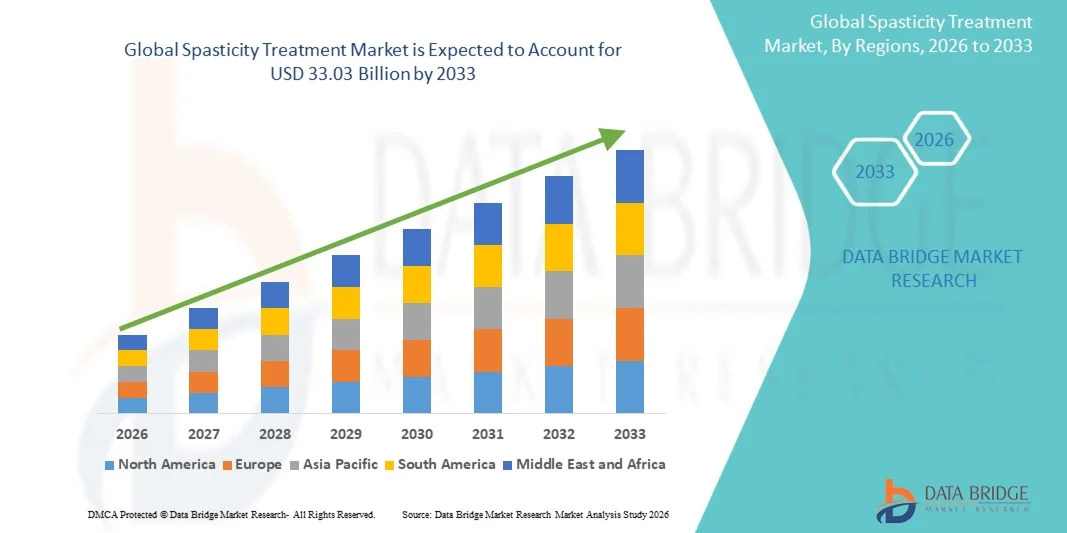

- The global spasticity treatment market size was valued at USD 15.30 billion in 2025 and is expected to reach USD 33.03 billion by 2033, at a CAGR of 10.1% during the forecast period

- The market growth is largely fueled by the increasing prevalence of neurological disorders such as multiple sclerosis, cerebral palsy, stroke, and spinal cord injuries, leading to higher demand for effective spasticity management therapies across healthcare settings

- Furthermore, rising awareness regarding early diagnosis and treatment, along with advancements in therapeutic options such as botulinum toxin injections, oral medications, and intrathecal baclofen therapy, is establishing spasticity treatment as a critical component of neurological care. These converging factors are accelerating the uptake of Spasticity Treatment solutions, thereby significantly boosting the industry's growth

Spasticity Treatment Market Analysis

- Spasticity treatment, involving pharmacological therapies, physical rehabilitation, and advanced interventions such as botulinum toxin injections and intrathecal baclofen therapy, is essential for managing muscle stiffness and spasms associated with neurological conditions like multiple sclerosis, cerebral palsy, stroke, and spinal cord injuries

- The escalating demand for spasticity treatment is primarily fueled by the rising prevalence of neurological disorders, increasing geriatric population, and growing awareness regarding early diagnosis and long-term management of motor function impairments. Advancements in treatment approaches and improved access to rehabilitation services are further supporting market growth

- North America dominated the spasticity treatment market with the largest revenue share of 39.1% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative therapies, and strong presence of key pharmaceutical and medical device companies. The U.S. continues to witness steady growth driven by increasing diagnosis rates and availability of specialized treatment options

- Asia-Pacific is expected to be the fastest growing region in the spasticity treatment market during the forecast period due to rising healthcare expenditure, increasing awareness of neurological conditions, and expanding access to rehabilitation and specialty care services in countries such as China and India

- The Medication segment dominated the largest market revenue share of 62.1% in 2025, driven by its widespread use as the primary treatment approach for managing spasticity symptoms

Report Scope and Spasticity Treatment Market Segmentation

|

Attributes |

Spasticity Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Spasticity Treatment Market Trends

“Advancements in Neuromodulation and Personalized Treatment Approaches”

- A significant and accelerating trend in the global Spasticity Treatment market is the growing adoption of advanced neuromodulation therapies, targeted drug delivery systems, and personalized rehabilitation approaches to improve patient outcomes. These innovations are enhancing treatment precision, reducing side effects, and enabling more effective long-term management of spasticity across neurological conditions.

- For instance, intrathecal baclofen therapy (ITB) pumps are increasingly being used to deliver medication directly to the spinal cord, allowing better control of severe spasticity with lower systemic drug exposure

- The integration of digital health tools and wearable devices is also enabling continuous monitoring of muscle activity and patient mobility, helping clinicians tailor treatment plans based on real-time data

- For instance, wearable sensor technologies are being used in rehabilitation programs to track muscle stiffness and movement patterns in patients with cerebral palsy or multiple sclerosis

- Increasing focus on combination therapies, including pharmacological treatments, physical therapy, and minimally invasive interventions such as botulinum toxin injections, is improving overall treatment effectiveness

- For instance, botulinum toxin injections are widely used alongside physiotherapy to target specific muscle groups and reduce stiffness in post-stroke patients

- This trend toward more targeted, patient-centric, and technology-enabled treatment strategies is transforming the management of spasticity, particularly in chronic neurological conditions

- For instance, rehabilitation centers are adopting multidisciplinary care models that combine neurologists, physiotherapists, and occupational therapists to optimize treatment outcomes

- The demand for advanced and personalized spasticity treatment solutions is growing steadily as healthcare providers focus on improving quality of life, mobility, and functional independence for patients

Spasticity Treatment Market Dynamics

Driver

“Increasing Prevalence of Neurological Disorders and Rising Demand for Rehabilitation Therapies”

- The rising incidence of neurological conditions such as stroke, multiple sclerosis, cerebral palsy, and spinal cord injuries is a key driver for the growth of the spasticity treatment market. These conditions often lead to muscle stiffness and movement disorders, increasing the demand for effective treatment solutions

- For instance, the growing global burden of stroke cases has significantly increased the number of patients requiring long-term spasticity management and rehabilitation therapies

- Increasing awareness regarding early diagnosis and treatment of spasticity is encouraging patients to seek timely medical intervention, improving treatment outcomes and driving market demand

- For instance, rehabilitation programs in developed countries are increasingly incorporating early physiotherapy and pharmacological treatments to prevent severe muscle contractures

- Advances in medical therapies, including improved muscle relaxants, injectable treatments, and neuromodulation techniques, are further supporting market growth

- For instance, the use of botulinum toxin type A injections has become a standard treatment for focal spasticity due to its effectiveness and minimally invasive nature

- In addition, growing investment in rehabilitation infrastructure and specialized care centers is enhancing access to treatment services globally

- For instance, emerging economies are expanding neuro-rehabilitation centers to cater to increasing patient populations with mobility disorders

Restraint/Challenge

“High Treatment Costs and Limited Access to Specialized Care”

- One of the major challenges in the spasticity treatment market is the high cost associated with advanced therapies, including neuromodulation devices, long-term rehabilitation programs, and surgical interventions, which can limit access for many patients

- For instance, intrathecal baclofen pump implantation and maintenance can be expensive, making it less accessible in low- and middle-income regions

- Limited availability of skilled healthcare professionals, including neurologists and rehabilitation specialists, further restricts access to effective treatment in certain regions

- For instance, rural areas in developing countries often lack specialized neuro-rehabilitation facilities, leading to delayed or inadequate treatment

- Variability in treatment outcomes and the need for long-term therapy adherence can also pose challenges for patients and healthcare providers

- For instance, some patients may require repeated botulinum toxin injections and ongoing physiotherapy, increasing treatment burden and cost over time

- Addressing these challenges requires improved healthcare infrastructure, increased awareness, and development of cost-effective treatment options to ensure broader accessibility

Spasticity Treatment Market Scope

The market is segmented on the basis of therapy, treatment, drugs, route of administration, indication, distribution channel, and end-users.

• By Therapy

On the basis of therapy, the Spasticity Treatment market is segmented into Physical Therapy and Occupational Therapy. The Physical Therapy segment dominated the largest market revenue share of 54.7% in 2025, driven by its widespread adoption as a first-line and non-invasive treatment approach for spasticity management. Physical therapy focuses on improving muscle strength, flexibility, and mobility, making it essential for patients with neurological disorders such as multiple sclerosis and cerebral palsy. Healthcare providers increasingly recommend physical therapy due to its effectiveness in reducing muscle stiffness and enhancing functional independence. The growing awareness regarding rehabilitation therapies further boosts segment demand. In addition, the rising prevalence of neurological disorders globally contributes to increased therapy adoption. Physical therapy is often combined with pharmacological treatments, enhancing overall patient outcomes. Advancements in rehabilitation techniques and assistive devices also support market growth. The availability of trained physiotherapists across hospitals and clinics ensures accessibility. Government initiatives promoting rehabilitation services further strengthen adoption. Increasing preference for non-drug therapies reduces dependency on medications. Long-term benefits and minimal side effects make it highly favorable. Overall, physical therapy remains the dominant segment due to its effectiveness, safety, and wide clinical acceptance.

The Occupational Therapy segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by its growing role in improving daily functional abilities and quality of life for patients. Occupational therapy helps individuals perform everyday activities independently, which is crucial for patients with severe spasticity conditions. Increasing emphasis on patient-centric care and rehabilitation outcomes accelerates segment growth. The rising number of long-term disability cases further boosts demand for occupational therapy services. Integration of advanced therapeutic tools and personalized treatment plans enhances effectiveness. Growing awareness among patients and caregivers about functional rehabilitation also supports adoption. Occupational therapy is increasingly being incorporated into comprehensive treatment programs. The expansion of homecare services further drives its utilization. In addition, favorable reimbursement policies in developed regions contribute to growth. Technological advancements such as virtual therapy platforms are gaining traction. Increasing investments in rehabilitation infrastructure also support expansion. Overall, occupational therapy is the fastest-growing segment due to its focus on functional independence and holistic care.

• By Treatment

On the basis of treatment, the market is segmented into Medication and Surgery. The Medication segment dominated the largest market revenue share of 62.1% in 2025, driven by its widespread use as the primary treatment approach for managing spasticity symptoms. Medications such as muscle relaxants and antispastic agents help reduce muscle stiffness and improve mobility. Physicians prefer pharmacological treatments due to their immediate effectiveness and ease of administration. The increasing prevalence of neurological disorders significantly contributes to demand for medications. Continuous advancements in drug formulations enhance efficacy and reduce side effects. Oral medications are widely prescribed, increasing patient compliance. In addition, growing awareness regarding early treatment further supports market growth. Pharmaceutical companies are actively investing in developing novel therapies. The availability of a wide range of drugs provides flexibility in treatment plans. Medications are often used in combination with physical therapy, improving outcomes. Strong distribution networks ensure easy accessibility. Overall, medication remains the dominant segment due to its effectiveness, accessibility, and widespread clinical use.

The Surgery segment is expected to witness the fastest CAGR of 7.6% from 2026 to 2033, driven by increasing demand for advanced treatment options in severe spasticity cases. Surgical procedures such as selective dorsal rhizotomy and intrathecal baclofen pump implantation provide long-term relief. Rising cases of treatment-resistant spasticity are boosting surgical adoption. Technological advancements in minimally invasive procedures improve patient outcomes and recovery time. Increasing availability of specialized surgical centers further supports growth. Surgeons are increasingly adopting innovative techniques for better precision. Growing awareness among patients regarding surgical benefits also contributes to demand. The aging population and rising neurological conditions increase the need for surgical interventions. In addition, improved healthcare infrastructure in emerging markets supports expansion. Favorable reimbursement policies in developed regions also play a role. Surgery offers long-term effectiveness compared to medication alone. Overall, the surgical segment is the fastest growing due to advancements in techniques and increasing demand for permanent solutions.

• By Drugs

On the basis of drugs, the market is segmented into Baclofen, Dantrolene Sodium, Gabapentin, and Others. The Baclofen segment dominated the largest market revenue share of 41.8% in 2025, driven by its high efficacy in reducing muscle spasticity and its widespread clinical use. Baclofen is commonly prescribed for conditions such as multiple sclerosis and spinal cord injuries. Its ability to act directly on the central nervous system enhances muscle relaxation. Physicians prefer baclofen due to its proven effectiveness and availability in multiple formulations. Intrathecal baclofen therapy is gaining popularity for severe cases. Increasing patient awareness and accessibility further support segment growth. The drug is often used in long-term treatment plans. Continuous research and development improve its safety profile. The availability of generic versions makes it cost-effective. Strong adoption across hospitals and clinics contributes to its dominance. In addition, its compatibility with combination therapies enhances outcomes. Overall, baclofen remains the leading drug segment due to its effectiveness and widespread usage.

The Gabapentin segment is expected to witness the fastest CAGR of 9.2% from 2026 to 2033, driven by its increasing use in managing neuropathic pain and spasticity-related symptoms. Gabapentin offers dual benefits, making it a preferred choice in complex cases. Growing awareness among healthcare providers supports its adoption. The drug is increasingly prescribed as part of combination therapy. Rising prevalence of neurological disorders boosts demand. Its favorable safety profile compared to traditional muscle relaxants enhances patient compliance. Pharmaceutical advancements improve its formulation and effectiveness. Increasing research into new indications further expands its application. The expansion of healthcare access in emerging markets also contributes to growth. In addition, rising off-label usage supports demand. Strong distribution networks ensure availability. Overall, gabapentin is the fastest-growing segment due to its versatility and increasing clinical acceptance.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Intramuscular, and Others. The Oral segment dominated the largest market revenue share of 57.9% in 2025, driven by its convenience, ease of administration, and high patient compliance. Oral medications are widely prescribed for long-term management of spasticity. Patients prefer oral routes due to non-invasiveness and accessibility. The availability of multiple oral drug options further supports segment growth. Healthcare providers recommend oral therapy as a first-line treatment. Increasing awareness about early treatment boosts demand. Oral drugs are cost-effective and easily available through pharmacies. Technological advancements improve drug absorption and efficacy. Strong distribution channels ensure widespread accessibility. In addition, oral therapies are often combined with physical therapy for better outcomes. The growing prevalence of neurological disorders increases usage. Overall, oral administration dominates due to convenience and widespread adoption.

The Intramuscular segment is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by its effectiveness in targeted muscle treatment. Intramuscular injections provide faster and more localized relief compared to oral medications. Increasing use of botulinum toxin injections significantly contributes to growth. Physicians prefer this route for severe or localized spasticity cases. Rising awareness regarding advanced treatment options supports adoption. Technological advancements improve precision and safety of injections. Growing demand for minimally invasive treatments further boosts the segment. Expansion of specialty clinics enhances accessibility. Increasing patient preference for quicker results supports demand. In addition, improved healthcare infrastructure drives growth. Intramuscular treatments are often used alongside rehabilitation therapies. Overall, this segment is the fastest growing due to effectiveness and targeted treatment benefits.

• By Indication

On the basis of indication, the market is segmented into Multiple Sclerosis (MS), Cerebral Palsy (CP), Traumatic Brain Injury (TBI), and Others. The Multiple Sclerosis (MS) segment dominated the largest market revenue share of 38.6% in 2025, driven by the high prevalence of spasticity among MS patients. Spasticity is one of the most common symptoms of MS, requiring long-term management. Increasing global incidence of MS significantly contributes to segment growth. Healthcare providers focus on early intervention to improve patient outcomes. Availability of multiple treatment options supports demand. Growing awareness among patients enhances diagnosis and treatment rates. Continuous research into MS therapies further strengthens the segment. Rehabilitation therapies are widely used alongside medications. Strong healthcare infrastructure in developed regions supports growth. Pharmaceutical advancements improve treatment effectiveness. Increasing patient support programs also contribute. Overall, MS remains the dominant indication segment due to high disease burden.

The Cerebral Palsy (CP) segment is expected to witness the fastest CAGR of 9.0% from 2026 to 2033, driven by increasing diagnosis rates and improved access to pediatric care. CP-related spasticity requires long-term and multidisciplinary treatment approaches. Growing awareness among parents and caregivers supports early intervention. Advances in rehabilitation therapies significantly improve patient outcomes. Increasing government initiatives for pediatric healthcare boost growth. The adoption of assistive technologies further supports treatment. Rising investments in pediatric specialty clinics contribute to expansion. In addition, improved diagnostic capabilities enhance case detection. Increasing demand for personalized treatment plans drives adoption. Expansion of homecare services also supports growth. Strong focus on improving quality of life accelerates demand. Overall, CP is the fastest-growing segment due to rising awareness and treatment advancements.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated the largest market revenue share of 49.5% in 2025, driven by high patient inflow and availability of specialized treatments. Hospitals are primary centers for spasticity diagnosis and treatment. Patients prefer hospital pharmacies for reliable and prescribed medications. Availability of advanced drugs supports segment growth. Healthcare professionals ensure proper medication management. Increasing hospitalization rates further boost demand. Strong infrastructure and supply chains support availability. Hospitals also provide combination therapies, increasing utilization. Government support for hospital infrastructure enhances growth. Integration with treatment plans ensures continuous demand. The presence of skilled professionals further supports adoption. Overall, hospital pharmacies dominate due to trust and accessibility.

The Online Pharmacy segment is expected to witness the fastest CAGR of 10.3% from 2026 to 2033, driven by increasing digitalization and convenience. Patients prefer online platforms for easy access to medications. Growth in e-commerce and telemedicine supports adoption. Competitive pricing and home delivery services attract consumers. Increasing internet penetration further boosts growth. Online pharmacies offer a wide range of products. Rising awareness about digital healthcare supports expansion. Regulatory improvements enhance trust in online platforms. Growing preference for contactless services also contributes. Expansion in emerging markets accelerates adoption. Overall, online pharmacies are the fastest-growing segment due to convenience and digital transformation.

• By End-Users

On the basis of end-users, the market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. The Hospitals segment dominated the largest market revenue share of 46.8% in 2025, driven by the availability of comprehensive treatment facilities. Hospitals handle severe and complex spasticity cases requiring multidisciplinary care. Presence of skilled professionals ensures effective treatment. Advanced infrastructure supports diagnosis and therapy. High patient inflow contributes to demand. Hospitals provide both medical and surgical treatments. Increasing healthcare investments further support growth. Strong reimbursement policies enhance accessibility. Integration of rehabilitation services boosts utilization. Continuous monitoring ensures better outcomes. Overall, hospitals dominate due to comprehensive care capabilities.

The Homecare segment is expected to witness the fastest CAGR of 9.6% from 2026 to 2033, driven by increasing preference for at-home treatment and rehabilitation. Patients prefer homecare for convenience and cost-effectiveness. Growing aging population supports demand. Technological advancements enable remote monitoring. Expansion of home healthcare services boosts adoption. Increasing focus on patient comfort drives growth. Availability of portable medical devices supports treatment. Rising chronic disease burden further contributes. Government initiatives promoting homecare enhance adoption. Improved caregiver support systems also play a role. Overall, homecare is the fastest-growing segment due to convenience and evolving healthcare models.

Spasticity Treatment Market Regional Analysis

- North America dominated the spasticity treatment market with the largest revenue share of 39.1% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative therapies, and a strong presence of key pharmaceutical and medical device companies. The region continues to benefit from well-established neurological care frameworks, increasing diagnosis rates of spasticity-related conditions, and growing use of advanced treatment options such as botulinum toxin therapies and intrathecal baclofen pumps

- Healthcare providers in the region increasingly rely on multidisciplinary treatment approaches, including pharmacological therapy, physical rehabilitation, and minimally invasive procedures, which is supporting higher treatment adoption and improved patient outcomes

- This growth is further supported by strong clinical research activity, favorable reimbursement systems, and continuous innovation in neurology and rehabilitation therapies, making North America a key revenue-contributing region in the global spasticity treatment market

U.S. Spasticity Treatment Market Insight

The U.S. spasticity treatment market captured a dominant revenue share within North America in 2025, driven by increasing diagnosis rates of neurological disorders and strong availability of advanced treatment options. The country benefits from a well-developed healthcare system, high patient awareness, and widespread access to neurologists and rehabilitation specialists. For instance, hospitals and specialty clinics in the U.S. are increasingly utilizing botulinum toxin injections and intrathecal baclofen therapy for managing both focal and generalized spasticity. In addition, ongoing clinical research and strong presence of leading pharmaceutical companies are further enhancing treatment accessibility and effectiveness.

Europe Spasticity Treatment Market Insight

The Europe spasticity treatment market is projected to expand at a steady CAGR during the forecast period, supported by increasing prevalence of neurological disorders and strong public healthcare systems. Growing awareness regarding early intervention and rehabilitation is encouraging the adoption of standardized treatment protocols. For instance, several European countries are expanding neuro-rehabilitation programs to support patients with stroke and multiple sclerosis. The region’s focus on improving long-term patient outcomes and quality of life is further supporting market growth.

U.K. Spasticity Treatment Market Insight

The U.K. spasticity treatment market is anticipated to grow steadily during the forecast period, driven by increasing demand for neurological care services and strong support from the National Health Service (NHS). For instance, NHS-backed rehabilitation programs are increasingly incorporating physiotherapy and pharmacological treatments for spasticity management. Growing awareness among patients and healthcare professionals regarding early treatment is further contributing to market expansion.

Germany Spasticity Treatment Market Insight

The Germany spasticity treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure and high adoption of innovative medical therapies. For instance, German healthcare providers are increasingly utilizing combination treatment approaches, including botulinum toxin injections and physiotherapy, to improve patient outcomes. The country’s strong emphasis on precision medicine and rehabilitation services is further driving market growth.

Asia-Pacific Spasticity Treatment Market Insight

The Asia-Pacific spasticity treatment market is expected to be the fastest growing region during the forecast period due to rising healthcare expenditure, increasing awareness of neurological conditions, and expanding access to rehabilitation and specialty care services in countries such as China and India. For instance, governments in these countries are investing in healthcare infrastructure and rehabilitation centers to support growing patient populations. Increasing diagnosis rates and improved access to treatment are further accelerating market growth in the region.

Japan Spasticity Treatment Market Insight

The Japan spasticity treatment market is gaining momentum due to its advanced healthcare system, rapidly aging population, and strong focus on neurological care. For instance, Japanese hospitals are increasingly adopting advanced therapies such as intrathecal baclofen pumps and targeted rehabilitation programs for elderly patients. The country’s emphasis on improving quality of life and long-term care outcomes is further supporting market expansion.

China Spasticity Treatment Market Insight

The China spasticity treatment market accounted for a significant revenue share in Asia Pacific in 2025, driven by expanding healthcare infrastructure, increasing awareness of neurological disorders, and rising demand for rehabilitation services. For instance, large hospitals and rehabilitation centers in urban areas are increasingly adopting advanced treatment options for spasticity management. Strong government initiatives, growing healthcare investments, and improving access to specialized care are further enhancing the availability and adoption of spasticity treatment solutions across the country.

Spasticity Treatment Market Share

The Spasticity Treatment industry is primarily led by well-established companies, including:

- Ipsen Pharma (France)

- Merz Pharma (Germany)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Cipla Ltd. (India)

- Lupin Limited (India)

- Aurobindo Pharma Ltd. (India)

- Zydus Lifesciences Ltd. (India)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Johnson & Johnson (U.S.)

- Bayer AG (Germany)

- GlaxoSmithKline plc (U.K.)

- Sanofi (France)

- Hikma Pharmaceuticals PLC (U.K.)

- Viatris Inc. (U.S.)

- Sandoz Group AG (Switzerland)

- Endo International plc (Ireland)

Latest Developments in Global Spasticity Treatment Market

- In December 2021, the U.S. Food and Drug Administration (FDA) approved Lyvispah (baclofen oral granules) developed by Saol Therapeutics for the treatment of spasticity associated with multiple sclerosis, introducing a novel formulation designed for patients with swallowing difficulties and enabling administration with soft food or feeding tubes

- In January 2022, Amneal Pharmaceuticals, Inc. announced the acquisition of Saol Therapeutics’ baclofen franchise, including Lyvispah and Lioresal (intrathecal baclofen), strengthening its neurology portfolio and expanding its presence in the spasticity treatment market

- In February 2022, Azurity Pharmaceuticals received U.S. FDA approval for Fleqsuvy (baclofen oral suspension), providing an alternative liquid formulation for patients with spasticity, particularly benefiting those who have difficulty swallowing tablets or require precise dose titration

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.