Global Specialty Carbon Black Market

Market Size in USD Billion

USD

3.14 Billion

USD

5.66 Billion

2024

2032

USD

3.14 Billion

USD

5.66 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.14 Billion | |

| USD 5.66 Billion | |

| % | |

|

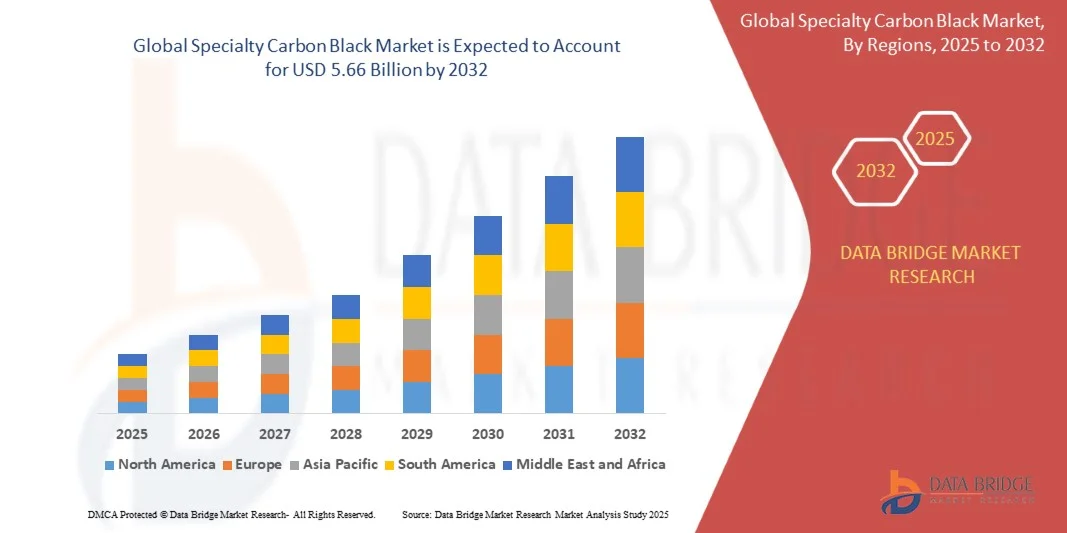

Specialty Carbon Black Market Size

- The Specialty Carbon Black Market size was valued at USD 3.14 billion in 2024 and is projected to reach USD 5.66 billion by 2032, growing at a CAGR of 7.66% during the forecast period.

- The market expansion is primarily driven by the rising demand for high-performance coatings, plastics, and battery electrodes, coupled with rapid industrialization and technological advancements in manufacturing processes.

- Additionally, the increasing use of specialty carbon black in electric vehicles, conductive polymers, and sustainable packaging materials is creating strong growth opportunities, positioning it as a crucial material for next-generation industrial and energy applications.

Specialty Carbon Black Market Analysis

- Specialty carbon black, a high-purity form of carbon black used to enhance conductivity, color, UV protection, and performance in various materials, is becoming increasingly essential across industries such as automotive, plastics, coatings, and electronics due to its superior physical and chemical properties.

- The growing demand for specialty carbon black is primarily fueled by the rapid expansion of the automotive and electronics sectors, rising adoption of electric vehicles, and increasing need for advanced materials with improved conductivity and durability.

- Asia-Pacific dominated the Specialty Carbon Black Market with the largest revenue share of 33.7% in 2024, supported by strong demand from the automotive and construction industries, technological advancements, and the presence of major manufacturers focusing on product innovation and sustainable production methods.

- North America is expected to be the fastest-growing region in the Specialty Carbon Black Market during the forecast period due to increasing industrialization, urbanization, and expanding manufacturing activities in countries such as China, India, and Japan.

- The powder segment dominated the market with the largest revenue share of 58.7% in 2024, owing to its widespread use in applications requiring fine dispersion and high surface area, such as coatings, inks, and conductive polymers.

Report Scope and Specialty Carbon Black Market Segmentation

|

Attributes |

Specialty Carbon Black Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Specialty Carbon Black Market Trends

“Enhanced Performance Through Advanced Functionalization and Sustainability”

- A significant and accelerating trend in the Specialty Carbon Black Market is the development of advanced functionalization techniques and sustainable production processes that enhance product performance while reducing environmental impact. These innovations are enabling specialty carbon black to meet the increasingly stringent requirements of industries such as automotive, electronics, and energy storage.

- For instance, functionalized specialty carbon blacks with improved dispersion and surface chemistry are being used to enhance the conductivity and durability of battery electrodes and conductive polymers. Similarly, bio-based and recycled carbon blacks are gaining traction as eco-friendly alternatives, aligning with global sustainability goals.

- Advances in material science are enabling specialty carbon blacks to provide enhanced UV protection, better reinforcement in rubber and plastics, and improved electrical conductivity, which are critical for applications like electric vehicle batteries and high-performance coatings. Furthermore, manufacturers are focusing on reducing carbon footprint through energy-efficient production and waste minimization strategies.

- The integration of specialty carbon black into next-generation energy storage solutions, such as lithium-ion and solid-state batteries, supports the transition to cleaner energy and electric mobility. Companies like Cabot Corporation and Orion Engineered Carbons are investing heavily in R&D to develop customized carbon black variants tailored for these advanced applications.

- This trend towards higher performance, sustainability, and customization is driving product innovation and setting new industry standards. As a result, market leaders are collaborating with automotive, electronics, and chemical manufacturers to co-develop specialty carbon black products that meet evolving technical and environmental demands.

- The demand for specialty carbon black with enhanced functional properties and sustainable credentials is growing rapidly across various sectors, as industries seek materials that combine performance excellence with ecological responsibility.

Specialty Carbon Black Market Dynamics

Driver

“Growing Need Due to Increasing Demand for High-Performance and Sustainable Materials”

- The rising demand for specialty carbon black is largely driven by its critical role in enhancing the performance and durability of products across automotive, electronics, and energy storage industries, alongside growing emphasis on sustainability and eco-friendly manufacturing.

- For instance, in early 2024, Cabot Corporation announced advancements in developing low-emission, bio-based specialty carbon black products aimed at reducing the carbon footprint of rubber and plastic applications. Such innovations by leading companies are expected to significantly propel market growth during the forecast period.

- As industries seek materials that improve conductivity, UV protection, and reinforcement while aligning with environmental regulations, specialty carbon black offers compelling benefits over traditional alternatives. These include improved battery performance, lighter automotive components, and longer-lasting coatings.

- Furthermore, the increasing adoption of electric vehicles and renewable energy technologies is driving demand for specialty carbon blacks that enhance battery efficiency and durability, positioning it as a vital component in the global transition to cleaner energy solutions.

- The trend toward lightweight, high-strength, and sustainable materials in manufacturing is further accelerating the uptake of specialty carbon black across diverse applications, supported by growing industrialization and urbanization in emerging markets.

Restraint/Challenge

Concerns Regarding Environmental Impact and Raw Material Costs

- Environmental concerns related to the carbon black production process, including emissions and energy consumption, pose a significant challenge to the broader adoption and expansion of specialty carbon black products. Stricter environmental regulations worldwide increase compliance costs and operational complexity for manufacturers.

- For Instance, regulatory pressures in key markets such as Europe and North America have prompted companies to invest heavily in cleaner production technologies and emissions control systems, which can raise product costs and impact pricing competitiveness.

- Additionally, fluctuations in raw material prices, such as feedstock for carbon black production, create cost uncertainties that may hinder market growth, particularly in price-sensitive regions and industries.

- Addressing these challenges requires ongoing innovation in sustainable production methods, such as bio-based feedstocks and energy-efficient processes, alongside efforts to optimize supply chains and reduce manufacturing costs. Companies like Orion Engineered Carbons and Tokai Carbon are actively focusing on these areas to balance environmental responsibility with economic viability.

- While specialty carbon black products with enhanced sustainability credentials are gaining market traction, the initial higher costs and complexity of green technologies may slow adoption among certain segments. Overcoming these barriers through technological advancements, government incentives, and increased consumer awareness will be crucial for long-term market growth.

Specialty Carbon Black Market Scope

The specialty carbon market is segmented on the basis of form, grade, function, process type, and application.

- By Form

On the basis of form, the Specialty Carbon Black Market is segmented into granules and powder. The powder segment dominated the market with the largest revenue share of 58.7% in 2024, owing to its widespread use in applications requiring fine dispersion and high surface area, such as coatings, inks, and conductive polymers. Powdered specialty carbon black provides better consistency and performance in enhancing color strength, conductivity, and UV protection.

The granules segment is expected to witness the fastest CAGR of 19.4% from 2025 to 2032, driven by its ease of handling, reduced dust generation, and growing adoption in rubber compounding and battery electrode manufacturing. Granular forms are preferred in industrial processes that require safer and more efficient handling of carbon black powders, supporting increased production efficiency and workplace safety.

- By Grade

On the basis of grade, the Specialty Carbon Black Market is segmented into conductive carbon black, fiber carbon black, and food carbon black. The conductive carbon black segment held the largest market revenue share of 45.3% in 2024, fueled by rising demand in battery electrodes, conductive plastics, and electronics applications where high electrical conductivity is critical. Conductive carbon blacks improve energy storage efficiency and provide electromagnetic interference (EMI) shielding, making them indispensable in advanced technologies.

Fiber carbon black is anticipated to experience the fastest CAGR of 21.2% during the forecast period, as its reinforcement properties in composite materials and specialty fibers gain traction, especially in automotive and aerospace industries. Food carbon black, used as a coloring and additive agent, is growing steadily but represents a smaller market share compared to industrial grades.

- By Function

On the basis of function, the Specialty Carbon Black Market is segmented into color, UV protection, conductive, and others. The color segment dominated the market with a 50.5% revenue share in 2024, driven by its extensive use in inks, paints, plastics, and coatings to enhance pigmentation and opacity. Specialty carbon black’s superior tinting strength and stability make it a preferred choice for color applications across industries.

The conductive segment is expected to register the fastest CAGR of 22.1% from 2025 to 2032, supported by expanding use in electric vehicle batteries, electronic devices, and conductive polymers. The UV protection segment is also growing, attributed to increasing demand for materials that resist degradation in outdoor and high-exposure environments, particularly in automotive and packaging sectors.

- By Process Type

On the basis of process type, the Specialty Carbon Black Market is segmented into furnace black, gas black, lamp black, and thermal black. The furnace black segment accounted for the largest market revenue share of 61.4% in 2024, due to its cost-effectiveness and adaptability in producing various grades of specialty carbon black with tailored properties. Furnace black is widely used in rubber reinforcement, plastics, and coatings, making it the backbone of the specialty carbon black industry.

Thermal black is expected to witness the fastest CAGR of 20.3% during the forecast period, driven by its superior purity and performance in high-end applications such as battery electrodes and conductive polymers. Gas black and lamp black segments hold smaller shares but serve niche applications requiring specific physical and chemical properties.

- By Application

On the basis of application, the Specialty Carbon Black Market is segmented into plastics, battery electrodes, paints and coatings, inks and toners, rubber, and others. The plastics segment dominated the market with the largest revenue share of 38.9% in 2024, due to growing use of specialty carbon black for color enhancement, UV resistance, and electrical conductivity in consumer goods and automotive components.

The battery electrodes segment is anticipated to register the fastest CAGR of 23.5% from 2025 to 2032, fueled by rapid growth in electric vehicle production and energy storage systems that require high-performance conductive materials. Paints and coatings, inks and toners, and rubber applications also contribute significantly to the market, driven by demand for improved durability, aesthetics, and functional properties.

Specialty Carbon Black Market Regional Analysis

- Asia-Pacific dominated the Specialty Carbon Black Market with the largest revenue share of 33.7% in 2024, driven by strong demand from automotive, electronics, and energy storage industries.

- The region benefits from advanced manufacturing infrastructure, technological innovation, and stringent environmental regulations that encourage the use of high-performance and sustainable specialty carbon black products.

- High disposable incomes, well-established industrial sectors, and ongoing investments in electric vehicle production and renewable energy technologies further support market growth. Additionally, North America’s focus on research and development facilitates the adoption of customized specialty carbon black grades tailored to specific applications, reinforcing its leadership position in the global market.

U.S. Specialty Carbon Black Market Insight

The U.S. specialty carbon black market captured the largest revenue share of 81% in North America in 2024, driven by strong demand from the automotive, electronics, and energy storage sectors. The rapid growth of electric vehicles and renewable energy technologies is boosting the need for high-performance conductive and reinforcing carbon blacks. Additionally, the country’s well-established manufacturing base, ongoing R&D investments, and regulatory focus on sustainable materials are accelerating market expansion. The increasing integration of specialty carbon black in battery electrodes, plastics, and coatings further supports the market’s robust growth trajectory.

Europe Specialty Carbon Black Market Insight

The Europe specialty carbon black market is projected to grow at a substantial CAGR during the forecast period, driven by stringent environmental regulations and a rising emphasis on sustainable production practices. The demand for specialty carbon black in automotive lightweighting, renewable energy storage, and industrial applications is surging. Europe’s advanced industrial infrastructure and increasing adoption of green technologies in countries such as Germany, France, and the UK underpin market growth. The region is witnessing expanding applications across electric vehicle batteries, conductive polymers, and high-performance coatings, fueled by innovation and regulatory compliance.

U.K. Specialty Carbon Black Market Insight

The U.K. specialty carbon black market is expected to grow at a noteworthy CAGR, supported by increased investments in advanced manufacturing and clean energy sectors. Growing awareness of environmental impact and government initiatives promoting sustainable materials adoption are driving demand. The country’s focus on electrification and innovation in battery technology is also fostering growth in specialty carbon black usage, particularly in automotive and electronics industries. Additionally, the U.K.’s strategic position as a hub for research and development facilitates partnerships that accelerate product development and market penetration.

Germany Specialty Carbon Black Market Insight

The Germany specialty carbon black market is anticipated to expand at a significant CAGR during the forecast period, driven by the country’s leadership in automotive manufacturing and renewable energy technologies. Germany’s commitment to sustainability and innovation encourages the use of eco-friendly specialty carbon blacks in battery electrodes, plastics, and coatings. The presence of key global manufacturers and robust industrial infrastructure supports market growth. Integration of specialty carbon black into lightweight materials and energy-efficient products aligns with Germany’s stringent environmental standards and consumer demand for high-performance sustainable solutions.

Asia-Pacific Specialty Carbon Black Market Insight

The Asia-Pacific specialty carbon black market is poised to grow at the fastest CAGR of 24% from 2025 to 2032, fueled by rapid industrialization, urbanization, and rising disposable incomes in countries such as China, India, Japan, and South Korea. The expanding electric vehicle market, coupled with government initiatives supporting clean energy and smart manufacturing, is driving demand for specialty carbon black in battery electrodes and conductive applications. Additionally, Asia-Pacific’s emergence as a major manufacturing hub for automotive and electronics components is increasing the availability and affordability of specialty carbon black products, further accelerating regional growth.

Japan Specialty Carbon Black Market Insight

The Japan specialty carbon black market is gaining momentum due to the country’s focus on advanced technology, automotive innovation, and renewable energy. Japan’s automotive and electronics sectors heavily rely on specialty carbon black for enhancing product performance, particularly in batteries and conductive materials. The aging population and demand for energy-efficient technologies are also driving adoption. Integration with IoT and smart energy solutions further fuels growth. Japan’s emphasis on sustainability and cutting-edge research strengthens its position as a key market for specialty carbon black innovations.

China Specialty Carbon Black Market Insight

The China specialty carbon black market accounted for the largest revenue share in Asia-Pacific in 2024, driven by rapid urbanization, a growing middle class, and massive industrial expansion. China’s leadership in electric vehicle production and energy storage technology is a major catalyst, with specialty carbon black being crucial in battery electrode manufacturing and conductive applications. Government initiatives promoting smart cities and clean energy adoption, along with competitive domestic manufacturers, are significantly propelling market growth. The availability of cost-effective specialty carbon black variants supports widespread adoption across automotive, electronics, and industrial sectors.

Specialty Carbon Black Market Share

The Specialty Carbon Black industry is primarily led by well-established companies, including:

- Cabot Corporation (U.S.)

- Orion Engineered Carbons (Germany)

- Tokai Carbon (Japan)

- Mitsubishi Chemical Corporation (Japan)

- Cancarb (Canada)

- Jiangxi Black Cat Carbon Black (China)

- Sid Richardson Carbon & Energy (U.S.)

- Continental Carbon (U.S.)

- Jiangsu Carbon Black (China)

- Shenzhen Sanshun Carbon (China)

- Aditya Birla Group (India)

- Sid Richardson Carbon & Energy (U.S.)

- China Synthetic Rubber Corporation (Taiwan)

- Cabot Norit Activated Carbon (Netherlands)

- Sid Richardson Carbon & Energy (U.S.)

- Huber Carbon Black (U.S.)

- Continental Carbon (U.S.)

- NGC (Japan)

- Continental Carbon (U.S.)

What are the Recent Developments in Specialty Carbon Black Market?

- In April 2023, Cabot Corporation, a leading global specialty carbon black manufacturer, announced the expansion of its production capacity in Asia to meet rising demand for high-performance carbon black in battery electrodes and conductive applications. This strategic move highlights Cabot’s commitment to supporting the growing electric vehicle and electronics industries, reinforcing its position as a key supplier in the expanding Specialty Carbon Black Market.

- In March 2023, Orion Engineered Carbons unveiled a new line of conductive specialty carbon blacks tailored for advanced energy storage applications. Designed to improve battery efficiency and durability, this innovation underscores Orion’s focus on technological advancement and sustainability within the specialty carbon black sector, aiming to address evolving needs in automotive and renewable energy markets.

- In March 2023, Birla Carbon, part of the Aditya Birla Group, launched a new eco-friendly carbon black product line aimed at reducing environmental impact without compromising performance. This initiative supports growing regulatory pressures and customer demand for greener materials, positioning Birla Carbon as a frontrunner in sustainable specialty carbon black production globally.

- In February 2023, Phillips Carbon Black Limited entered into a strategic partnership with a leading battery manufacturer to co-develop specialty carbon black formulations optimized for next-generation lithium-ion batteries. This collaboration is set to accelerate innovation in the energy storage sector and enhance market reach, demonstrating Phillips Carbon Black’s commitment to technological excellence and market expansion.

- In January 2023, Tokai Carbon Co., Ltd. announced the launch of a new high-dispersion specialty carbon black product designed for use in high-performance coatings and inks. Presented at a major international trade show, this product emphasizes Tokai’s dedication to innovation and quality, catering to the growing demand for advanced materials in automotive and industrial applications within the Specialty Carbon Black Market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Specialty Carbon Black Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Specialty Carbon Black Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Specialty Carbon Black Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.