Global Specialty Vehicle Market

Market Size in USD Billion

USD

93.14 Billion

USD

127.56 Billion

2025

2033

USD

93.14 Billion

USD

127.56 Billion

2025

2033

| 2026 - 2033 | |

| USD 93.14 Billion | |

| USD 127.56 Billion | |

| % | |

|

What is the Global Specialty Vehicle Market Size and Growth Rate?

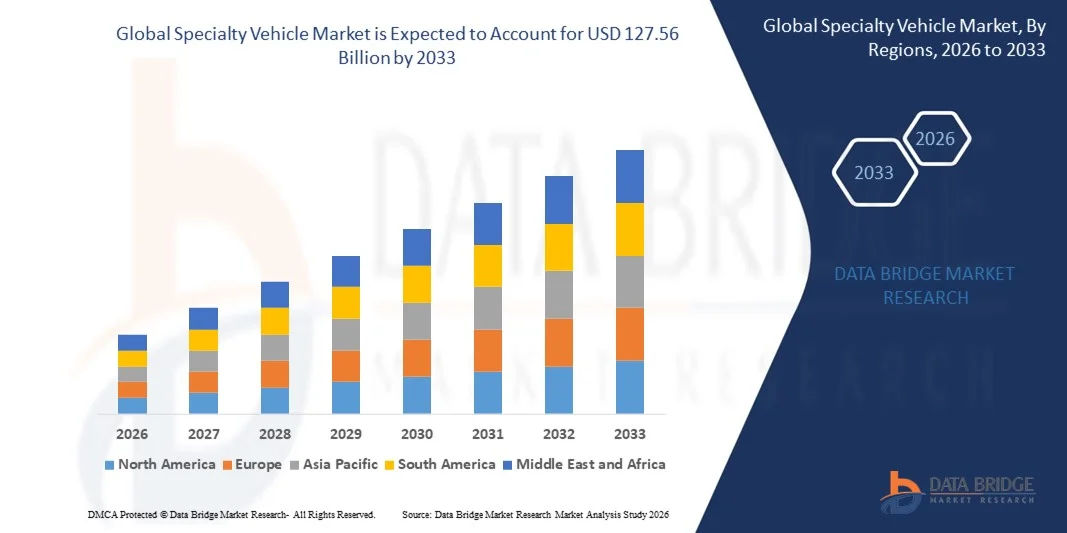

- The global specialty vehicle market size was valued at USD 93.14 billion in 2025 and is expected to reach USD 127.56 billion by 2033, at a CAGR of4.01% during the forecast period

- Increasing demand for advanced emergency response vehicles, rising investments in defense modernization programs, growing need for rapid medical deployment units, expansion of airport ground support infrastructure, and modernization of municipal service fleets are some of the major as well as vital factors which will likely augment the growth of the Specialty Vehicle market

What are the Major Takeaways of Specialty Vehicle Market?

- Growing urbanization, rising public safety investments, and increasing government funding for fire, rescue, and healthcare mobility solutions across developing economies will further contribute by generating massive opportunities that will lead to the growth of the Specialty Vehicle market

- High procurement and maintenance costs, complex customization requirements, long replacement cycles, and budget constraints among municipal agencies which will such asly act as market restraint factors for the growth of the Specialty Vehicle market

- North America dominated the specialty vehicle market with a 36.32% revenue share in 2025, driven by strong investments in emergency response infrastructure, defense modernization programs, airport expansion projects, and municipal fleet upgrades across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 8.36% from 2026 to 2033, driven by rapid urbanization, increasing defense spending, airport infrastructure expansion, and strengthening emergency healthcare systems across China, Japan, India, South Korea, and Southeast Asia

- The Fire and Rescue Vehicles segment dominated the market with a 29.7% share in 2025, driven by continuous investments in emergency response infrastructure, rising urban fire incidents, and fleet modernization programs across municipalities

Report Scope and Specialty Vehicle Market Segmentation

|

Attributes |

Specialty Vehicle Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Specialty Vehicle Market?

Growing Integration of Electrification, Smart Technologies, and Custom-Built Platforms

- The specialty vehicle market is witnessing strong adoption of electric and hybrid-powered platforms designed to improve fuel efficiency, reduce emissions, and comply with stringent environmental regulations across municipal, defense, and airport operations

- Manufacturers are introducing smart telematics systems, advanced safety features, AI-enabled fleet management tools, and modular vehicle architectures that enhance operational efficiency and real-time monitoring capabilities

- Growing demand for customized, mission-specific vehicles is driving development of application-based configurations for fire rescue, medical response, tactical missions, and airport ground handling

- For instance, companies such as Oshkosh Corporation, REV Group, Inc., Rosenbauer International AG, and Magirus GmbH are expanding electric fire trucks, advanced rescue vehicles, and modular specialty platforms

- Increasing emphasis on sustainability, rapid emergency response, and fleet modernization is accelerating innovation across the sector

- As urban infrastructure and public safety requirements evolve, Specialty Vehicles will remain critical for mission-ready mobility, operational efficiency, and next-generation emergency services

What are the Key Drivers of Specialty Vehicle Market?

- Rising government investments in emergency response infrastructure, defense modernization, and healthcare mobility solutions are significantly driving demand

- For instance, in 2025, Oshkosh Corporation and Morita Holdings Corporation expanded their advanced firefighting and rescue vehicle portfolios to address growing global safety requirements

- Increasing urbanization and industrial expansion are generating higher demand for municipal service vehicles, utility trucks, and mobile command units

- Advancements in lightweight materials, electric drivetrains, integrated communication systems, and autonomous support features have strengthened performance and operational efficiency

- Rising airport expansion projects and defense procurement programs globally are further boosting adoption

- Supported by long-term public safety budgets and infrastructure development initiatives, the Specialty Vehicle market is expected to witness steady growth

Which Factor is Challenging the Growth of the Specialty Vehicle Market?

- High procurement costs and extensive customization requirements limit adoption among budget-constrained municipal and regional agencies

- For instance, during 2024–2025, fluctuations in steel, aluminum, and electronic component prices increased manufacturing and fleet acquisition costs for several global vendors

- Long production cycles and complex regulatory certifications delay vehicle deployment timelines

- Maintenance complexity and high lifecycle costs pose additional operational challenges for fleet operators

- Growing shift toward outsourcing and leasing models may create pricing pressure and competitive intensity

- To address these challenges, companies are focusing on modular vehicle platforms, electrification cost optimization, public-private partnerships, and enhanced aftersales support to strengthen global adoption of specialty vehicles

How is the Specialty Vehicle Market Segmented?

The market is segmented on the basis of type, propulsion type, application, and end user.

- By Type

On the basis of type, the Specialty Vehicle market is segmented into Fire and Rescue Vehicles, Medical Response Vehicles, Municipal Service Vehicles, Defense and Armored Vehicles, Airport Support and ARFF Vehicles, and Others. The Fire and Rescue Vehicles segment dominated the market with a 29.7% share in 2025, driven by continuous investments in emergency response infrastructure, rising urban fire incidents, and fleet modernization programs across municipalities. Increasing regulatory standards for safety equipment and rapid response capabilities further strengthen demand.

The Defense and Armored Vehicles segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by rising geopolitical tensions, border security requirements, and expanding military procurement budgets globally.

- By Propulsion Type

On the basis of propulsion type, the market is segmented into Internal Combustion Engine (ICE), Electric, and Others. The ICE segment dominated the market with a 71.4% share in 2025, as most specialty fleets continue to rely on diesel-powered platforms for heavy-duty performance, long operational range, and established refueling infrastructure.

The Electric segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by emission regulations, sustainability targets, and increasing deployment of electric fire trucks, ambulances, and municipal vehicles.

- By Application

On the basis of application, the market is segmented into Fire & Rescue Operations, Medical Deployment & Mobile Healthcare, Utility & Infrastructure Services, Industrial & On-Site Support, Tactical & Security Missions, Airport Ground Handling, and Others. The Fire & Rescue Operations segment dominated the market with a 27.9% share in 2025, supported by rising emergency preparedness initiatives and urban safety programs.

The Medical Deployment & Mobile Healthcare segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by expanding emergency medical services and mobile healthcare infrastructure.

- By End User

On the basis of end user, the market is segmented into Municipal & Public Agencies, Fire Departments & Emergency Agencies, Healthcare Providers & EMS Operators, Military & Defense Organizations, Industrial & Commercial Enterprises, Airport & Aviation Operators, and Others. The Municipal & Public Agencies segment dominated the market with a 31.6% share in 2025, owing to large-scale procurement of public safety and service vehicles.

The Military & Defense Organizations segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing defense modernization and tactical mobility investments globally.

Which Region Holds the Largest Share of the Specialty Vehicle Market?

- North America dominated the specialty vehicle market with a 36.32% revenue share in 2025, driven by strong investments in emergency response infrastructure, defense modernization programs, airport expansion projects, and municipal fleet upgrades across the U.S. and Canada. High adoption of advanced fire apparatus, armored vehicles, mobile healthcare units, and airport support vehicles continues to fuel demand across public safety, military, and industrial sectors

- Leading manufacturers such as Oshkosh Corporation, REV Group, Inc., and Sutphen Corporation are introducing technologically advanced electric fire trucks, next-generation rescue vehicles, and modular specialty platforms, strengthening the region’s competitive advantage. Continuous government funding, replacement of aging fleets, and integration of smart telematics solutions further support long-term expansion

- Strong regulatory frameworks, high defense budgets, advanced manufacturing ecosystems, and well-established emergency response systems further reinforce North America’s leadership position in the global Specialty Vehicle market

U.S. Specialty Vehicle Market Insight

The U.S. represents the largest contributor within North America, supported by extensive federal and state-level investments in public safety, homeland security, healthcare mobility, and military vehicle modernization. Rising procurement of advanced fire engines, ambulances, ARFF vehicles, and tactical armored platforms drives sustained demand. The presence of leading manufacturers, robust R&D capabilities, and growing adoption of electric and hybrid specialty vehicles further accelerates innovation. Expanding airport infrastructure projects and industrial safety regulations continue to strengthen long-term market growth.

Canada Specialty Vehicle Market Insight

Canada contributes significantly to regional revenue, driven by increasing modernization of municipal fleets, defense equipment upgrades, and expansion of emergency medical services. Government-backed infrastructure development programs and public safety initiatives are encouraging adoption of technologically advanced rescue vehicles and utility service platforms. Rising emphasis on sustainability is also supporting gradual integration of electric specialty vehicles across provinces.

Asia-Pacific Specialty Vehicle Market

Asia-Pacific is projected to register the fastest CAGR of 8.36% from 2026 to 2033, driven by rapid urbanization, increasing defense spending, airport infrastructure expansion, and strengthening emergency healthcare systems across China, Japan, India, South Korea, and Southeast Asia. Growing investments in disaster management capabilities, industrial safety vehicles, and municipal service fleets are accelerating regional demand. Rising local manufacturing capacity and export-focused production further enhance the region’s growth trajectory.

China Specialty Vehicle Market Insight

China is the largest contributor within Asia-Pacific, supported by rising defense procurement, large-scale airport construction projects, and expanding municipal infrastructure development. Strong domestic manufacturing capabilities and government-supported industrial policies drive adoption of fire rescue trucks, armored vehicles, and airport ground support units. Increasing disaster preparedness initiatives and industrial safety standards further stimulate demand.

Japan Specialty Vehicle Market Insight

Japan demonstrates steady growth due to its strong disaster response framework, advanced firefighting systems, and modernization of airport and industrial support fleets. High-quality engineering standards and focus on reliability encourage adoption of technologically advanced specialty vehicles. Continued infrastructure upgrades and defense readiness programs reinforce market expansion.

India Specialty Vehicle Market Insight

India is emerging as a key growth hub, supported by expanding healthcare mobility programs, state-level ambulance procurement projects, and rising defense modernization initiatives. Increasing investments in smart cities, airport expansion, and industrial infrastructure are driving demand for municipal service and utility vehicles. Government-backed manufacturing incentives further accelerate domestic production and market penetration.

South Korea Specialty Vehicle Market Insight

South Korea contributes notably due to growing defense mobility requirements, advanced airport infrastructure, and strong industrial safety regulations. Increasing procurement of tactical vehicles, emergency response fleets, and high-performance airport support units supports sustained demand. Technological innovation and expanding export capabilities further strengthen long-term market growth.

Which are the Top Companies in Specialty Vehicle Market?

The specialty vehicle industry is primarily led by well-established companies, including:

- REV Group, Inc. (U.S.)

- Oshkosh Corporation (U.S.)

- Rosenbauer International AG (Austria)

- Magirus GmbH (Iveco Group) (Germany)

- Morita Holdings Corporation (Japan)

- Sutphen Corporation (U.S.)

- Seagrave Fire Apparatus, LLC (U.S.)

- The Shyft Group, Inc. (Aebi Schmidt Group) (U.S.)

- Binz GmbH (Germany)

- Mowag GmbH (Switzerland)

What are the Recent Developments in Global Specialty Vehicle Market?

- In November 2025, Indonesia’s PT SSE unveiled the P2 Tiger 4x4 armored personnel carrier at the Defense and Security 2025 in Bangkok after successfully completing comprehensive road trials. Developed on the Celeris platform by Texelis and engineered in line with NATO standards, the vehicle is designed to meet domestic defense needs while targeting wider Southeast Asian export opportunities through its modular and high-mobility configuration, strengthening Indonesia’s regional defense manufacturing footprint

- In September 2025, Torsus launched the Terrastorm 4x4 Ambulance, purpose-built for extreme off-road and flood-affected environments. Based on the VW Crafter/MAN TGE 4Motion chassis, the ambulance integrates advanced life-support systems, high water-wading capability, reinforced suspension, and customizable configurations, enhancing emergency medical accessibility across remote European regions and setting new standards for rugged medical mobility solutions

- In July 2025, Medix Specialty Vehicles introduced an extended cab variant for its MSV-II 157 Type I ambulance, built on the Ford F-450 SuperCab/Ford F-550 SuperCab platform. The upgraded configuration improves crew comfort, workspace efficiency, and onboard storage capacity, supporting EMS and fire departments with enhanced operational flexibility and reinforcing Medix’s competitive positioning in the U.S. emergency vehicle market

- In February 2025, Shell Oman deployed the nation’s first 7.5KL mobile fuel tanker equipped with advanced safety technologies including electronic stability control, rollover prevention systems, and fatigue monitoring features. The innovation significantly improves fuel distribution safety and operational efficiency within Oman’s energy infrastructure, establishing a new benchmark for specialty utility and work vehicle standards in the region

- In January 2025, Force Motors Limited secured a major contract to deliver 2,429 ambulances to the Uttar Pradesh Government Health Department. The Force Traveller Ambulance, offered in BLS, ALS, and Mobile Medical Unit variants, enhances emergency healthcare delivery with improved safety, comfort, and reliability features, further solidifying Force Motors’ leadership in India’s specialty vehicle and emergency transport sector

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.