Global Spina Bifida Hydrocephalus Market

Market Size in USD Billion

USD

4.64 Billion

USD

8.52 Billion

2024

2032

USD

4.64 Billion

USD

8.52 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.64 Billion | |

| USD 8.52 Billion | |

| % | |

|

SPINA Bifida & Hydrocephalus Market Size

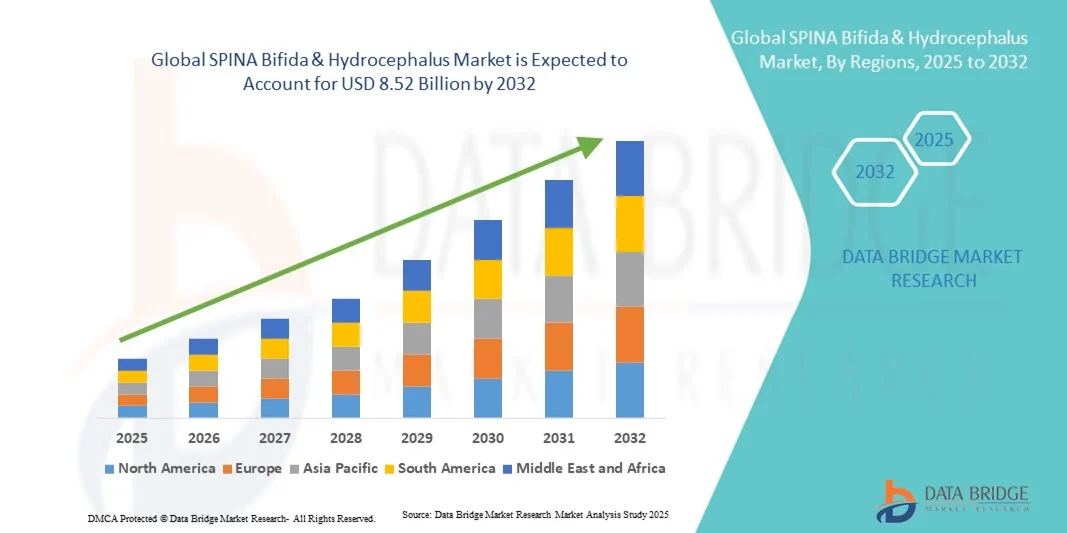

- The global SPINA Bifida & hydrocephalus market size was valued at USD 4.64 billion in 2024 and is expected to reach USD 8.52 billion by 2032, at a CAGR of7.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of neural tube defects globally and continuous advancements in prenatal diagnostic technologies, which have enhanced early detection and intervention for spina bifida and hydrocephalus cases

- Furthermore, rising awareness among healthcare professionals and patients, coupled with growing government initiatives to improve neonatal and maternal healthcare, is accelerating the adoption of advanced treatment and management solutions for spina bifida & hydrocephalus, thereby significantly boosting the industry’s growth

SPINA Bifida & Hydrocephalus Market Analysis

- The Spina Bifida & Hydrocephalus market is witnessing steady growth, primarily driven by the rising prevalence of congenital neurological disorders and increased access to advanced prenatal and postnatal healthcare services. Growing awareness about early diagnosis, coupled with the availability of improved neurosurgical techniques and shunt systems, continues to enhance patient outcomes globally

- The demand for spina bifida & hydrocephalus treatment solutions is further supported by government initiatives, research funding, and the introduction of advanced neuroimaging and minimally invasive surgical technologies. Increasing collaborations between healthcare institutions and research organizations are fostering innovation in both diagnostics and treatment

- North America dominated the spina bifida & hydrocephalus market with the largest revenue share of 43.5% in 2024, supported by a robust healthcare infrastructure, early access to advanced neurosurgical care, and a strong presence of leading medical device manufacturers. The U.S. market particularly benefits from increased awareness programs, better insurance coverage for rare congenital disorders, and continuous technological innovations in shunt and catheter systems

- Asia-Pacific is expected to be the fastest-growing region in the spina bifida & hydrocephalus market during the forecast period, registering a CAGR of 23.6% from 2025 to 2032, driven by expanding healthcare access, improving neonatal care infrastructure, and growing awareness of congenital anomalies in countries such as India, China, and Japan

- The Surgeries segment captured the largest market revenue share of 49.5% in 2024, as surgical intervention remains the primary approach for managing severe neural tube defects and cerebrospinal fluid accumulation

Report Scope and SPINA Bifida & Hydrocephalus Market Segmentation

|

Attributes |

SPINA Bifida & Hydrocephalus Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

SPINA Bifida & Hydrocephalus Market Trends

Advancements in Gene Therapy and Early Diagnosis Technologies

- A significant and accelerating trend in the global Spina Bifida & hydrocephalus market is the integration of gene therapy, advanced imaging technologies, and AI-based diagnostic tools to enhance early detection and treatment outcomes. This convergence of medical innovations is transforming the approach to managing congenital neurological disorders

- For instance, in March 2024, Roche and Spark Therapeutics announced progress in their preclinical studies exploring adeno-associated virus (AAV)-based gene therapies aimed at repairing neural tube defects associated with Spina Bifida. Similarly, companies such as Biogen and Pfizer are investing in neuromodulation and regenerative technologies to restore neural function and improve patient quality of life

- The use of artificial intelligence in neuroimaging is revolutionizing early diagnosis by enabling high-precision analysis of fetal MRI and ultrasound data to identify neural tube defects earlier in pregnancy. For instance, AI-enabled diagnostic systems developed by Siemens Healthineers and GE Healthcare enhance the detection accuracy of structural brain abnormalities linked to Hydrocephalus and Spina Bifida. Furthermore, early diagnosis enables timely surgical or medical interventions, reducing postnatal complications and long-term disability

- The adoption of minimally invasive surgical techniques such as endoscopic third ventriculostomy (ETV) and prenatal corrective surgeries is increasing globally, driven by technological advancements and growing awareness among clinicians and parents. These innovations are significantly improving survival rates and neurological outcomes for affected infants

- This growing trend towards early, gene-targeted, and image-assisted diagnosis and treatment is fundamentally reshaping the clinical landscape for Spina Bifida and Hydrocephalus. Consequently, leading healthcare firms such as Boston Scientific and Medtronic are advancing neuro-shunt and drainage technologies integrated with smart monitoring systems to manage cerebrospinal fluid (CSF) flow more effectively

- The demand for advanced diagnostic tools, gene-based therapies, and minimally invasive neurosurgical solutions is rapidly expanding across both developed and emerging markets as healthcare systems increasingly prioritize early intervention and precision medicine in congenital neurological disorders

SPINA Bifida & Hydrocephalus Market Dynamics

Driver

Rising Incidence of Neural Tube Defects and Technological Advancements in Treatment

- The increasing global prevalence of neural tube defects (NTDs), including Spina Bifida and Hydrocephalus, along with rapid advancements in neurosurgical and diagnostic technologies, is a major driver of market growth

- For instance, in June 2023, Medtronic announced the development of an advanced programmable shunt system designed to reduce the frequency of revision surgeries in Hydrocephalus management. Such innovations by key companies are expected to drive the Spina Bifida & Hydrocephalus industry growth during the forecast period

- Growing awareness about prenatal screening programs and the importance of folic acid supplementation in pregnancy are also contributing to early detection and prevention efforts. Governments and healthcare organizations across regions such as North America, Europe, and Asia-Pacific are expanding access to maternal health programs to lower birth defect rates

- Furthermore, advancements in fetal surgery and stem cell therapy have opened new avenues for treating severe forms of Spina Bifida before birth, improving both survival and mobility outcomes. Hospitals are increasingly adopting integrated care models combining pediatrics, neurosurgery, and rehabilitation services

- The integration of AI in diagnostic imaging, coupled with innovations in neuromonitoring systems and post-surgical rehabilitation devices, is expected to enhance patient management outcomes significantly. The development of portable and adaptive drainage systems is also contributing to improved post-operative care for Hydrocephalus patients

Restraint/Challenge

High Treatment Costs, Surgical Risks, and Limited Access to Specialized Care

- The high cost of surgical treatments, long-term rehabilitation, and assistive medical devices for Spina Bifida and Hydrocephalus poses a major barrier to market expansion, particularly in low- and middle-income countries. Complex procedures such as fetal repair surgeries and programmable shunt placements require specialized infrastructure and trained neurosurgeons, which limits accessibility

- For instance, several low-resource regions report limited availability of pediatric neurosurgeons and neonatal intensive care facilities, leading to delayed or suboptimal treatment outcomes for affected infants

- Addressing these disparities through increased investment in healthcare infrastructure, global aid programs, and telemedicine-driven diagnostic support is crucial for broadening patient access. Companies such as Medtronic and Integra LifeSciences are focusing on cost-optimized shunt systems to improve affordability. In addition, long-term shunt dependency and risk of infection or malfunction remain ongoing clinical challenges, increasing patient morbidity and treatment costs

- The relatively high cost of advanced neuro-monitoring devices, imaging technologies, and surgical robotics further restricts adoption in developing regions. While international NGOs and public-private partnerships are working to subsidize treatment for low-income families, affordability remains a critical issue

- Overcoming these barriers through policy support, research funding, and equitable healthcare access will be vital for ensuring sustained market growth and improved clinical outcomes in Spina Bifida and Hydrocephalus management

SPINA Bifida & Hydrocephalus Market Scope

The market is segmented on the basis of disease type, treatment, diagnosis, and end-user.

- By Disease Type

On the basis of disease type, the Spina Bifida & Hydrocephalus market is segmented into Myelomeningocele, Occulta, Closed Neural Tube Defects, and Meningocele. The Myelomeningocele segment dominated the largest market revenue share of 46.8% in 2024, primarily due to its high global incidence and complex nature requiring continuous medical intervention. Myelomeningocele represents the most severe form of Spina Bifida, leading to significant neurological and orthopedic complications. The increasing number of prenatal screenings and growing public health awareness programs focusing on neural tube defects contribute to higher diagnosis rates. Continuous advancements in prenatal surgical procedures, such as fetal closure techniques, and improvements in neonatal intensive care units (NICUs) are enhancing patient survival outcomes. Government support for congenital disorder management and research funding in major economies such as the U.S. and Japan further sustain the market’s dominance. In addition, rising adoption of minimally invasive surgeries and assistive technologies for mobility rehabilitation strengthen the growth of this segment. Strategic collaborations between healthcare organizations and non-profit groups are also improving early intervention programs. As healthcare infrastructure and maternal health awareness rise globally, the Myelomeningocele segment continues to lead the overall market.

The Occulta segment is anticipated to witness the fastest growth rate of 20.9% CAGR from 2025 to 2032, driven by the rising accessibility of advanced imaging modalities that detect previously underdiagnosed mild cases. Increasing awareness among clinicians regarding early signs of spinal abnormalities contributes to timely interventions. The segment benefits from the growing number of routine spine MRI screenings and expanding adoption of preventive care during pregnancy. Public education campaigns and improved prenatal nutrition programs emphasizing folic acid intake also play a critical role in reducing severe cases and identifying milder forms such as Occulta. Furthermore, non-invasive management approaches and targeted physiotherapy treatments are increasing treatment compliance. Technological improvements in imaging accuracy and the integration of AI-assisted diagnostics enable faster detection. As healthcare systems in emerging economies expand, early diagnosis and personalized care strategies are likely to propel the segment’s rapid growth.

- By Treatment

On the basis of treatment, the Spina Bifida & Hydrocephalus market is segmented into Medical Procedures, Surgeries, Oral Medications, and Others. The Surgeries segment captured the largest market revenue share of 49.5% in 2024, as surgical intervention remains the primary approach for managing severe neural tube defects and cerebrospinal fluid accumulation. Fetal surgery advancements, especially intrauterine repairs, have shown significant improvements in neurological outcomes and mobility. Increasing availability of trained neurosurgeons, adoption of image-guided techniques, and integration of robotic-assisted surgery systems have further strengthened this segment’s growth. Hospitals in developed countries continue to expand pediatric neurosurgery units, enhancing accessibility to critical treatments. The demand for ventriculoperitoneal shunt procedures and endoscopic third ventriculostomy (ETV) surgeries remains high. Governments and insurance providers are increasingly covering congenital disorder surgeries, improving affordability and patient outreach. The continuous launch of advanced surgical devices designed to minimize post-operative complications enhances patient recovery rates. Collaborations between surgical centers and medical technology companies are driving innovation in hydrocephalus treatment solutions. As a result, the surgeries segment maintains its leading position across global healthcare settings.

The Oral Medications segment is projected to record the fastest CAGR of 22.4% from 2025 to 2032, driven by growing interest in pharmacological therapies aimed at managing secondary neurological and developmental symptoms. Ongoing R&D in neuroprotective compounds, anti-inflammatory agents, and regenerative therapies is creating new opportunities for non-invasive management. Increasing collaborations between biotech firms and academic institutions are accelerating drug pipeline development for rare neurological disorders. The market is witnessing the introduction of oral therapies focused on reducing oxidative stress and promoting nerve regeneration. Patient preference for less invasive and home-based treatment options also contributes to segment growth. Governments in several countries are supporting orphan drug designations, encouraging faster regulatory approvals. Technological advances in drug delivery systems ensure better bioavailability and patient adherence. As pharmaceutical innovation accelerates, oral medication usage is expected to complement surgical interventions, resulting in improved long-term patient outcomes.

- By Diagnosis

On the basis of diagnosis, the Spina Bifida & Hydrocephalus market is segmented into Ultrasound, Blood Tests, Amniocentesis, and Others. The Ultrasound segment dominated the market with a revenue share of 44.3% in 2024, owing to its position as the cornerstone of prenatal diagnosis for neural tube defects. It allows early and non-invasive visualization of fetal abnormalities, contributing to rapid decision-making and timely interventions. The growing implementation of national maternal health screening programs in developed and emerging countries boosts utilization rates. The availability of high-resolution imaging devices and portable ultrasound systems enhances accessibility in remote areas. Increased government funding for prenatal health and strong adoption in hospitals and diagnostic centers continue to fuel growth. Continuous improvements in 3D and 4D imaging technologies improve precision and early detection capabilities. Rising public awareness campaigns advocating routine pregnancy scans have improved compliance rates among expectant mothers. As healthcare systems prioritize early detection of congenital disorders, ultrasound remains the gold standard diagnostic tool. Strong support from global health organizations and maternal wellness programs further cements its market dominance.

The Amniocentesis segment is anticipated to grow at the fastest CAGR of 19.7% from 2025 to 2032, owing to its exceptional diagnostic accuracy and its expanding use in high-risk pregnancy assessments. Advances in genetic testing and molecular biology allow more precise detection of chromosomal abnormalities linked with Spina Bifida and Hydrocephalus. Increasing availability of specialized maternal-fetal medicine centers and safer sampling procedures are reducing complications, improving patient confidence. Rising demand for confirmatory genetic testing in developed nations further supports adoption. The introduction of next-generation sequencing (NGS)-based amniotic fluid testing provides more comprehensive fetal health insights. Healthcare providers are increasingly integrating amniocentesis results with AI-assisted data analysis for faster interpretation. The expansion of prenatal diagnostic programs in Asia-Pacific and Europe also contributes to the segment’s growth. As awareness regarding early genetic detection continues to rise, amniocentesis is set to gain significant traction in prenatal care worldwide.

- By End-User

On the basis of end-user, the Spina Bifida & Hydrocephalus market is segmented into Hospitals, Clinics, Diagnostic Centers, Pharmacies, and Others. The Hospitals segment accounted for the largest revenue share of 53.6% in 2024, driven by their role as the primary centers for diagnosis, surgery, and post-operative rehabilitation. The availability of advanced neurosurgical equipment, multidisciplinary medical teams, and neonatal intensive care units supports superior patient outcomes. Hospitals often lead in adopting cutting-edge fetal and pediatric neurosurgical procedures, enhancing their share of patient admissions. Government and private investments in healthcare infrastructure are expanding access to specialized treatments for congenital disorders. The presence of comprehensive patient monitoring systems and specialized neurology departments ensures holistic management. Hospitals also partner with research institutes for clinical trials on innovative therapies, further strengthening their market position. Insurance coverage and reimbursement policies for surgeries and diagnostics attract more patients to hospital-based care. In addition, hospitals serve as training hubs for surgeons and healthcare professionals, reinforcing their dominance in the treatment landscape.

The Diagnostic Centers segment is projected to exhibit the fastest CAGR of 21.1% from 2025 to 2032, supported by increasing demand for early prenatal screening and advanced imaging technologies. The growing number of private and standalone diagnostic laboratories equipped with 3D/4D ultrasound, MRI, and genetic sequencing platforms is expanding accessibility. Technological progress in imaging accuracy and non-invasive prenatal testing (NIPT) continues to boost reliability and patient trust. Diagnostic centers are increasingly collaborating with hospitals to provide comprehensive prenatal and postnatal screening packages. The expansion of point-of-care diagnostics and portable imaging units improves service delivery in rural and semi-urban regions. Rising healthcare expenditure and government initiatives encouraging early screening of congenital disorders are driving this segment forward. As awareness of early detection’s importance spreads globally, diagnostic centers are emerging as crucial players in reducing delays in treatment initiation.

SPINA Bifida & Hydrocephalus Market Regional Analysis

- North America dominated the spina bifida & hydrocephalus market with the largest revenue share of 43.5% in 2024

- Supported by a robust healthcare infrastructure, early access to advanced neurosurgical care, and a strong presence of leading medical device manufacturers

- The market particularly benefits from increased awareness programs, better insurance coverage for rare congenital disorders, and continuous technological innovations in shunt and catheter systems

U.S. Spina Bifida & Hydrocephalus Market Insight

The U.S. spina bifida & hydrocephalus market captured the largest revenue share in 2024 within North America, driven by strong healthcare spending, early diagnosis initiatives, and the availability of advanced treatment modalities. Widespread adoption of innovative shunt systems and improved surgical precision technologies have contributed significantly to growth. Furthermore, the active role of patient advocacy groups and ongoing clinical research supported by NIH funding continue to strengthen the U.S. market outlook.

Europe Spina Bifida & Hydrocephalus Market Insight

The Europe spina bifida & hydrocephalus market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by advancements in neurosurgical care and government support for congenital disorder management. The region’s focus on healthcare quality, coupled with increased research funding and awareness programs, is fostering growth. Key markets such as Germany, France, and the U.K. are emphasizing early screening and access to multidisciplinary care centers, ensuring better patient outcomes.

U.K. Spina Bifida & Hydrocephalus Market Insight

The U.K. spina bifida & hydrocephalus market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by an advanced healthcare infrastructure and strong government initiatives promoting rare disease management. The rising prevalence of neural tube defects and increased availability of prenatal diagnostic tests are driving market growth. Furthermore, collaborations between the NHS and research institutions are improving access to advanced surgical and postnatal care.

Germany Spina Bifida & Hydrocephalus Market Insight

The Germany spina bifida & hydrocephalus market is expected to expand at a considerable CAGR during the forecast period, driven by technological progress in neurosurgical tools and a growing focus on personalized medicine. The presence of leading medtech manufacturers and strong government investment in healthcare innovation are propelling market development. Germany’s well-structured hospital network and emphasis on early intervention contribute to improved patient survival rates and recovery outcomes.

Asia-Pacific Spina Bifida & Hydrocephalus Market Insight

Asia-Pacific spina bifida & hydrocephalus market is expected to be the fastest-growing region in the Spina Bifida & Hydrocephalus market during the forecast period, registering a CAGR of 23.6% from 2025 to 2032, driven by expanding healthcare access, improving neonatal care infrastructure, and growing awareness of congenital anomalies in countries such as India, China, and Japan.

Japan Spina Bifida & Hydrocephalus Market Insight

The Japan spina bifida & hydrocephalus market is gaining momentum due to advanced medical technology adoption, strong research capabilities, and an aging population requiring long-term care solutions. The integration of robotics and precision tools in neurosurgical procedures is driving treatment efficiency. Moreover, government initiatives promoting early prenatal screening are improving diagnosis rates, thereby supporting early interventions.

China Spina Bifida & Hydrocephalus Market Insight

The China spina bifida & hydrocephalus market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid healthcare infrastructure development, a rising middle-class population, and growing awareness of neonatal health. The country’s strong domestic medical device manufacturing sector and government-backed public health campaigns are fueling adoption of affordable treatment solutions, including advanced shunt systems and minimally invasive neurosurgical equipment.

SPINA Bifida & Hydrocephalus Market Share

The SPINA Bifida & Hydrocephalus industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Johnson & Johnson Services, Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Amicus Therapeutics, Inc. (U.S.)

- BioMarin Pharmaceutical Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- AbbVie Inc. (U.S.)

- Sanofi (France)

- Lilly (U.S.)

- GSK plc (U.K.)

- AstraZeneca plc (U.K.)

- Boehringer Ingelheim International GmbH (Germany)

- Vertex Pharmaceuticals Incorporated (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- CSL Behring (Australia)

- Alexion Pharmaceuticals, Inc. (U.S.)

Latest Developments in Global SPINA Bifida & Hydrocephalus Market

- In February 2023, a study presented at a major neurosurgery conference demonstrated the successful implementation of a virtual-reality simulator for training surgeons in fetoscopic repair of spina bifida, enhancing procedural proficiency and potentially improving outcomes for prenatal intervention

- In May 2022, the “Hydrocephalus Market Industry Forecast Report 2022” highlighted a rising global demand for neurosurgery devices and hydrocephalus shunts, driven by increases in congenital abnormalities and traumatic brain injuries

- In July 2025, CereVasc, Inc. announced that its minimally invasive eShunt System had treated its 100th patient and was advancing toward regulatory submission, marking a significant milestone in hydrocephalus device innovation

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.