Global Spinal Non Fusion Technologies Market

Market Size in USD Billion

USD

4.90 Billion

USD

8.43 Billion

2025

2033

USD

4.90 Billion

USD

8.43 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.90 Billion | |

| USD 8.43 Billion | |

| % | |

|

Spinal Non Fusion Technologies Market Size

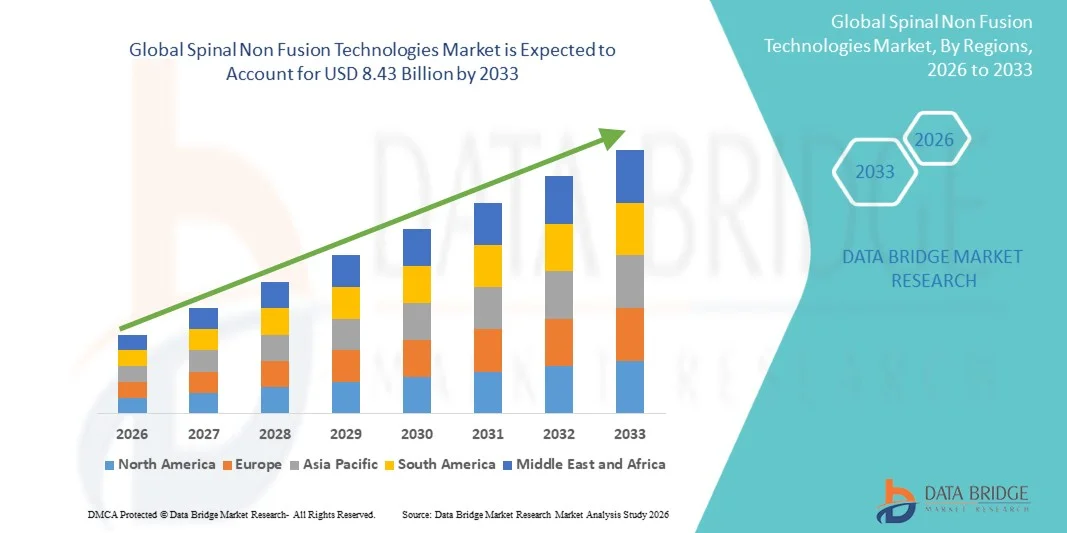

- The global Spinal Non Fusion Technologies market size was valued at USD 4.90 billion in 2025and is expected to reach USD 8.43 billion by 2033, at a CAGR of 7.02% during the forecast period

- The market growth is largely fueled by the increasing prevalence of spinal disorders, degenerative disc diseases, and chronic back pain conditions, leading to rising demand for minimally invasive and motion-preserving spinal treatment solutions across global healthcare systems

- Furthermore, growing preference for alternatives to spinal fusion surgery, advancements in orthopedic implant technologies, and increasing adoption of motion-preservation devices such as artificial discs and dynamic stabilization systems are establishing Spinal Non Fusion Technologies as a critical component of modern spinal care. These converging factors are accelerating the uptake of Spinal Non Fusion Technologies solutions, thereby significantly boosting the industry's growth

Spinal Non Fusion Technologies Market Analysis

- Spinal non fusion technologies, which include motion-preserving spinal implants and minimally invasive stabilization systems designed to treat spinal disorders without permanently fusing vertebrae, are increasingly vital in modern orthopedic and neurosurgical care due to their ability to maintain spinal flexibility, reduce recovery time, and improve patient mobility outcomes

- The escalating demand for spinal non fusion technologies is primarily fueled by the rising prevalence of degenerative disc disease, spinal stenosis, and chronic lower back pain, along with growing preference for minimally invasive spine procedures and motion-preserving treatment alternatives among patients and healthcare providers

- North America dominated the spinal non fusion technologies market with the largest revenue share of 37.8% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative spinal implants, increasing spinal surgery volumes, and strong presence of leading orthopedic device manufacturers, with the U.S. accounting for the majority of procedural demand and technological advancements

- Asia-Pacific is expected to be the fastest growing region in the spinal non fusion technologies market during the forecast period due to rising geriatric population, increasing incidence of spinal disorders, improving healthcare infrastructure, and growing access to advanced orthopedic treatments across countries such as China, India, and Japan

- The degenerative disc disease segment accounted for the largest market revenue share of 57.4% in 2025, driven by the high global prevalence of age-related spinal degeneration and chronic lower back pain conditions

Report Scope and Spinal Non Fusion Technologies Market Segmentation

|

Attributes |

Spinal Non Fusion Technologies Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Medtronic plc (Ireland) |

|

Market Opportunities |

· Increasing Preference for Motion-Preserving Spine Procedures · Rising Demand in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Spinal Non Fusion Technologies Market Trends

“Growing Adoption of Motion Preservation Devices and Minimally Invasive Spine Procedures”

- A significant and accelerating trend in the global Spinal Non Fusion Technologies market is the increasing adoption of motion-preserving spinal implants and minimally invasive surgical procedures aimed at improving patient outcomes and reducing recovery times

- For instance, technologies such as artificial disc replacement systems, dynamic stabilization devices, and annulus repair implants are increasingly being preferred over traditional spinal fusion procedures due to their ability to preserve spinal mobility and reduce stress on adjacent vertebral segments

- The growing focus on minimally invasive spine surgery is encouraging healthcare providers to adopt advanced spinal non fusion technologies that offer smaller incisions, reduced blood loss, shorter hospital stays, and faster postoperative recovery

- Furthermore, continuous advancements in biomaterials, implant design, and robotic-assisted surgical systems are improving procedural precision, implant durability, and long-term clinical outcomes in spinal disorder treatment

- The increasing prevalence of degenerative disc disease, spinal stenosis, and chronic lower back pain is driving higher demand for innovative non fusion treatment options that maintain natural spinal biomechanics

- This trend toward motion preservation, minimally invasive intervention, and technologically advanced spine care is reshaping the orthopedic and neurosurgical treatment landscape. Consequently, companies such as Medtronic and Zimmer Biomet are expanding their spinal non fusion product portfolios and strengthening research initiatives

- The demand for spinal non fusion technologies is increasing steadily across hospitals, ambulatory surgical centers, and specialty spine clinics due to the growing preference for mobility-preserving treatment approaches

Spinal Non Fusion Technologies Market Dynamics

Driver

“Increasing Prevalence of Degenerative Spine Disorders and Demand for Motion Preservation”

- The rising prevalence of degenerative spinal disorders and chronic back pain conditions is a major driver for the growth of the global Spinal Non Fusion Technologies market

- For instance, aging populations, sedentary lifestyles, obesity, and sports-related injuries are contributing significantly to the increasing incidence of degenerative disc disease and spinal instability disorders worldwide

- The growing demand for treatments that preserve natural spinal movement while reducing pain and improving functionality is encouraging wider adoption of spinal non fusion technologies over conventional spinal fusion procedures

- Furthermore, increasing patient preference for minimally invasive surgical procedures with shorter recovery times and reduced postoperative complications is supporting market expansion globally

- Advancements in imaging technologies, robotic-assisted surgery, and precision implant systems are also improving surgical outcomes and encouraging healthcare providers to adopt innovative non fusion spinal solutions

- In addition, expanding healthcare infrastructure, increasing healthcare expenditure, and growing awareness regarding advanced spine treatment options are further driving market growth

Restraint/Challenge

“High Procedure Costs and Limited Long-Term Clinical Evidence”

- The high cost associated with spinal non fusion procedures and advanced implant technologies remains a significant challenge affecting broader market adoption

- For instance, artificial disc replacement systems and dynamic stabilization implants often involve substantial procedural and device costs, limiting accessibility for patients in cost-sensitive healthcare markets

- In addition, reimbursement limitations and inconsistent insurance coverage for certain non fusion procedures can create financial barriers for both patients and healthcare providers

- The limited availability of long-term clinical outcome data for some newer spinal non fusion technologies may also create hesitation among surgeons and regulatory authorities regarding widespread adoption

- Furthermore, surgical complexity, specialized training requirements, and the risk of implant-related complications may restrict procedure adoption in some healthcare settings

- Overcoming these challenges through expanded clinical research, improved reimbursement policies, technological advancements, and cost-effective implant development will be essential for sustaining long-term growth in the global Spinal Non Fusion Technologies market

Spinal Non Fusion Technologies Market Scope

The market is segmented on the basis of product and application.

- By Product

On the basis of product, the Spinal Non Fusion Technologies market is segmented into dynamic stabilization devices, disc nucleus replacement products, annulus repair devices, nuclear disc prostheses, disc arthroplasty devices, and nuclear arthroplasty devices. The dynamic stabilization devices segment dominated the largest market revenue share of 38.9% in 2025, driven by increasing preference for motion-preserving spinal treatments over traditional spinal fusion procedures. These devices help stabilize the spine while maintaining flexibility and reducing adjacent segment degeneration. Rising prevalence of chronic spinal disorders and degenerative disc conditions is significantly supporting segment growth. Healthcare providers increasingly prefer minimally invasive spinal solutions due to faster recovery and improved patient outcomes. The segment benefits from growing advancements in biomaterials and implant technologies. Increasing aging population and sedentary lifestyles are also contributing to rising spinal disorder incidence. Favorable reimbursement policies in developed economies are further driving adoption. Orthopedic and neurosurgical specialists are increasingly utilizing dynamic stabilization systems in complex spinal procedures. Continuous innovation in implant design is enhancing long-term clinical outcomes. Furthermore, rising demand for non-fusion alternatives is expected to sustain segment dominance during the forecast period.

The disc arthroplasty devices segment is expected to witness the fastest CAGR of 10.7% from 2026 to 2033, driven by increasing adoption of artificial disc replacement procedures for preserving spinal mobility. Disc arthroplasty devices are gaining popularity as effective alternatives to spinal fusion surgeries. The segment benefits from growing awareness regarding motion-preserving technologies among surgeons and patients. Advancements in implant materials and biomechanical engineering are improving device performance and durability. Increasing prevalence of degenerative disc disease is significantly supporting demand. Healthcare providers are increasingly recommending minimally invasive procedures with faster rehabilitation outcomes. Rising healthcare expenditure and improved surgical infrastructure are further contributing to market growth. Regulatory approvals for advanced spinal implants are also accelerating commercialization. Expanding clinical evidence supporting long-term efficacy is encouraging wider adoption. Furthermore, increasing patient preference for mobility-preserving spinal procedures is expected to drive strong segment growth during the forecast period.

- By Application

On the basis of application, the Spinal Non Fusion Technologies market is segmented into degenerative disc disease, spinal stenosis, and degenerative spondylolisthesis. The degenerative disc disease segment accounted for the largest market revenue share of 57.4% in 2025, driven by the high global prevalence of age-related spinal degeneration and chronic lower back pain conditions. Degenerative disc disease is one of the most common indications for non-fusion spinal procedures due to increasing demand for motion-preserving treatments. The segment benefits from rising aging population and sedentary lifestyle patterns contributing to spinal deterioration. Increasing awareness regarding minimally invasive spinal procedures is significantly supporting adoption. Healthcare providers are increasingly utilizing advanced spinal implants for improved patient mobility and pain relief. Technological advancements in spinal stabilization devices are enhancing treatment outcomes. Rising healthcare expenditure and improved diagnostic imaging are also contributing to market growth. Growing incidence of obesity and musculoskeletal disorders is further driving demand for spinal interventions. Expanding orthopedic surgical infrastructure in emerging economies is supporting treatment accessibility. Furthermore, increasing patient preference for faster recovery and reduced post-operative complications is expected to sustain segment dominance during the forecast period.

The spinal stenosis segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by increasing incidence of spinal canal narrowing among elderly populations. Spinal stenosis is becoming more prevalent due to aging demographics and rising musculoskeletal degeneration globally. The segment benefits from increasing adoption of minimally invasive decompression and stabilization procedures. Technological advancements in spinal implants and imaging-guided surgeries are improving treatment precision and outcomes. Healthcare providers are increasingly focusing on preserving spinal mobility while reducing pain and nerve compression. Rising awareness regarding early diagnosis and treatment is significantly supporting growth. Expanding access to advanced orthopedic care in emerging economies is further contributing to segment expansion. Favorable reimbursement policies for spinal surgeries are also supporting adoption. Research and development activities in next-generation spinal implants are strengthening innovation. Furthermore, increasing demand for effective and less invasive spinal treatment options is expected to drive strong segment growth during the forecast period.

Spinal Non Fusion Technologies Market Regional Analysis

- North America dominated the spinal non fusion technologies market with the largest revenue share of 37.8% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative spinal implants, increasing spinal surgery volumes, and the strong presence of leading orthopedic device manufacturers. The region benefits from rising prevalence of degenerative spinal disorders, increasing awareness regarding minimally invasive spine procedures, and strong clinical adoption of motion-preserving spinal technologies

- The growing demand for alternatives to spinal fusion surgeries, increasing incidence of chronic back pain, and rising preference for faster recovery procedures are significantly driving the adoption of spinal non fusion technologies across hospitals and specialty orthopedic centers in the region

- Furthermore, continuous advancements in spinal implant design, favorable reimbursement frameworks, and increasing investments in orthopedic research and innovation are reinforcing North America’s leadership in the global Spinal Non Fusion Technologies market

U.S. Spinal Non Fusion Technologies Market Insight

The U.S. spinal non fusion technologies market captured the largest revenue share within North America in 2025, accounting for the majority of procedural demand and technological advancements. Growth in the market is driven by increasing spinal surgery volumes, rising prevalence of degenerative disc disease, and growing adoption of minimally invasive spinal procedures. In addition, the presence of major orthopedic device manufacturers, strong surgeon expertise, and increasing use of artificial disc replacement and dynamic stabilization systems continue to propel market growth in the U.S.

Europe Spinal Non Fusion Technologies Market Insight

The Europe spinal non fusion technologies market is projected to expand at a substantial CAGR throughout the forecast period, supported by rising geriatric population, increasing prevalence of spinal disorders, and growing demand for advanced orthopedic procedures. The region’s strong healthcare systems and increasing adoption of motion-preserving spinal implants are encouraging wider use of spinal non fusion technologies. Furthermore, expanding access to minimally invasive spine surgery and increasing orthopedic research initiatives are contributing significantly to market growth across Europe.

U.K. Spinal Non Fusion Technologies Market Insight

The U.K. spinal non fusion technologies market is anticipated to grow at a noteworthy CAGR during the forecast period due to increasing prevalence of spinal disorders, rising awareness regarding minimally invasive spine treatments, and growing demand for advanced orthopedic care. Expanding access to specialized spinal surgery centers and increasing focus on improving patient outcomes are supporting market growth. In addition, growing adoption of artificial disc replacement procedures is further driving demand for spinal non fusion technologies in the country.

Germany Spinal Non Fusion Technologies Market Insight

The Germany spinal non fusion technologies market is expected to expand at a considerable CAGR during the forecast period, fueled by strong orthopedic healthcare infrastructure, increasing adoption of innovative spinal implants, and rising investments in medical technology advancements. Germany’s emphasis on precision surgical techniques and advanced spinal care solutions is supporting the broader adoption of spinal non fusion procedures. Moreover, increasing clinical research activities and growing demand for motion-preserving therapies are contributing positively to market expansion.

Asia-Pacific Spinal Non Fusion Technologies Market Insight

The Asia-Pacific spinal non fusion technologies market is expected to witness the fastest CAGR during the forecast period due to rising geriatric population, increasing incidence of spinal disorders, improving healthcare infrastructure, and growing access to advanced orthopedic treatments across countries such as China, India, and Japan. Rapid urbanization, sedentary lifestyles, and increasing cases of degenerative spinal conditions are significantly driving demand for spinal surgeries in the region. Furthermore, growing healthcare investments and expanding availability of minimally invasive spinal procedures are accelerating market growth across Asia-Pacific.

Japan Spinal Non Fusion Technologies Market Insight

The Japan spinal non fusion technologies market is gaining momentum due to the country’s aging population, high prevalence of spinal degenerative diseases, and advanced orthopedic healthcare infrastructure. Rising adoption of minimally invasive spinal procedures and increasing demand for motion-preserving spinal implants are driving market growth. In addition, Japan’s strong focus on medical innovation and rehabilitation-based patient care is contributing to the expansion of the spinal non fusion technologies market in the country.

China Spinal Non Fusion Technologies Market Insight

The China spinal non fusion technologies market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to expanding healthcare infrastructure, increasing prevalence of spinal disorders, and growing demand for advanced orthopedic treatments. Rising healthcare expenditure, increasing awareness regarding minimally invasive spine surgeries, and improving access to specialized spinal care centers are key factors driving market growth. In addition, strong government support for healthcare modernization and increasing adoption of technologically advanced spinal implants are significantly contributing to the growth of the Spinal Non Fusion Technologies market in China.

Spinal Non Fusion Technologies Market Share

The Spinal Non Fusion Technologies industry is primarily led by well-established companies, including:

• Medtronic plc (Ireland)

• Johnson & Johnson (U.S.)

• Stryker Corporation (U.S.)

• Zimmer Biomet Holdings, Inc. (U.S.)

• Globus Medical, Inc. (U.S.)

• NuVasive, Inc. (U.S.)

• Orthofix Medical Inc. (U.S.)

• SeaSpine Holdings Corporation (U.S.)

• RTI Surgical Holdings, Inc. (U.S.)

• Alphatec Holdings, Inc. (U.S.)

• B. Braun Melsungen AG (Germany)

• Centinel Spine, LLC (U.S.)

• Spine Wave, Inc. (U.S.)

• Aurora Spine Corporation (Canada)

• Premia Spine Ltd. (Israel)

• Spinal Kinetics (U.S.)

• Life Spine, Inc. (U.S.)

• Aesculap Implant Systems, LLC (Germany)

• Xtant Medical Holdings, Inc. (U.S.)

• DePuy Synthes (U.S.)

Latest Developments in Global Spinal Non Fusion Technologies Market

- In July 2021, Centinel Spine received U.S. FDA approval for three additional prodisc Cervical Total Disc Replacement devices — prodisc C Vivo, prodisc C Nova, and prodisc C SK — expanding its portfolio of motion-preserving spinal non-fusion technologies for cervical degenerative disc disease. The approvals strengthened the company’s position in the artificial disc replacement segment and increased surgeon customization options for patient-specific anatomy

- In April 2022, SeaSpine Holdings Corporation announced the full commercial launch of the Reef TA (TLIF Articulating) Interbody System, designed to improve sagittal alignment and optimize interbody placement during lumbar spine procedures. The launch expanded minimally invasive spinal technology solutions and enhanced surgical efficiency in spinal reconstruction procedures

- In August 2022, Nexus Spine announced the full commercial launch of its PressON posterior lumbar fixation system, featuring a novel rod-to-pedicle screw attachment mechanism without traditional set screws. The technology was designed to improve biomechanical strength, reduce implant size, and enable patient-specific rod construction in spinal stabilization procedures

- In September 2022, SeaSpine announced the full commercial launch of the WaveForm TA (TLIF Articulating) Interbody System, a 3D-printed spinal implant platform developed to support anatomical customization and minimally invasive spinal surgery workflows. The system expanded SeaSpine’s advanced interbody technology portfolio for degenerative spinal disorders

- In December 2022, Becker’s Spine Review reported significant growth in the artificial disc replacement segment, highlighting first commercial procedures using Centinel Spine’s prodisc C Vivo and prodisc C SK devices. The report also noted rising adoption of motion-preserving spinal technologies and increasing clinical milestones in lumbar artificial disc replacement

- In January 2024, Providence Medical Technology announced that the U.S. FDA granted clearance for its CAVUX FFS-LX Lumbar Facet Fixation System, a novel integrated cage-and-screw technology designed for lumbar degenerative disc disease treatment. The system demonstrated a 96% fusion rate in clinical studies and represented continued innovation in spinal stabilization technologies

- In May 2024, Canary Medical announced that its Canturio Smart Spine Lumbar Cartridge received FDA Breakthrough Device Designation. The implantable smart sensor technology was developed to provide objective kinematic and recovery data from implanted spinal devices, representing advancement in intelligent spinal monitoring and digital spine health technologies

- In September 2024, Nevro Corp. announced the FDA approval and limited market release of HFX AdaptivAI, the first AI-enabled spinal cord stimulation technology designed to deliver personalized pain management through real-time adaptive therapy. The platform integrated artificial intelligence and patient-specific analytics to improve chronic pain treatment outcomes

- In December 2024, ONWARD Medical received FDA De Novo classification and U.S. market authorization for its ARC-EX System, the world’s first non-invasive spinal cord stimulation platform approved for improving hand strength and sensation in patients with chronic spinal cord injury. The authorization marked a major advancement in non-fusion spinal neuromodulation technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.