Global Spoon In Lid Packaging Market

Market Size in USD Million

USD

360.86 Million

USD

1,604.13 Million

2025

2033

USD

360.86 Million

USD

1,604.13 Million

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 360.86 Million |

Market Size (Forecast Year) |

USD 1,604.13 Million |

CAGR |

% |

Major Markets Players |

|

What is the Global Spoon in Lid Packaging Market Size and Growth Rate?

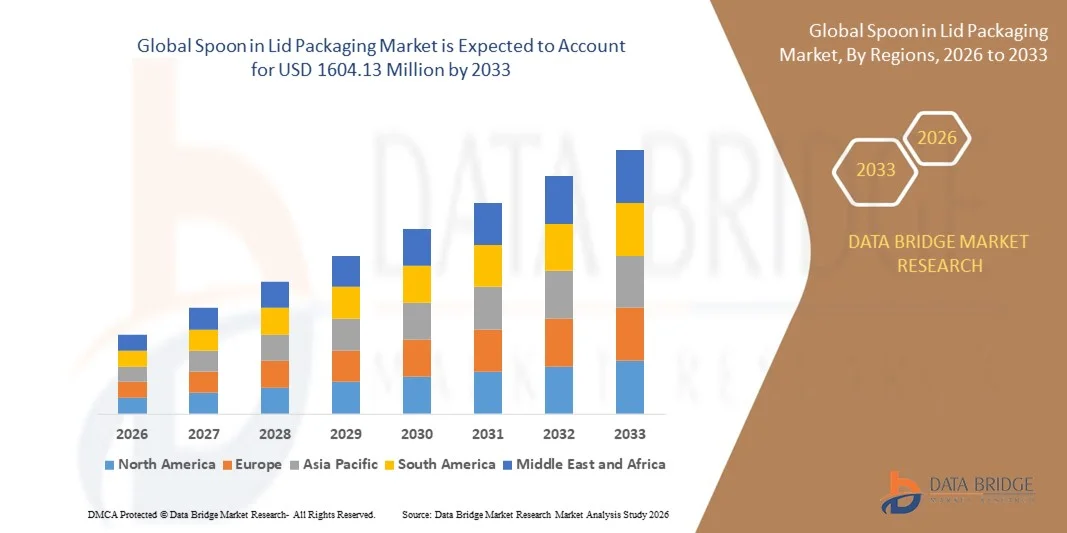

- The global spoon in lid packaging market size was valued at USD 360.86 million in 2025 and is expected to reach USD 1604.13 million by 2033, at a CAGR of20.5% during the forecast period

- The rise in demand for convenience packaging in the food industry acts as one of the major factors driving the growth of spoon in lid packaging market

- The rise in the consumption of frozen foods worldwide because of the high utilization for the packaging of desserts, yogurts, and ice creams among others and increase in consumption of on-the-go foods due to the hectic lifestyle accelerate the market growth

What are the Major Takeaways of Spoon in Lid Packaging Market?

- The high demand for the packaging provides convenience to the end consumers and improves the shelf appeal of food products in retail stores, and rises in popularity of the packaging due to the manufactures using compostable or recyclable materials among the millennial population of consumer’s further influence the market

- In addition, increase in purchasing goods online, growing acceptance of these channels and increasing preference for easy-to-use packaging positively affect the spoon in lid packaging market. Furthermore, rise in internet penetration especially in emerging economies extends profitable opportunities to the market players

- Europe dominated the spoon in lid packaging market with a 42.05% revenue share in 2025, driven by high adoption of advanced food packaging solutions, stringent food safety regulations, and rising demand for sustainable, portion-controlled packaging across retail, bakery, and dairy sectors in Germany, France, U.K., Italy, and Spain

- North America is projected to register the fastest CAGR of 10.69% from 2026 to 2033, fueled by rapid adoption of ready-to-eat meals, dessert cups, and portion-controlled food packaging in the U.S. and Canada

- The Polypropylene (PP) segment dominated the market with an estimated 41.2% share in 2025, owing to its lightweight, durable, and heat-resistant properties

Report Scope and Spoon in Lid Packaging Market Segmentation

|

Attributes |

Spoon in Lid Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Spoon in Lid Packaging Market?

Increasing Focus on Sustainable, Convenience-Driven, and Multi-Functional Spoon in Lid Packagings

- The spoon in lid packaging market is witnessing a growing shift toward eco-friendly, biodegradable, and compostable materials, meeting rising consumer demand for sustainability and reduced plastic usage

- Manufacturers are introducing innovative designs combining convenience and functionality, including integrated spoons, resealable lids, and multi-compartment formats for on-the-go consumption

- Rising adoption of lightweight, durable, and tamper-proof packaging solutions is driving demand across ready-to-eat meals, dairy products, and dessert segments

- For instance, companies such as Dart Container Corporation, Huhtamäki Oyj, Georgia-Pacific, Pactiv LLC, and Berry Global have expanded their sustainable and multi-functional packaging lines to enhance user experience and comply with environmental regulations

- Increasing demand for convenient, portable, and hygienic serving solutions is accelerating the development of high-quality Spoon in Lid Packagings

- As consumers increasingly prefer ready-to-eat meals and eco-conscious packaging, spoon in lid packagings remain essential for modern foodservice and retail sectors

What are the Key Drivers of Spoon in Lid Packaging Market?

- Rising demand for convenience, portion control, and hygienic eating solutions in foodservice, retail, and institutional applications is driving market growth

- For instance, in 2025, leading packaging companies such as Huhtamäki Oyj, Dart Container Corporation, and Georgia-Pacific introduced multi-functional spoon-in-lid designs with biodegradable materials to cater to sustainability-conscious consumers

- Growth of on-the-go food consumption, rising frozen and ready-to-eat meal sales, and expansion of quick-service restaurants (QSRs) are boosting adoption globally

- Innovations in material technology, such as compostable plastics, renewable fibers, and lightweight polymers, enhance durability, shelf-life, and recyclability

- Increasing regulatory focus on plastic reduction, sustainability mandates, and eco-friendly packaging standards is further driving adoption

- Supported by growth in packaged desserts, dairy, and convenience foods, the Spoon in Lid Packaging market is expected to witness steady long-term expansion

Which Factor is Challenging the Growth of the Spoon in Lid Packaging Market?

- High production costs for eco-friendly, multi-functional, and customized spoon-in-lid solutions limit adoption, particularly for smaller foodservice operators

- For instance, during 2024–2025, rising raw material costs, supply chain disruptions, and compliance with environmental regulations increased production expenses for key global vendors

- Complexity in manufacturing durable yet compostable or recyclable lids with integrated spoons increases design and tooling requirements

- Limited consumer awareness in certain emerging markets about biodegradable or sustainable packaging slows uptake

- Competition from traditional single-use packaging, reusable cutlery solutions, and other convenience formats creates pricing and adoption pressures

- To overcome these challenges, companies are focusing on material innovation, cost optimization, process efficiency, and marketing sustainability benefits to boost global Spoon in Lid Packaging adoption

How is the Spoon in Lid Packaging Market Segmented?

The market is segmented on the basis of material type, packaging format, and application.

- By Material Type

On the basis of material type, the spoon in lid packaging market is segmented into Polyethylene (PE), Polypropylene (PP), Paper, Polyethylene Terephthalate (PET), and Others. The Polypropylene (PP) segment dominated the market with an estimated 41.2% share in 2025, owing to its lightweight, durable, and heat-resistant properties. PP is widely used for dairy cups, dessert tubs, and ready-to-eat food containers because it ensures product safety, maintains integrity during storage and transportation, and allows easy sealing with integrated spoons.

The Paper segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing adoption of sustainable and biodegradable packaging materials across foodservice, bakery, and dairy segments. Rising consumer awareness of eco-friendly packaging and regulatory emphasis on reducing single-use plastics are accelerating demand for paper-based spoon-in-lid formats. Companies are increasingly innovating with coated and fiber-based papers to balance durability, hygiene, and environmental sustainability, supporting long-term material adoption trends.

- By Packaging Format

On the basis of packaging format, the market is segmented into Cups and Tubs. The Cups segment dominated the market with a 45.7% share in 2025, supported by high usage in single-serve desserts, yogurts, puddings, and dairy products. Spoon-in-lid cups offer convenience, portion control, and portability, making them ideal for retail, quick-service restaurants, and on-the-go consumption.

The Tubs segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for multi-serving food products, bakery items, ice creams, and sauces. Tubs provide larger capacity, stackability, and enhanced shelf visibility, appealing to supermarkets and foodservice operators. Rising customization of tub designs, including resealable lids with integrated spoons, is encouraging adoption. Expansion of frozen and ready-to-eat meals, combined with consumer preference for reusable or portioned containers, further propels growth in the tub packaging format.

- By Application

On the basis of application, the spoon in lid packaging market is segmented into Dairy Products, Bakery Products, Food Products, and Other Products. The Dairy Products segment dominated the market with an estimated 48.6% share in 2025, driven by widespread use in yogurts, puddings, flavored milk, and cream-based desserts. Spoon-in-lid packaging offers convenience, hygiene, and portability, aligning with on-the-go consumption trends and retail-ready presentation.

The Bakery Products segment is expected to grow at the fastest CAGR from 2026 to 2033, fueled by rising demand for individual pastries, muffins, and desserts in cafes, bakeries, and packaged retail formats. Innovations in portion-controlled, tamper-evident, and visually appealing spoon-in-lid packaging are supporting adoption. Growth in convenience foods, ready-to-eat snacks, and premium bakery offerings is further driving market expansion across foodservice and retail channels globally.

Which Region Holds the Largest Share of the Spoon in Lid Packaging Market?

- Europe dominated the spoon in lid packaging market with a 42.05% revenue share in 2025, driven by high adoption of advanced food packaging solutions, stringent food safety regulations, and rising demand for sustainable, portion-controlled packaging across retail, bakery, and dairy sectors in Germany, France, U.K., Italy, and Spain. Increasing preference for convenience foods and ready-to-eat meals supports consistent market growth

- Leading companies in Europe are investing in biodegradable, recyclable, and multi-material spoon-in-lid packaging solutions, enhancing shelf appeal and compliance with EU packaging directives. Innovation in barrier coatings, printability, and lid-spoon integration further strengthens the region’s competitive position

- Well-established manufacturing infrastructure, high consumer awareness, and continuous technological upgrades in packaging machinery reinforce Europe’s leadership in the global market

Germany Spoon in Lid Packaging Market Insight

Germany is the largest contributor in Europe, supported by strong industrial manufacturing capabilities, innovative packaging R&D, and a focus on eco-friendly materials. Rising production of dairy, desserts, and bakery items drives demand for integrated spoon-in-lid packaging. Companies prioritize high-quality, tamper-evident designs to ensure product safety and convenience.

France Spoon in Lid Packaging Market Insight

France contributes significantly due to growing bakery and dairy product consumption, expanding foodservice chains, and increasing adoption of pre-portioned packaging. Investments in automated packaging lines and sustainable material solutions support market growth.

Italy Spoon in Lid Packaging Market Insight

Italy shows steady expansion, driven by high demand in desserts, gelato, and single-serve food items. Manufacturers are increasingly adopting recyclable plastics and fiber-based alternatives to align with environmental regulations and consumer preference.

U.K. Spoon in Lid Packaging Market Insight

The U.K. market is growing on account of convenience-focused retail products, ready-to-eat meals, and premium desserts. Adoption of recyclable and tamper-proof packaging enhances product safety, supporting long-term market penetration.

Spain Spoon in Lid Packaging Market Insight

Spain contributes steadily, driven by rising packaged bakery, dairy, and frozen dessert consumption. Innovation in portion control, sealing, and integrated spoons strengthens demand across retail and foodservice channels.

North America Spoon in Lid Packaging Market

North America is projected to register the fastest CAGR of 10.69% from 2026 to 2033, fueled by rapid adoption of ready-to-eat meals, dessert cups, and portion-controlled food packaging in the U.S. and Canada. High consumption of convenience foods, expanding foodservice chains, and rising demand for premium packaging solutions accelerate market growth. Companies are introducing multi-material, recyclable, and tamper-evident spoon-in-lid designs that improve product shelf life, usability, and brand differentiation. Strong innovation ecosystems, investment in automated packaging lines, and growing e-commerce distribution channels further support rapid expansion.

U.S. Spoon in Lid Packaging Market Insight

The U.S. is the largest contributor to North America, supported by high consumption of dairy, bakery, and snack products in convenience formats. Rising awareness of eco-friendly packaging and integration of spoons with lids drives adoption across retail, quick-service restaurants, and foodservice channels.

Canada Spoon in Lid Packaging Market Insight

Canada contributes significantly due to growing demand for single-serve, on-the-go food packaging and rising adoption of sustainable materials. Government incentives for eco-friendly packaging and rising urban consumption further accelerate growth.

Which are the Top Companies in Spoon in Lid Packaging Market?

The spoon in lid packaging industry is primarily led by well-established companies, including:

- Dart Container Corporation (U.S.)

- Georgia-Pacific (U.S.)

- Huhtamäki Oyj (Finland)

- Greiner Packaging International GmbH (Austria)

- Frugalpac Limited (U.K.)

- James Cropper plc (U.K.)

- Berry Global Inc. (U.S.)

- Pactiv LLC (U.S.)

- Genpak, LLC (U.S.)

- ConverPack, Inc. (U.S.)

- Eco-Products, Inc. (U.S.)

- Churchill Container (U.S.)

- WinCup (U.S.)

- Airlite Plastics (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Spoon In Lid Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Spoon In Lid Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Spoon In Lid Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.