Global Stargardts Treatment Market

Market Size in USD Million

USD

472.34 Million

USD

3,853.34 Million

2025

2033

USD

472.34 Million

USD

3,853.34 Million

2025

2033

| 2026 - 2033 | |

| USD 472.34 Million | |

| USD 3,853.34 Million | |

| % | |

|

Stargardts Treatment Market Overview

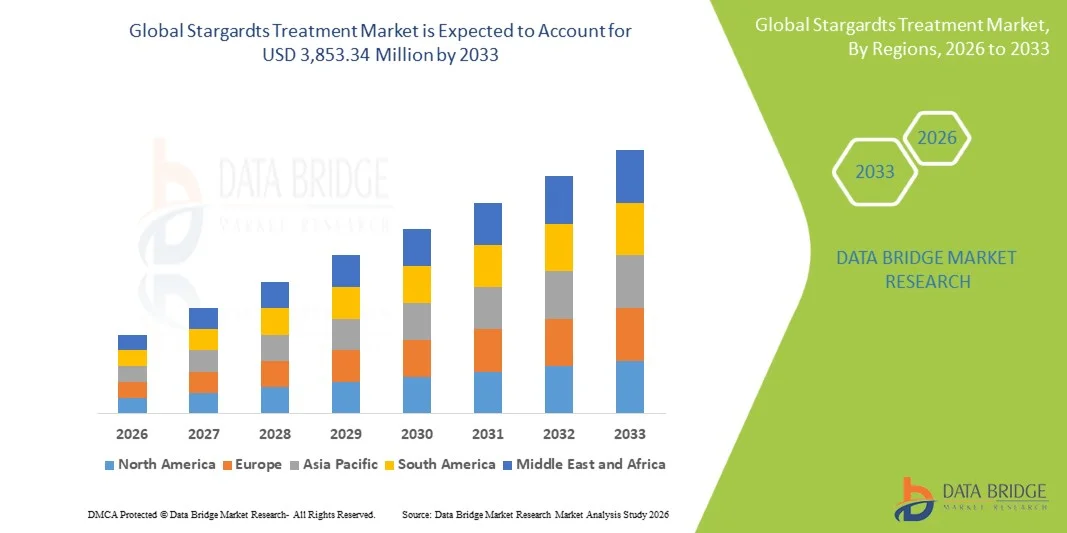

The Stargardts Treatment Market was valued at USD 472.34 million in 2025 and is projected to reach USD 3,853.34 million by 2033, growing at a CAGR of 30.0% from 2026 to 2033. Market growth is supported by rising prevalence of Stargardt disease among the global population, alongside increasing research and development investments in novel therapeutic approaches including gene therapy and visual cycle modulators.

The excellent progress in understanding the genetic basis of Stargardt disease, combined with accelerating clinical trials for disease-modifying treatments and improved diagnostic capabilities compared to traditional ophthalmic assessments, are driving increased adoption among both patients and medical professionals. Ongoing technological advancements in gene therapy delivery systems, including enhanced viral vector technologies, improved retinal targeting mechanisms, and integrated patient monitoring platforms, are expanding the clinical applicability of Stargardts treatments across pediatric, juvenile, and adult patient populations. In addition, growing healthcare infrastructure investments in emerging markets and the expansion of specialty ophthalmic clinics are creating new opportunities for stakeholders across the forecast period.

Key Market Trends & Insights

- North America dominated the Stargardts Treatment Market with the largest revenue share of 42.8% in 2025, supported by high adoption rates of advanced therapeutic technologies, strong reimbursement frameworks, and the presence of leading market players.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 33.5% from 2026 to 2033, driven by expanding healthcare infrastructure, rising awareness of rare genetic eye diseases, and increasing healthcare expenditure.

- The Gene Therapy segment led the treatment category market with a 48.2% market share in 2025, reflecting its established position as the most promising therapeutic approach and strong clinical evidence supporting improved visual outcomes.

- The LBS-008 segment is anticipated to be the fastest-growing drug type category, projected to register a CAGR of 34.2% during the forecast period, driven by advancing clinical trials, favorable safety profiles, and emerging regulatory support for visual cycle modulator therapies.

- The Hospitals segment dominated the end-user category with a 52.6% market share in 2025, supported by access to advanced diagnostic platforms, multidisciplinary ophthalmic teams, and comprehensive patient care infrastructure.

- The Online Pharmacy segment is expected to witness strong growth during the forecast period, driven by cost-effective medication delivery, expanded patient access, and growing digital health adoption among rare disease patient communities.

Market Size & Forecast

- Global Market Value (2025): USD 472.34 Million

- Expected Market Value (2033): USD 3,853.34 Million

- Forecast CAGR (2026–2033): 30.0%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Stargardts Treatment Market Segmentation

|

Attributes |

Stargardts Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of gene therapy platforms into emerging markets with growing healthcare infrastructure and rare disease treatment capabilities · Development of novel visual cycle modulators enabling disease modification and slowing progression in early-stage Stargardt patients |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Stargardts Treatment Market Trends

Trend: Accelerating Gene Therapy Development and Clinical Advancement

Clinical adoption of Stargardts treatment approaches continues to accelerate as gene therapy innovations improve therapeutic precision, delivery mechanisms, and patient outcomes. Advanced viral vector technologies, including adeno-associated virus (AAV) delivery systems and enhanced retinal targeting platforms, enable researchers to address the root genetic cause of Stargardt disease with greater accuracy and reduced immunogenic response. Clinical trial infrastructure embedded within specialized ophthalmic centers allows researchers to develop therapeutic proficiency and optimize treatment protocols, reducing the translational gap between research and clinical application.

For instance,

SpliceBio's SB-007 gene therapy candidate has gained significant market attention due to its dual-vector AAV approach addressing the oversized ABCA4 gene, providing patients with a potentially disease-modifying treatment option targeting the underlying genetic mutation causing Stargardt disease.

In addition, research demonstrates that gene therapy approaches targeting ABCA4 mutations show promising preliminary safety and efficacy profiles compared to symptomatic management strategies, supporting broader clinical adoption across specialized retinal treatment centers globally. The accelerating development of gene therapy platforms is expected to fundamentally transform the Stargardts treatment landscape during the forecast period.

Stargardts Treatment Market Dynamics

Key Market Driver: Rising Prevalence and Improved Diagnosis of Stargardt Disease

The growing identification of Stargardt disease patients through improved diagnostic technologies and increased awareness among healthcare providers is a primary driver of market growth. Stargardts treatment approaches benefit from enhanced diagnostic capabilities including optical coherence tomography, fundus autofluorescence imaging, and genetic testing, enabling earlier disease identification and intervention. The increasing prevalence of Stargardt disease, estimated to affect approximately 1 in 8,000 to 10,000 individuals globally, is expanding the patient population eligible for therapeutic intervention.

For instance,

A 2025 epidemiological analysis confirmed that improved genetic screening programs and advanced retinal imaging technologies are enabling earlier Stargardt disease diagnosis, with detection rates increasing by approximately 18% annually in developed healthcare markets, demonstrating significant diagnostic advancement.

Rising diagnosis rates are expected to strengthen adoption of Stargardts treatment technologies globally.

Key Restraint/Challenge: High Development Costs and Limited Treatment Options

The substantial research and development investment required for gene therapy development, along with complex manufacturing processes, regulatory requirements, and extended clinical trial timelines, presents a significant barrier to market expansion. The limited number of approved treatments specifically indicated for Stargardt disease constrains patient access and therapeutic choice, particularly in emerging markets with limited specialty care infrastructure.

For instance,

Healthcare systems evaluating Stargardts treatment adoption must balance the potential clinical benefits against significant development costs, with gene therapy programs requiring substantial capital investment compared to symptomatic management approaches.

High development costs and limited approved therapies may constrain market growth, particularly among healthcare systems with limited rare disease treatment budgets.

Key Market Opportunity: Expansion of Visual Cycle Modulator Therapies

The development of oral visual cycle modulators, including LBS-008 (tinlarebant) and emixustat, is creating opportunities for disease modification beyond traditional supportive care approaches. These therapies aim to reduce toxic lipofuscin accumulation in retinal pigment epithelium cells by modulating the visual cycle, potentially slowing disease progression. Simultaneously, advancing clinical trial programs are generating evidence supporting regulatory approval pathways and commercial launch strategies.

For instance,

Belite Bio completed enrollment in its phase 2/3 DRAGON II clinical trial evaluating tinlarebant for Stargardt disease type 1 in January 2026, representing a significant milestone in visual cycle modulator development and supporting potential regulatory submission and commercial launch.

The expansion of visual cycle modulator therapies is expected to significantly broaden treatment options for Stargardt disease patients during the forecast period.

Stargardts Treatment Market Scope

The Stargardts treatment market is segmented on the basis of drug type, diagnosis, treatment, end user, and distribution channel.

By Drug Type

On the basis of drug type, the Stargardts Treatment Market is segmented into Emixustat and LBS-008. The Emixustat segment dominated the market with a market share of 58.5% in 2025, due to its earlier entry into clinical development and established safety profile from extended clinical trial programs. Strong physician familiarity with the compound and ongoing research investment from Kubota Pharmaceutical Holdings contributed to segment leadership.

The LBS-008 segment is expected to witness the fastest growth at a CAGR of 34.2% from 2026 to 2033, driven by positive phase 2/3 clinical trial results, favorable tolerability profiles, and emerging regulatory support for visual cycle modulator therapies. Belite Bio's advancing clinical development program and strong investor support are accelerating market penetration and competitive positioning.

By Diagnosis

On the basis of diagnosis, the Stargardts Treatment Market is segmented into Visual Field Testing, Colour Testing, Fundus Photo, Electroretinography (ERG), Optical Coherence Tomography (OCT), and Others. The Optical Coherence Tomography (OCT) segment dominated the diagnosis category with a market share of 32.4% in 2025, reflecting its established position as the gold standard for retinal imaging and disease monitoring. Strong clinical evidence supporting OCT-based disease progression assessment and widespread availability across ophthalmic practices contributed to segment leadership.

The Electroretinography (ERG) segment is anticipated to witness the fastest growth at a CAGR of 33.8% from 2026 to 2033, driven by increasing recognition of functional retinal assessment importance in clinical trial endpoints, advancing ERG technology platforms, and growing integration of electrophysiology testing into comprehensive Stargardt disease evaluation protocols.

By Treatment

On the basis of treatment, the Stargardts Treatment Market is segmented into Dark Sunglasses, Gene Therapy, and Others. The Gene Therapy segment dominated the treatment category with a market share of 48.2% in 2025, reflecting its established position as the most promising therapeutic approach for addressing the underlying genetic cause of Stargardt disease. Strong clinical evidence supporting improved visual outcomes, extensive research investment, and favorable regulatory pathways for gene therapy products contributed to segment leadership.

The Gene Therapy segment is expected to witness the fastest growth at a CAGR of 35.6% from 2026 to 2033, driven by advancing clinical trial programs, emerging regulatory approvals, technological advancements in viral vector delivery systems, and expanding treatment center infrastructure capable of administering gene therapy interventions.

By End User

On the basis of end user, the Stargardts Treatment Market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment dominated the end-user category with a market share of 52.6% in 2025, driven by access to advanced diagnostic platforms, multidisciplinary ophthalmic teams, and comprehensive patient care infrastructure. Hospitals serve as primary centers for complex Stargardts treatment procedures requiring specialized equipment, extended patient monitoring, and coordinated care delivery. The concentration of rare disease treatment programs within hospital systems contributes to high patient volumes and resource utilization.

The Specialty Clinics segment is expected to witness the fastest growth at a CAGR of 32.4% from 2026 to 2033, driven by expanding retinal specialty practices, growing physician expertise in rare genetic eye diseases, and increasing patient preference for specialized care settings offering focused treatment and monitoring services.

By Distribution Channel

On the basis of distribution channel, the Stargardts Treatment Market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the distribution channel category with a market share of 54.8% in 2025, driven by direct integration with hospital-based treatment programs, specialized medication handling requirements, and comprehensive patient counseling capabilities. Hospital pharmacies serve as primary dispensing points for complex Stargardts treatments requiring cold chain management and patient education.

The Online Pharmacy segment is expected to witness the fastest growth at a CAGR of 36.2% from 2026 to 2033, driven by cost-effective medication delivery, expanded patient access in underserved regions, growing digital health adoption among rare disease patient communities, and increasing manufacturer partnerships with specialty online pharmacy platforms.

Stargardts Treatment Market Regional Analysis

North America dominated the Stargardts treatment market with a revenue share of 42.8% in 2025, supported by high adoption rates of advanced therapeutic technologies, strong reimbursement frameworks, and the presence of leading market players including Belite Bio, Alkeus Pharmaceuticals, and reVision Therapeutics. Favorable regulatory pathways, robust clinical trial infrastructure, and extensive physician expertise with rare genetic eye diseases contribute to regional market leadership.

U.S. Stargardts Treatment Market Insight

The U.S. Stargardts treatment market benefits from the highest concentration of rare disease clinical trials globally, extensive physician training programs, and strong regulatory support for orphan drug development. Academic medical centers, specialized retinal practices, and integrated health systems continue to expand Stargardt disease treatment programs across gene therapy, visual cycle modulator, and supportive care applications. Favorable FDA orphan drug designation pathways and strong commercial payer reimbursement support clinical development and market access.

Europe Stargardts Treatment Market Insight

The Europe Stargardts treatment market remains a major contributor, with strong hospital-based rare disease treatment programs across Germany, the U.K., France, and the Netherlands. Growing adoption of gene therapy approaches and visual cycle modulators is expanding treatment options in public and private healthcare systems. Cross-disciplinary guidelines and structured clinical pathways are improving patient outcomes and standardizing care delivery across the region.

U.K. Stargardts Treatment Market Insight

The U.K. Stargardts treatment market is characterized by expanding rare genetic eye disease treatment programs within NHS hospitals and specialized ophthalmic centers. Investment in gene therapy infrastructure and clinical trial participation is improving access to innovative treatment options and advancing therapeutic development.

Germany Stargardts Treatment Market Insight

The Germany Stargardts treatment market’s robust hospital infrastructure and advanced ophthalmic capabilities support comprehensive Stargardts treatment programs across academic medical centers and specialty practices. Strong clinical research networks and favorable reimbursement frameworks contribute to high clinical trial participation and technology adoption.

Asia-Pacific Stargardts Treatment Market Insight

The Asia-Pacific Stargardts treatment market is poised for rapid growth with a CAGR of 33.5% during the forecast period, driven by expanding healthcare infrastructure, rising awareness of rare genetic diseases, and increasing healthcare expenditure. Private healthcare systems in Japan, China, South Korea, and Australia are investing in specialized ophthalmic capabilities to meet growing patient demand and improve clinical outcomes.

Japan Stargardts Treatment Market Insight

The Japan Stargardts treatment market benefits from advanced healthcare infrastructure, strong pharmaceutical research capabilities, and favorable regulatory frameworks for rare disease treatments. Kubota Pharmaceutical Holdings' presence as a leading emixustat developer strengthens domestic market development and clinical research activity.

China Stargardts Treatment Market Insight

The China Stargardts treatment market is experiencing rapid growth driven by healthcare modernization initiatives, expanding rare disease treatment coverage, and increasing patient demand for advanced therapeutic options. Government support for rare disease drug development and growing specialty hospital networks are improving market accessibility.

Stargardts Treatment Market Share

The Stargardts treatment industry is primarily led by well-established companies, including:

- Belite Bio, Inc. (U.S.)

- Kubota Pharmaceutical Holdings Co., Ltd. (Japan)

- Alkeus Pharmaceuticals, Inc. (U.S.)

- SpliceBio (Netherlands)

- reVision Therapeutics, Inc. (U.S.)

- Spark Therapeutics, Inc. (U.S.)

- Applied Genetic Technologies Corporation (U.S.)

- Ocugen, Inc. (U.S.)

- ProQR Therapeutics N.V. (Netherlands)

- Lineage Cell Therapeutics, Inc. (U.S.)

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche Ltd. (Switzerland)

Latest Developments in Stargardts Treatment Market

- In January 2026, Belite Bio announced the completion of enrollment in its phase 2/3 DRAGON II clinical trial evaluating tinlarebant (LBS-008) for the treatment of Stargardt disease type 1 (STGD1). The milestone represents a significant advancement in visual cycle modulator development and positions the company for potential regulatory submission and commercial launch.

- In December 2024, SpliceBio announced U.S. FDA IND clearance for SB-007 to commence a phase 1/2 clinical study in patients with Stargardt disease. SB-007 is the only clinical-stage therapeutic addressing the root genetic cause of Stargardt disease through a dual-vector AAV gene therapy approach.

- In October 2024, reVision Therapeutics received U.S. FDA rare pediatric disease and orphan drug designation for REV-0100 for the treatment of Stargardt disease. The designations support accelerated development pathways and potential priority review for the repurposed GRAS compound.

- In September 2024, Kubota Pharmaceutical Holdings announced positive interim results from its ongoing phase 3 clinical trial evaluating emixustat for Stargardt disease, demonstrating favorable safety profiles and preliminary efficacy signals supporting continued development.

- In July 2024, Alkeus Pharmaceuticals reported advancement of its ALK-001 (C20-D3-retinyl acetate) clinical program, with enrollment completion in its phase 3 TANGO trial evaluating the vitamin A analog for slowing progression of geographic atrophy and Stargardt disease.

- In April 2024, Applied Genetic Technologies Corporation announced continued progress in its ABCA4 gene therapy research program, with preclinical data supporting advancement toward clinical trial initiation for Stargardt disease treatment.

- In January 2024, ProQR Therapeutics announced strategic refocusing of its rare eye disease pipeline, with continued investment in RNA-based therapeutic approaches for inherited retinal diseases including Stargardt disease.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.