Global Stem Cell And Progenitor Cell Based Therapeutics Market

Market Size in USD Billion

USD

5.85 Billion

USD

15.57 Billion

2025

2033

USD

5.85 Billion

USD

15.57 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.85 Billion | |

| USD 15.57 Billion | |

| % | |

|

Stem Cell and Progenitor Cell-based Therapeutics Market Size

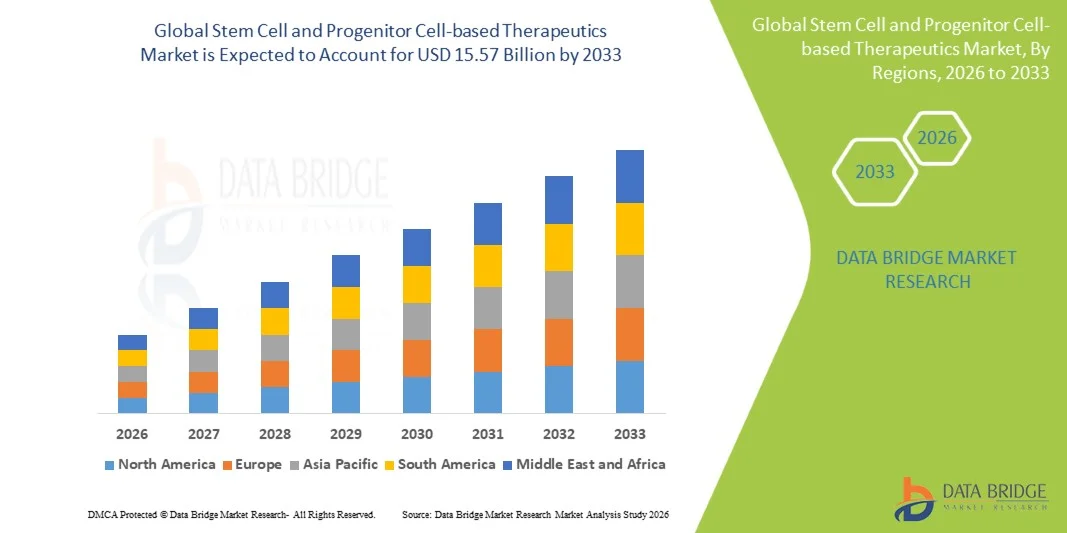

- The global Stem Cell and Progenitor Cell-based Therapeutics market size was valued at USD 5.85 billion in 2025and is expected to reach USD 15.57 billion by 2033, at a CAGR of 13.02% during the forecast period

- The market growth is largely fueled by increasing prevalence of chronic and degenerative diseases, rapid advancements in regenerative medicine, and growing investments in biotechnology research, leading to accelerated development of innovative cell-based therapies across healthcare system

- Furthermore, rising demand for personalized, disease-modifying, and minimally invasive treatment options is establishing Stem Cell and Progenitor Cell-based Therapeutics as a transformative approach in modern medicine. These converging factors are accelerating the uptake of Stem Cell and Progenitor Cell-based Therapeutics solutions, thereby significantly boosting the industry's growth

Stem Cell and Progenitor Cell-based Therapeutics Market Analysis

- Stem Cell and Progenitor Cell-based Therapeutics, including hematopoietic stem cells, mesenchymal stem cells, induced pluripotent stem cells, and progenitor cell therapies, are increasingly vital components of modern regenerative medicine due to their potential to repair damaged tissues, restore organ function, and address unmet medical needs across multiple chronic diseases

- The escalating demand for Stem Cell and Progenitor Cell-based Therapeutics is primarily fueled by the rising prevalence of degenerative disorders, increasing incidence of cancer and autoimmune diseases, growing investments in cell therapy research, and expanding clinical applications in personalized medicine

- North America dominated the stem cell and progenitor cell-based therapeutics market with the largest revenue share of approximately 44.1% in 2025, characterized by advanced biotechnology infrastructure, high healthcare expenditure, strong presence of leading regenerative medicine companies, and increasing clinical trial activity, with the U.S. witnessing substantial growth in approved cell therapy programs and translational research initiatives

- Asia-Pacific is expected to be the fastest-growing region in the stem cell and progenitor cell-based therapeutics market during the forecast period, projected to register a CAGR of approximately 12.8%, due to rising healthcare investments, expanding biotechnology sector, supportive regulatory reforms, and growing adoption of advanced regenerative therapies

- The Parkinson disease segment dominated the largest market revenue share of 58.4% in 2025, driven by the rising global prevalence of neurodegenerative disorders and increasing research focused on regenerative medicine for dopamine neuron restoration

Report Scope and Stem Cell and Progenitor Cell-based Therapeutics Market Segmentation

|

Attributes |

Stem Cell and Progenitor Cell-based Therapeutics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Mesoblast Limited (Australia) |

|

Market Opportunities |

· Expansion of regenerative medicine applications across chronic diseases · Rising Demand in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Stem Cell and Progenitor Cell-based Therapeutics Market Trends

“Advancing Regenerative Medicine Through Next-Generation Cell Therapies”

- A significant and accelerating trend in the global Stem Cell and Progenitor Cell-based Therapeutics market is the growing focus on regenerative medicine approaches designed to repair, replace, or restore damaged tissues and organs. These therapies are gaining momentum as healthcare systems seek long-term treatment options for chronic, degenerative, and previously hard-to-treat diseases

- Increasing clinical adoption of mesenchymal stem cells, hematopoietic stem cells, induced pluripotent stem cells (iPSCs), and progenitor cell therapies is expanding the therapeutic landscape across multiple indications

- For instance, Novartis and Gilead Sciences have invested heavily in advanced cell therapy platforms, supporting broader commercialization of innovative regenerative and immune-based treatments

- Growing research activity in neurology, cardiology, orthopedics, autoimmune disorders, and oncology is accelerating product development pipelines. Stem cell and progenitor cell technologies are increasingly being evaluated for spinal cord injuries, heart failure, cartilage regeneration, diabetes complications, and cancer-related applications

- Technological advancements in cell expansion, cryopreservation, gene editing, and bioprocess manufacturing are improving scalability, product consistency, and treatment efficacy. These innovations are helping manufacturers move from experimental models toward commercially viable therapeutic solutions

- Strategic collaborations between biotechnology firms, pharmaceutical companies, hospitals, and academic institutions are strengthening translational research and accelerating regulatory pathways. This collaborative ecosystem is enabling faster movement of therapies from laboratory studies into clinical practice

- As a result, stem cell and progenitor cell-based therapeutics are becoming a central pillar of next-generation medicine, with increasing demand for personalized and disease-modifying treatment solutions worldwide

Stem Cell and Progenitor Cell-based Therapeutics Market Dynamics

Driver

“Rising Burden of Chronic Diseases and Expanding Regenerative Medicine Demand”

- The increasing prevalence of chronic diseases, degenerative disorders, and organ damage is a major driver for the global Stem Cell and Progenitor Cell-based Therapeutics market. Conventional treatments often manage symptoms rather than repair underlying tissue damage, creating strong demand for regenerative alternatives

- Rising investment in cell therapy research, manufacturing infrastructure, and clinical trials is significantly accelerating market growth

- For instance, Fate Therapeutics and Mesoblast have expanded development programs focused on stem cell therapies for inflammatory, cardiovascular, and immune-related diseases

- Increasing aging populations globally are further boosting demand, as older individuals are more vulnerable to osteoarthritis, neurodegenerative disorders, heart disease, and other conditions where regenerative therapies may provide long-term benefits

- Growing success rates of hematopoietic stem cell transplantation in blood cancers and immune disorders are improving confidence in broader cell-based therapeutic models

- Advances in personalized medicine are also supporting adoption, as patient-derived cells and targeted regenerative treatments offer the potential for better compatibility and improved clinical outcomes

- Favorable regulatory pathways for advanced therapy medicinal products (ATMPs) in selected regions are encouraging innovation and faster commercialization of promising therapies

Restraint/Challenge

“High Treatment Costs, Complex Manufacturing, and Regulatory Uncertainty”

- The high cost associated with stem cell and progenitor cell therapies remains one of the most significant barriers to widespread adoption. Personalized manufacturing processes, specialized storage, and hospital-based administration often make these treatments expensive for both providers and patients

- Manufacturing complexity is another major challenge, as living cell products require strict quality control, sterile environments, and highly controlled logistics

- For instance, maintaining cell viability during transport and storage can substantially increase operational costs and supply chain risk

- Regulatory approval pathways remain demanding due to the need for extensive safety and long-term efficacy data. Since many cell therapies involve novel biological mechanisms, regulatory agencies often require prolonged monitoring before granting broad approvals

- Limited reimbursement coverage in several countries further restrains market expansion, as insurers may hesitate to cover costly therapies with evolving long-term evidence

- Ethical concerns surrounding certain stem cell sources, particularly embryonic stem cells, continue to create policy and public acceptance challenges in some regions

- Variability in patient response and difficulty standardizing biological outcomes may also slow adoption, especially in early-stage indications where clinical evidence is still developing

- Overcoming these restraints through scalable manufacturing, lower production costs, clearer regulations, stronger reimbursement frameworks, and continued clinical validation will be essential for sustained market growth

Stem Cell and Progenitor Cell-based Therapeutics Market Scope

The market is segmented on the basis of disease type, application, and end-user.

- By Disease Type

On the basis of disease type, the Stem Cell and Progenitor Cell-based Therapeutics market is segmented into Parkinson disease and Huntington disease. The Parkinson disease segment dominated the largest market revenue share of 58.4% in 2025, driven by the rising global prevalence of neurodegenerative disorders and increasing research focused on regenerative medicine for dopamine neuron restoration. Stem cell therapies are being widely investigated for their ability to repair damaged neural tissues and improve motor function in Parkinson’s patients. Growing elderly populations across developed and emerging economies are significantly contributing to patient volume. Strong pipeline activity, clinical trials, and public-private investments in neurological therapeutics further support segment growth. Academic institutions and biotechnology companies are prioritizing Parkinson-focused cell therapies due to high unmet clinical need. Favorable regulatory incentives for orphan and advanced therapies are also accelerating development. Increasing awareness regarding minimally invasive regenerative treatment options supports adoption. Expanding healthcare expenditure and improved diagnosis rates continue to strengthen demand. As a result, Parkinson disease remained the dominant segment in 2025.

The Huntington disease segment is anticipated to witness the fastest growth rate of 19.7% CAGR from 2026 to 2033, fueled by increasing genetic screening and growing investment in rare disease therapeutics. Stem and progenitor cell approaches are being explored to slow neuronal degeneration and improve cognitive outcomes. Rising support from patient advocacy organizations and orphan drug funding programs is accelerating research activity. Advancements in gene-editing combined with stem cell platforms are further expected to drive future segment expansion.

- By Applications

On the basis of applications, the Stem Cell and Progenitor Cell-based Therapeutics market is segmented into tissue engineering, stem cells, gene therapy, drug discovery, and nanotechnology. The tissue engineering segment held the largest market revenue share of 34.9% in 2025, driven by increasing use of stem cells in regenerative scaffolds, organ repair, and wound healing applications. Tissue engineering solutions are gaining traction in orthopedics, cardiology, dermatology, and reconstructive surgery where damaged tissues require functional restoration. Growing demand for personalized medicine and bioengineered implants is supporting adoption globally. Healthcare providers increasingly prefer regenerative techniques that reduce recovery time and improve long-term outcomes. Significant investments in biomaterials and 3D bioprinting technologies are strengthening segment growth. Research institutes are also expanding studies involving stem-cell seeded matrices for tissue regeneration. Rising chronic disease burden and traumatic injury cases further increase demand. Strong collaboration between biotech firms and hospitals supports commercialization. Therefore, tissue engineering remained the leading application segment in 2025.

The gene therapy segment is expected to witness the fastest CAGR of 21.3% from 2026 to 2033, driven by the convergence of stem cell science with genetic modification technologies. Gene-corrected stem cells are increasingly being explored for inherited and degenerative diseases. Rising approvals of advanced therapy medicinal products and expanding precision medicine programs are accelerating growth. Continued progress in CRISPR and viral vector delivery systems is expected to create substantial future opportunities.

- By End-Users

On the basis of end-users, the Stem Cell and Progenitor Cell-based Therapeutics market is segmented into pharmaceutical and biotechnology industries, hospitals, research institutes, biotechnology companies, and others. The pharmaceutical and biotechnology industries segment accounted for the largest market revenue share of 42.6% in 2025, driven by high R&D spending, extensive clinical trial pipelines, and commercialization capabilities. These organizations are leading the development of stem cell therapeutics for oncology, neurology, cardiovascular, and autoimmune disorders. Large companies possess advanced manufacturing infrastructure required for scalable cell processing and regulatory compliance. Strategic partnerships with academic centers and contract manufacturers are further strengthening segment leadership. Growing investor interest in regenerative medicine has increased funding for pipeline expansion. These companies also benefit from intellectual property ownership and global distribution networks. Rising acquisitions of innovative cell therapy startups are supporting market consolidation. Demand for next-generation biologics and personalized treatments further enhances growth. Consequently, pharmaceutical and biotechnology industries remained dominant in 2025.

The research institutes segment is projected to register the fastest CAGR of 20.8% from 2026 to 2033, fueled by expanding government grants and translational medicine programs. Universities and public laboratories are actively conducting early-stage stem cell research and proof-of-concept studies. Increasing collaboration with private industry for technology transfer is accelerating commercialization pathways. Growing focus on rare diseases and novel cell platforms is expected to sustain rapid expansion.

Stem Cell and Progenitor Cell-based Therapeutics Market Regional Analysis

- North America dominated the stem cell and progenitor cell-based therapeutics market with the largest revenue share of approximately 44.1% in 2025, characterized by advanced biotechnology infrastructure, high healthcare expenditure, strong presence of leading regenerative medicine companies, and increasing clinical trial activity

- Healthcare institutions and research organizations in the region highly value innovative regenerative therapies, advanced cell processing technologies, and expanding applications in oncology, orthopedics, neurology, and autoimmune disorders

- This widespread adoption is further supported by robust funding for translational medicine, favorable reimbursement pathways, and strong collaborations between biotechnology firms, academic centers, and hospitals, establishing stem cell and progenitor cell-based therapeutics as a transformative segment in modern medicine

U.S. Stem Cell and Progenitor Cell-based Therapeutics Market Insight

The U.S. stem cell and progenitor cell-based therapeutics market captured the largest revenue share in 2025 within North America, fueled by the rapid expansion of regenerative medicine programs, increasing FDA approvals for advanced cell therapies, and growing investments in biotechnology innovation. Healthcare providers are increasingly prioritizing personalized treatment approaches, tissue repair solutions, and next-generation biologics. Moreover, the presence of leading pharmaceutical and biotech companies, combined with strong clinical research infrastructure, is significantly contributing to the market's expansion.

Europe Stem Cell and Progenitor Cell-based Therapeutics Market Insight

The Europe stem cell and progenitor cell-based therapeutics market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing investments in biomedical research, growing adoption of regenerative medicine, and supportive healthcare innovation frameworks. The region’s strong academic research ecosystem and rising demand for advanced therapies in chronic and degenerative diseases are fostering market growth. Significant progress is being witnessed across hospitals, specialty clinics, and research institutes, with cell-based therapeutics being integrated into advanced treatment pipelines.

U.K. Stem Cell and Progenitor Cell-based Therapeutics Market Insight

The U.K. stem cell and progenitor cell-based therapeutics market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing government support for life sciences innovation, rising clinical trial activity, and growing demand for precision regenerative therapies. Healthcare institutions are emphasizing advanced treatment development for neurological disorders, cancer, and musculoskeletal conditions. The country’s strong biotechnology ecosystem and translational research capabilities are expected to continue stimulating market growth.

Germany Stem Cell and Progenitor Cell-based Therapeutics Market Insight

The Germany stem cell and progenitor cell-based therapeutics market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of regenerative healthcare solutions, rising healthcare investments, and strong pharmaceutical manufacturing capabilities. Germany’s advanced healthcare infrastructure, combined with its focus on innovation and precision medicine, promotes the adoption of stem cell and progenitor cell-based therapies across hospitals and research centers. The integration of cell therapy platforms with advanced diagnostics and personalized medicine strategies is also becoming increasingly prevalent.

Asia-Pacific Stem Cell and Progenitor Cell-based Therapeutics Market Insight

The Asia-Pacific stem cell and progenitor cell-based therapeutics market is poised to grow at the fastest CAGR of approximately 12.8% during the forecast period, driven by rising healthcare investments, expanding biotechnology sector, supportive regulatory reforms, and growing adoption of advanced regenerative therapies. Increasing demand for innovative chronic disease treatments, improving healthcare access, and growing public-private partnerships are accelerating market growth across the region.

Japan Stem Cell and Progenitor Cell-based Therapeutics Market Insight

The Japan stem cell and progenitor cell-based therapeutics market is gaining momentum due to the country’s advanced biotechnology capabilities, aging population, and strong demand for innovative healthcare solutions. The Japanese market places significant emphasis on regenerative medicine, and adoption is driven by increasing use of cell therapies for age-related diseases, neurological disorders, and tissue repair applications. Supportive regulatory pathways and strong academic-industry collaboration are further fueling growth. Moreover, Japan’s aging population is expected to spur demand for advanced therapies that improve quality of life and long-term patient outcomes.

China Stem Cell and Progenitor Cell-based Therapeutics Market Insight

The China stem cell and progenitor cell-based therapeutics market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding biotechnology industry, increasing healthcare expenditure, and rising clinical research activity. China stands as one of the largest emerging markets for regenerative medicine, and stem cell therapies are becoming increasingly popular in oncology, orthopedics, and chronic disease management. The push toward biopharmaceutical innovation, supportive government initiatives, and the availability of cost-effective manufacturing capabilities are key factors propelling the market in China.

Stem Cell and Progenitor Cell-based Therapeutics Market Share

The Stem Cell and Progenitor Cell-based Therapeutics industry is primarily led by well-established companies, including:

- Mesoblast Limited (Australia)

- Athersys, Inc. (U.S.)

- Fate Therapeutics, Inc. (U.S.)

- BlueRock Therapeutics LP (U.S.)

- Lineage Cell Therapeutics, Inc. (U.S.)

- Vericel Corporation (U.S.)

- STEMCELL Technologies Inc. (Canada)

- Takeda Pharmaceutical Company Limited (Japan)

- Novartis AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Lonza Group AG (Switzerland)

- Thermo Fisher Scientific Inc. (U.S.)

- FUJIFILM Holdings Corporation (Japan)

- Catalent, Inc. (U.S.)

- Sartorius AG (Germany)

- Pluristem Therapeutics Inc. (Israel)

- Gamida Cell Ltd. (Israel)

- Stempeutics Research Pvt. Ltd. (India)

Latest Developments in Global Stem Cell and Progenitor Cell-based Therapeutics Market

- In January 2021, BlueRock Therapeutics, a subsidiary of Bayer AG, announced continued advancement of DA01, an investigational pluripotent stem cell-derived dopaminergic neuron therapy for Parkinson’s disease, following encouraging early-stage clinical progress. The development highlighted growing momentum in stem cell-based regenerative therapies for neurological disorders

- In June 2021, Mesoblast Limited reported progress in the commercialization and regulatory expansion of its mesenchymal stem cell therapy programs targeting inflammatory and regenerative conditions. The company continued strengthening its late-stage pipeline for graft-versus-host disease and cardiovascular disorders

- In April 2022, Fate Therapeutics expanded clinical development of its induced pluripotent stem cell (iPSC)-derived cell therapy portfolio, including off-the-shelf immune cell products for oncology indications. This marked a significant advancement in scalable progenitor and stem cell-based therapeutic manufacturing

- In November 2022, Lineage Cell Therapeutics announced progress in its OpRegen retinal pigment epithelium cell therapy program for geographic atrophy associated with dry age-related macular degeneration. The therapy demonstrated continued promise in regenerative ophthalmology applications

- In April 2023, the U.S. FDA approved Omisirge (omidubicel-onlv), developed by Gamida Cell, for use in adults and children aged 12 years and older undergoing umbilical cord blood transplantation for hematologic malignancies. The approval represented a major milestone in stem cell and progenitor cell-based therapeutics, improving neutrophil recovery after transplant

- In December 2023, Vertex Pharmaceuticals and CRISPR Therapeutics received approvals in multiple markets for Casgevy, a gene-edited therapy using modified patient stem cells for sickle cell disease and beta thalassemia. The launch underscored the commercial potential of autologous stem cell-based advanced therapeutics

- In December 2024, Mesoblast Limited received U.S. FDA approval for Ryoncil (remestemcel-L) for steroid-refractory acute graft-versus-host disease in pediatric patients. This became the first FDA-approved mesenchymal stromal cell therapy in the United States, significantly advancing the regenerative medicine market

- In April 2025, Abeona Therapeutics received U.S. FDA approval for Zevaskyn (pz-cel), the first cell-based gene therapy approved for recessive dystrophic epidermolysis bullosa. The therapy uses genetically corrected patient skin cells and demonstrated the expanding commercial viability of personalized stem/progenitor cell therapeutics

- In July 2025, Steminent Biotherapeutics announced completion of regulatory documentation in Japan for Stemchymal, an allogeneic mesenchymal stem cell therapy for Spinocerebellar Ataxia, with filing preparations through partner REPROCELL. This development highlighted growing commercialization of stem cell therapies for rare neurological diseases

- In September 2025, Bayer AG announced that BlueRock Therapeutics had advanced its Parkinson’s stem cell therapy into Phase III clinical trials, marking one of the most advanced regenerative neurology programs globally. The company also confirmed ongoing investment in dedicated cell therapy manufacturing infrastructure

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.