Global Stereotactic Surgery Market

Market Size in USD Billion

USD

35.68 Billion

USD

49.02 Billion

2024

2032

USD

35.68 Billion

USD

49.02 Billion

2024

2032

| 2025 - 2032 | |

| USD 35.68 Billion | |

| USD 49.02 Billion | |

| % | |

|

Stereotactic Surgery Market Size

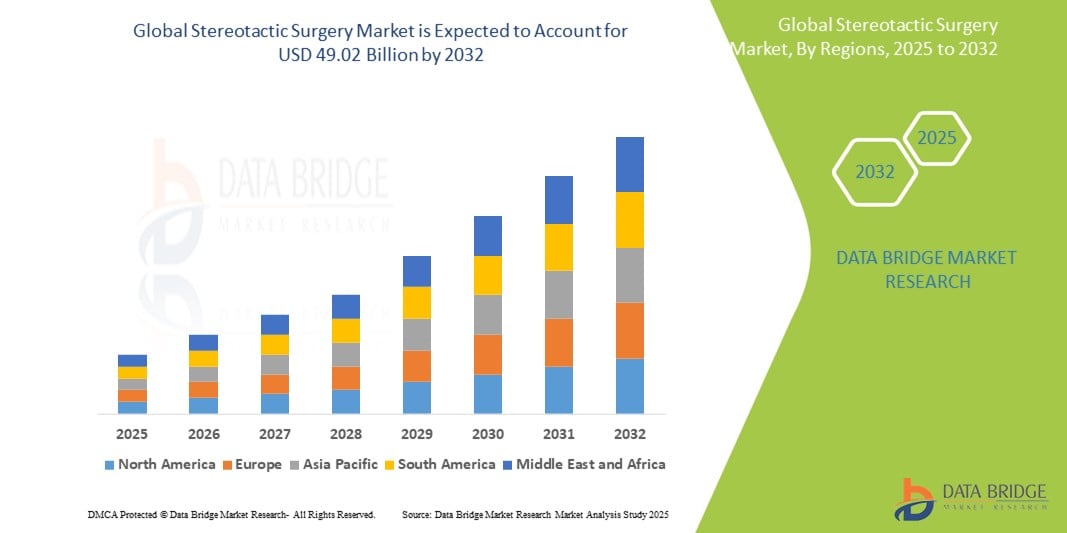

- The Global Stereotactic Surgery Market size was valued at USD 35.68 billion in 2024 and is expected to reach USD 49.02 billion by 2032, at a CAGR of 4.05% during the forecast period

- The market growth is largely driven by the increasing prevalence of neurological disorders and advancements in non-invasive surgical technologies such as Gamma Knife, Cyber Knife, and Proton Beam Therapy. These innovations are enabling precise targeting of abnormal tissues, reducing surgical complications and recovery time

- Additionally, the growing demand for minimally invasive procedures, coupled with the rising number of patients suffering from brain tumors, epilepsy, Parkinson’s disease, and arteriovenous malformations, is contributing to the accelerated adoption of stereotactic surgery. These converging factors are significantly propelling the market’s expansion across both developed and emerging healthcare markets.

Stereotactic Surgery Market Analysis

- Stereotactic surgery, a form of minimally invasive surgical intervention that uses 3D imaging for precise targeting of anatomical structures, is becoming increasingly critical in the treatment of complex neurological conditions such as brain tumors, epilepsy, Parkinson’s disease, and arteriovenous malformations. Its precision, reduced operative trauma, and shorter recovery times are making it the preferred alternative to traditional open brain surgeries

- The growing demand for stereotactic surgical procedures is primarily driven by the rising global burden of neurological disorders, the increasing availability of advanced imaging and robotic technologies, and a shift towards non-invasive treatment approaches in both developed and emerging healthcare systems

- North America dominates the global stereotactic surgery market, holding the largest revenue share of 41.3% in 2025, owing to robust healthcare infrastructure, early adoption of advanced surgical technologies, and the presence of leading device manufacturers. The U.S. leads the region with a significant number of Gamma Knife and Cyber Knife installations in high-volume hospitals and research institutions

- Asia-Pacific is expected to be the fastest-growing region in the stereotactic surgery market over the forecast period, fueled by a rising patient population, increasing healthcare investments, improving diagnostic infrastructure, and expanding access to advanced neurosurgical procedures in countries like China, India, and Japan

- The Gamma Knife segment is projected to dominate the stereotactic surgery market with a market share of 38.7% in 2025, due to its proven track record in non-invasive treatment of brain lesions and tumors, along with strong clinical efficacy and favorable reimbursement policies in key markets.

Report Scope and Stereotactic Surgery Market Segmentation

|

Attributes |

Stereotactic Surgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Stereotactic Surgery Market Trends

“Rising Adoption of Robotic Assistance and AI in Precision Neurosurgery”

- A significant and rapidly evolving trend in the global stereotactic surgery market is the increasing incorporation of robotic-assisted systems and artificial intelligence (AI) into neurosurgical procedures to enhance accuracy, safety, and patient outcomes. These technologies are transforming the precision and efficiency of stereotactic surgeries by enabling better visualization, real-time guidance, and automated navigation during interventions

- For instance, Renishaw’s neuromate stereotactic robot enables precise targeting in deep brain stimulation (DBS) and epilepsy treatment, significantly reducing surgical time and risk. Similarly, Brainlab’s AI-enabled platforms integrate high-resolution imaging with software algorithms to enhance preoperative planning and intraoperative guidance for stereotactic procedures

- AI applications in stereotactic surgery also include predictive analytics for surgical planning, automated trajectory mapping, and adaptive radiation delivery, particularly in radiosurgery techniques like Gamma Knife and Cyber Knife. These tools not only reduce variability but also optimize treatment personalization based on individual patient anatomy and pathology

- The integration of robotic platforms with advanced 3D imaging systems such as MRI and CT has also facilitated frameless stereotactic surgery, offering less invasive alternatives for patients while expanding procedural capabilities for surgeons. Systems like ROSATM by Zimmer Biomet and Stealth Autoguide by Medtronic exemplify this shift toward image-guided, robotic-enabled precision

- This trend is setting new standards for minimally invasive neurosurgical care, with hospitals and surgical centers increasingly investing in such technologies to improve procedural success rates and reduce postoperative complications. As healthcare providers seek to differentiate through technological excellence, the demand for AI- and robot-enhanced stereotactic systems is expected to continue growing

Stereotactic Surgery Market Dynamics

Driver

“Growing Neurological Disease Burden and Demand for Minimally Invasive Procedures”

- The global surge in neurological conditions such as brain tumors, epilepsy, Parkinson’s disease, and arteriovenous malformations (AVMs) is a key driver of the stereotactic surgery market. These disorders often require highly precise interventions, for which stereotactic techniques offer optimal treatment solutions with minimal damage to surrounding tissues

- For Instance, According to the World Health Organization, neurological disorders are now the leading cause of disability-adjusted life years (DALYs) globally, underscoring the urgent need for innovative treatment approaches. In response, healthcare providers are increasingly adopting stereotactic surgery methods that offer targeted therapy with fewer complications and faster recovery

- Furthermore, the rising preference for outpatient and minimally invasive procedures is driving adoption of stereotactic systems in ambulatory surgery centers and specialized neurosurgical clinics. Gamma Knife, Cyber Knife, and LINAC-based systems offer non-invasive alternatives to open surgery, enabling treatment of inoperable or hard-to-reach lesions

- Technological advancements in image guidance, robotic surgery, and real-time monitoring are making stereotactic procedures more accessible and reliable, while favorable reimbursement policies in key markets further support their adoption

Restraint/Challenge

“High Equipment Costs and Limited Access in Low-Income Regions”

- Despite their clinical advantages, stereotactic surgery systems involve significant capital expenditure, including the cost of equipment, imaging systems, and specialized surgical infrastructure. The installation of devices such as Gamma Knife and Proton Beam Therapy units often requires millions of dollars in investment, posing a major barrier for smaller healthcare facilities and hospitals in developing nations

- In addition to cost, the shortage of skilled neurosurgeons and radiological specialists limits the widespread implementation of stereotactic procedures in lower-income and rural regions. Access to advanced imaging and support services, which are essential for these procedures, remains uneven across many parts of the world

- Moreover, the high maintenance and training requirements for operating complex systems like Cyber Knife and robotic surgical units add to the total cost of ownership, discouraging adoption among institutions with constrained budgets

- To overcome these challenges, manufacturers are working on cost-effective and compact stereotactic platforms, along with offering flexible leasing or financing models. Governments and private players are also investing in capacity-building programs to train more specialists in minimally invasive neurosurgical techniques, which will be essential for unlocking broader market potential

Stereotactic Surgery Market Scope

The market is segmented on the basis of product type, application, and end user.

• By Product Type

On the basis of product type, the stereotactic surgery market is segmented into Gamma Knife, Linear Accelerators (LINAC), Proton Beam Therapy (PBRT), and Cyber Knife.The Gamma Knife segment dominates the market with the largest revenue share of 38.7% in 2025, driven by its precision and widespread use in radiosurgical treatment of brain tumors and functional disorders. Its ability to deliver high-dose radiation to specific targets without damaging surrounding tissues makes it the standard in many neurosurgical centers.

The Cyber Knife segment is expected to witness the fastest growth rate of 13.5% CAGR from 2025 to 2032, fueled by its robotic versatility, real-time tracking, and growing application in treating both cranial and extracranial conditions. Increased global installations and clinical preference for non-invasive, image-guided solutions support this strong growth trajectory.

• By Application

On the basis of application, the market is segmented into Brain Tumor Treatment, Arteriovenous Malformations (AVM) Treatment, Parkinson’s Disease, Epilepsy, and Others.The Brain Tumor Treatment segment holds the largest revenue share of 45.2% in 2025, driven by the high global incidence of brain tumors and the suitability of stereotactic systems like Gamma Knife and LINAC for delivering targeted treatment. These systems are increasingly used as a frontline or adjunct therapy in both benign and malignant tumor cases.

The Epilepsy segment is projected to register the fastest CAGR of 12.9% from 2025 to 2032, supported by rising adoption of minimally invasive stereotactic procedures, such as laser ablation and DBS. These techniques are proving to be highly effective in treating drug-resistant epilepsy cases, especially in pediatric and adult patients where open surgery is riskier.

• By End User

On the basis of end user, the market is segmented into Hospitals and Ambulatory Surgery Centres.The Hospitals segment accounts for the largest market share of 64.3% in 2025, due to their access to advanced surgical systems, skilled neurosurgical teams, and comprehensive post-operative care. Hospitals also receive more funding for high-cost equipment like Proton Beam Therapy, making them central to stereotactic surgery adoption.

The Ambulatory Surgery Centres (ASCs) segment is expected to grow at the fastest CAGR of 11.6% from 2025 to 2032, driven by the healthcare industry’s shift towards outpatient care. ASCs are increasingly equipped with stereotactic technologies due to growing patient demand for less invasive, shorter-duration procedures with minimal hospitalization.

Stereotactic Surgery Market Regional Analysis

- North America dominates the global stereotactic surgery market with the largest revenue share of 41.3% in 2025, driven by the high prevalence of neurological disorders, availability of advanced neurosurgical infrastructure, and the early adoption of precision-based surgical technologies

- The region benefits from strong reimbursement policies, a well-established healthcare system, and the presence of leading medical device manufacturers offering Gamma Knife, Cyber Knife, and Proton Beam Therapy systems

- The increasing demand for minimally invasive treatments and the growing number of outpatient neurosurgery centers contribute significantly to the region’s leadership in the global market

U.S. Stereotactic Surgery Market Insight

The U.S. stereotactic surgery market captured 82% of North America’s revenue share in 2025, led by a robust network of academic medical centers, high investment in neurological R&D, and rapid integration of robotic and image-guided surgical systems. Patients in the U.S. increasingly prefer non-invasive radiosurgery options, and hospitals are adopting advanced tools such as Cyber Knife and frameless stereotactic systems to enhance precision and safety. Additionally, rising cases of brain tumors and Parkinson’s disease, coupled with the country’s leadership in medical technology innovation, are key growth drivers.

Europe Stereotactic Surgery Market Insight

The European stereotactic surgery market is projected to expand at a healthy CAGR throughout the forecast period, driven by rising demand for functional neurosurgery, increasing elderly population, and growing focus on early diagnosis and treatment. Favorable regulatory frameworks, government-backed healthcare modernization programs, and increased adoption of non-invasive surgical techniques are boosting the market. Key countries in the region are actively investing in advanced neurosurgical equipment and training programs to expand access to stereotactic procedures.

U.K. Stereotactic Surgery Market Insight

The U.K. stereotactic surgery market is expected to grow at a notable CAGR, supported by rising adoption of precision-based radiosurgery techniques in NHS hospitals and private clinics. Increasing awareness of early brain tumor detection and the expansion of outpatient surgical services are fueling demand. The country’s strong academic partnerships and clinical research in neuro-oncology are also contributing to the wider use of stereotactic tools, especially for Parkinson’s and epilepsy treatment.

Germany Stereotactic Surgery Market Insight

The German stereotactic surgery market is projected to grow at a considerable CAGR, driven by the country's highly advanced medical infrastructure, aging population, and commitment to innovation in medical technology. Germany’s adoption of robotic-assisted stereotactic systems, along with increased public healthcare expenditure, is enabling hospitals to upgrade surgical capabilities. Emphasis on quality care and accurate treatment outcomes is further accelerating the use of advanced stereotactic platforms.

Asia-Pacific Stereotactic Surgery Market Insight

The Asia-Pacific stereotactic surgery market is poised to grow at the fastest CAGR of over 14.8% in 2025, propelled by rising neurological disease incidence, expanding medical tourism, and significant investments in healthcare infrastructure. Countries like China, India, Japan, and South Korea are rapidly adopting stereotactic systems to meet the growing demand for minimally invasive neurosurgical solutions. Government-led initiatives to modernize healthcare delivery and increase access to cancer and neurological treatment centers are driving regional growth.

Japan Stereotactic Surgery Market Insight

The Japan stereotactic surgery market is gaining momentum owing to the country’s leadership in advanced robotics, strong neurosurgical capabilities, and high public health awareness. Demand is being driven by an aging population prone to Parkinson’s disease and brain disorders, as well as the rising number of facilities offering Gamma Knife and Cyber Knife procedures. Integration with AI and imaging systems is becoming increasingly prevalent, aligning with Japan’s innovation-focused healthcare ecosystem.

.

China Stereotactic Surgery Market Insight

The China stereotactic surgery market accounted for the largest market revenue share in Asia-Pacific in 2025, supported by rapid urbanization, growing healthcare investments, and rising rates of brain tumor diagnosis. China’s increasing focus on building specialized cancer and neurological hospitals, along with local manufacturing of radiosurgical equipment, is driving accessibility and adoption. Partnerships with global medical device companies and domestic innovation are fueling growth, especially in tertiary hospitals across major metropolitan regions.

Stereotactic Surgery Market Share

The Stereotactic Surgery industry is primarily led by well-established companies, including:

- Koninklijke Philips N.V. (Netherlands)

- Huiheng Group (China)

- MITSUBISHI HEAVY INDUSTRIES, LTD. (Japan)

- Renishaw plc (U.K.)

- Varian Medical Systems, Inc. (U.S.)

- Hitachi Medical Systems Europe (Holding) AG (Switzerland)

- Accuray Incorporated (U.S.)

- Ferring B.V. (Switzerland)

- SHINVA MEDICAL INSTRUMENT CO., LTD. (China)

- Elekta AB (publ) (Sweden)

- Radiological Society of North America (RSNA) (U.S.)

- Mevion Medical Systems (U.S.)

- Siemens Healthineers (Germany)

- ProTom International (U.S.)

- Provision Healthcare (U.S.)

- Nordion (Canada) Inc. (Canada)

- Vision RT Ltd (U.K.)

Latest Developments in Global Stereotactic Surgery Market

- In July 2024, Apollo Cancer Centres partnered with Accuray to introduce the Indian sub-continent’s first robotic stereotactic radiotherapy program, aiming to enhance precision in cancer treatment through advanced non-invasive technology

- In January 2024, ClearPoint Neuro received FDA clearance for its SmartFrame OR stereotactic system, designed to streamline neurosurgical procedures with greater accuracy and workflow efficiency

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.