Global Subdural Hematoma Treatment Market

Market Size in USD Billion

USD

1.76 Billion

USD

2.54 Billion

2025

2033

USD

1.76 Billion

USD

2.54 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.76 Billion | |

| USD 2.54 Billion | |

| % | |

|

Subdural Hematoma Treatment Market Size

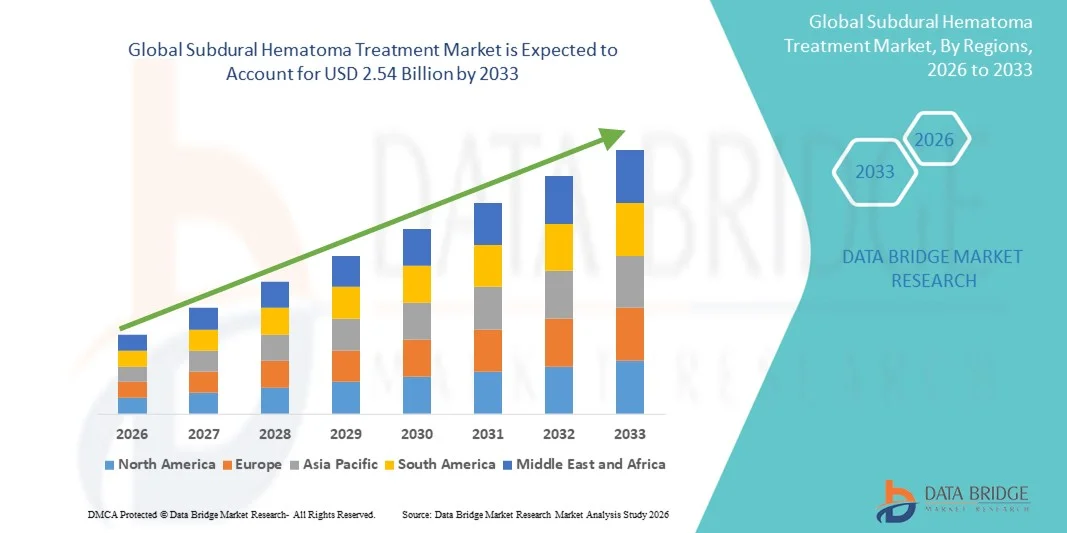

- The global subdural hematoma treatment market size was valued at USD 1.76 billion in 2025 and is expected to reach USD 2.54 billion by 2033, at a CAGR of 4.70% during the forecast period

- The market growth is largely fueled by the rising prevalence of head injuries, aging population, and increasing incidence of neurological disorders, driving demand for advanced surgical and minimally invasive treatment options

- Furthermore, growing investments in healthcare infrastructure, technological advancements in neuroimaging and surgical devices, and rising patient awareness about timely intervention are positioning subdural hematoma treatments as critical solutions in neurosurgical care. These factors are accelerating the adoption of innovative treatment modalities, thereby significantly boosting the market's growth

Subdural Hematoma Treatment Market Analysis

- Subdural hematoma treatments covering acute, subacute, and chronic forms are increasingly essential in neurology and emergency care, as they help manage intracranial bleeding, prevent neurological deterioration, and support patient recovery through both medical and surgical interventions across diverse clinical settings

- The escalating demand for subdural hematoma treatment is primarily fueled by the rising incidence of traumatic brain injuries, an expanding elderly population vulnerable to falls, and increased clinical awareness, which together are driving adoption of advanced imaging-based diagnosis and multimodal treatment approaches, including medications and surgery

- North America dominated the subdural hematoma treatment market with the largest revenue share of 38.7% in 2025, supported by advanced diagnostic infrastructure such as CT and MRI, high accessibility to neurosurgical care, and strong presence of specialized hospitals, with the U.S. witnessing notable growth in treatment procedures across hospitals and clinics

- Asia-Pacific is expected to be the fastest-growing region in the subdural hematoma treatment market during the forecast period due to expanding healthcare capacity, rising trauma incidence, increasing investment in neuro-critical care, and higher adoption of hospital and online pharmacy channels for treatment access

- Acute Subdural Hematoma segment dominated the subdural hematoma treatment market with a market share of 46.8% in 2025, driven by its higher prevalence in emergency trauma cases and the frequent need for rapid diagnosis using CT scans and prompt interventions such as surgery, anticonvulsants, and supportive therapies in hospital settings

Report Scope and Subdural Hematoma Treatment Market Segmentation

|

Attributes |

Subdural Hematoma Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Subdural Hematoma Treatment Market Trends

Advancement of AI-Driven Neuroimaging and Precision Treatment Planning

- A significant and accelerating trend in the global subdural hematoma treatment market is the expanding integration of artificial intelligence (AI) into neuroimaging modalities such as CT and MRI, allowing clinicians to detect hematoma size, severity, and progression with greater speed, accuracy, and predictive capability in both emergency and hospital environments

- For instance, AI-enabled CT analysis platforms from companies such as RapidAI support automated detection of intracranial bleeding, helping physicians rapidly classify acute, subacute, or chronic subdural hematomas and triage patients who require urgent surgical or medical intervention

- AI integration in subdural hematoma care enables features such as automated volumetric assessment, progression alerts, and decision-support tools that can guide optimal treatment whether anticonvulsant therapy, diuretics, corticosteroids, or surgery based on evolving clinical data and patient-specific risk profiles

- Furthermore, intelligent diagnostic platforms allow neurologists and neurosurgeons to streamline care pathways, offering the ability to review imaging, laboratory results, and treatment recommendations through unified interfaces that improve workflow and reduce diagnostic delays

- The seamless integration of AI-driven imaging with hospital electronic health record systems facilitates comprehensive monitoring, enabling clinicians to coordinate treatment across surgery, intensive care, physical therapy, and follow-up recovery, creating a more connected and efficient neurology care ecosystem

- This trend toward more intelligent, automated, and data-driven diagnostic and treatment systems is fundamentally reshaping expectations in neuro-critical care. Consequently, companies such as Viz.ai are developing AI-powered brain hemorrhage detection tools that support rapid identification of subdural hematomas and faster neurosurgical decision-making

- The demand for AI-enhanced imaging and precision treatment platforms is growing rapidly across clinics and hospitals as providers increasingly prioritize accuracy, speed, and integrated management of neurological emergencies

Subdural Hematoma Treatment Market Dynamics

Driver

Growing Need Due to Rising Traumatic Brain Injuries and Aging Population

- The increasing global incidence of traumatic brain injuries (TBIs), coupled with the rapidly growing elderly population that is more prone to falls and chronic subdural hematomas, is a significant driver for the rising demand for advanced treatment solutions

- For instance, in March 2025, BrainScope announced progress in portable EEG-based head-injury assessment tools intended to support earlier identification of intracranial bleeding, demonstrating how technological innovation is shaping the future of brain trauma diagnostics

- As healthcare providers become more aware of neurological risks and seek timely intervention, subdural hematoma treatments offer essential capabilities including rapid imaging, anticonvulsant therapy, corticosteroid management, and surgical decompression, making them indispensable in emergency and neuro-critical care

- Furthermore, growing adoption of advanced CT/MRI systems, along with the increasing availability of minimally invasive surgical tools, is strengthening the role of subdural hematoma care within hospitals and trauma centers, improving patient outcomes and reducing complications

- The need for faster diagnosis, improved treatment efficacy, and integrated patient management is propelling the adoption of multimodal therapies, with clinics and hospitals expanding capabilities through specialized neurosurgical units and enhanced rehabilitation services

- The convenience of improved imaging speed, remote access to diagnostic data, and the ability to monitor patients through digital neuro-monitoring systems are key factors accelerating treatment adoption in both developed and developing healthcare markets

- The trend toward integrated neurological care pathways and the rising number of trained neurosurgeons further contribute to sustained market growth across global healthcare ecosystems

Restraint/Challenge

Cybersecurity of AI Systems and High Cost of Advanced Neurological Care

- Concerns surrounding the cybersecurity vulnerabilities of AI-enabled diagnostic platforms and connected hospital systems pose a significant challenge to broader adoption, as unauthorized access to imaging data or clinical decision software could compromise patient safety and clinical workflows

- For instance, reported vulnerabilities in healthcare IT and imaging software have raised caution among hospitals implementing AI-driven diagnostic tools, making some institutions hesitant to rely heavily on connected platforms for critical neurological evaluations

- Addressing these cybersecurity concerns through strong data-protection frameworks, secure encryption, and regular software updates is essential for building trust among clinicians and hospital administrators who rely on these systems for urgent diagnostic decisions

- In addition, the relatively high cost of advanced neurosurgical procedures, AI-powered imaging tools, and postoperative rehabilitation services can act as a barrier in regions with limited healthcare budgets or lower insurance coverage, restricting patient access to optimal care

- While cost-effective imaging and treatment options are gradually expanding, the perceived premium associated with advanced neurological technologies can hinder widespread adoption, particularly in low- and middle-income countries where infrastructure is still developing

- Overcoming these challenges through improved cybersecurity standards, provider education on data protection, and development of more affordable diagnostic and treatment solutions will be essential for achieving broader global adoption

Subdural Hematoma Treatment Market Scope

The market is segmented on the basis of type, treatment, diagnosis, dosage, route of administration, symptoms, end-users, and distribution channel.

- By Type

On the basis of type, the subdural hematoma treatment market is segmented into acute subdural hematoma, subacute subdural hematoma, and chronic subdural hematoma. The acute subdural hematoma segment dominated the market with the largest revenue share of 46.8% in 2025, driven by the high incidence of trauma-related cases requiring immediate intervention. Acute SDH often results from high-impact injuries, increasing the need for rapid surgical management and intensive monitoring in emergency care settings. The segment benefits from advanced neuroimaging tools and improved surgical outcomes, particularly with minimally invasive surgical techniques. In addition, increased awareness and improved emergency response systems accelerate diagnosis and treatment timelines. The rising number of road accidents and fall-related injuries globally further strengthens this segment’s dominance.

The chronic subdural hematoma segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by the increasing aging population and higher prevalence of age-related brain atrophy. Chronic SDH typically develops gradually, making early detection more common in elderly patients with frequent medical monitoring. The growing adoption of minimally invasive burr-hole drainage and catheter-based evacuation techniques also contributes to strong forecasted growth. In addition, chronic cases have lower surgical risks and shorter hospitalization periods, making treatment more accessible in emerging markets. Expanding healthcare access and improved postoperative care drive further adoption.

- By Treatment

On the basis of treatment, the market is segmented into anticonvulsants, diuretics, corticosteroids, surgery, catheter, physical therapy, speech therapy, vitamin K therapy, and others. The surgery segment dominated the market in 2025, primarily due to the necessity of surgical intervention in moderate to severe cases to relieve intracranial pressure. Surgical procedures such as craniotomy, decompressive craniectomy, and burr-hole drainage remain the gold standard for acute and recurrent cases. Technological advancements, including neuronavigation systems and endoscopic assistance, continue to improve clinical outcomes. The rise in trauma cases and greater availability of neurosurgical centers globally strengthen the segment’s market share. Increasing adoption of minimally invasive neurosurgical techniques has further boosted utilization.

The catheter-based treatment segment is expected to witness the fastest growth from 2026 to 2033, driven by its minimally invasive nature and shorter recovery times. Catheter-assisted drainage is becoming increasingly preferred for chronic subdural hematoma due to reduced complications and hospital stays. Ongoing innovations in catheter design and placement techniques enhance safety and efficiency. The growing preference for outpatient or short-stay procedures also contributes to rapid adoption. As healthcare facilities focus on cost-effective treatment strategies, catheter-based interventions continue to gain traction worldwide.

- By Diagnosis

On the basis of diagnosis, the market is segmented into CT scan, MRI, and others. The CT scan segment held the largest market share in 2025, supported by its widespread availability, rapid imaging speed, and high sensitivity in detecting acute bleeding. CT remains the first-line diagnostic modality in emergency settings, enabling quick assessment of hematoma size and midline shift. Its cost-effectiveness compared to MRI further supports dominance across developing and developed markets. Technological improvements in multi-slice CT have enhanced accuracy and reduced radiation exposure. Increasing installation of CT scanners in trauma and emergency departments strengthens segment leadership.

The MRI segment is projected to witness the fastest growth from 2026 to 2033, driven by its superior imaging resolution and ability to detect subtle or chronic hematomas. MRI is especially valuable in identifying mixed-density or recurrent cases where CT may be less conclusive. Growing preference for advanced imaging in neurological evaluation and research further promotes adoption. The expansion of MRI facilities in emerging economies enhances accessibility. Its ability to differentiate between acute, subacute, and chronic presentations supports precise clinical decision-making.

- By Dosage

On the basis of dosage, the market is segmented into tablet, injection, and others. The injection segment dominated the market in 2025, primarily due to the need for rapid drug delivery in emergency and acute care settings. Injections are widely used for anticonvulsants, diuretics, corticosteroids, and emergency supportive therapies. The segment benefits from its fast action and suitability for hospital administration under monitored care. Increased hospitalization rates for traumatic brain injuries contribute significantly to segment dominance. The availability of multiple injectable formulations further strengthens its market position.

The tablet segment is expected to register the fastest growth between 2026 and 2033, driven by its rising use in chronic management, rehabilitation, and long-term symptom control. Tablets are widely adopted in outpatient settings for anticonvulsants and supportive therapies. Their cost-effectiveness, ease of administration, and high patient compliance boost growth. Increasing awareness and early diagnosis of chronic SDH cases result in prolonged medication use. The expanding availability of generic oral formulations further stimulates adoption.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, intravenous, and others. The intravenous segment dominated the market in 2025, due to its essential role in acute and emergency treatment where rapid drug action is critical. IV administration is the standard for diuretics, anticonvulsants, and corticosteroids in hospital settings. Its precision and immediate bioavailability make it indispensable in managing elevated intracranial pressure. Growing hospitalization rates and the rise of neurocritical care units further support segment strength. Technological improvements in IV infusion systems enhance safety and accuracy.

The oral segment is projected to witness the fastest growth from 2026 to 2033, driven by increasing treatment of chronic and stable cases outside hospital settings. Oral medications offer convenience, affordability, and strong adherence among elderly patients. Growing adoption in post-surgical rehabilitation and long-term therapy programs contributes to strong market expansion. The development of improved oral formulations with fewer side effects boosts patient acceptance. Expansion of telehealth follow-ups also supports oral therapy use.

- By Symptoms

On the basis of symptoms, the market is segmented into seizures, change in behavior, headache, nausea, confusion, dizziness, vomiting, lethargy, apathy, weakness, and others. The headache segment dominated the market in 2025, as headache is the most common presenting symptom of both acute and chronic subdural hematoma. High patient awareness of persistent or worsening headaches contributes to early diagnosis. Healthcare professionals often rely on headache symptoms to initiate imaging and further evaluation. The rising burden of age-related chronic headaches also increases diagnostic screenings. Increased adoption of pain management and early neurology consultation supports segment leadership.

The confusion segment is expected to see the fastest growth between 2026 and 2033, primarily due to its higher prevalence in elderly populations with chronic SDH. Cognitive decline and behavioral changes are increasingly recognized as early indicators, boosting timely evaluation. As the geriatric population expands, the number of patients presenting with confusion-related complaints is rising significantly. Growing clinical awareness of subtle neurological changes improves diagnostic rates. Integration of cognitive screening in primary care also enhances early detection.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The hospital segment dominated the market in 2025, driven by the need for specialized neurosurgical procedures and 24/7 emergency care availability. Hospitals remain the central point for diagnosis, imaging, surgical intervention, and postoperative monitoring. The presence of skilled neurosurgeons and advanced critical care units supports treatment of complex cases. Increasing admissions due to trauma and falls further strengthen hospital reliance. Investment in advanced neuroimaging and minimally invasive surgical technologies supports segment dominance.

The clinic segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by growing outpatient visits for follow-up, rehabilitation, and long-term monitoring. Clinics play a crucial role in managing stable chronic cases and prescribing oral medications. Increasing availability of neurologists and rehabilitation specialists at outpatient centers boosts utilization. Cost-effective care and shorter waiting times make clinics an attractive option for non-emergency management. Expansion of specialty neurology centers in emerging markets enhances growth prospects.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market in 2025, due to the high reliance on prescription-based medications for acute and hospitalized cases. Hospital pharmacies maintain essential emergency drugs, including anticonvulsants and corticosteroids. Their close integration with inpatient care ensures timely drug availability and strict monitoring. Increased surgical cases requiring postoperative medications further boost demand. Advancements in hospital pharmacy automation enhance operational efficiency.

The online pharmacy segment is projected to expand at the fastest rate from 2026 to 2033, driven by rising digital adoption and increased patient preference for convenient medication access. Growth in chronic SDH cases requiring long-term prescriptions strengthens online drug purchases. The rise of e-pharmacy platforms offering home delivery and competitive pricing accelerates market expansion. Improved regulatory frameworks in many regions are boosting patient trust and platform reliability. Elderly patients and caregivers increasingly prefer doorstep delivery for long-term medications.

Subdural Hematoma Treatment Market Regional Analysis

- North America dominated the subdural hematoma treatment market with the largest revenue share of 38.7% in 2025, supported by advanced diagnostic infrastructure such as CT and MRI, high accessibility to neurosurgical care, and strong presence of specialized hospitals, with the U.S. witnessing notable growth in treatment procedures across hospitals and clinics

- Patients and healthcare providers in the region highly value rapid diagnosis, minimally invasive surgical options, and availability of specialized neurocritical care units that enhance clinical outcomes

- This strong adoption is further supported by high healthcare spending, a mature hospital network, and widespread awareness of early neurological symptom detection, establishing North America as a leading market for both acute and chronic subdural hematoma treatment

U.S. Subdural Hematoma Treatment Market Insight

The U.S. subdural hematoma treatment market captured the largest revenue share within North America in 2025, fueled by the high incidence of traumatic brain injuries and the widespread availability of advanced neurosurgical facilities. Healthcare providers are increasingly prioritizing rapid diagnosis, minimally invasive surgical approaches, and continuous neuro-monitoring to improve patient outcomes. A growing preference for early intervention, supported by strong emergency care infrastructure, further propels treatment adoption. Moreover, increasing utilization of CT and MRI imaging, along with access to specialized neurocritical care units, is significantly contributing to the expansion of the U.S. market.

Europe Subdural Hematoma Treatment Market Insight

The Europe subdural hematoma treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent clinical guidelines and the rising need for improved neurological care in hospitals. The increasing burden of age-related chronic subdural hematoma, coupled with demand for advanced diagnostic precision, is fostering adoption of modern treatment protocols. European healthcare systems are also focusing on enhancing neurosurgical capacity and post-operative rehabilitation. The region is experiencing growing utilization of imaging tools, surgical therapies, and multidisciplinary care, with SDH treatments being implemented across both emergency and long-term care settings.

U.K. Subdural Hematoma Treatment Market Insight

The U.K. subdural hematoma treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of neurological disorders and an increasing need for timely intervention in trauma and elderly populations. In addition, a growing focus on early detection of symptoms such as confusion, headache, and behavioral changes is encouraging both hospitals and clinics to adopt improved diagnostic frameworks. The U.K.’s strong public healthcare infrastructure, combined with access to advanced neurosurgical solutions, is expected to continue stimulating market growth.

Germany Subdural Hematoma Treatment Market Insight

The Germany subdural hematoma treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by a well-developed clinical research environment and rising emphasis on innovative, patient-centered neurological treatment options. Germany’s advanced healthcare infrastructure, in combination with high adoption of CT and MRI for early diagnosis, promotes significant use of modern surgical and non-surgical therapies. The integration of advanced neurosurgical technologies, along with strong focus on safety, clinical accuracy, and evidence-based care, aligns with rising patient expectations and drives market progression.

Asia-Pacific Subdural Hematoma Treatment Market Insight

The Asia-Pacific subdural hematoma treatment market is poised to grow at the fastest CAGR during the forecast period, driven by rising trauma cases, rapid urbanization, and increasing healthcare investments across countries such as China, Japan, and India. The region’s expanding access to neuroimaging, coupled with improving hospital infrastructure, is driving the uptake of SDH treatment modalities. Furthermore, government initiatives to upgrade emergency care and neurosurgical capabilities are accelerating market adoption. As APAC strengthens its healthcare manufacturing ecosystem, access to treatment tools and diagnostic equipment is expanding across diverse patient populations.

Japan Subdural Hematoma Treatment Market Insight

The Japan subdural hematoma treatment market is gaining momentum due to the country’s rapidly aging population, high emphasis on clinical precision, and strong demand for advanced neurological care. The Japanese healthcare system places considerable importance on early diagnosis, utilizing CT and MRI widely for detection of subdural bleeding. The integration of minimally invasive surgical tools, along with expansion of rehabilitation services such as physical and speech therapy, is fueling growth. Moreover, Japan’s technologically advanced medical ecosystem is such asly to drive demand for efficient and safe treatment solutions across clinical settings.

India Subdural Hematoma Treatment Market Insight

The India subdural hematoma treatment market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, rising road-traffic injuries, and increasing access to diagnostic and neurosurgical services. India stands as one of the fastest-developing healthcare markets, with treatment adoption rising across hospitals, trauma centers, and specialty clinics. The push toward strengthening emergency medical systems and growing availability of cost-effective treatment options are major contributors to market growth. In addition, increasing awareness of neurological symptoms and expanding medical insurance coverage are propelling treatment demand across the country.

Subdural Hematoma Treatment Market Share

The Subdural Hematoma Treatment industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Stryker (U.S.)

- Integra LifeSciences Corporation (U.S.)

- B. Braun SE (Germany)

- Terumo Corporation (Japan)

- Smith & Nephew (U.K.)

- Boston Scientific Corporation (U.S.)

- Penumbra, Inc. (U.S.)

- KARL STORZ SE & Co. KG (Germany)

- Olympus Corporation (Japan)

- Richard Wolf GmbH (Germany)

- GE Healthcare (U.S.)

- Zimmer Biomet. (U.S.)

- Brainlab AG (Germany)

- Abbott (U.S.)

- MicroVention, Inc. (U.S.)

- NICO Corporation (U.S.)

- KLS Martin Group (Germany)

- Elekta AB (Sweden)

- Synaptive Medical Inc. (Canada)

What are the Recent Developments in Global Subdural Hematoma Treatment Market?

- In July 2025, follow-up real-world data on the Borvo EVAC System were released: across five medical centers treating 25 chronic SDH patients (with MMA embolization plus EVAC drainage), the system demonstrated 100% success rate in this initial cohort. Physicians involved said this combination may reshape SDH treatment, particularly for chronic cases requiring both embolization and drainage and Borvo announced plans to expand commercial distribution

- In February 2025, Arsenal Medical announced that it had completed enrollment of the initial cohort (10 patients) in its EMBO-02 Study evaluating NeoCast, a next-generation, non-adhesive, solvent-free liquid embolic agent for MMA embolization in chronic SDH. The company stated that NeoCast is designed for deep distal penetration, aiming to improve embolization efficacy and safety

- In November 2024, Balt, Inc. published results of the STEM Trial in the New England Journal of Medicine, showing that embolization of the Middle Meningeal Artery (MMA) significantly reduced treatment failure in patients with symptomatic chronic subdural hematoma compared to standard therapy alone, without increasing risk of disabling stroke or death. This represents the first randomized prospective IDE trial validating MMA embolization for cSDH treatment

- In November 2024, a multi-center study EMBOLISE Study conducted by Weill Cornell Medicine and University at Buffalo demonstrated that combining surgery with MMA embolization lowered hematoma recurrence/progression requiring re-operation to about 4%, compared to ~11% for surgery alone. The authors called for MMA embolization to become part of standard care for chronic SDH, especially given aging population risks

- In October 2024, Borvo Medical announced U.S. FDA 510(k) clearance for its Borvo EVAC System, an advanced minimally-invasive device for draining subdural hematoma. The EVAC System is designed as a modern replacement for older drainage tools, using improved materials and ergonomic design to enhance safety and imaging compatibility. Borvo described it as a response to increasing SDH drainage needs driven by head injuries and aging populations, and anticipated commercial availability

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.