Global Sun Visor Market

Market Size in USD Billion

USD

3.39 Billion

USD

5.89 Billion

2025

2033

USD

3.39 Billion

USD

5.89 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.39 Billion | |

| USD 5.89 Billion | |

| % | |

|

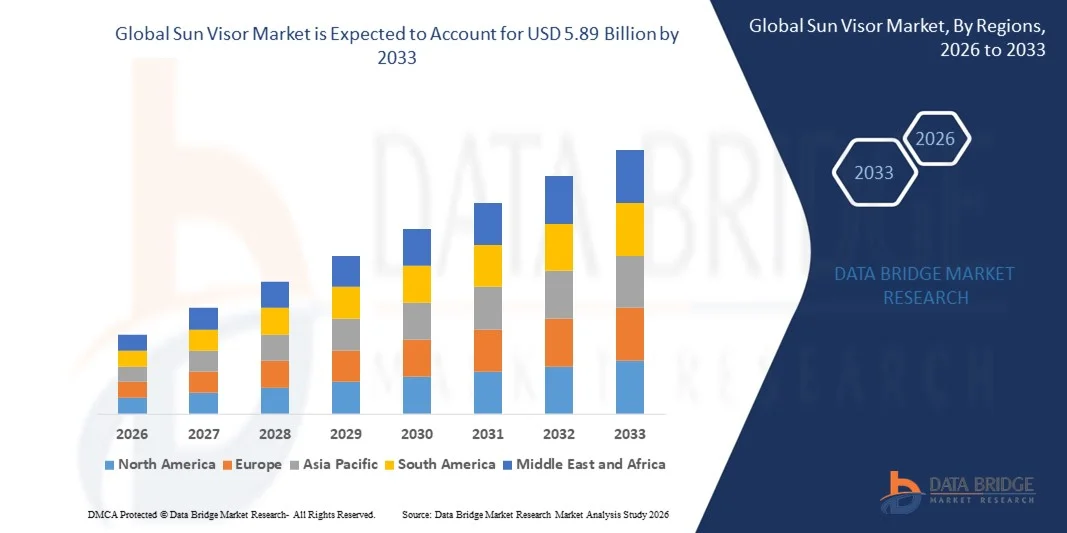

Global Sun Visor Market Size

- The global Sun Visor Market size was valued at USD 3.39 billion in 2025 and is expected to reach USD 5.89 billion by 2033, at a CAGR of 7.13% during the forecast period.

- The market growth is primarily driven by increasing vehicle sales worldwide and rising consumer demand for enhanced in-car comfort, safety, and convenience features, prompting automakers to integrate advanced sun visor solutions in both passenger and commercial vehicles.

- Additionally, technological advancements such as adjustable, illuminated, and smart sun visors, along with rising awareness about driver safety and UV protection, are encouraging adoption across various vehicle segments, thereby significantly propelling the market’s expansion.

Global Sun Visor Market Analysis

- Sun visors, designed to block sunlight and enhance driver comfort and safety, are increasingly essential components of modern vehicles in both passenger and commercial segments due to their ergonomic design, adjustability, and integration with vehicle interiors.

- The rising demand for advanced sun visors is primarily driven by growing vehicle production, increasing focus on driver comfort and safety, and consumer preference for features such as illuminated mirrors, adjustable panels, and smart visors with integrated technology.

- North America dominated the Global Sun Visor Market with the largest revenue share of 34.5% in 2025, characterized by high vehicle ownership rates, strong automotive innovation, and a robust presence of leading OEMs, with the U.S. witnessing significant adoption of premium and technologically advanced sun visors in both new vehicles and aftermarket upgrades.

- Asia-Pacific is expected to be the fastest-growing region in the Global Sun Visor Market during the forecast period due to rapid urbanization, rising disposable incomes, and expanding automotive manufacturing hubs in countries like China and India.

- The fabric segment dominated the market with the largest revenue share of 57.4% in 2025, driven by its lightweight nature, durability, and comfort during prolonged exposure to sunlight.

Report Scope and Global Sun Visor Market Segmentation

|

Attributes |

Sun Visor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Global Sun Visor Market Trends

Enhanced Convenience Through AI and Voice Integration

- A significant and accelerating trend in the global Sun Visor Market is the integration of advanced technologies, including AI-assisted features and voice-controlled vehicle ecosystems such as Amazon Alexa, Google Assistant, and Apple CarPlay. This integration is enhancing driver convenience, safety, and overall in-car experience.

- For instance, smart visors with voice-activated controls allow drivers to adjust visor position, deploy sun shades, or activate built-in lighting without taking their hands off the wheel. Similarly, AI-assisted visors can automatically adjust tint levels based on sunlight intensity and driving conditions.

- AI integration in sun visors enables adaptive functionality, such as learning driver preferences for glare reduction or automatic dimming based on time of day and driving environment. Some advanced models can even detect driver eye strain or fatigue and adjust the visor angle or alert the driver.

- The seamless integration of sun visors with connected car systems and infotainment platforms facilitates centralized control over multiple in-car comfort features. Through a single interface, users can manage visor settings alongside interior lighting, climate control, and navigation, creating a safer and more personalized driving experience.

- This trend toward more intelligent, adaptive, and interconnected vehicle components is fundamentally reshaping user expectations for in-car comfort and safety. Consequently, companies such as Gentex and Magna are developing AI-enabled smart visors with automatic glare reduction, voice command control, and compatibility with major connected car platforms.

- The demand for sun visors that offer seamless AI and voice control integration is growing rapidly across both passenger and commercial vehicle segments, as consumers increasingly prioritize convenience, safety, and a fully connected driving experience.

Global Sun Visor Market Dynamics

Driver

Growing Need Due to Rising Driver Safety Awareness and Vehicle Comfort Expectations

- The increasing focus on driver safety, coupled with rising consumer expectations for enhanced in-car comfort, is a significant driver for the growing demand for advanced sun visors.

- For instance, in 2025, Gentex Corporation introduced a new AI-assisted auto-dimming sun visor with integrated lighting and glare reduction sensors, aiming to improve driver visibility and reduce eye strain. Such innovations by leading companies are expected to drive sun visor market growth during the forecast period.

- As drivers and passengers become more aware of potential hazards from sunlight glare and UV exposure, advanced sun visors offer features such as adjustable panels, illuminated mirrors, and automatic tinting, providing a clear upgrade over traditional fixed visors.

- Furthermore, the increasing integration of sun visors with connected car systems and in-car infotainment platforms is making them a key component of modern vehicle interiors, offering seamless interaction with other comfort and safety features such as climate control, driver-assistance systems, and ambient lighting.

- The convenience of adaptive, AI-assisted visors, automatic glare reduction, and ergonomic designs are key factors propelling adoption across passenger and commercial vehicles. The trend toward premium, user-focused interiors and increasing consumer demand for enhanced driving experiences further supports market growth.

Restraint/Challenge

Concerns Regarding High Costs and Technological Complexity

- The relatively high cost and technological complexity of advanced sun visors pose a significant challenge to broader market adoption. Features such as AI-assisted glare reduction, automatic tinting, and integration with connected car systems increase production costs, which can limit accessibility in price-sensitive segments.

- For instance, luxury vehicles equipped with fully adaptive, AI-enabled visors offer enhanced safety and comfort, but their premium pricing makes them less attainable for mid-range and budget-conscious buyers.

- Addressing these challenges through the development of more affordable, modular, and user-friendly visor solutions is crucial for expanding market penetration. Companies such as Gentex, Magna, and Mobis are focusing on balancing advanced features with cost-effective designs to attract a wider customer base.

- While prices for smart and adaptive visors are gradually decreasing, the perceived premium for technology-driven features can still hinder adoption, particularly among consumers who do not immediately recognize the added safety and comfort benefits.

- Overcoming these challenges through cost optimization, consumer education on the advantages of advanced visors, and gradual introduction of AI and connected features in mid-range vehicles will be vital for sustained growth in the global sun visor market.

Global Sun Visor Market Scope

Sun visor market is segmented on the basis of surface material, type, vehicle type, sales channel, and propulsion.

- By Surface Material

On the basis of surface material, the Global Sun Visor Market is segmented into fabric and vinyl. The fabric segment dominated the market with the largest revenue share of 57.4% in 2025, driven by its lightweight nature, durability, and comfort during prolonged exposure to sunlight. Fabric visors are widely preferred in passenger vehicles due to their aesthetic appeal, resistance to heat, and ability to complement vehicle interiors.

The vinyl segment is expected to witness the fastest CAGR of 19.8% from 2026 to 2033, fueled by its cost-effectiveness, ease of cleaning, and growing adoption in commercial vehicles and trucks. Vinyl visors offer resistance to wear and tear and can endure harsh environmental conditions, making them suitable for fleet and utility vehicles. Rising consumer preference for durable, low-maintenance interior components is accelerating the adoption of vinyl sun visors globally.

- By Type

On the basis of type, the Global Sun Visor Market is segmented into conventional type and LCD sun visors. The conventional segment dominated the market in 2025 with a revenue share of 62.3%, driven by its simplicity, affordability, and widespread compatibility across vehicle types. Conventional visors continue to be the preferred choice in mid-range passenger vehicles and commercial fleets due to their functional design and cost efficiency.

The LCD sun visor segment is expected to witness the fastest CAGR of 21.5% during 2026–2033, fueled by technological advancements in connected cars and increasing demand for integrated infotainment, touch-screen displays, and augmented driver-assist features. LCD visors offer additional functionalities such as navigation display, media controls, and digital rearview enhancements, appealing to luxury and electric vehicle segments. Growing interest in futuristic and multifunctional vehicle interiors is supporting market growth for LCD visors.

- By Vehicle Type

On the basis of vehicle type, the Global Sun Visor Market is segmented into passenger vehicles, trucks, buses, and commercial vehicles. The passenger vehicle segment dominated the market in 2025 with a revenue share of 54.7%, driven by the growing focus on driver comfort, vehicle aesthetics, and rising sales of mid-range and premium cars. Passenger vehicles increasingly feature sun visors with glare reduction, adjustable panels, and integrated lighting to enhance convenience.

The commercial vehicle segment is expected to witness the fastest CAGR of 20.2% from 2026 to 2033, fueled by the expansion of logistics, fleet operations, and public transportation sectors. Drivers of commercial vehicles are increasingly demanding durable, multifunctional visors that improve safety and reduce fatigue during long driving hours. Government regulations and fleet modernization programs further contribute to this growth trend.

- By Sales Channel

On the basis of sales channel, the Global Sun Visor Market is segmented into OEM and aftermarket. The OEM segment dominated the market in 2025 with a revenue share of 68.1%, driven by increasing vehicle production and the trend of installing advanced visors during initial assembly. OEM partnerships with leading automakers allow sun visor manufacturers to integrate features such as AI-assisted glare reduction, lighting, and digital displays directly into new vehicles.

The aftermarket segment is expected to witness the fastest CAGR of 22.0% during 2026–2033, fueled by rising vehicle refurbishment trends, replacement needs, and demand for upgraded or multifunctional visors in older vehicles. Aftermarket adoption is particularly strong among consumers seeking enhanced safety, aesthetic upgrades, and smart visor functionalities without purchasing a new vehicle.

- By Propulsion

On the basis of propulsion, the Global Sun Visor Market is segmented into internal combustion engine (ICE) and electric vehicles (EVs). The ICE segment dominated the market in 2025 with a revenue share of 65.3%, due to the predominance of ICE vehicles globally and the high adoption of standard sun visors in conventional passenger cars and commercial vehicles.

The EV segment is expected to witness the fastest CAGR of 23.1% during 2026–2033, driven by the growing production and sales of electric vehicles, which often integrate smart, multifunctional, and LCD sun visors. EV manufacturers are increasingly incorporating visors with AI-assisted glare reduction, connected car integration, and enhanced driver-assist features to complement high-tech interiors and appeal to tech-savvy consumers. Rising EV adoption in North America, Europe, and Asia-Pacific is fueling this segment’s rapid growth.

Global Sun Visor Market Regional Analysis

- North America dominated the Global Sun Visor Market with the largest revenue share of 34.5% in 2025, driven by increasing demand for enhanced driver safety, in-vehicle comfort, and premium vehicle interiors.

- Consumers in the region highly value advanced features in sun visors, such as glare reduction, adjustable panels, integrated lighting, and multifunctional LCD displays, which improve driving convenience and safety.

- This widespread adoption is further supported by high disposable incomes, a large fleet of passenger and commercial vehicles, and a growing preference for technologically advanced and ergonomically designed vehicle components, establishing premium and multifunctional sun visors as a standard in both personal and commercial vehicles.

U.S. Sun Visor Market Insight

The U.S. sun visor market captured the largest revenue share of 81% in 2025 within North America, driven by increasing demand for vehicle safety, driver comfort, and premium in-car features. Consumers are prioritizing sun visors with advanced functionalities such as glare reduction, integrated lighting, adjustable panels, and multifunctional LCD displays. The growing adoption of high-end vehicles and the trend toward vehicle personalization and enhanced ergonomics further boost the market. Moreover, the integration of sun visors with infotainment systems and smart vehicle technologies is contributing to the market’s expansion.

Europe Sun Visor Market Insight

The Europe sun visor market is projected to grow at a substantial CAGR during the forecast period, primarily fueled by strict automotive safety regulations and increasing demand for premium vehicle interiors. Urbanization, rising disposable incomes, and the popularity of technologically advanced vehicles are fostering adoption. Consumers in Europe are drawn to sun visors offering multifunctional features, ergonomic design, and improved driver comfort. Growth is observed across passenger vehicles, commercial vehicles, and luxury segments, particularly in new vehicle models and retrofitting applications.

U.K. Sun Visor Market Insight

The U.K. sun visor market is anticipated to grow at a notable CAGR over the forecast period, supported by rising awareness of vehicle safety and driver convenience. The demand for sun visors with integrated lighting, anti-glare functions, and advanced material finishes is increasing among both personal and commercial vehicle owners. Additionally, the adoption of connected and smart vehicle technologies in the U.K. supports the integration of multifunctional sun visors in modern vehicles, stimulating market growth.

Germany Sun Visor Market Insight

The Germany sun visor market is expected to expand at a significant CAGR during the forecast period, driven by a strong automotive industry, high consumer preference for premium vehicles, and emphasis on driver safety and comfort. Multifunctional sun visors with LCD displays, adjustable panels, and anti-glare features are gaining popularity, particularly in luxury and commercial vehicles. Germany’s focus on innovation, vehicle ergonomics, and advanced automotive interiors supports the increasing adoption of technologically enhanced sun visors.

Asia-Pacific Sun Visor Market Insight

The Asia-Pacific sun visor market is poised to grow at the fastest CAGR of 24% from 2026 to 2033, fueled by rising vehicle production, urbanization, and increasing disposable incomes in countries such as China, Japan, and India. The growing preference for vehicles with enhanced comfort, safety, and multifunctional features is driving adoption. Government initiatives promoting automotive safety and smart vehicle technologies are supporting market growth. Additionally, as APAC emerges as a manufacturing hub for automotive components, sun visors with advanced materials and integrated technology are becoming more affordable and accessible to a broader consumer base.

Japan Sun Visor Market Insight

The Japan sun visor market is gaining momentum due to high vehicle technology adoption, urbanization, and demand for convenience and driver safety. Japanese consumers increasingly prefer multifunctional sun visors with LCD displays, anti-glare technology, and ergonomic designs. The integration of sun visors with advanced vehicle systems and smart interiors further supports growth. Moreover, Japan’s aging population drives demand for sun visors that enhance visibility, comfort, and ease of use in both personal and commercial vehicles.

China Sun Visor Market Insight

The China sun visor market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid vehicle production, urbanization, and growing consumer preference for technologically advanced vehicles. Multifunctional sun visors with glare reduction, integrated lighting, and LCD displays are becoming increasingly popular across passenger cars, commercial vehicles, and luxury segments. Strong domestic automotive manufacturers, growing adoption of smart vehicle technologies, and affordability of advanced sun visor options are key factors propelling market growth in China.

Global Sun Visor Market Share

The Sun Visor industry is primarily led by well-established companies, including:

• Denso Corporation (Japan)

• Gentex Corporation (U.S.)

• Valeo (France)

• Magna International (Canada)

• Continental AG (Germany)

• Sumitomo Electric Industries (Japan)

• Hyundai Mobis (South Korea)

• Daewoo International (South Korea)

• Stanley Electric Co., Ltd. (Japan)

• Takata Corporation (Japan)

• Samsung SDI (South Korea)

• Aptiv PLC (Ireland)

• Ficosa International (Spain)

• Koito Manufacturing Co., Ltd. (Japan)

• Toyota Boshoku Corporation (Japan)

• Autoliv Inc. (Sweden)

• Magneti Marelli (Italy)

• Ford Motor Company (U.S.)

• Brose Fahrzeugteile GmbH & Co. KG (Germany)

• Bosch Automotive (Germany)

What are the Recent Developments in Global Sun Visor Market?

- In April 2024, Denso Corporation, a global leader in automotive components, launched a strategic initiative in South Africa aimed at enhancing vehicle safety and driver comfort through its advanced sun visor technologies. This initiative emphasizes Denso’s commitment to delivering innovative, ergonomically designed sun visors tailored to the unique needs of both passenger and commercial vehicles in the region. By leveraging its global expertise and cutting-edge product offerings, Denso is strengthening its presence in the rapidly growing global Sun Visor Market.

- In March 2024, Gentex Corporation, a U.S.-based automotive technology company, introduced its next-generation LCD sun visor for premium and commercial vehicles. The visor integrates anti-glare technology, LED lighting, and digital display functionality, offering drivers improved visibility, convenience, and entertainment options. This launch highlights Gentex’s focus on innovation and its dedication to enhancing in-car experiences, reinforcing its position in the competitive sun visor market.

- In March 2024, Valeo successfully deployed an advanced sun visor system in its “Smart Mobility” project in Bengaluru, India. The initiative aims to improve driver safety and comfort in urban traffic conditions by integrating multifunctional sun visors with anti-glare panels, adjustable angles, and integrated lighting. This deployment underscores Valeo’s role in advancing automotive interior technologies and contributes to safer, smarter driving environments.

- In February 2024, Magna International announced a strategic partnership with leading automotive OEMs in North America to supply high-performance sun visors with fabric and vinyl finishes for both passenger and commercial vehicles. This collaboration aims to enhance interior aesthetics, driver ergonomics, and functionality, emphasizing Magna’s commitment to innovation and quality in the sun visor segment of the automotive market.

- In January 2024, Continental AG unveiled its new “VisionGuard” sun visor at the CES 2024 automotive expo, featuring an LCD display, glare reduction, and adaptive lighting for premium vehicles. The launch reflects Continental’s commitment to integrating cutting-edge technology into vehicle interiors, offering drivers enhanced comfort, visibility, and convenience while reinforcing the company’s position in the global Sun Visor Market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.