Global Surface Vision And Inspection Market

Market Size in USD Billion

USD

6.80 Billion

USD

14.70 Billion

2024

2032

USD

6.80 Billion

USD

14.70 Billion

2024

2032

| 2025 - 2032 | |

| USD 6.80 Billion | |

| USD 14.70 Billion | |

| % | |

|

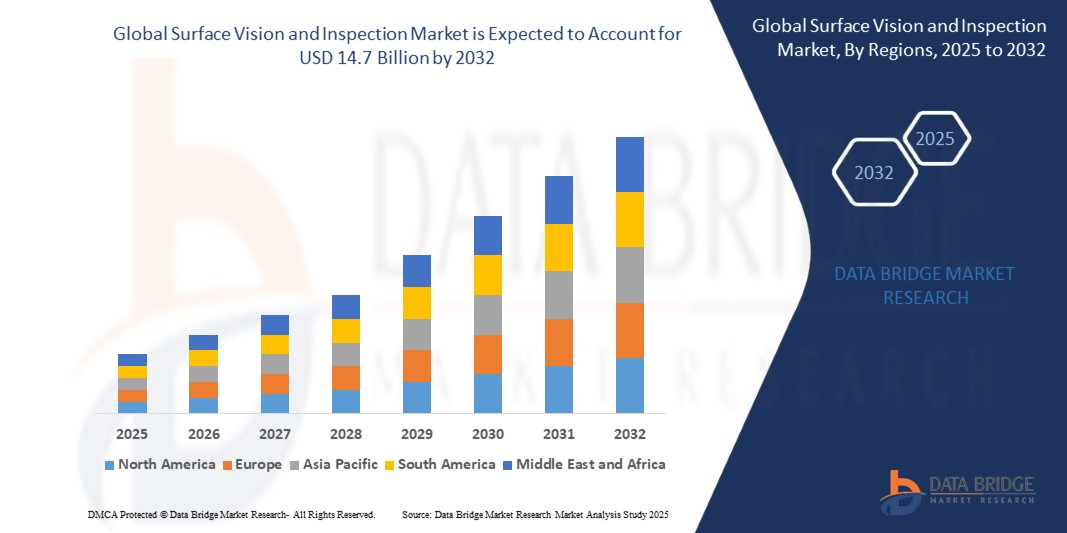

Global Surface Vision and Inspection Market Size

- The global surface vision and inspection market size was valued at USD 6.8 billion in 2024 and is projected to reach USD 14.7 billion by 2032, growing at a CAGR of 11.64% during the forecast period..

- This strong market growth is propelled by the rising adoption of automated quality control systems, growing industrial automation across multiple sectors, and the increasing demand for precision in defect detection and product consistency. The continuous evolution of AI-powered machine vision and advanced 3D inspection technologies is encouraging manufacturers to implement smarter, real-time inspection solutions across production lines, enhancing both operational efficiency and regulatory compliance.

Global Surface Vision and Inspection Market Analysis

- Surface vision and inspection systems are playing an increasingly vital role in modern manufacturing by transforming how quality assurance is handled on production floors. These systems use high-resolution cameras, real-time image processing, and intelligent software to detect surface flaws, dimensional errors, or irregularities—without the need for manual checks. Industries like automotive, electronics, and semiconductors are leading the way, especially with the rising adoption of 3D vision technologies that offer the kind of precision required at microscopic levels.

- The integration of artificial intelligence and deep learning is also making these systems smarter over time, allowing them to learn from data, reduce false alarms, and improve inspection accuracy.

- In regions like Asia-Pacific and Europe, where manufacturing output is high and quality benchmarks are rising, these technologies are also being used for predictive maintenance, process optimization, and guiding robotics—highlighting a broader shift toward automation and efficiency across global factories.

Global Surface Vision and Inspection Market Segmentation

|

Attributes |

Global Surface Vision and Inspection Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

The integration of artificial intelligence and machine learning algorithms in inspection systems is creating powerful, self-optimizing solutions that evolve with each production cycle—enhancing accuracy and operational intelligence..

The push toward smart manufacturing is accelerating demand for integrated vision systems that can interact with industrial robots and MES (Manufacturing Execution Systems), enabling real-time process control.

Innovation in miniaturized, low-cost vision systems is opening up access for small and medium enterprises (SMEs), particularly in developing economies. Plug-and-play cameras and cloud-based analytics tools are reducing barriers to entry

Beyond automotive and electronics, vision systems are finding newer applications in agriculture (e.g., fruit sorting), logistics (e.g., package integrity), and pharmaceuticals (e.g., blister pack verification), creating new growth avenues.

Real-time defect detection reduces material wastage and energy consumption, aligning with global sustainability efforts and encouraging adoption in environmentally-conscious industries . |

|

Value Added Data Infosets |

|

Global Surface Vision and Inspection Market Trends

“Rise of AI-Driven Vision Systems Transforming Industrial Inspection”

- One of the most impactful shifts in the surface vision and inspection market today is the rapid rise of AI-driven vision systems. Traditional inspection tools relied heavily on fixed rules and predefined algorithms, which often struggled with complex or variable product environments. But with artificial intelligence and deep learning entering the scene, vision systems are becoming far more adaptive and intelligent. These next-generation tools are capable of learning from thousands of images, recognizing subtle patterns, and improving their accuracy over time without the need for manual reprogramming.

- In industries like electronics, automotive, and pharmaceuticals—where even the smallest defect can have serious implications—AI-based systems are proving to be game-changers. They can detect defects that are difficult to define or inconsistent in appearance, which older systems might miss or misclassify. What makes these systems stand out is their ability to make decisions in real time, with better precision and fewer false positives, which directly translates into reduced waste, improved product quality, and faster production cycles.

- Moreover, AI-driven vision isn’t just about better inspection—it’s also about enabling smarter manufacturing environments. These systems can now interact with robotics, adjust parameters on the fly, and feed valuable insights back into the production line. As factories continue to embrace Industry 4.0, the role of AI in vision technology is expected to expand even further, shaping a future where machines continuously learn, adapt, and optimize without human intervention.

- One of the biggest advantages of AI-driven vision systems is their consistency. Unlike human inspectors, who can get tired or distracted, these systems maintain the same high level of attention 24/7. This consistency helps companies drastically reduce errors caused by fatigue or subjective judgment. Plus, AI vision systems can handle massive volumes of inspections without slowing down, which is crucial for industries with high-speed production lines.

- Another exciting aspect is how AI vision technology is enabling predictive maintenance and proactive problem-solving. By continuously monitoring products and equipment, these systems can detect subtle changes or early signs of wear and tear. This early warning allows manufacturers to address issues before they cause costly downtime or product recalls. It’s like having a vigilant digital guardian watching over every step of the process, ensuring everything runs smoothly.

Global Surface Vision and Inspection Market Dynamics

Driver

“Growing Demand for Automated Quality Control and Smart Manufacturing”

- The increasing emphasis on product quality, consistency, and traceability is fueling the demand for advanced surface vision and inspection systems. Manufacturers are under pressure to reduce defects, eliminate human error, and meet global quality standards—especially in critical sectors like automotive, electronics, and pharmaceuticals.

- Smart vision systems, empowered by AI and IoT, offer real-time feedback, enable predictive maintenance, and ensure zero-defect manufacturing. As industrial IoT gains momentum, surface inspection technologies are emerging as the central nervous system of intelligent factory floors.

- Rising labor costs and global labor shortages are also compelling industries to invest in automated inspection tools, ensuring high-speed processing with unmatched precision. As a result, machine vision is not just an option—but a competitive necessity.

- Another important factor pushing the adoption of automated surface inspection is the challenge of rising labor costs and global shortages of skilled workers. It’s becoming harder and more expensive to rely on manual inspection for every product, especially as production speeds increase and quality expectations become stricter. Automated machine vision systems offer a solution that combines speed with precision—inspecting thousands of parts quickly without fatigue or inconsistency. For manufacturers, investing in these systems isn’t just about upgrading technology; it’s about staying competitive in a market where flawless quality and fast turnaround times are critical. In this way, machine vision has shifted from a luxury to a necessity for businesses that want to thrive in today’s demanding industrial environment.

Restraint/Challenge

“High Initial Investment and Integration Complexity”

- One of the significant restraints hampering the growth of the global surface vision and inspection market is the high initial cost associated with deploying advanced vision systems. These solutions often require sophisticated hardware components such as high-resolution cameras, sensors, image processors, and custom lighting setups, in addition to complex software frameworks that involve artificial intelligence (AI) and machine learning (ML) algorithms. The upfront capital expenditure for integrating such systems into existing production lines can be substantial, particularly for small and mid-sized enterprises (SMEs) operating on constrained budgets.

- Moreover, the integration of surface inspection technologies into legacy manufacturing environments is technically demanding and time-consuming. Achieving seamless interoperability with existing machinery, ensuring data compatibility with enterprise software systems, and maintaining real-time processing speeds across different production scenarios require highly skilled personnel and expert-level calibration. These complexities can delay deployment timelines and increase total implementation costs, acting as a deterrent for companies that lack the technical capacity or resources to adapt quickly.

- Another challenge lies in the customization and scalability of these systems. Since inspection requirements vary widely across industries—from microelectronics and automotive to pharmaceuticals and packaging—vendors often need to develop tailored solutions, which further escalates costs and prolongs deployment cycles. In addition, the lack of standardized protocols across different platforms and vendors makes system upgrades and multi-line coordination difficult, posing a long-term barrier to wide-scale adoption. As a result, many manufacturers are hesitant to invest heavily in surface vision and inspection systems without clear, short-term ROI assurances.

Global Surface Vision and Inspection Market Scope

The global surface vision and inspection market is segmented based on component, system type, application, and end-user industry.

The global surface vision and inspection market is segmented based on component, system type, application, and end-user industry.

- By component

the market includes hardware, software, and services. Hardware dominates the segment, as high-performance cameras, sensors, lighting systems, and processors are essential for accurate image capture and defect detection. However, the software segment is rapidly gaining traction due to the increasing use of artificial intelligence (AI) and machine learning algorithms that enhance pattern recognition and predictive analytics. Services—such as installation, training, and maintenance—also play a vital role, especially for companies seeking end-to-end solutions

- By system type

The market is categorized into 1D, 2D, and 3D vision systems. 2D systems currently lead the market, thanks to their affordability and suitability for most surface inspection applications. However, 3D systems are witnessing faster growth, particularly in industries where depth, contours, and structural integrity are critical, such as in automotive or aerospace manufacturing.

- By Application

The market covers inspection, measurement, identification, and others. Inspection remains the core application, driven by the need for real-time defect detection and quality control. Measurement applications are also expanding, especially in precision manufacturing where dimensional accuracy is essential. Identification solutions, including barcode reading and part recognition, are increasingly used to enhance traceability across production cycles.

- By end-user industry

The market is segmented into automotive, electronics & semiconductors, pharmaceuticals, food & beverages, packaging, and others. The electronics and semiconductor industry is a major adopter due to its stringent quality requirements and microscopic defect tolerances. Meanwhile, the automotive sector is leveraging vision systems for surface finish inspection, paint quality checks, and component alignment. The pharmaceutical and food industries are embracing these systems to ensure packaging integrity, labeling accuracy, and contamination-free production.

Global Surface Vision and Inspection Market Regional Analysis

North America global surface vision and inspection market insight.

The North America surface vision and inspection market is experiencing steady growth due to strong adoption of automation in manufacturing and the presence of leading technology providers. The U.S. continues to dominate regional demand, supported by advancements in AI-powered inspection tools and increased implementation across automotive, electronics, and pharmaceutical sectors. Companies are investing in upgrading their quality assurance processes, especially in high-precision manufacturing, while regulatory compliance further drives demand in sectors like food and pharma.

Europe global surface vision and inspection market insight

Europe remains a key player in the global surface vision and inspection market, with countries like Germany, the U.K., and France leading technological innovation. The region benefits from a well-established automotive and industrial manufacturing base, where precision and quality control are critical. EU regulations on product safety and traceability are pushing companies to integrate advanced inspection systems. Additionally, Industry 4.0 initiatives and growing demand for smart factories are accelerating the adoption of surface vision solutions across sectors.

Asia-pacific global surface vision and inspection market insight

Asia-Pacific is projected to witness the fastest growth in the surface vision and inspection market, driven by rapid industrialization, large-scale manufacturing, and strong demand for consumer electronics. Countries like China, Japan, South Korea, and India are investing heavily in automation and smart production systems. Electronics and automotive sectors are at the forefront of this transformation, using vision technologies to improve quality, reduce waste, and meet global export standards. Increasing labor costs are also encouraging companies to shift from manual inspection to automated solutions.

Middle east and Africa global surface vision and inspection market insight

The surface vision and inspection market in the Middle East and Africa is still emerging but shows promising growth potential. The focus is primarily on industrial automation and enhancing quality control in packaging, food processing, and pharmaceuticals. As industries in countries like the UAE and Saudi Arabia modernize their manufacturing ecosystems, there is a growing interest in smart vision systems. The gradual shift toward regulatory compliance and investment in non-oil industries are expected to open new opportunities in the region.

South America global surface vision and inspection market insight

South America is witnessing growing adoption of surface vision systems, particularly in Brazil and Argentina, where industrial activity is on the rise. The automotive and food processing industries are key drivers, seeking greater efficiency and accuracy in production. Although challenges like high equipment costs and limited awareness persist, increased focus on quality assurance and export readiness is encouraging gradual adoption. As automation gains momentum, the demand for inspection technologies is likely to strengthen across the region.

Global Surface Vision and Inspection Market Share

The global surface vision and inspection market is moderately fragmented, with several key players competing on technological innovation, solution customization, and global reach. Leading companies are investing heavily in R&D to develop smarter, faster, and more accurate inspection systems that can handle a wider range of surfaces and materials across various industries. Companies like Cognex Corporation, Keyence Corporation, Teledyne Technologies, Basler AG, and Omron Corporation hold a significant portion of the market share due to their strong product portfolios and established presence in both developed and emerging economies.

In recent years, competition has intensified with the entry of new players offering AI-based vision solutions at more accessible price points. These entrants are particularly targeting small and mid-sized manufacturers looking to upgrade their inspection processes without the burden of high capital costs. Meanwhile, established firms are expanding their market share through strategic acquisitions, global partnerships, and by integrating AI and deep learning capabilities into their existing platforms to meet evolving industry needs.

Regional market share distribution also varies significantly. Asia-Pacific leads in terms of adoption, thanks to the rapid growth of manufacturing hubs in countries like China, Japan, South Korea, and India. North America and Europe follow closely, driven by stringent regulatory standards, high automation levels, and advanced production facilities across sectors such as automotive, electronics, and pharmaceuticals. As global manufacturers continue to prioritize quality and process optimization, the surface vision and inspection market is expected to witness healthy competition and steady growth in its global market share

The following companies are recognized as major players in the Global Surface Vision and Inspection market:

- KEYENCE Corporation (Japan)

- Cognex Corporation (US)

- OMRON Corporation (Japan)

- ISRA VISION (Germany)

- Panasonic Corporation (Japan)

Latest Developments in Global Surface Vision and Inspection Market

- In May 2025, Cognex Corporation announced the launch of its next-generation In-Sight 9902L vision system, equipped with ultra-high-resolution line scan technology and advanced AI-powered defect classification. The system is designed to deliver enhanced performance in complex inspection environments such as printed circuit boards and metal surfaces.

- In April 2025, Keyence Corporation expanded its surface inspection portfolio with the introduction of the LJ-X8000 Series, a high-speed 3D laser displacement sensor that enables micron-level surface analysis in real-time. This solution targets high-precision industries such as automotive, electronics, and medical devices.

- In March 2025, Teledyne DALSA introduced a new high-speed CMOS line scan camera Linea2 tailored for surface inspection in web materials, textiles, and semiconductor wafers. The camera offers improved sensitivity and supports multi-line configurations, helping manufacturers reduce false defect rates and improve inspection accuracy.

- In February 2025, Basler AG unveiled its AI Vision Suite 3.0, combining deep learning-based surface inspection with edge computing capabilities. The suite supports smart integration into existing production lines and enables real-time decision-making for dynamic quality control applications.

- In January 2025, ISRA VISION, a subsidiary of Atlas Copco, launched an automated surface inspection solution for electric vehicle battery components. The new system aims to optimize the production of battery cells by detecting micro-defects in electrode coatings and separator films, improving safety and overall battery efficiency.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL SURFACE VISION AND INSPECTION MARKET

1.4 CURRENCY AND PRICING

1.5 IMPACT OF COVID-19 PANDEMIC ON THE MARKET

1.5.1 PRICE IMPACT

1.5.2 IMPACT ON DEMAND

1.5.3 IMPACT ON SUPPLY CHAIN

1.5.4 CONCLUSION

1.6 LIMITATION

1.7 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 KEY TAKEAWAYS

2.2 ARRIVING AT THE GLOBAL SURFACE VISION AND INSPECTION MARKET

2.2.1 VENDOR POSITIONING GRID

2.2.2 TECHNOLOGY LIFE LINE CURVE

2.2.3 MARKET GUIDE

2.2.4 COMPANY POSITIONING GRID

2.2.5 COMAPANY MARKET SHARE ANALYSIS

2.2.6 MULTIVARIATE MODELLING

2.2.7 TOP TO BOTTOM ANALYSIS

2.2.8 STANDARDS OF MEASUREMENT

2.2.9 VENDOR SHARE ANALYSIS

2.2.10 DATA POINTS FROM KEY PRIMARY INTERVIEWS

2.2.11 DATA POINTS FROM KEY SECONDARY DATABASES

2.3 GLOBAL SURFACE VISION AND INSPECTION MARKET: RESEARCH SNAPSHOT

2.4 ASSUMPTIONS

3 MARKET OVERVIEW AND INDUSTRY TRENDS

3.1 DRIVERS

3.2 RESTRAINTS

3.3 OPPORTUNITIES

3.4 CHALLENGES

4 EXECUTIVE SUMMARY

5 PREMIUM INSIGHTS

5.1 DEFECTS RECOVERED BY SURFACE VISION AND INSPECTION

5.1.1 FINISH

5.1.2 JOINTS

5.1.3 CRACKS

5.1.4 WEAR

5.1.5 HOLES

5.1.6 SCRATCHES

5.1.7 OTHERS

6 IMPACT OF COVID-19 PANDEMIC ON THE MARKET

6.1 ANALYSIS ON IMPACT OF COVID-19 ON THE MARKET

6.2 AFTER MATH OF COVID-19 AND GOVERNMENT INITIATIVE TO BOOST THE MARKET

6.3 STRATEGIC DECISIONS FOR MANUFACTURERS AFTER COVID-19 TO GAIN COMPETITIVE MARKET SHARE

6.4 PRICE IMPACT/PRICING ANALYSIS

6.5 IMPACT ON DEMAND

6.6 IMPACT ON SUPPLY CHAIN

6.7 CONCLUSION

7 GLOBAL SURFACE VISION AND INSPECTION MARKET, BY TYPE

7.1 OVERVIEW

7.2 COMPUTER SYSTEM

7.3 CAMERA SYSTEM

8 GLOBAL SURFACE VISION AND INSPECTION MARKET, BY SURFACE TYPE

8.1 OVERVIEW

8.2 2D

8.3 3D

8.4 OTHERS

9 GLOBAL SURFACE VISION AND INSPECTION MARKET, BY FUNCTIONALITY

9.1 OVERVIEW

9.2 WEB INSPECTION

9.2.1 NARROW WEB

9.2.2 BROAD WEB

9.3 SURFACE DEFECTS

9.4 SURFACE INSPECTION

9.4.1 PAINTED SURFACE

9.4.2 COATED SURFACE

9.5 OTHERS

10 GLOBAL SURFACE VISION AND INSPECTION MARKET, BY COMPONENT

10.1 OVERVIEW

10.2 SOFTWARE

10.2.1 INTEGRATED

10.2.2 STANDALONE

10.3 HARDWARE

10.3.1 CAMERAS

10.3.1.1. SENSING TECHNOLOGY

10.3.1.2. IMAGING TECHNOLOGY

10.3.1.3. INTERFACE STANDARDS

10.3.1.4. FRAME RATES

10.3.1.5. FORMAT

10.3.2 OPTICS

10.3.3 LIGHTING EQUIPMENT

10.3.4 FRAME GRABBER

10.3.5 PROCESSORS

11 GLOBAL SURFACE VISION AND INSPECTION MARKET, BY DEPLOYMENT TYPE

11.1 OVERVIEW

11.2 TRADITIONAL

11.3 ROBOTIC CELL BASED

12 GLOBAL SURFACE VISION AND INSPECTION MARKET, BY INDUSTRY

12.1 OVERVIEW

12.2 HEALTHCARE

12.2.1 VIAL INSPECTION

12.2.2 TRANSDERMAL PATCHES INSPECTION

12.2.3 BLISTER PACK INSPECTION

12.2.4 INSULIN PEN INSPECTION

12.3 PRINTING

12.4 PLASTIC & RUBBER

12.5 AUTOMOTIVE

12.5.1 ASSEMBLY VERIFICATION

12.5.2 PAINTED SURFACE INSPECTION

12.5.3 WELD & BRAZED SEAMS INSPECTION

12.5.4 CFRP & GFRP CAR MATS INSPECTION

12.5.5 FLAW DETECTION

12.5.6 OTHERS

12.6 FOOD & BEVERAGES

12.6.1 GRADING

12.6.2 LABEL VALIDATION

12.6.3 QUALITY ASSURANCE

12.6.4 INSPECTION

12.6.4.1. GLASS CONTAINER

12.6.4.2. PLASTIC BOTTLES

12.6.4.3. METAL CONTAINERS

12.6.5 OTHERS

12.7 SEMICONDUCTOR

12.7.1 IR VISION-BASED INSPECTION

12.7.2 ROBOT VISION-BASED INSPECTION

12.7.3 PCB INSPECTION

12.7.4 MACRO-DEFECT INSPECTION

12.7.5 SEMICONDUCTOR FABRICATION INSPECTION

12.8 ELECTRICAL & ELECTRONICS

12.9 GLASS & METAL

12.9.1 CUT PLATE INSPECTION

12.9.2 STRUCTURED SOLAR GLASS INSPECTION

12.9.3 FLOAT GLASS INSPECTION

12.9.4 COATED GLASS INSPECTION

12.9.5 MIRRORED GLASS INSPECTION

12.9.6 LAMINATED GLASS INSPECTION

12.9.7 OTHERS

12.1 PAPER & WOOD

12.11 POSTAL & LOGISTICS

12.12 OTHERS

13 GLOBAL SURFACE VISION AND INSPECTION MARKET, BY GEOGRAPHY

GLOBAL SURFACE VISION AND INSPECTION MARKET, (ALL SEGMENTATION PROVIDED ABOVE IS REPRESENTED IN THIS CHAPTER BY COUNTRY)

13.1.1 NORTH AMERICA

13.1.1.1. U.S.

13.1.1.2. CANADA

13.1.1.3. MEXICO

13.1.2 EUROPE

13.1.2.1. GERMANY

13.1.2.2. FRANCE

13.1.2.3. U.K.

13.1.2.4. ITALY

13.1.2.5. SPAIN

13.1.2.6. RUSSIA

13.1.2.7. TURKEY

13.1.2.8. BELGIUM

13.1.2.9. NETHERLANDS

13.1.2.10. SWITZERLAND

13.1.2.11. REST OF EUROPE

13.1.3 ASIA PACIFIC

13.1.3.1. JAPAN

13.1.3.2. CHINA

13.1.3.3. SOUTH KOREA

13.1.3.4. INDIA

13.1.3.5. AUSTRALIA

13.1.3.6. SINGAPORE

13.1.3.7. THAILAND

13.1.3.8. MALAYSIA

13.1.3.9. INDONESIA

13.1.3.10. PHILIPPINES

13.1.3.11. REST OF ASIA PACIFIC

13.1.4 SOUTH AMERICA

13.1.4.1. BRAZIL

13.1.4.2. ARGENTINA

13.1.4.3. REST OF SOUTH AMERICA

13.1.5 MIDDLE EAST AND AFRICA

13.1.5.1. SOUTH AFRICA

13.1.5.2. EGYPT

13.1.5.3. SAUDI ARABIA

13.1.5.4. U.A.E

13.1.5.5. ISRAEL

13.1.5.6. REST OF MIDDLE EAST AND AFRICA

13.2 KEY PRIMARY INSIGHTS: BY MAJOR COUNTRIES

14 GLOBAL SURFACE VISION AND INSPECTION MARKET,COMPANY LANDSCAPE

14.1 COMPANY SHARE ANALYSIS: GLOBAL

14.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

14.3 COMPANY SHARE ANALYSIS: EUROPE

14.4 COMPANY SHARE ANALYSIS: ASIA PACIFIC

14.5 MERGERS & ACQUISITIONS

14.6 NEW PRODUCT DEVELOPMENT AND APPROVALS

14.7 EXPANSIONS

14.8 REGULATORY CHANGES

14.9 PARTNERSHIP AND OTHER STRATEGIC DEVELOPMENTS

15 GLOBAL SURFACE VISION AND INSPECTION MARKET , SWOT & DBMR ANALYSIS

16 GLOBAL SURFACE VISION AND INSPECTION MARKET, COMPANY PROFILE

16.1 BAUMER INSPECTION

16.1.1 COMPANY SNAPSHOT

16.1.2 REVENUE ANALYSIS

16.1.3 GEOGRAPHIC PRESENCE

16.1.4 PRODUCT PORTFOLIO

16.1.5 RECENT DEVELOPMENTS

16.2 ADEPT TECHNOLOGY, INC

16.2.1 COMPANY SNAPSHOT

16.2.2 REVENUE ANALYSIS

16.2.3 GEOGRAPHIC PRESENCE

16.2.4 PRODUCT PORTFOLIO

16.2.5 RECENT DEVELOPMENTS

16.3 NATIONAL INSTRUMENTS

16.3.1 COMPANY SNAPSHOT

16.3.2 REVENUE ANALYSIS

16.3.3 GEOGRAPHIC PRESENCE

16.3.4 PRODUCT PORTFOLIO

16.3.5 RECENT DEVELOPMENTS

16.4 PERCEPTRON INC

16.4.1 COMPANY SNAPSHOT

16.4.2 REVENUE ANALYSIS

16.4.3 GEOGRAPHIC PRESENCE

16.4.4 PRODUCT PORTFOLIO

16.4.5 RECENT DEVELOPMENTS

16.5 COGNEX CORPORATION

16.5.1 COMPANY SNAPSHOT

16.5.2 REVENUE ANALYSIS

16.5.3 GEOGRAPHIC PRESENCE

16.5.4 PRODUCT PORTFOLIO

16.5.5 RECENT DEVELOPMENTS

16.6 SHELTON VISION

16.6.1 COMPANY SNAPSHOT

16.6.2 REVENUE ANALYSIS

16.6.3 GEOGRAPHIC PRESENCE

16.6.4 PRODUCT PORTFOLIO

16.6.5 RECENT DEVELOPMENTS

16.7 ISRA VISION AG

16.7.1 COMPANY SNAPSHOT

16.7.2 REVENUE ANALYSIS

16.7.3 GEOGRAPHIC PRESENCE

16.7.4 PRODUCT PORTFOLIO

16.7.5 RECENT DEVELOPMENTS

16.8 VITRONIC GMBH

16.8.1 COMPANY SNAPSHOT

16.8.2 REVENUE ANALYSIS

16.8.3 GEOGRAPHIC PRESENCE

16.8.4 PRODUCT PORTFOLIO

16.8.5 RECENT DEVELOPMENTS

16.9 TELEDYNE DALSA INC

16.9.1 COMPANY SNAPSHOT

16.9.2 REVENUE ANALYSIS

16.9.3 GEOGRAPHIC PRESENCE

16.9.4 PRODUCT PORTFOLIO

16.9.5 RECENT DEVELOPMENT

16.1 MATROX IMAGING

16.10.1 COMPANY SNAPSHOT

16.10.2 REVENUE ANALYSIS

16.10.3 GEOGRAPHIC PRESENCE

16.10.4 PRODUCT PORTFOLIO

16.10.5 RECENT DEVELOPMENTS

16.11 MICROSCAN SYSTEMS INC

16.11.1 COMPANY SNAPSHOT

16.11.2 REVENUE ANALYSIS

16.11.3 GEOGRAPHIC PRESENCE

16.11.4 PRODUCT PORTFOLIO

16.11.5 RECENT DEVELOPMENTS

16.12 OMRON CORPORATION (ACQUIRED BY NIDEC)

16.12.1 COMPANY SNAPSHOT

16.12.2 REVENUE ANALYSIS

16.12.3 GEOGRAPHIC PRESENCE

16.12.4 PRODUCT PORTFOLIO

16.12.5 RECENT DEVELOPMENTS

16.13 PANASONIC CORPORATION

16.13.1 COMPANY SNAPSHOT

16.13.2 REVENUE ANALYSIS

16.13.3 GEOGRAPHIC PRESENCE

16.13.4 PRODUCT PORTFOLIO

16.13.5 RECENT DEVELOPMENTS

16.14 KEYENCE CORPORATION

16.14.1 COMPANY SNAPSHOT

16.14.2 REVENUE ANALYSIS

16.14.3 GEOGRAPHIC PRESENCE

16.14.4 PRODUCT PORTFOLIO

16.14.5 RECENT DEVELOPMENTS

16.15 ALLIED VISION TECHNOLOGIES GMBH

16.15.1 COMPANY SNAPSHOT

16.15.2 REVENUE ANALYSIS

16.15.3 GEOGRAPHIC PRESENCE

16.15.4 PRODUCT PORTFOLIO

16.16 DATALOGIC S.P.A.

16.16.1 COMPANY SNAPSHOT

16.16.2 REVENUE ANALYSIS

16.16.3 GEOGRAPHIC PRESENCE

16.16.4 PRODUCT PORTFOLIO

16.16.5 RECENT DEVELOPMENTS

16.17 AMETEK SURFACE VISION

16.17.1 COMPANY SNAPSHOT

16.17.2 REVENUE ANALYSIS

16.17.3 GEOGRAPHIC PRESENCE

16.17.4 PRODUCT PORTFOLIO

16.18 TOSHIBA TELI CORPORATION

16.18.1 COMPANY SNAPSHOT

16.18.2 REVENUE ANALYSIS

16.18.3 GEOGRAPHIC PRESENCE

16.18.4 PRODUCT PORTFOLIO

16.19 RADIANT VISION SYSTEM

16.19.1 COMPANY SNAPSHOT

16.19.2 REVENUE ANALYSIS

16.19.3 GEOGRAPHIC PRESENCE

16.19.4 PRODUCT PORTFOLIO

16.2 QVISION

16.20.1 COMPANY SNAPSHOT

16.20.2 REVENUE ANALYSIS

16.20.3 GEOGRAPHIC PRESENCE

16.20.4 PRODUCT PORTFOLIO

16.21 DARK FIELD TECHNOLOGIES

16.21.1 COMPANY SNAPSHOT

16.21.2 REVENUE ANALYSIS

16.21.3 GEOGRAPHIC PRESENCE

16.21.4 PRODUCT PORTFOLIO

NOTE: THE COMPANIES PROFILED IS NOT EXHAUSTIVE LIST AND IS AS PER OUR PREVIOUS CLIENT REQUIREMENT. WE PROFILE MORE THAN 100 COMPANIES IN OUR STUDY AND HENCE THE LIST OF COMPANIES CAN BE MODIFIED OR REPLACED ON REQUEST

17 CONCLUSION

18 RELATED REPORTS

19 ABOUT DATA BRIDGE MARKET RESEARCH

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.