Global Surgery Pouch Market

Market Size in USD Billion

USD

1.91 Billion

USD

3.53 Billion

2025

2033

USD

1.91 Billion

USD

3.53 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.91 Billion | |

| USD 3.53 Billion | |

| % | |

|

Surgery Pouch Market Overview

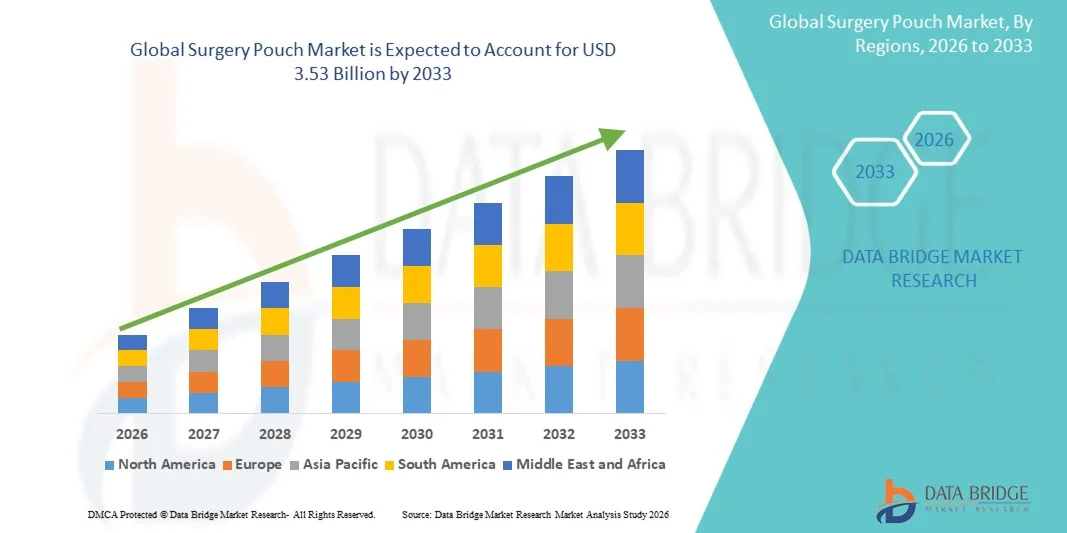

The Surgery Pouch Market was valued at USD 1.91 billion in 2025 and is projected to reach USD 3.53 billion by 2033, growing at a CAGR of 7.99% from 2026 to 2033. The Surgery Pouch Market is experiencing steady growth driven by rising demand for minimally invasive and laparoscopic surgical procedures, increasing prevalence of chronic diseases requiring surgical intervention, and continuous advancements in surgical consumables and medical device technologies. Growing adoption of single-use and sterile surgical pouches across hospitals and ambulatory surgical centers is further supporting market expansion.

The increasing number of surgical procedures globally, combined with stringent infection control regulations and hospital-acquired infection (HAI) prevention standards, is compelling healthcare providers, surgical centers, and medical device manufacturers to adopt advanced surgical pouch solutions. High-barrier, sterilizable, and single-use surgery pouches are increasingly replacing conventional reusable containment methods in many healthcare settings, offering improved safety, reduced contamination risk, and enhanced operational efficiency during surgical procedures.

Key Market Trends & Insights

- North America dominated the Surgery Pouch Market with the largest revenue share of 38.62% in 2025, supported by advanced healthcare infrastructure, strong presence of leading medical device manufacturers, and high adoption of minimally invasive and bariatric surgical procedures. The region also benefits from well-established hospital networks, favorable reimbursement policies, and increasing prevalence of chronic diseases such as obesity, colorectal disorders, Crohn’s disease, and ulcerative colitis, which are driving surgical pouch procedures across the U.S. and Canada.

- The J-Pouch segment dominated the market with a 58.91% share in 2025, driven by its strong clinical preference in restorative proctocolectomy procedures, high success rates in ulcerative colitis treatment, and improved post-surgical bowel function outcomes

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by rising healthcare expenditure, expanding access to advanced gastrointestinal surgical procedures, and increasing awareness of treatment options for inflammatory bowel diseases. Rapid growth in hospital infrastructure across China, India, and Japan, along with improving insurance coverage and expanding presence of global medical device companies, is accelerating adoption of surgery pouch procedures in the region.

- The K-Pouch segment is expected to register the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by its suitability for patients requiring continent ileostomy and those seeking alternatives to external ostomy bags. Advances in surgical techniques and increasing preference for improved patient quality of life are supporting adoption, particularly in specialized colorectal surgery centers.

- The Ulcerative Colitis segment dominates the therapeutic area category with a 44.91% revenue share in 2025, driven by rising global prevalence of inflammatory bowel disease and increasing number of colectomy procedures requiring pouch reconstruction. Growing awareness of early diagnosis, improved biologic treatment failure rates, and higher surgical intervention rates in refractory cases are reinforcing segment leadership.

- The Direct Tender segment accounts for 52.34% of the market in 2025, supported by bulk procurement by hospitals, government healthcare systems, and large surgical centers. Strong institutional purchasing agreements, cost advantages, and long-term supply contracts with medical device manufacturers are key factors driving dominance of this distribution channel.

- The Hospitals segment dominates the end-user category with a 57.18% revenue share in 2025, owing to high patient inflow for gastrointestinal surgeries, availability of advanced surgical infrastructure, and presence of specialized colorectal surgeons. Increasing hospital investments in minimally invasive surgical capabilities and post-operative care units continues to strengthen this segment’s leadership position.

Market Size & Forecast

- Global Market Value (2025): USD 1.91 Billion

- Expected Market Value (2033): USD 3.53 Billion

- Forecast CAGR (2026–2033): 7.99%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Surgery Pouch Market Segmentation

|

Attributes |

Surgery Pouch Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Medtronic plc (Ireland) |

|

Market Opportunities |

· Expansion of minimally invasive and restorative colorectal surgeries · Rising adoption in emerging healthcare markets · Technological advancements in surgical materials and postoperative care |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Surgery Pouch Market Trends

Trend: Growth in Advanced Surgical Reconstruction & Rising IBD Burden

The Surgery Pouch Market is witnessing strong growth driven by the increasing prevalence of inflammatory bowel diseases (IBD), particularly ulcerative colitis and familial adenomatous polyposis (FAP), which are major indications for pouch-based reconstructive surgeries. For instance, clinical reports from 2023–2025 indicate a steady rise in colectomy procedures across the U.S., Germany, and Japan, where surgical pouch reconstruction is increasingly preferred over permanent ileostomy due to improved quality of life outcomes. Hospitals and specialty colorectal centers are increasingly adopting advanced J-pouch reconstruction techniques supported by minimally invasive laparoscopic and robotic-assisted surgeries, improving recovery time and reducing post-operative complications.

Surgery Pouch Market Dynamics

Key Market Driver: Rising Demand for Restorative Colorectal Surgical Procedures

The increasing global burden of gastrointestinal disorders, including a rising incidence of ulcerative colitis (estimated at over 5–10 million cases globally) and Crohn’s disease, is a major driver of the Surgery Pouch market. Surgery pouch procedures, particularly ileal pouch-anal anastomosis (IPAA), are widely adopted when medical therapy fails or complications arise. For example, between 2022 and 2024, major tertiary care hospitals in North America and Europe reported increased utilization of J-pouch surgeries due to improved surgical outcomes and enhanced post-operative bowel function. In addition, advancements in surgical stapling technologies and perioperative care protocols such as Enhanced Recovery After Surgery (ERAS) programs have significantly improved patient recovery rates, further accelerating adoption across high-volume surgical centers.

Key Restraint/Challenge: Surgical Complexity and Post-Operative Complications

A key challenge in the Surgery Pouch market is the complexity associated with pouch reconstruction procedures and the risk of post-operative complications such as pouchitis, bowel obstruction, and leakage. These procedures require highly skilled colorectal surgeons and advanced hospital infrastructure, limiting adoption in smaller healthcare facilities and emerging markets. For instance, clinical studies between 2022 and 2024 have reported pouchitis incidence rates ranging from 20% to 50% in long-term follow-up patients, highlighting the need for continuous medical management and monitoring. In addition, high surgical costs, prolonged hospital stays, and requirement for specialized post-operative care can restrict access in cost-sensitive regions, particularly in parts of Asia-Pacific and Latin America.

Key Market Opportunity: Expansion of Minimally Invasive and Robotics-Assisted Colorectal Surgery

The increasing adoption of minimally invasive and robotic-assisted surgical systems presents a significant opportunity for the Surgery Pouch market. Robotic platforms such as those increasingly used in colorectal surgery enable greater precision, reduced blood loss, and improved surgical accuracy in complex pouch reconstruction procedures. For example, between 2023 and 2025, hospitals in the U.S., South Korea, and Germany expanded robotic colorectal surgery programs, improving patient outcomes and reducing recovery times by several days compared to open surgery. In addition, growing investments in surgical training programs, simulation-based surgical education, and AI-assisted operative planning are further enhancing procedural success rates. The expansion of advanced colorectal surgery infrastructure in emerging markets such as India and China is expected to further broaden access to pouch reconstruction procedures globally.

Surgery Pouch Market Scope

The Surgery Pouch market is segmented on the basis of type of pouch, shape, distribution channel, therapeutic area, and end user.

- By Type of Pouch

On the basis of type of pouch, the Surgery Pouch Market is segmented into J-Pouch and K-Pouch. The J-Pouch segment dominated the market with a 58.91% share in 2025, driven by its strong clinical preference in restorative proctocolectomy procedures, high success rates in ulcerative colitis treatment, and improved post-surgical bowel function outcomes. It is widely adopted due to standardized surgical techniques, lower complication rates, and strong long-term patient recovery performance. Increasing number of colorectal surgeries and rising awareness of minimally invasive reconstructive procedures are further supporting demand. In addition, strong surgeon familiarity and established clinical guidelines continue to reinforce its dominant position across hospitals and specialty surgical centers globally.

The K-Pouch segment is expected to witness the fastest growth with a CAGR of 6.9% from 2026 to 2033, driven by increasing demand for continent ileostomy solutions in patients not suitable for J-Pouch procedures. It provides better quality-of-life outcomes for selected patient groups requiring alternative reconstructive options. Growing adoption in complex colorectal surgeries and revision cases is further accelerating demand. In addition, advancements in surgical techniques, improving clinical expertise, and rising awareness among surgeons regarding alternative pouch reconstruction methods are supporting segment expansion globally.

- By Shape

On the basis of shape, the Surgery Pouch Market is segmented into J, S, and W pouch configurations. The J-shaped pouch segment dominated the market with a 52.47% share in 2025, driven by its widespread use in standard colorectal reconstruction surgeries and proven long-term functional outcomes. It offers ease of construction, predictable performance, and reduced post-operative complications, making it the most preferred choice among surgeons. High adoption in ileal pouch-anal anastomosis (IPAA) procedures and strong clinical guidelines further reinforce its dominance. In addition, increasing volume of colectomy procedures globally continues to support steady market demand.

The S-shaped pouch segment is expected to witness the fastest growth with a CAGR of 6.6% from 2026 to 2033, driven by its suitability in specialized reconstructive procedures requiring higher reservoir capacity and customized surgical approaches. It is increasingly used in complex cases where standard pouch designs are less effective. Advancements in surgical reconstruction techniques and improved post-operative management are supporting adoption. Furthermore, growing clinical research into alternative pouch designs and rising surgeon preference for flexible reconstruction options are accelerating segment growth.

- By Distribution Channel

On the basis of distribution channel, the Surgery Pouch Market is segmented into direct tender, retail sales, and others. The Direct Tender segment dominated the market with a 61.38% share in 2025, driven by bulk procurement by hospitals, government healthcare systems, and large surgical institutions. It ensures cost efficiency, streamlined procurement processes, and long-term supply agreements with manufacturers. High patient inflow in tertiary care hospitals and increasing surgical procedures further strengthen demand. In addition, structured healthcare procurement systems and strong institutional purchasing frameworks continue to reinforce segment dominance.

The Retail Sales segment is expected to witness the fastest growth with a CAGR of 6.5% from 2026 to 2033, driven by expanding access to surgical products through distributors and private healthcare providers. Growth in small and mid-sized healthcare facilities and increasing penetration in emerging markets are supporting expansion. Improved supply chain networks and better product availability are further enhancing adoption. In addition, rising demand for accessible surgical devices and expansion of private surgical centers are accelerating segment growth.

- By Therapeutic Area

On the basis of therapeutic area, the Surgery Pouch Market is segmented into ulcerative colitis, Crohn’s disease, familial adenomatous polyposis (FAP), and others. The Ulcerative Colitis segment dominated the market with a 46.82% share in 2025, driven by high disease prevalence and strong dependence on surgical intervention in severe and refractory cases. Increasing adoption of ileal pouch procedures and strong clinical success outcomes further support dominance. Established treatment guidelines and rising awareness of surgical management options are reinforcing segment growth. In addition, increasing hospitalization rates for chronic inflammatory bowel diseases continue to support market expansion.

The Crohn’s Disease segment is expected to witness the fastest growth with a CAGR of 7.1% from 2026 to 2033, driven by rising global incidence and increasing requirement for surgical intervention in advanced disease stages. Improved surgical techniques and better post-operative care are supporting adoption. Growing awareness among patients and healthcare professionals regarding surgical options is further boosting demand. In addition, advancements in minimally invasive procedures and improved disease management strategies are accelerating segment growth globally.

- By End User

On the basis of end user, the Surgery Pouch Market is segmented into hospitals, ambulatory surgical centers, speciality clinics, and others. The Hospitals segment dominated the market with a 64.27% share in 2025, driven by availability of advanced surgical infrastructure, high patient inflow, and presence of skilled colorectal surgeons. Hospitals remain the primary centers for complex pouch reconstruction surgeries and post-operative care. Increasing adoption of advanced surgical technologies and strong clinical expertise further support dominance. In addition, high volume of inpatient surgical procedures reinforces market leadership.

The Ambulatory Surgical Centers segment is expected to witness the fastest growth with a CAGR of 6.7% from 2026 to 2033, driven by increasing shift toward outpatient surgical procedures and cost-efficient treatment settings. Rising adoption of minimally invasive surgeries and faster recovery protocols are supporting demand. Expansion of healthcare infrastructure and growing preference for reduced hospital stays are further accelerating growth. In addition, increasing patient inclination toward convenient surgical care models is driving segment expansion globally.

Surgery Pouch Market Regional Analysis

North America dominated the Surgery Pouch market and accounted for the largest revenue share of 38.62% in 2025, supported by advanced healthcare infrastructure, strong presence of leading medical device manufacturers, and high adoption of minimally invasive and bariatric surgical procedures. The region benefits from well-established hospital networks, favorable reimbursement policies, and high procedural volumes across colorectal surgeries. Increasing prevalence of chronic diseases such as obesity, Crohn’s disease, ulcerative colitis, and other colorectal disorders is further driving demand for surgery pouch procedures. Continuous technological advancements in surgical techniques and strong clinical expertise across the U.S. and Canada further reinforce the region’s leadership in the global market.

U.S. Surgery Pouch Market Insight

The U.S. Surgery Pouch market is witnessing strong growth due to rising incidence of gastrointestinal disorders, increasing adoption of minimally invasive colorectal surgeries, and strong healthcare infrastructure. The country benefits from advanced hospital systems, high adoption of innovative surgical technologies, and strong presence of leading medical device companies. Growing focus on obesity management, inflammatory bowel disease treatment, and improved surgical outcomes is further supporting market demand. In addition, favorable reimbursement policies and continuous clinical research activities are accelerating adoption of surgery pouch procedures across healthcare facilities.

Europe Surgery Pouch Market Insight

The Europe Surgery Pouch market remains a key contributor to global demand, driven by strong healthcare systems, increasing prevalence of colorectal diseases, and rising adoption of advanced surgical procedures. The region benefits from well-established surgical expertise, strong regulatory frameworks, and increasing focus on minimally invasive treatments. Growing investments in hospital infrastructure and rising awareness regarding early disease diagnosis are further supporting market growth. In addition, expanding use of pouch reconstruction procedures in specialized surgical centers is strengthening regional adoption.

U.K. Surgery Pouch Market Insight

The U.K. Surgery Pouch market is experiencing steady growth due to increasing cases of inflammatory bowel diseases and strong adoption of advanced colorectal surgical techniques. Rising investment in NHS healthcare infrastructure and growing access to specialized surgical care are supporting demand. The country is also witnessing increasing use of minimally invasive procedures, improving patient recovery outcomes. In addition, strong clinical expertise and growing awareness of surgical treatment options are contributing to market expansion.

Germany Surgery Pouch Market Insight

The Germany Surgery Pouch market is expanding steadily due to strong healthcare infrastructure, high surgical standards, and increasing prevalence of gastrointestinal disorders. The country benefits from advanced hospital systems, strong medical research capabilities, and early adoption of innovative surgical procedures. Rising demand for minimally invasive surgeries and increasing focus on patient recovery outcomes are further driving market growth. In addition, strong regulatory support and continuous innovation in surgical technologies are reinforcing adoption.

Asia-Pacific Surgery Pouch Market Insight

The Asia-Pacific Surgery Pouch market is expected to witness the fastest growth at a CAGR of 8.1% from 2026 to 2033, fueled by rising healthcare expenditure, expanding access to advanced gastrointestinal surgical procedures, and increasing awareness of treatment options for inflammatory bowel diseases. Rapid expansion of hospital infrastructure across China, India, and Japan is significantly improving surgical access. Growing medical tourism, improving insurance coverage, and increasing presence of global medical device companies are further accelerating market growth in the region.

Japan Surgery Pouch Market Insight

The Japan Surgery Pouch market is witnessing steady growth due to advanced healthcare systems, rising prevalence of colorectal disorders, and increasing adoption of minimally invasive surgical procedures. Strong focus on precision medicine and high-quality surgical outcomes is driving demand. The country also benefits from advanced hospital infrastructure and strong technological integration in healthcare. In addition, increasing use of robotic-assisted and laparoscopic surgeries is supporting market expansion.

China Surgery Pouch Market Insight

The China Surgery Pouch market is growing rapidly due to increasing healthcare investments, rising incidence of gastrointestinal diseases, and expanding access to advanced surgical procedures. Strong government focus on healthcare modernization and rapid expansion of hospital infrastructure are supporting demand. Increasing awareness of inflammatory bowel disease treatment options and rising adoption of minimally invasive surgeries are further accelerating growth. In addition, growing presence of global medical device companies and improving healthcare insurance coverage are strengthening market expansion.

Surgery Pouch Market Share

The Surgery Pouch industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- ConvaTec Group plc (U.K.)

- B. Braun Melsungen AG (Germany)

- Hollister Incorporated (U.S.)

- Coloplast A/S (Denmark)

- Teleflex Incorporated (U.S.)

- Cook Medical (U.S.)

- Smith & Nephew plc (U.K.)

- Cardinal Health (U.S.)

- Boston Scientific Corporation (U.S.)

- W. L. Gore & Associates (U.S.)

- Olympus Corporation (Japan)

- Stryker Corporation (U.S.)

- Johnson & Johnson (Ethicon) (U.S.)

- 3M Company (U.S.)

- Becton, Dickinson and Company (U.S.)

- Acelity (KCI Medical) (U.S.)

- Hologic Inc. (U.S.)

- Dornier MedTech (Germany)

- Turkiye Hospital Supply Companies (Turkey)

- Welland Medical Ltd. (U.K.)

- Shriner Medical (U.S.)

- GPC Medical Ltd. (India)

- Narang Medical Limited (India)

- Terumo Corporation (Japan)

- Nipro Corporation (Japan)

- Fujifilm Holdings Corporation (Japan)

- Henan Shuguang Jianshi Medical Equipment (China)

- Shandong Weigao Group Medical Polymer (China)

- Suzhou Kangli Medical (China)

- Jiangsu Kangjin Medical Instruments Co., Ltd. (China)

- Hospitech Co. Ltd. (South Korea)

- Ansell Limited (Australia)

- Medline Industries (U.S.)

Latest Developments in Surgery Pouch Market

- In February 2021, surgeons and researchers published updated long-term outcome data on ileal pouch–anal anastomosis (IPAA), highlighting improved surgical techniques and reduced complication rates over the past decades. The study emphasized the evolution of pouch surgery from open procedures to minimally invasive approaches, showing better patient recovery, lower anastomotic leak rates, and improved pouch durability. It also confirmed that high-volume colorectal centers achieve significantly better outcomes, reinforcing the importance of specialized surgical expertise in surgery pouch procedures

- In October 2023, Cleveland Clinic updated its clinical guidance on ileal pouch–anal anastomosis (J-pouch surgery), explaining its role as the most common reconstructive procedure after total proctocolectomy in ulcerative colitis patients. The update highlighted that the surgery creates an internal pouch from the ileum, allowing patients to pass stool normally without a permanent external ostomy bag. It also emphasized improvements in surgical safety, patient quality of life, and expanding use in colorectal disease management

- In June 2024, Mayo Clinic published updated procedural insights on J-pouch surgery, reinforcing its continued role as a standard treatment for ulcerative colitis when medications fail. The update described advancements in multi-stage surgical techniques, where the colon and rectum are removed and an internal pouch is created for intestinal continuity. It also highlighted growing adoption of minimally invasive surgical approaches that reduce recovery time and improve postoperative outcomes

- In March 2026 (reported retrospective developments from 2021–2025 treatment evolution), clinical literature highlighted that UC J-pouch alternatives and pouch surgical innovations have expanded significantly due to improved biologic therapies and surgical techniques. The development shows a clear shift toward personalized surgical decision-making, better patient selection, and reduced dependency on permanent ostomy procedures. These advancements are strongly influencing modern colorectal surgical practice and expanding treatment options for inflammatory bowel disease patients

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.