Global Surgical Simulator Market

Market Size in USD Million

USD

369.09 Million

USD

683.15 Million

2024

2032

USD

369.09 Million

USD

683.15 Million

2024

2032

| 2025 - 2032 | |

| USD 369.09 Million | |

| USD 683.15 Million | |

| % | |

|

Surgical Simulator Market Size

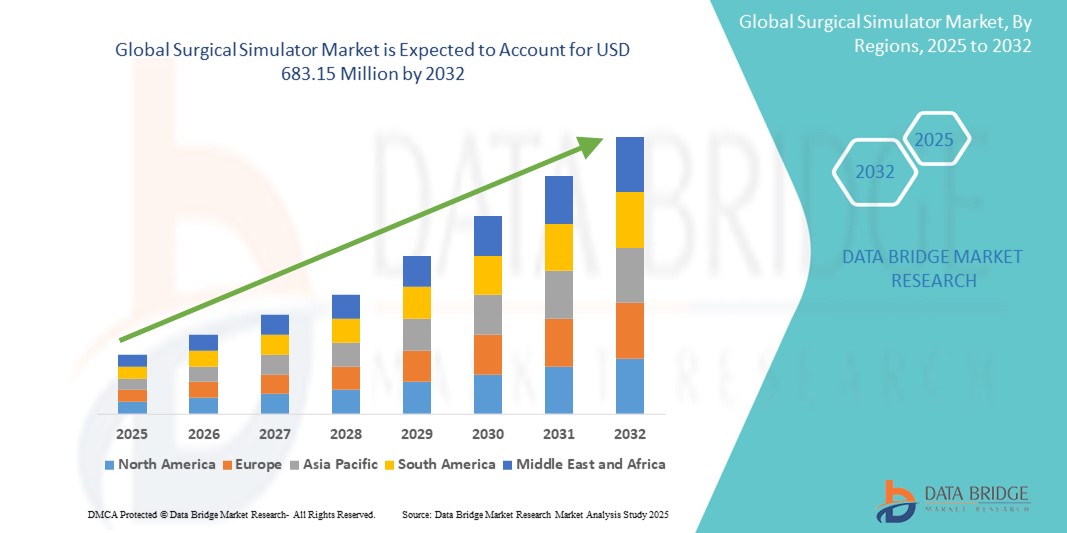

- The global surgical simulator market size was valued at USD 369.09 Million in 2024 and is expected to reach USD 683.15 Million by 2032, at a CAGR of 8.00% during the forecast period

- The market growth is largely fueled by the increasing need for advanced training tools in medical education, coupled with technological advancements in simulation-based learning. Surgical simulators are gaining traction as they offer a risk-free environment for healthcare professionals to refine their skills, leading to improved patient outcomes and safety

- Furthermore, the growing demand for minimally invasive procedures and the integration of virtual reality (VR) and augmented reality (AR) into surgical training modules are establishing surgical simulators as a critical component in modern medical curricula. These converging factors are accelerating the adoption of Surgical Simulator solutions, thereby significantly boosting the industry's growth

Surgical Simulator Market Analysis

- Surgical simulators, offering high-fidelity, computer-based training environments, are becoming essential tools in medical education and surgical skill development due to their ability to replicate real-life surgical procedures without putting patients at risk. Their integration into medical institutions is transforming how surgeons and healthcare professionals acquire and maintain technical proficiency

- The escalating demand for surgical simulators is primarily fueled by advancements in minimally invasive surgical techniques, increasing use of virtual reality (VR) and augmented reality (AR) technologies, and a growing emphasis on patient safety and training efficiency

- North America dominated the surgical simulator market with the largest revenue share of 31.7% in 2024, characterized by early adoption of simulation-based medical education, presence of leading manufacturers, and strong investment in healthcare infrastructure and training programs. The U.S., in particular, is experiencing rapid growth in simulator installations across medical schools and hospitals, driven by regulatory emphasis on clinical competency and innovation in AI-powered simulation platforms

- Asia-Pacific is expected to be the fastest growing region in the surgical simulator market during the forecast period, projected to grow at a CAGR of 16.2%, due to increasing investments in healthcare education, growing medical tourism, and expanding awareness about surgical training technologies in countries such as China, India, and Japan

- The products segment dominated the surgical simulator market with a market share of 68.5% in 2024, driven by the rising demand for advanced surgical training tools across medical institutions. High-fidelity simulators, virtual reality (VR) systems, and haptic feedback-enabled devices are widely used to improve surgical precision and enhance trainee competence in complex procedures

Report Scope and Surgical Simulator Market Segmentation

|

Attributes |

Surgical Simulator Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Surgical Simulator Market Trends

“Advancements in Realistic Simulation and Immersive Training”

- A significant and accelerating trend in the global surgical simulator market is the increasing sophistication of simulation technologies, emphasizing high-fidelity, immersive environments that replicate real-life surgical procedures. This shift is enhancing the training of medical professionals by offering hands-on experience in a risk-free setting

- For instance, VirtaMed’s ArthroS simulator provides highly realistic arthroscopy training for orthopedic procedures using actual surgical tools and anatomically accurate tactile feedback. Similarly, CAE Healthcare’s Vimedix system enables clinicians to practice ultrasound-guided interventions in a virtual patient environment with dynamic physiological responses

- Modern simulators are now capable of replicating complex procedures across multiple specialties—ranging from neurosurgery and cardiology to obstetrics—using haptic feedback, real-time complication scenarios, and procedure-specific modules. These features ensure a more comprehensive and customized training experience

- The integration of virtual reality (VR) and augmented reality (AR) in simulators further enhances realism, allowing trainees to interact with 3D anatomical structures and respond to evolving surgical challenges. For instance, companies such as Osso VR and FundamentalVR offer immersive VR platforms that track hand movements and provide performance analytics

- This trend towards hyper-realistic, interactive, and specialty-specific simulation tools is fundamentally reshaping medical education. As a result, institutions are rapidly investing in these platforms to standardize surgical training, reduce learning curves, and improve patient safety

- The demand for advanced surgical simulators is surging across teaching hospitals, medical schools, and healthcare training centers, driven by the need to prepare the next generation of surgeons with hands-on, skill-intensive training that complements traditional didactic learning

Surgical Simulator Market Dynamics

Driver

“Growing Need Due to Rising Demand for Skilled Surgeons and Minimally Invasive Procedures”

- The increasing demand for minimally invasive surgeries, coupled with the global shortage of skilled surgeons, is a major driver fueling the growth of the surgical simulator market. These simulators provide a risk-free, cost-effective solution to enhance surgical training and reduce procedural errors

- For instance, in April 2024, Surgical Science Sweden AB announced an upgrade to its laparoscopic training platform, incorporating more advanced anatomical realism and feedback mechanisms to accelerate skill development. Innovations such as these are expected to propel the adoption of surgical simulators during the forecast period

- As healthcare systems prioritize patient safety and procedural efficiency, surgical simulators enable medical professionals to rehearse complex procedures, refine motor skills, and familiarize themselves with new tools and techniques, all without endangering patient lives

- Furthermore, the rise in virtual training programs—especially post-COVID-19—has prompted academic institutions and hospitals to invest in VR- and AR-enabled simulation tools that offer remote access and immersive learning

- The ability to track performance metrics, receive real-time feedback, and adapt training modules based on individual learning curves has made surgical simulators indispensable in modern surgical education. The growing integration of these tools into medical curricula and residency programs is further driving their widespread adoption across the globe

Restraint/Challenge

“High Capital Investment and Limited Access in Low-Income Settings”

- Despite their benefits, surgical simulators come with high upfront costs, often making them inaccessible to healthcare institutions in low- and middle-income countries. The investment required for full simulation labs, including hardware, software, and maintenance, can be a significant barrier

- For instance, setting up a full-suite laparoscopic simulator can cost tens of thousands of dollars, making it difficult for smaller hospitals and medical colleges to integrate such technology into their training programs

- In addition, concerns about the lack of trained personnel to operate and maintain these advanced systems can further delay their adoption, particularly in developing regions where digital infrastructure and technical training are limited

- To overcome these challenges, manufacturers are increasingly exploring cloud-based and modular simulation platforms that reduce hardware dependency and offer scalable, affordable solutions. Moreover, partnerships with academic institutions and non-profit organizations could help expand access to simulation training in resource-constrained environments

- Bridging this accessibility gap through cost-effective innovation and broader training initiatives will be essential for unlocking the full potential of surgical simulators globally

Surgical Simulator Market Scope

The market is segmented on the basis of offering, type, and end user.

- By Offering

On the basis of offering, the surgical simulator market is segmented into products and services. The products segment accounted for the largest market revenue share of 68.5% in 2024, driven by the rising demand for advanced surgical training tools across medical institutions. High-fidelity simulators, virtual reality (VR) systems, and haptic feedback-enabled devices are widely used to improve surgical precision.

The services segment is expected to witness the fastest growth with a CAGR of 17.9% from 2025 to 2032, fueled by growing demand for simulation-based training programs, technical support, software updates, and cloud-based access to virtual procedures.

- By Type

On the basis of type, the surgical simulator market is segmented into technology-based simulator, model-based simulator, and computer-based simulator. The technology-based simulator segment held the largest market revenue share of 52.3% in 2024, driven by widespread adoption of virtual and augmented reality simulators with real-time feedback. These offer immersive and repeatable training environments across surgical disciplines.

The computer-based simulator segment is projected to witness the fastest CAGR of 18.7% from 2025 to 2032, due to their accessibility, low cost, and the ease of integrating them into remote learning and online training platforms.

• By End User

On the basis of end user, the surgical simulator market is segmented into academic and research institutes, hospitals, surgical clinics, and military organizations. The academic and research institutes segment dominated the market in 2024 with a revenue share of 41.2%, driven by growing incorporation of simulation technologies into medical education curricula and residency training programs.

The hospitals segment is expected to register the fastest CAGR of 16.4% from 2025 to 2032, as healthcare facilities invest in surgical simulators to enhance patient safety, reduce complications, and support ongoing professional development.

Surgical Simulator Market Regional Analysis

- North America dominated the surgical simulator market with the largest revenue share of 31.7% in 2024, driven by the region’s strong emphasis on medical education reform and adoption of advanced healthcare training technologies

- The presence of well-established medical institutions, favorable reimbursement policies, and early adoption of virtual and augmented reality-based simulation tools significantly contribute to regional growth

- In addition, increased investments in healthcare infrastructure, growing demand for minimally invasive surgical training, and a highly skilled workforce are accelerating the uptake of surgical simulators across academic, clinical, and military settings, solidifying North America’s leadership in this market

U.S. Surgical Simulator Market Insight

The U.S. surgical simulator market captured the largest revenue share of 82.86% in 2024 within North America, driven by a strong focus on simulation-based medical training and widespread adoption across academic institutions, hospitals, and military organizations. The U.S. market benefits from robust investment in healthcare education infrastructure, increasing demand for minimally invasive surgical training, and early adoption of advanced technologies such as virtual reality (VR), augmented reality (AR), and AI-enhanced simulators. Furthermore, supportive government initiatives, high healthcare spending, and partnerships between medical schools and simulation providers are accelerating growth in the country.

Europe Surgical Simulator Market Insight

The Europe surgical simulator market is projected to expand at a substantial CAGR throughout the forecast period, primarily fueled by increasing demand for patient safety, reduction of surgical errors, and a growing preference for competency-based surgical education. European countries are embracing simulation-based training to comply with stringent regulatory guidelines and improve surgical proficiency. Countries such as Germany, the U.K., and France are at the forefront of integrating simulation into medical curricula and certification programs.

U.K. Surgical Simulator Market Insight

The U.K. surgical simulator market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by a strong emphasis on medical education reform and enhanced clinical training requirements. The National Health Service (NHS) and various academic institutions are investing in simulation labs to improve clinical outcomes and meet rising training standards. The U.K.'s proactive approach in adopting innovative healthcare training technologies is expected to drive substantial market growth.

Germany Surgical Simulator Market Insight

The Germany surgical simulator market is expected to expand at a considerable CAGR during the forecast period, fueled by the country's strong commitment to medical innovation, structured residency programs, and continuous professional development initiatives. Germany’s healthcare system is rapidly integrating surgical simulators to enhance procedural accuracy and patient safety. The emphasis on training for minimally invasive and robotic surgeries is further driving simulator adoption across hospitals and academic centers.

Asia-Pacific Surgical Simulator Market Insight

The Asia-Pacific surgical simulator market is poised to grow at the fastest CAGR of 16.2% from 2025 to 2032, driven by increasing investments in healthcare infrastructure, a rising number of medical schools, and technological advancements in countries such as China, Japan, and India. Government initiatives promoting medical education reform and digital health transformation are bolstering the adoption of simulation tools. In addition, partnerships between global simulation companies and regional institutions are enhancing access and affordability across the region.

Japan Surgical Simulator Market Insight

The Japan surgical simulator market is gaining momentum due to the country’s strong emphasis on precision medicine, technological leadership, and demand for high-quality surgical outcomes. Japan’s aging population and increasing surgical volume are prompting hospitals and training centers to adopt advanced simulation solutions to reduce complication rates and improve procedural efficiency. Integration of simulators with robotics and AR/VR technologies is a key growth driver.

China Surgical Simulator Market Insight

The China surgical simulator market accounted for the largest revenue share in Asia-Pacific in 2024, supported by rapid growth in medical education institutions, expanding healthcare access, and strong government support for smart healthcare technologies. China is actively deploying simulation-based learning in universities and hospitals to address a growing physician workforce and improve surgical competency. In addition, local manufacturers are contributing to innovation and cost-effective simulator production, enhancing domestic market penetration.

Surgical Simulator Market Share

The surgical simulator industry is primarily led by well-established companies, including:

- Materialise (Belgium)

- Stratasys (Israel)

- CAE Inc. (Canada)

- Surgical Science Sweden AB (Sweden)

- Mentice AB (Sweden)

- Gaumard Scientific (U.S.)

- Simulab Corporation (U.S.)

- VirtaMed AG (Switzerland)

- 3-Dmed Learning Through Simulation (U.S.)

- Laerdal Medical (Norway)

- 3D Systems, Inc. (U.S.)

- Osteo3d (U.S.)

- AXIAL3D (U.K.)

Latest Developments in Global Surgical Simulator Market

- In April 2023, CAE Healthcare, a global leader in medical simulation, announced the launch of CAE VimedixAR, an augmented reality ultrasound simulator developed in partnership with Microsoft HoloLens. This advancement enhances training by offering a 360-degree anatomical view, helping learners visualize complex procedures in real-time. With CAE holding approximately 19.2% of the global surgical simulator market share in 2024, this innovation underscores the company's ongoing commitment to immersive simulation technologies in clinical education

- In March 2023, Surgical Science Sweden AB, which captured 13.6% of the global market share in 2024, acquired SenseGraphics AB, a provider of advanced VR-based medical simulation software. This acquisition aimed to strengthen Surgical Science’s presence in high-fidelity simulation, combining cutting-edge graphics with advanced haptics. The strategic move supports the company’s expansion into more advanced and interactive simulation platforms, driving the broader adoption of VR-based simulators in laparoscopic and robotic surgery training

- In March 2023, Mentice AB, which accounted for around 8.9% of the global market in 2024, launched Mentice VIST One TEE, a new simulator dedicated to transesophageal echocardiography (TEE) training. This system allows interventional teams to practice complex cardiac procedures using real-time image feedback. The launch aligns with the growing demand for cardiology-focused simulation training in hospitals and academic centers

- In February 2023, 3D Systems Corporation, representing 7.4% of global revenue share in the surgical simulation space, announced the expansion of its Simbionix portfolio to include robot-assisted surgical training modules. These new training systems are tailored for the Da Vinci surgical platform, addressing the rising demand for robotic surgery education. This development positions 3D Systems as a key contributor to the advancement of robotic surgery simulation technologies

- In January 2023, VirtaMed AG, holding 5.7% of the market share, unveiled a strategic collaboration with major urology training programs in Europe to integrate its UroSim simulator into residency curricula. This partnership supports enhanced proficiency in urological procedures and reflects the increasing institutional adoption of surgical simulators as mandatory training tools

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.