Global Sustainable Bottled Water Packaging Market

Market Size in USD Billion

USD

11.41 Billion

USD

22.98 Billion

2025

2033

USD

11.41 Billion

USD

22.98 Billion

2025

2033

| 2026 - 2033 | |

| USD 11.41 Billion | |

| USD 22.98 Billion | |

| % | |

|

Sustainable Bottled Water Packaging Market Size

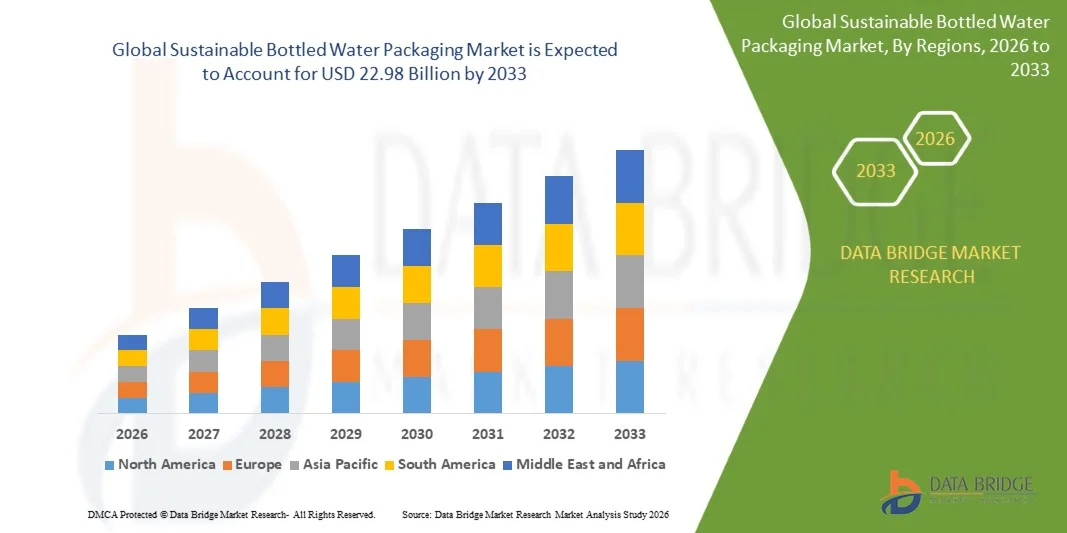

- The global sustainable bottled water packaging market size was valued at USD 11.41 billion in 2025 and is expected to reach USD 22.98 billion by 2033, at a CAGR of 9.15% during the forecast period

- The market growth is largely fueled by rising environmental concerns over plastic pollution and increasing global pressure to adopt sustainable packaging alternatives in the bottled water industry, leading to a strong shift toward recyclable, reusable, and bio-based packaging materials such as rPET, aluminum, and bioplastics

- Furthermore, stringent government regulations on single-use plastics, combined with corporate sustainability commitments and circular economy initiatives by leading beverage brands, are significantly accelerating the transition toward eco-friendly bottled water packaging solutions, thereby driving overall market expansion

Sustainable Bottled Water Packaging Market Analysis

- Sustainable bottled water packaging refers to environmentally responsible packaging solutions designed to reduce plastic waste, improve recyclability, and lower carbon footprint through the use of materials such as recycled PET, bioplastics, glass, aluminum, and paper-based formats

- The growing demand for sustainable bottled water packaging is primarily driven by increasing consumer awareness regarding environmental impact, regulatory restrictions on plastic usage, and strong adoption of circular economy practices by global beverage manufacturers

- Asia-Pacific dominated the sustainable bottled water packaging market with a share of 38.5% in 2025, due to rising bottled water consumption, rapid urbanization, and increasing environmental awareness across developing economies

- North America is expected to be the fastest growing region in the sustainable bottled water packaging market during the forecast period due to rising demand for sustainable packaging in the beverage industry and increasing regulatory pressure on plastic waste reduction

- Bottles segment dominated the market with a market share of 68.8% in 2025, due to their widespread usage, convenience, and strong compatibility with recycling systems. Bottled formats remain the most preferred packaging option due to ease of handling, transportation efficiency, and consumer familiarity across both developed and emerging markets. Manufacturers are increasingly adopting lightweight designs and incorporating recycled materials to enhance sustainability without compromising functionality

Report Scope and Sustainable Bottled Water Packaging Market Segmentation

|

Attributes |

Sustainable Bottled Water Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Sustainable Bottled Water Packaging Market Trends

“Growing Shift Toward Recycled and Bio-Based Packaging Materials”

- A key trend in the sustainable bottled water packaging market is the increasing transition toward recycled plastics and bio-based packaging solutions driven by rising environmental awareness and corporate sustainability commitments. This shift is reshaping packaging strategies across the beverage industry as brands focus on reducing virgin plastic usage and improving circularity in packaging systems.

- For instance, Nestlé Waters and Danone have expanded the use of rPET bottles across their bottled water portfolios, while companies such as Coca-Cola are investing in bottles made with higher recycled content under their World Without Waste initiative. These developments are strengthening demand for closed-loop packaging systems and improving material recovery efficiency across global supply chains

- The adoption of lightweight packaging designs is also gaining momentum as manufacturers aim to reduce material consumption without compromising product safety and durability. This is enabling cost optimization while simultaneously lowering the environmental footprint associated with bottled water distribution

- Major packaging suppliers such as Amcor and ALPLA are actively developing recyclable and bio-based bottle solutions that support brand sustainability targets and regulatory compliance requirements. This is accelerating innovation in alternative materials such as plant-based plastics and compostable packaging formats

- The increasing focus on circular economy principles is encouraging beverage companies to redesign packaging formats to enhance recyclability and reuse potential. This is leading to stronger collaboration between packaging producers and water brands to establish efficient recycling ecosystems

- The market is witnessing growing alignment between consumer expectations and corporate sustainability strategies as demand rises for environmentally responsible bottled water packaging. This is reinforcing long-term adoption of recycled and bio-based materials across global production networks

Sustainable Bottled Water Packaging Market Dynamics

Driver

“Rising Regulatory Pressure to Reduce Single-Use Plastic Consumption”

- The increasing enforcement of regulations aimed at limiting single-use plastic usage is a major driver supporting the adoption of sustainable bottled water packaging solutions. Governments and regulatory bodies are implementing stricter policies that encourage recycling, reuse, and reduced plastic waste generation across the beverage industry

- For instance, the European Union Single-Use Plastics Directive has mandated higher recycled content targets and improved collection systems, influencing companies such as Danone and Nestlé to accelerate their shift toward recyclable packaging formats. These regulatory frameworks are driving large-scale investment in sustainable packaging technologies across global markets

- National authorities in regions such as India through the Central Pollution Control Board have introduced bans and restrictions on single-use plastics, pushing bottled water manufacturers to adopt eco-friendly alternatives. This is increasing demand for biodegradable materials and reusable packaging systems in domestic markets

- Major beverage companies such as PepsiCo are redesigning packaging portfolios to comply with evolving sustainability regulations while maintaining product accessibility and cost efficiency. This is encouraging continuous innovation in lightweight and recyclable bottle designs

- The sustained tightening of global plastic waste regulations continues to reinforce the need for scalable sustainable packaging solutions, making regulatory pressure a critical growth driver for the bottled water packaging market

Restraint/Challenge

“High Production Costs of Sustainable Packaging Alternatives”

- The high cost associated with producing sustainable packaging materials remains a significant challenge in the bottled water packaging market due to expensive raw materials, advanced processing requirements, and limited large-scale infrastructure. These cost pressures make it difficult for manufacturers to achieve price parity with conventional plastic packaging

- For instance, companies such as ALPLA and Amcor face higher production expenses when manufacturing rPET bottles due to the additional processing and purification steps required for recycled content integration. These cost structures limit rapid expansion in price-sensitive markets

- The sourcing of bio-based materials such as plant-derived polymers also increases overall production costs as supply chains for these materials are still developing and not fully optimized. This affects scalability and restricts widespread adoption across smaller bottled water brands

- Advanced manufacturing technologies required for sustainable packaging, including high-precision molding and specialized recycling systems, further increase capital investment requirements. This raises operational complexity for packaging manufacturers and beverage companies alike

- The overall economic challenge of balancing sustainability goals with cost competitiveness continues to restrain rapid market expansion, making cost optimization a key focus area for industry participants in sustainable bottled water packaging

Sustainable Bottled Water Packaging Market Scope

The market is segmented on the basis of material type, packaging type, sustainability type, and pack size.

• By Material Type

On the basis of material type, the sustainable bottled water packaging market is segmented into recycled PET (rPET), bioplastics, glass, aluminum, and paper-based packaging. The recycled PET (rPET) segment dominated the largest market revenue share in 2025, driven by increasing regulatory pressure to use recycled content and strong industry commitments toward circular economy goals. Beverage manufacturers are rapidly shifting toward rPET due to its compatibility with existing production infrastructure and its ability to significantly reduce carbon footprint compared to virgin plastics. The availability of improved recycling technologies and growing investments in recycling infrastructure further support the widespread adoption of rPET across global markets. In addition, major brands are setting ambitious targets for recycled content usage, accelerating demand for rPET-based packaging solutions. The cost-effectiveness and scalability of rPET make it a preferred material for large-scale bottled water production.

The bioplastics segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising consumer demand for plant-based and environmentally friendly alternatives to conventional plastics. Bioplastics offer the advantage of reduced dependence on fossil fuels and lower greenhouse gas emissions, aligning with global sustainability goals and brand positioning strategies. Continuous advancements in bio-based polymer technologies are improving performance characteristics such as durability and barrier properties, making them more viable for bottled water packaging. Increasing government support for bio-based materials and stricter regulations on single-use plastics are further accelerating adoption. The growing awareness among environmentally conscious consumers is also encouraging brands to introduce innovative bioplastic packaging formats.

• By Packaging Type

On the basis of packaging type, the sustainable bottled water packaging market is segmented into bottles, cans, cartons, and pouches. The bottles segment held the largest market revenue share of 68.8% in 2025 driven by their widespread usage, convenience, and strong compatibility with recycling systems. Bottled formats remain the most preferred packaging option due to ease of handling, transportation efficiency, and consumer familiarity across both developed and emerging markets. Manufacturers are increasingly adopting lightweight designs and incorporating recycled materials to enhance sustainability without compromising functionality. The extensive distribution network and established manufacturing processes further strengthen the dominance of bottles in the market. In addition, innovations in bottle design and labeling are supporting brand differentiation and environmental compliance.

The cartons segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing demand for plastic-free and low-carbon packaging alternatives. Cartons are gaining traction due to their renewable raw material base and favorable environmental perception among consumers. Technological advancements in barrier coatings and structural integrity are enabling cartons to effectively store water while maintaining product safety and shelf life. Growing regulatory emphasis on reducing plastic waste and increasing recyclability is encouraging companies to explore carton-based solutions. The shift toward sustainable retail packaging and rising investments in paper-based packaging infrastructure are further supporting segment growth.

• By Sustainability Type

On the basis of sustainability type, the sustainable bottled water packaging market is segmented into recyclable, reusable, biodegradable, and compostable. The recyclable segment dominated the largest market revenue share in 2025, driven by well-established recycling systems and strong regulatory frameworks promoting material recovery. Recyclable packaging materials such as PET and aluminum are widely accepted across global recycling networks, making them a practical choice for manufacturers aiming to meet sustainability targets. Increasing consumer awareness regarding recycling practices and waste reduction is further supporting demand for recyclable packaging solutions. Companies are focusing on improving recyclability rates and incorporating higher recycled content to strengthen environmental credentials. The scalability and economic feasibility of recycling infrastructure continue to reinforce the dominance of this segment.

The biodegradable segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by growing concerns over plastic pollution and landfill accumulation. Biodegradable packaging offers the advantage of natural decomposition, reducing long-term environmental impact and supporting waste management efforts. Continuous innovation in biodegradable materials is improving durability and usability for bottled water applications. Governments and environmental organizations are actively promoting biodegradable alternatives through policies and awareness campaigns. The increasing shift toward sustainable consumption patterns is encouraging brands to adopt biodegradable packaging as a differentiation strategy.

• By Pack Size

On the basis of pack size, the sustainable bottled water packaging market is segmented into 331ml-500ml, 501ml-1000ml, 1001ml-1500ml, and above 1500ml. The 501ml-1000ml segment held the largest market revenue share in 2025 driven by its optimal balance between portability and adequate hydration volume. This pack size is widely preferred by consumers for daily use, travel, and on-the-go consumption, making it a dominant format across retail and convenience channels. Manufacturers favor this segment due to its high turnover rate and compatibility with sustainable packaging innovations such as lightweight bottles and recycled materials. The segment also benefits from strong demand across urban populations and growing health awareness trends. Efficient logistics and storage advantages further contribute to its widespread adoption.

The above 1500ml segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing demand for bulk consumption and reduced packaging waste per liter. Larger pack sizes are gaining popularity among households and workplaces aiming to minimize frequent purchases and lower environmental impact. The cost efficiency associated with bulk packaging and reduced material usage per unit volume supports its growing adoption. Manufacturers are focusing on developing durable and reusable large-format packaging solutions to enhance sustainability. Rising awareness regarding waste reduction and resource efficiency is further accelerating demand in this segment.

Sustainable Bottled Water Packaging Market Regional Analysis

- Asia-Pacific dominated the sustainable bottled water packaging market with the largest revenue share of 38.5% in 2025, driven by rising bottled water consumption, rapid urbanization, and increasing environmental awareness across developing economies

- The region benefits from strong manufacturing capabilities, large-scale packaging production hubs, and growing adoption of recyclable and lightweight packaging solutions. Expanding retail networks and rising demand for convenient hydration formats are further accelerating market penetration across both urban and semi-urban populations

- In addition, supportive government initiatives promoting plastic waste reduction and circular economy practices are strengthening the shift toward sustainable packaging materials

China Sustainable Bottled Water Packaging Market Insight

China held the largest share in the Asia-Pacific sustainable bottled water packaging market in 2025, supported by its massive bottled water consumption base and strong packaging manufacturing ecosystem. The country’s strict environmental regulations and aggressive policies on plastic reduction are driving rapid adoption of rPET, cartons, and other sustainable alternatives. Large-scale investments in recycling infrastructure and advanced packaging technologies are further enhancing material recovery efficiency. In addition, strong participation from domestic beverage giants and packaging manufacturers is reinforcing China’s leadership in sustainable packaging innovation.

India Sustainable Bottled Water Packaging Market Insight

India is witnessing the fastest growth in the Asia-Pacific region from 2026 to 2033, fueled by rising health awareness, increasing bottled water consumption, and expanding urban population. Government initiatives focused on banning single-use plastics and promoting sustainable materials are accelerating the shift toward eco-friendly packaging solutions. Rapid growth in retail distribution networks and e-commerce channels is further supporting demand for packaged drinking water. In addition, increasing investments in recycling infrastructure and growing participation of domestic brands are strengthening market expansion.

Europe Sustainable Bottled Water Packaging Market Insight

Europe accounted for a significant share of the sustainable bottled water packaging market in 2025, driven by stringent environmental regulations, high recycling rates, and strong consumer preference for eco-friendly packaging. The region has well-established sustainability frameworks that encourage the use of recyclable, reusable, and bio-based packaging materials. Beverage companies are actively transitioning toward carbon-neutral packaging solutions to meet regulatory and corporate sustainability targets. In addition, strong innovation in bioplastics and paper-based packaging is further supporting regional market growth.

Germany Sustainable Bottled Water Packaging Market Insight

Germany held a leading position in the European market in 2025, supported by its advanced recycling systems, strong environmental policies, and highly developed packaging industry. The country’s emphasis on circular economy practices and extended producer responsibility is driving high adoption of recyclable and reusable packaging formats. Strong presence of packaging technology providers and beverage manufacturers is further enhancing innovation in sustainable bottle design. In addition, consumer preference for environmentally responsible products continues to strengthen market demand.

U.K. Sustainable Bottled Water Packaging Market Insight

The U.K. market is growing steadily, driven by increasing regulatory focus on reducing plastic waste and rising consumer demand for sustainable packaging solutions. Government initiatives promoting deposit return schemes and recyclable packaging are encouraging beverage companies to shift toward eco-friendly materials. The strong retail sector and growing on-the-go consumption trends are further supporting bottled water demand. In addition, increasing investments in sustainable packaging innovation and circular economy initiatives are contributing to market development.

North America Sustainable Bottled Water Packaging Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for sustainable packaging in the beverage industry and increasing regulatory pressure on plastic waste reduction. Strong consumer awareness regarding environmental sustainability is accelerating adoption of recyclable and bioplastic packaging solutions. The region also benefits from advanced recycling infrastructure and high investment in sustainable material innovation. In addition, major beverage companies are actively committing to 100% recyclable packaging goals, further supporting market expansion.

U.S. Sustainable Bottled Water Packaging Market Insight

The U.S. accounted for the largest share in the North America sustainable bottled water packaging market in 2025, driven by high bottled water consumption and strong presence of leading beverage manufacturers. Increasing corporate sustainability commitments and regulatory focus on reducing single-use plastics are driving rapid adoption of rPET and other recyclable materials. Advanced recycling technologies and strong collection systems further support circular packaging initiatives. In addition, continuous innovation in lightweight and eco-friendly packaging formats is strengthening the country’s leadership position in the region.

Sustainable Bottled Water Packaging Market Share

The sustainable bottled water packaging industry is primarily led by well-established companies, including:

- Greif, Inc. (U.S.)

- Amcor plc (Switzerland)

- PLASTIPAK HOLDINGS, INC. (U.S.)

- Graham Packaging Company (U.S.)

- Kaufman Container (U.S.)

- Greiner Packaging (Austria)

- Alpha Group (U.S.)

- Sidel Group (France)

- Silgan Holdings Inc. (U.S.)

- Berry Global Inc. (U.S.)

- CKS Packaging, Inc. (U.S.)

- APEX Plastics (U.S.)

- SKS Bottle & Packaging, Inc. (U.S.)

- Exo Packaging (Australia)

- Alpack Plastics (Ireland)

- P.P.C., Inc. (U.S.)

Latest Developments in Global Sustainable Bottled Water Packaging Market

- In July 2025, Kopu, a premium bottled water brand, introduced aluminum bottles along with a turnkey recycling program designed for luxury hotels and resorts. This development is strengthening circular packaging adoption in the hospitality sector by replacing single-use plastic bottles with fully recyclable aluminum formats. It is also helping premium hotels reduce operational waste while meeting sustainability targets and improving environmental responsibility in guest services. The integrated recycling system enhances material recovery efficiency and supports long-term reduction of packaging waste across luxury hospitality operations

- In February 2025, Win Water launched its innovative bottled water solution featuring 100% plant-based bottles that are fully biodegradable. This development is accelerating the shift toward bio-based packaging in the bottled water industry by addressing rising concerns over plastic pollution. It supports growing consumer demand for environmentally responsible hydration products while positioning the brand as a leader in sustainable packaging innovation. The launch further reinforces industry movement toward replacing conventional plastics with renewable and compostable alternatives

- In January 2025, Brand New Day partnered with a small entrepreneurial business to develop mineral water packaged in bottles made 100% from plant-based materials that are recyclable and biodegradable. This development is driving early-stage innovation in sustainable packaging by combining product strategy with full brand identity creation, including design and logo development. It highlights the increasing role of design-led entrepreneurship in introducing eco-friendly packaging concepts to the bottled water market. The initiative is also encouraging wider exploration of plant-based packaging solutions among emerging beverage brands focused on sustainability

- In August 2024, Berry Global Inc. partnered with Aquafigure to launch a reusable 330ml water bottle made from BPA-free Tritan, a recyclable and food-approved copolyester. This development is strengthening the sustainable bottled water packaging market by promoting reusable “bottle for life” solutions aimed at reducing single-use plastic consumption. The inclusion of customizable 3D artwork cards enhances consumer engagement while supporting behavioral shifts toward reuse-based consumption. It also reinforces circular economy principles by combining durability, recyclability, and personalization in packaging design

- In July 2024, Source introduced Sky Wtr, a canned water product created using air and sunlight technology and packaged in recyclable aluminum cans and bottles. This development is contributing to innovation in sustainable bottled water packaging by integrating renewable production methods with fully recyclable packaging formats. It helps address global water accessibility challenges while reducing reliance on conventional water sourcing systems. The use of aluminum packaging further strengthens recyclability and supports growing demand for low-impact, sustainability-driven bottled water solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Sustainable Bottled Water Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Sustainable Bottled Water Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Sustainable Bottled Water Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.