Global Sustainable Dairy Value Chain Market

Market Size in USD Billion

USD

28.97 Billion

USD

47.15 Billion

2025

2033

USD

28.97 Billion

USD

47.15 Billion

2025

2033

| 2026 - 2033 | |

| USD 28.97 Billion | |

| USD 47.15 Billion | |

| % | |

|

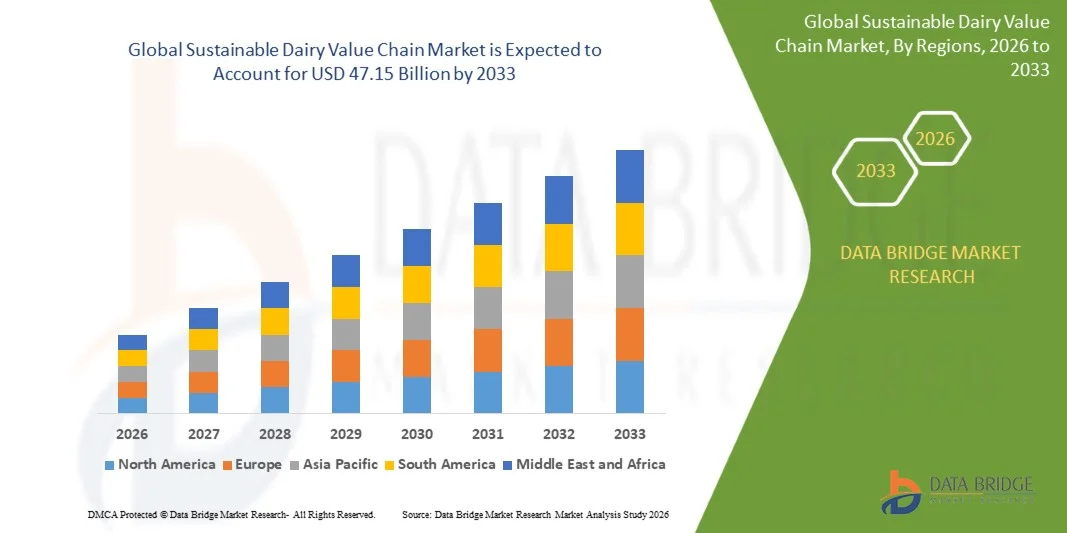

Sustainable Dairy Value Chain Market Size

- The global Sustainable Dairy Value Chain market size was valued at USD 28.97 billion in 2025and is expected to reach USD 47.15 billion by 2033, at a CAGR of 6.28% during the forecast period

- The market growth is largely fueled by increasing global demand for sustainable food systems, rising focus on reducing greenhouse gas emissions in livestock farming, and continuous advancements in precision agriculture, digital dairy farming, and eco-friendly processing technologies across the dairy industry

- Furthermore, growing consumer preference for ethically sourced, traceable, and environmentally responsible dairy products, along with rising adoption of circular economy practices, renewable energy integration, and water-efficient farming methods, is establishing Sustainable Dairy Value Chain solutions as a key transformation driver in the dairy industry. These converging factors are accelerating the uptake of Sustainable Dairy Value Chain solutions, thereby significantly boosting the industry's growth

Sustainable Dairy Value Chain Market Analysis

- Sustainable Dairy Value Chain solutions, including precision dairy farming systems, methane-reduction technologies, sustainable feed optimization, cold-chain efficiency solutions, and traceable dairy sourcing platforms, are increasingly vital components of modern agri-food systems due to their role in improving productivity, reducing environmental impact, and ensuring end-to-end supply chain transparency

- The escalating demand for sustainable dairy value chain market solutions is primarily fueled by rising global demand for low-carbon food production, increasing regulatory pressure on emissions reduction, growing consumer preference for ethically sourced dairy products, and rapid adoption of digital farming and supply chain traceability technologies

- North America dominated the sustainable dairy value chain market with the largest revenue share of approximately 39.8% in 2025, characterized by advanced dairy production infrastructure, strong adoption of sustainable farming practices, high investment in precision agriculture technologies, and the presence of major dairy processors and food companies driving sustainability initiatives across the value chain

- Asia-Pacific is expected to be the fastest growing region in the Sustainable Dairy Value Chain market during the forecast period due to increasing dairy consumption, rapid modernization of farming practices, rising environmental awareness, government support for sustainable agriculture, and growing investments in dairy infrastructure across India, China, and Southeast Asia

- The Carbon-Neutral Dairy Production segment held the largest market revenue share of 41.5% in 2025, driven by rising global pressure to reduce greenhouse gas emissions in agriculture

Report Scope and Sustainable Dairy Value Chain Market Segmentation

|

Attributes |

Sustainable Dairy Value Chain Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Nestlé S.A. (Switzerland) · Danone S.A. (France) · Lactalis Group (France) · Arla Foods amba (Denmark) · FrieslandCampina (Netherlands) · Fonterra Co-operative Group (New Zealand) · Saputo Inc. (Canada) · Royal DSM (Netherlands) · Kerry Group plc (Ireland) · Cargill, Incorporated (U.S.) · ADM (Archer Daniels Midland Company) (U.S.) · Groupe Bel (France) · Amul (Gujarat Co-operative Milk Marketing Federation) (India) · Dairy Farmers of America (U.S.) · Yili Group (China) · Mengniu Dairy (China) · Unilever PLC (U.K.) · Valio Ltd. (Finland) · Schreiber Foods (U.S.) · Savencia Fromage & Dairy (France) |

|

Market Opportunities |

· Adoption of Low-Carbon Dairy Production Technologies · Expansion of Digital Traceability and Premium Sustainable Dairy Products |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Sustainable Dairy Value Chain Market Trends

“Enhanced Efficiency Through Digital Traceability and Data-Driven Dairy Supply Chain Optimization”

- A significant and accelerating trend in the global Sustainable Dairy Value Chain market is the increasing adoption of digital traceability systems, IoT-enabled monitoring, and AI-powered analytics to improve transparency, reduce waste, and optimize dairy production and distribution efficiency. These technologies are strengthening sustainability and quality assurance across the entire dairy ecosystem

- Advanced data platforms are increasingly being used to track milk production from farm to processing units, ensuring quality control, animal health monitoring, and supply chain transparency

- For instance, companies such as Nestlé, Danone, and Arla Foods have implemented digital tracking systems to monitor sourcing practices and improve sustainability reporting

- The growing use of precision livestock farming tools, including sensor-based cattle monitoring and automated feeding systems, is improving milk yield efficiency while reducing environmental impact

- Another major trend is the integration of blockchain-based traceability solutions that allow retailers and consumers to verify product origin, ethical sourcing, and carbon footprint in real time

- In addition, sustainable packaging innovations and cold-chain optimization technologies are helping reduce food loss and environmental impact across dairy distribution networks

- This shift toward transparent, efficient, and environmentally responsible dairy production is fundamentally reshaping the global dairy value chain

Sustainable Dairy Value Chain Market Dynamics

Driver

“Rising Demand for Sustainable, Ethical, and High-Quality Dairy Products”

- Increasing consumer awareness regarding environmental sustainability, animal welfare, and food quality is a major driver for the Sustainable Dairy Value Chain market. Consumers are actively seeking responsibly sourced dairy products with lower environmental impact

- Growing global demand for protein-rich diets and natural dairy products is further accelerating market growth

- For instance, in regions such as Europe, North America, and Asia-Pacific, consumers are increasingly preferring sustainably certified milk, cheese, and yogurt products

- Government initiatives promoting sustainable agriculture, carbon reduction, and regenerative farming practices are also supporting industry transformation

- Furthermore, major dairy companies are investing in carbon-neutral farming, renewable energy usage, and waste reduction initiatives to meet sustainability targets

- Expanding retail demand for eco-labeled and traceable dairy products is expected to further strengthen market growth during the forecast period

Restraint/Challenge

“High Implementation Costs, Infrastructure Limitations, and Supply Chain Complexity”

- One of the major challenges restraining the Sustainable Dairy Value Chain market is the high cost of implementing advanced sustainability technologies, including digital monitoring systems, precision farming equipment, and cold-chain infrastructure upgrades

- Small and medium dairy farmers often face difficulties adopting sustainable technologies due to limited financial resources and lack of technical expertise

- For instance, many rural dairy producers in developing regions such as South Asia and parts of Africa struggle to implement automated milking systems or advanced traceability platforms due to high upfront investment requirements

- Fragmentation of dairy supply chains and lack of standardized sustainability measurement frameworks can also create operational inefficiencies and limit scalability

- In addition, dependency on traditional farming practices in several regions slows down digital transformation and sustainability adoption

- Overcoming these barriers through government subsidies, cooperative farming models, affordable technology solutions, and standardized sustainability regulations will be essential for long-term market growth

Sustainable Dairy Value Chain Market Scope

The market is segmented on the basis of product type, sustainability initiative, distribution channel, and end-user.

- By Product Type

On the basis of product type, the Sustainable Dairy Value Chain market is segmented into Milk & Liquid Dairy, Cheese, Butter & Spreads, Yogurt & Fermented Dairy, and Dairy Ingredients. The Milk & Liquid Dairy segment dominated the largest market revenue share of 38.6% in 2025, driven by its essential role in daily nutrition and widespread global consumption across households. Rising demand for sustainably sourced milk with reduced carbon footprint is strengthening adoption. Consumers are increasingly preferring traceable and ethically produced dairy products. Dairy companies are investing in low-emission processing and eco-friendly packaging to meet sustainability goals. North America leads due to strong dairy consumption and advanced supply chains. Europe follows with strict sustainability regulations and organic dairy demand. Asia-Pacific is expanding rapidly due to population growth and rising nutrition awareness. Improvements in cold-chain logistics are enhancing product availability. Retail expansion is further supporting sales growth. Sustainable branding is becoming a key purchase driver. Overall, milk and liquid dairy remain the dominant product type in the market.

The Yogurt & Fermented Dairy segment is expected to witness the fastest CAGR of 24.3% from 2026 to 2033, driven by rising consumer awareness of gut health and probiotic benefits. Fermented dairy products are increasingly viewed as functional foods supporting digestion and immunity. Growing preference for low-sugar and high-protein yogurt variants is accelerating demand. Sustainability-focused production methods, including reduced energy fermentation processes, are gaining traction. North America and Europe lead innovation in probiotic dairy products. Asia-Pacific is witnessing rapid growth due to traditional fermented dairy consumption habits. Plant-based fermentation hybrid products are also emerging in the market. Manufacturers are introducing recyclable packaging and carbon-neutral production processes. Premiumization and flavored yogurt innovations are expanding consumer appeal. Online retail channels are boosting product accessibility. Overall, yogurt and fermented dairy is projected to be the fastest-growing product segment.

- By Sustainability Initiative

On the basis of sustainability initiative, the Sustainable Dairy Value Chain market is segmented into Carbon-Neutral Dairy Production, Water-Efficient Farming, Ethical Animal Welfare Practices, and Waste Reduction & Circular Economy Solutions. The Carbon-Neutral Dairy Production segment held the largest market revenue share of 41.5% in 2025, driven by rising global pressure to reduce greenhouse gas emissions in agriculture. Dairy producers are increasingly adopting methane reduction technologies, renewable energy systems, and carbon offset programs. Governments and regulatory bodies are enforcing stricter emission targets across major dairy-producing regions. North America and Europe lead adoption due to strong environmental policies. Asia-Pacific is gradually increasing investments in sustainable dairy infrastructure. Large dairy corporations are committing to net-zero emissions targets. Consumer preference for eco-labeled dairy products is further supporting growth. Carbon tracking and certification systems are improving transparency. Investment in sustainable feed and livestock management is rising. Supply chain decarbonization initiatives are expanding rapidly. Overall, carbon-neutral production remains the dominant sustainability initiative segment.

The Waste Reduction & Circular Economy Solutions segment is expected to witness the fastest CAGR of 25.1% from 2026 to 2033, driven by increasing focus on reducing food waste and improving resource efficiency in dairy processing. Companies are adopting circular economy models such as byproduct reuse, packaging recycling, and energy recovery systems. Dairy waste is increasingly being converted into biogas, fertilizers, and animal feed. Governments are promoting zero-waste production policies across the food industry. North America and Europe are leading implementation of circular dairy systems. Asia-Pacific is rapidly adopting waste-to-energy dairy initiatives. Consumer awareness of sustainable packaging is also driving change. Technological advancements in waste tracking and processing are improving efficiency. Dairy processors are investing in closed-loop production systems. Corporate sustainability commitments are accelerating adoption. Overall, waste reduction and circular economy solutions are projected to be the fastest-growing initiative segment.

- By Distribution Channel

On the basis of distribution channel, the Sustainable Dairy Value Chain market is segmented into Supermarkets/Hypermarkets, Convenience Stores, Online Retail, and Specialty Stores. The Supermarkets/Hypermarkets segment accounted for the largest market revenue share of 44.2% in 2025, driven by strong consumer preference for one-stop shopping and wide product availability. Retail chains offer extensive ranges of sustainable dairy products with clear labeling and certifications. Bulk purchasing options and promotional pricing further support sales. North America and Europe dominate due to organized retail infrastructure. Asia-Pacific is expanding rapidly with increasing supermarket penetration. Consumers trust supermarkets for product authenticity and freshness assurance. Sustainable dairy branding is prominently displayed in retail shelves. Strong cold-chain logistics ensure product quality. Private-label sustainable dairy products are also increasing. Frequent in-store promotions boost demand. Overall, supermarkets and hypermarkets remain the dominant distribution channel.

The Online Retail segment is expected to witness the fastest CAGR of 23.9% from 2026 to 2033, driven by rapid digital adoption and increasing demand for doorstep delivery of dairy products. Consumers prefer online platforms for access to organic, sustainable, and niche dairy brands. Subscription-based milk delivery services are gaining strong popularity. E-commerce platforms provide transparency on sourcing and sustainability certifications. North America leads due to advanced digital grocery systems. Asia-Pacific is growing rapidly with rising smartphone usage and online grocery penetration. Europe is also expanding through sustainable food delivery platforms. Direct-to-consumer dairy brands are increasing online presence. Cold-chain logistics improvements are enhancing delivery efficiency. Digital marketing and personalized recommendations are boosting sales. Overall, online retail is projected to be the fastest-growing distribution channel.

- By End-User

On the basis of end-user, the Sustainable Dairy Value Chain market is segmented into Household Consumers, Food & Beverage Industry, HoReCa (Hotels, Restaurants & Catering), and Industrial Processors. The Household Consumers segment dominated the largest market revenue share of 46.8% in 2025, driven by strong daily consumption of dairy products across global households. Increasing awareness of sustainable food choices is influencing household purchasing behavior. Consumers are prioritizing ethically sourced and environmentally friendly dairy products. North America and Europe lead due to high per capita dairy consumption. Asia-Pacific shows strong growth due to rising income levels and dietary diversification. Retail availability and branding influence household demand significantly. Organic and sustainable milk products are particularly popular. Health and nutrition awareness is driving repeat purchases. Packaging innovations are improving household convenience. Government labeling standards are enhancing consumer trust. Overall, household consumers remain the dominant end-user segment.

The Food & Beverage Industry segment is expected to witness the fastest CAGR of 24.7% from 2026 to 2033, driven by increasing use of sustainable dairy ingredients in processed foods, bakery, confectionery, and beverages. Manufacturers are shifting toward sustainably sourced dairy inputs to meet ESG goals and consumer demand. Dairy ingredients such as whey protein, casein, and lactose are widely used in industrial food production. North America and Europe lead due to strong processed food industries. Asia-Pacific is expanding rapidly with growing packaged food demand. Companies are adopting certified sustainable dairy sourcing practices. Clean-label product demand is accelerating ingredient adoption. Food manufacturers are partnering with sustainable dairy suppliers. Innovation in high-protein and functional foods is boosting usage. Regulatory pressure on sustainable sourcing is increasing globally. Overall, the food & beverage industry is projected to be the fastest-growing end-user segment.

Sustainable Dairy Value Chain Market Regional Analysis

- North America dominated the sustainable dairy value chain market with the largest revenue share of approximately 39.8% in 2025, characterized by advanced dairy production infrastructure, strong adoption of sustainable farming practices, high investment in precision agriculture technologies, and the presence of major dairy processors and food companies driving sustainability initiatives across the value chain. The region has also witnessed increasing integration of data-driven dairy farming, carbon footprint reduction programs, and resource-efficient milk production systems

- Stakeholders across the region highly value sustainability, traceability, animal welfare standards, and efficiency improvements enabled through digital dairy management systems. Growing emphasis on reducing greenhouse gas emissions, optimizing feed utilization, and improving milk yield quality continues to strengthen market demand

- This widespread adoption is further supported by strong regulatory frameworks, high consumer demand for sustainable dairy products, advanced cold chain and processing infrastructure, and increasing collaboration between dairy cooperatives and agri-tech firms, establishing sustainable dairy practices as a core component of modern food supply chains across both residential and commercial dairy ecosystems

U.S. Sustainable Dairy Value Chain Market Insight

The U.S. sustainable dairy value chain market captured the largest revenue share in 2025 within North America, driven by rapid adoption of precision dairy farming, strong sustainability commitments from large dairy processors, and increasing investment in smart agriculture technologies. Producers are increasingly prioritizing methane reduction strategies, automated milking systems, and data-driven herd management to improve productivity and environmental performance. The growing integration of IoT-based farm monitoring systems, AI-powered livestock analytics, and supply chain traceability platforms is further propelling the market. Moreover, rising demand from food service companies and retail brands for sustainably sourced dairy products is significantly contributing to market expansion.

Europe Sustainable Dairy Value Chain Market Insight

The Europe sustainable dairy value chain market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent environmental regulations, strong sustainability mandates under EU agricultural policies, and rising demand for low-carbon food production. The region’s focus on organic farming, regenerative agriculture, and animal welfare standards is fostering adoption of sustainable dairy practices. European dairy producers are also investing in renewable energy integration, waste reduction technologies, and circular economy models. The region is experiencing significant growth in both large-scale commercial dairy farms and cooperative-based farming systems adopting sustainable value chain practices.

U.K. Sustainable Dairy Value Chain Market Insight

The U.K. sustainable dairy value chain market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing sustainability commitments from dairy producers and strong consumer preference for ethically sourced dairy products. In addition, government-backed environmental targets and carbon neutrality goals are encouraging adoption of greener dairy farming practices. The UK’s strong retail and food processing sector is also pushing suppliers to adopt transparent and traceable dairy supply chains, supporting market growth.

Germany Sustainable Dairy Value Chain Market Insight

The Germany sustainable dairy value chain market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing focus on climate-friendly agriculture, strong environmental policies, and high consumer demand for sustainable and organic dairy products. Germany’s well-developed agricultural infrastructure and emphasis on innovation promote the adoption of energy-efficient dairy farming systems and precision livestock management. Integration of renewable energy sources such as biogas and solar power into dairy farms is also becoming increasingly prevalent.

Asia-Pacific Sustainable Dairy Value Chain Market Insight

The Asia-Pacific sustainable dairy value chain market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing dairy consumption, rapid modernization of farming practices, rising environmental awareness, government support for sustainable agriculture, and growing investments in dairy infrastructure across India, China, Japan, and Southeast Asia. The region is witnessing strong transformation from traditional to technology-enabled dairy farming systems. Furthermore, expanding dairy cooperatives, rising demand for safe and high-quality milk products, and increasing adoption of cold chain logistics are accelerating market growth.

Japan Sustainable Dairy Value Chain Market Insight

The Japan sustainable dairy value chain market is gaining momentum due to the country’s advanced agricultural technologies, high quality standards, and focus on efficiency-driven dairy production. Japan emphasizes sustainable resource utilization, automation in dairy farming, and improved animal health management. The integration of smart monitoring systems and robotics in dairy operations is supporting productivity improvements. In addition, demand for premium, safe, and traceable dairy products is driving adoption of sustainable value chain practices.

China Sustainable Dairy Value Chain Market Insight

The China sustainable dairy value chain market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding dairy consumption, rapid urbanization, strong government support for agricultural modernization, and increasing focus on food safety and sustainability. China is investing heavily in large-scale dairy farms, smart farming technologies, and cold chain infrastructure to improve efficiency and reduce environmental impact. The presence of strong domestic dairy producers and rising demand for high-quality dairy products are key factors propelling market growth in China.

Sustainable Dairy Value Chain Market Share

The Sustainable Dairy Value Chain industry is primarily led by well-established companies, including:

- Nestlé S.A. (Switzerland)

- Danone S.A. (France)

- Lactalis Group (France)

- Arla Foods amba (Denmark)

- FrieslandCampina (Netherlands)

- Fonterra Co-operative Group (New Zealand)

- Saputo Inc. (Canada)

- Royal DSM (Netherlands)

- Kerry Group plc (Ireland)

- Cargill, Incorporated (U.S.)

- ADM (Archer Daniels Midland Company) (U.S.)

- Groupe Bel (France)

- Amul (Gujarat Co-operative Milk Marketing Federation) (India)

- Dairy Farmers of America (U.S.)

- Yili Group (China)

- Mengniu Dairy (China)

- Unilever PLC (U.K.)

- Valio Ltd. (Finland)

- Schreiber Foods (U.S.)

- Savencia Fromage & Dairy (France)

Latest Developments in Global Sustainable Dairy Value Chain Market

- In August 2021, Danone strengthened its regenerative agriculture strategy by expanding farmer-level programs aimed at reducing greenhouse gas emissions from dairy supply chains. The initiative focused on improving soil health, feed efficiency, and livestock management practices as part of Danone’s broader climate commitments, highlighting early corporate leadership in sustainable dairy transformation

- In August 2022, Arla Foods launched its Climate Roadmap – Towards Carbon Net Zero Dairy, after receiving Science Based Targets initiative (SBTi) validation for its emissions reduction targets. The roadmap outlined a 30% reduction in scope 3 emissions per kg of milk and whey and introduced value-chain-wide decarbonization strategies across farms, processing, and logistics

- In December 2023, the Dairy Methane Action Alliance was launched by leading global food companies including Danone, Nestlé, Kraft Heinz, and Starbucks to measure, disclose, and reduce methane emissions across dairy supply chains. The initiative represented one of the first coordinated industry efforts targeting methane, a major contributor to agricultural greenhouse gas emissions

- In November 2024, Arla Foods initiated large-scale field trials of methane-reducing feed additives (Bovaer) in partnership with UK retailers such as Tesco, Morrisons, and Aldi. The initiative aimed to reduce enteric methane emissions from dairy cattle by approximately 27%, marking a significant on-farm intervention in sustainable dairy production

- In July 2025, the global dairy industry launched a new unified Dairy Roadmap coalition involving processors, retailers, and foodservice companies including Arla Foods, Lactalis, Müller, Tesco, Sainsbury’s, McDonald’s, and Sysco. The initiative introduced a shared governance structure to accelerate progress on climate action, biodiversity protection, water efficiency, and sustainable dairy production across the entire value chain

- In October 2025, Nestlé withdrew from the Dairy Methane Action Alliance while reaffirming its commitment to net-zero emissions by 2050 and ongoing methane reduction efforts across its dairy supply chain. The move highlighted both progress and challenges in global coordinated methane reduction efforts within sustainable dairy systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Sustainable Dairy Value Chain Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Sustainable Dairy Value Chain Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Sustainable Dairy Value Chain Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.