Global Sustainable Packaging For Food Market

Market Size in USD Billion

USD

75.00 Billion

USD

140.89 Billion

2025

2033

USD

75.00 Billion

USD

140.89 Billion

2025

2033

| 2026 - 2033 | |

| USD 75.00 Billion | |

| USD 140.89 Billion | |

| % | |

|

Sustainable Packaging for Food Market Overview

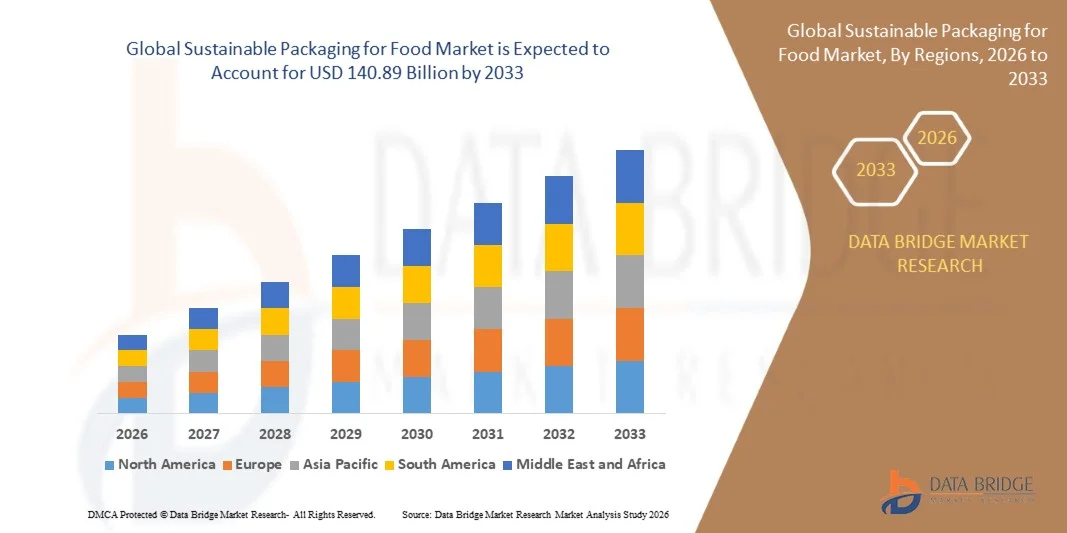

As per Data Bridge Market Research analysis the Sustainable Packaging for Food Market was valued at USD 75.00 billion in 2025 and is projected to reach USD 140.89 billion by 2033, growing at a CAGR of 8.20% from 2026 to 2033. The market is experiencing strong growth driven by increasing regulatory restrictions on single-use plastics, rising consumer preference for recyclable and compostable food packaging, and expanding adoption of paper-based, bio-based, reusable, and recycled-content packaging solutions across food retail, foodservice, and e-commerce channels.

The growing need to reduce food waste and packaging waste is encouraging food manufacturers, retailers, and quick-service restaurants to invest in packaging solutions that improve product protection while lowering environmental impact. Global food waste reached approximately 1.05 billion tonnes in 2022, while food loss and waste account for an estimated 8–10% of global greenhouse gas emissions, strengthening the need for durable packaging that extends shelf life and supports responsible end-of-life management.

Sustainable Packaging for Food Market Size & Forecast

- Global Market Value (2025): USD 75.00 Billion

- Expected Market Value (2033): USD 140.89 Billion

- Forecast CAGR (2026–2033): 8.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the sustainable packaging for food market with the largest revenue share of 36.4% in 2025, supported by strict packaging waste regulations, high consumer awareness, well-developed recycling infrastructure, and increasing sustainability commitments among food manufacturers, retailers, and quick service restaurants.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 9.6% from 2026 to 2033. Growth is driven by rapid urbanization, rising disposable incomes, increasing packaged food consumption, expanding food delivery and e-commerce platforms, and government initiatives focused on reducing plastic pollution across countries such as China, India, Japan, and South Korea.

- The flexible packaging segment held the largest market revenue share of approximately 38.6% in 2025 driven by its lightweight structure, lower material consumption, extended shelf-life capabilities, and growing adoption across snacks, frozen foods, bakery products, and ready-to-eat meals. Flexible formats such as recyclable films, stand-up pouches, wraps, and paper-based bags are increasingly preferred by food manufacturers due to reduced transportation costs and lower packaging waste generation.

- The pouches segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by rising demand for resealable, portion-controlled, and lightweight packaging solutions across snacks, pet food, sauces, baby food, and on-the-go meal categories. Growing use of mono-material recyclable pouches and compostable pouch structures is further supporting segment expansion.

- The paper and paperboard segment held the largest market revenue share of approximately 34.8% in 2025 driven by high recyclability, renewable feedstock availability, and expanding adoption of corrugated boxes, folding cartons, molded fiber trays, and paper-based food wraps. Paperboard continues to account for a significant share of global packaging material consumption, highlighting its strong position across food retail, food service, and e-commerce packaging applications.

- The bagasse, bamboo, starch-based materials, PLA, and PHA segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by rising adoption of compostable food service containers, disposable cutlery, trays, takeaway boxes, and fresh food packaging. Increasing production capacity for bioplastics and plant-based packaging materials is improving material availability for food packaging manufacturers.

- The recyclable packaging segment held the largest market revenue share of approximately 42.1% in 2025 driven by growing regulatory focus on circular economy practices, increasing recycled-content targets, and strong consumer preference for packaging that can enter existing waste collection systems. Food manufacturers are increasingly shifting toward recyclable paperboard cartons, recycled plastic bottles, mono-material pouches, and recyclable metal containers to reduce landfill waste.

- The compostable packaging segment is projected to register the fastest growth at a CAGR of 10.6% from 2026 to 2033, driven by rising adoption of certified compostable trays, cups, pouches, and food containers across takeaway meals, organic foods, and food delivery services. However, commercial composting infrastructure availability remains an important factor influencing large-scale adoption across developing economies.

- The meat, poultry and seafood segment held the largest market revenue share of approximately 23.7% in 2025 driven by high demand for protective, leak-resistant, and temperature-controlled packaging solutions. Sustainable vacuum packs, recyclable trays, paper-based absorbent pads, and modified atmosphere packaging formats are increasingly being adopted to preserve freshness and meet food safety requirements.

- The beverages segment is projected to register the fastest growth at a CAGR from 2026 to 2033, supported by strong demand for recycled plastic bottles, aluminum cans, glass bottles, paper cartons, and refillable packaging systems. Beverage companies are increasingly investing in recycled content, lightweighting, and returnable bottle models to meet packaging sustainability commitments and reduce virgin material consumption.

- The food manufacturers segment held the largest market revenue share of approximately 39.5% in 2025 driven by large-scale procurement of sustainable cartons, flexible films, trays, bottles, and labels for packaged foods, dairy products, beverages, frozen foods, and snack products. Food manufacturers are increasingly redesigning packaging structures to improve recyclability, reduce material use, and comply with evolving extended producer responsibility requirements.

- The quick service restaurants segment is projected to register the fastest growth at a CAGR of 10.1% from 2026 to 2033, driven by increasing restrictions on single-use plastic food service products and rising consumer demand for compostable cups, bagasse containers, paper straws, recyclable wraps, and molded fiber takeaway packaging.

Report Scope and Sustainable Packaging for Food Market Segmentation

|

Attributes |

Sustainable Packaging for Food Key Market Insights |

|

Segments Covered |

• By Packaging Type: Rigid Packaging, Flexible Packaging, Semi-Rigid Packaging, Pouches, Trays, Cartons and Boxes, Wraps, Bags, Bottles, and Others • By Material Type: Paper and Paperboard, Plastic, Metal, Glass, Wood, Bagasse, Bamboo, Starch-Based Materials, Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), and Others • By Process: Recyclable Packaging, Reusable Packaging, Biodegradable Packaging, Compostable Packaging, Edible Packaging, and Refillable Packaging • By Application: Fruits and Vegetables, Meat, Poultry and Seafood, Bakery and Confectionery, Dairy Products, Frozen Foods, Ready-To-Eat Meals, Snacks, Beverages, and Others • By End User: Food Manufacturers, Food Service Providers, Retail and E-Commerce, Quick Service Restaurants, Institutional Catering, and Others |

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Amcor plc (Switzerland) |

|

Market Opportunities |

• Expansion Of Reusable And Refillable Food Packaging Systems • Development Of High-Barrier Bio-Based And Compostable Packaging Materials |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Sustainable Packaging for Food Market Trends

Trend: Growth In Waste Heat Recovery And Advanced Solid-State Cooling Applications

Increasing demand for energy-efficient, compact, and environmentally sustainable thermal management technologies across automotive, industrial, electronics, aerospace, and defense sectors is supporting the adoption of thermoelectric modules. Conventional compressor-based cooling systems consume substantial energy, require periodic maintenance, and use refrigerants that may create environmental compliance concerns, encouraging manufacturers to evaluate solid-state alternatives with lower mechanical complexity and silent operation.

In modern electric vehicles, manufacturers are assessing thermoelectric systems for localized battery thermal management, seat cooling, and cabin comfort applications to improve temperature uniformity while reducing noise and vibration. For instance, thermoelectric modules can provide targeted cooling for battery cells and electronic control units where conventional liquid-cooling loops may be difficult to integrate. Research on advanced battery thermal management systems has demonstrated that improved thermal regulation can reduce peak cell temperatures by more than 10°C under demanding operating conditions, supporting battery safety, charging performance, and lifecycle optimization.

In industrial systems, thermoelectric generators are being deployed to convert low-grade waste heat from furnaces, exhaust streams, pipelines, and manufacturing equipment into usable electrical energy. For instance, bismuth telluride-based modules have demonstrated conversion efficiencies of approximately 8% across operating temperatures between 25°C and 250°C, highlighting their potential for recovering energy from medium-temperature industrial heat sources. These systems are particularly relevant for continuous-process industries seeking to reduce thermal losses without installing large-scale rotating equipment.

The rapid expansion of compact consumer electronics, data centers, and high-performance computing infrastructure is also increasing demand for silent and highly precise cooling systems capable of operating in restricted spaces. Thermoelectric modules are being considered for temperature-sensitive sensors, optical components, laser systems, semiconductor testing equipment, and edge computing devices where stable temperature control is more important than large-scale cooling capacity.

Space and defense sectors continue to validate the long-term reliability of thermoelectric technology in extreme environments. For instance, NASA uses radioisotope thermoelectric generators to convert heat from plutonium-238 decay into electricity for deep-space missions. NASA’s Voyager spacecraft have operated for more than 47 years using radioisotope power systems, while Multi-Mission Radioisotope Thermoelectric Generators provide power and heat for the Curiosity and Perseverance Mars rovers.

Global Thermoelectric Modules Market Dynamics

Key Market Driver: Rising Adoption Of Energy Efficient Waste Heat Recovery Systems

Industries worldwide are facing increasing regulatory and economic pressure to reduce energy wastage, lower carbon emissions, and improve operational efficiency. Large quantities of heat generated from industrial machinery, automotive engines, data centers, and manufacturing processes are typically released into the environment without productive use, creating demand for technologies capable of converting excess thermal energy into usable electricity.

Industries such as automotive, oil and gas, metals, cement, chemicals, and manufacturing are increasingly evaluating thermoelectric generators to capture waste heat from engines, exhaust systems, furnaces, and industrial equipment. For instance, thermoelectric systems can be installed around exhaust pipes, heat exchangers, and furnace outlets to generate supplementary power for sensors, monitoring devices, and low-power control systems without requiring moving components or additional fuel consumption.

Automotive OEMs are also testing thermoelectric energy recovery systems in hybrid and electric vehicle architectures to support energy-efficiency targets and reduce auxiliary power requirements. Thermoelectric technology is particularly relevant for localized energy harvesting applications where conventional waste heat recovery equipment may be too large, complex, or costly to deploy. In addition, the absence of moving parts supports long operating life in high-vibration automotive and industrial environments.

Similarly, data centers and semiconductor facilities are exploring advanced thermal management technologies to manage rising heat loads associated with AI-driven computing infrastructure. Thermoelectric cooling can support highly localized temperature regulation for processors, optical transceivers, sensors, and test equipment, reducing dependence on bulky cooling arrangements in space-constrained installations. Recent electric vehicle thermal management research using real driving and weather data reported reductions of up to 15% in HVAC energy use through integrated thermal control optimization, highlighting the importance of efficient thermal management in next-generation mobility systems.

Key Restraint/Challenge: Low Conversion Efficiency And High Material Costs

Currently available thermoelectric materials are unable to deliver energy conversion efficiencies comparable to conventional cooling and power generation technologies in large-scale applications. The performance limitations of commonly used materials, such as bismuth telluride, reduce the ability of thermoelectric modules to generate high electrical output from low-temperature heat sources, limiting their suitability for high-power industrial deployment.

Commercial and research-grade bismuth telluride modules typically demonstrate efficiency levels below 10% under practical operating conditions. For instance, an advanced bismuth telluride thermoelectric module demonstrated an 8% conversion efficiency across a 25°C to 250°C operating range, while another 2025 material benchmark estimated approximately 3.58% efficiency at a temperature difference of 120 K. These figures demonstrate progress in material engineering but also indicate the gap between thermoelectric generation and conventional high-capacity energy conversion technologies.

In addition, expensive raw materials, specialized semiconductor fabrication processes, metallization requirements, and complex module assembly increase overall system costs. Bismuth, tellurium, antimony, and other advanced thermoelectric materials can face supply-chain constraints and price volatility, creating affordability concerns for small-scale industries and cost-sensitive markets.

Limited scalability for high-energy-output applications further restricts commercialization in emerging economies where return on investment remains a key purchasing consideration. Manufacturers must also address module degradation, thermal cycling reliability, contact resistance, and system-level heat-exchanger design to achieve consistent performance across long-duration industrial operations.

Key Market Opportunity: Integration In Electric Vehicles And Next-Generation Electronics

Modern electric vehicles, wearable devices, AI processors, compact electronic systems, and connected sensors increasingly require lightweight, compact, and highly precise thermal management technologies. Conventional cooling systems can be bulky, noisy, and difficult to integrate into miniaturized electronic architectures, creating opportunities for solid-state cooling solutions with low maintenance requirements and rapid temperature response.

Automotive companies are increasingly exploring thermoelectric systems for seat cooling, battery thermal regulation, sensor temperature stabilization, and exhaust energy recovery. For instance, thermoelectric modules can be integrated into localized battery pack zones to manage thermal gradients during rapid charging and high-load driving conditions. Improved battery temperature uniformity can support charging efficiency, cell durability, and vehicle safety, particularly in high-temperature operating environments.

In consumer electronics, rising device miniaturization and increasing thermal density are accelerating demand for silent and compact cooling systems for smartphones, wearable devices, imaging sensors, optical modules, and IoT equipment. Thermoelectric modules are especially suitable for applications requiring precise temperature stability, such as infrared detectors, laser diodes, medical diagnostic devices, and semiconductor testing systems.

In addition, advancements in nanostructured thermoelectric materials, segmented module designs, and hybrid cooling architectures are improving performance potential across aerospace, defense, and AI-powered computing infrastructure. NASA’s continued use of radioisotope thermoelectric generators in missions such as Voyager, Curiosity, and Perseverance demonstrates the technology’s value in applications where reliability, long operating life, and maintenance-free performance are critical.

Sustainable Packaging for Food Market Scope

The market is segmented on the basis of packaging type, material type, process, application, and end user.

• By Packaging Type

On the basis of packaging type, the Sustainable Packaging for Food Market is segmented into rigid packaging, flexible packaging, semi-rigid packaging, pouches, trays, cartons and boxes, wraps, bags, bottles, and others. The flexible packaging segment held the largest market revenue share of approximately 38.6% in 2025 driven by its lightweight structure, lower material consumption, extended shelf-life capabilities, and growing adoption across snacks, frozen foods, bakery products, and ready-to-eat meals. Flexible formats such as recyclable films, stand-up pouches, wraps, and paper-based bags are increasingly preferred by food manufacturers due to reduced transportation costs and lower packaging waste generation.

The pouches segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by rising demand for resealable, portion-controlled, and lightweight packaging solutions across snacks, pet food, sauces, baby food, and on-the-go meal categories. Growing use of mono-material recyclable pouches and compostable pouch structures is further supporting segment expansion.

• By Material Type

On the basis of material type, the Sustainable Packaging for Food Market is segmented into paper and paperboard, plastic, metal, glass, wood, bagasse, bamboo, starch-based materials, polylactic acid (PLA), polyhydroxyalkanoates (PHA), and others. The paper and paperboard segment held the largest market revenue share of approximately 34.8% in 2025 driven by high recyclability, renewable feedstock availability, and expanding adoption of corrugated boxes, folding cartons, molded fiber trays, and paper-based food wraps. Paperboard continues to account for a significant share of global packaging material consumption, highlighting its strong position across food retail, food service, and e-commerce packaging applications.

The bagasse, bamboo, starch-based materials, PLA, and PHA segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by rising adoption of compostable food service containers, disposable cutlery, trays, takeaway boxes, and fresh food packaging. Increasing production capacity for bioplastics and plant-based packaging materials is improving material availability for food packaging manufacturers.

• By Process

On the basis of process, the Sustainable Packaging for Food Market is segmented into recyclable packaging, reusable packaging, biodegradable packaging, compostable packaging, edible packaging, and refillable packaging. The recyclable packaging segment held the largest market revenue share of approximately 42.1% in 2025 driven by growing regulatory focus on circular economy practices, increasing recycled-content targets, and strong consumer preference for packaging that can enter existing waste collection systems. Food manufacturers are increasingly shifting toward recyclable paperboard cartons, recycled plastic bottles, mono-material pouches, and recyclable metal containers to reduce landfill waste.

The compostable packaging segment is projected to register the fastest growth at a CAGR of 10.6% from 2026 to 2033, driven by rising adoption of certified compostable trays, cups, pouches, and food containers across takeaway meals, organic foods, and food delivery services. However, commercial composting infrastructure availability remains an important factor influencing large-scale adoption across developing economies.

• By Application

On the basis of application, the Sustainable Packaging for Food Market is segmented into fruits and vegetables, meat, poultry and seafood, bakery and confectionery, dairy products, frozen foods, ready-to-eat meals, snacks, beverages, and others. The meat, poultry and seafood segment held the largest market revenue share of approximately 23.7% in 2025 driven by high demand for protective, leak-resistant, and temperature-controlled packaging solutions. Sustainable vacuum packs, recyclable trays, paper-based absorbent pads, and modified atmosphere packaging formats are increasingly being adopted to preserve freshness and meet food safety requirements.

The beverages segment is projected to register the fastest growth at a CAGR from 2026 to 2033, supported by strong demand for recycled plastic bottles, aluminum cans, glass bottles, paper cartons, and refillable packaging systems. Beverage companies are increasingly investing in recycled content, lightweighting, and returnable bottle models to meet packaging sustainability commitments and reduce virgin material consumption.

• By End User

On the basis of end user, the Sustainable Packaging for Food Market is segmented into food manufacturers, food service providers, retail and e-commerce, quick service restaurants, institutional catering, and others. The food manufacturers segment held the largest market revenue share of approximately 39.5% in 2025 driven by large-scale procurement of sustainable cartons, flexible films, trays, bottles, and labels for packaged foods, dairy products, beverages, frozen foods, and snack products. Food manufacturers are increasingly redesigning packaging structures to improve recyclability, reduce material use, and comply with evolving extended producer responsibility requirements.

The quick service restaurants segment is projected to register the fastest growth at a CAGR of 10.1% from 2026 to 2033, driven by increasing restrictions on single-use plastic food service products and rising consumer demand for compostable cups, bagasse containers, paper straws, recyclable wraps, and molded fiber takeaway packaging.

Sustainable Packaging for Food Market Regional Analysis

North America Sustainable Packaging For Food Market Insight

North America dominated the sustainable packaging for food market with the largest revenue share in 2025, supported by stringent regulations on single-use plastics, high consumer awareness regarding packaging waste, and increasing sustainability commitments among food and beverage manufacturers. Food producers, retailers, and food service providers across the region are increasingly adopting recyclable paperboard cartons, recycled plastic bottles, compostable food containers, and fiber-based packaging solutions to reduce environmental impact. The widespread availability of recycling infrastructure, high disposable incomes, and growing demand for convenient packaged foods are further supporting the transition toward sustainable food packaging across residential, commercial, and institutional consumption channels.

U.S. Sustainable Packaging For Food Market Insight

The U.S. sustainable packaging for food market captured the largest revenue share in 2025 within North America, fueled by rising demand for recyclable, reusable, and compostable packaging across packaged foods, beverages, food delivery, and quick service restaurant applications. Food manufacturers are increasingly redesigning packaging formats to incorporate recycled content, reduce plastic usage, and improve recyclability in response to evolving extended producer responsibility requirements. The growing preference for online grocery shopping, meal-kit subscriptions, and direct-to-consumer food brands is further increasing demand for lightweight, protective, and sustainable packaging formats such as corrugated boxes, paper mailers, molded fiber trays, and recyclable pouches.

Europe Sustainable Packaging For Food Market Insight

The Europe sustainable packaging for food market is expected to witness a significant growth rate from 2026 to 2033, primarily driven by strict packaging waste regulations, circular economy targets, and rising adoption of recyclable and compostable food packaging materials. The region is witnessing increasing use of paper and paperboard, recycled plastic, aluminum, glass, bagasse, and plant-based packaging solutions across food retail, food service, and beverage applications. European food manufacturers are also investing in mono-material flexible packaging, refillable containers, and fiber-based alternatives to conventional plastic packaging to comply with sustainability targets and changing consumer preferences.

U.K. Sustainable Packaging For Food Market Insight

The U.K. sustainable packaging for food market is expected to witness a strong growth rate from 2026 to 2033, driven by increasing restrictions on avoidable plastic waste, expanding demand for environmentally responsible food packaging, and rising adoption of online food delivery services. Food retailers, quick service restaurants, and packaged food manufacturers are increasingly using recyclable cartons, compostable takeaway containers, paper-based wraps, and recycled-content plastic packaging. The U.K.’s well-developed retail and e-commerce infrastructure, combined with strong consumer awareness of food packaging waste, is expected to continue supporting the adoption of sustainable packaging solutions across food and beverage categories.

Germany Sustainable Packaging For Food Market Insight

The Germany sustainable packaging for food market is expected to witness a strong growth rate from 2026 to 2033, fueled by high recycling awareness, advanced waste management infrastructure, and increasing demand for environmentally responsible food and beverage packaging. Germany’s deposit return systems and focus on packaging recovery are supporting the adoption of reusable bottles, recyclable metal cans, glass containers, and recycled plastic packaging formats. Food manufacturers are increasingly investing in lightweight packaging designs, paper-based alternatives, and mono-material flexible packaging to reduce material consumption and improve circularity across retail and food service supply chains.

Asia-Pacific Sustainable Packaging For Food Market Insight

The Asia-Pacific sustainable packaging for food market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, rising disposable incomes, increasing packaged food consumption, and growing government initiatives to reduce plastic pollution. Countries across the region are increasingly adopting sustainable packaging materials such as paperboard, bagasse, bamboo, recycled plastic, starch-based materials, and compostable bioplastics. The rapid expansion of food delivery platforms, organized retail, e-commerce grocery services, and quick service restaurants is further increasing demand for affordable, lightweight, and sustainable food packaging solutions.

Japan Sustainable Packaging For Food Market Insight

The Japan sustainable packaging for food market is expected to witness a strong growth rate from 2026 to 2033 due to high consumer demand for hygienic, convenient, and high-quality food packaging solutions. The Japanese market places significant emphasis on food safety, product freshness, and packaging functionality, supporting the adoption of recyclable trays, lightweight flexible packaging, paper-based cartons, and reusable containers. The country’s advanced recycling systems and growing focus on reducing food packaging waste are encouraging manufacturers to develop packaging formats that use less material while maintaining strong barrier performance and product protection.

China Sustainable Packaging For Food Market Insight

The China sustainable packaging for food market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, expanding middle-class consumption, and strong growth in packaged foods, food delivery, and e-commerce retail. China is one of the largest markets for food and beverage packaging, and sustainable formats are increasingly being adopted across snacks, beverages, dairy products, ready-to-eat meals, and fresh food applications. Government initiatives to reduce plastic waste, growing availability of paper-based and biodegradable packaging materials, and the presence of large domestic packaging manufacturers are key factors supporting market expansion in China.

Sustainable Packaging for Food Market Share

The Sustainable Packaging for Food industry is primarily led by well-established companies, including:

• Amcor plc (Switzerland)

• International Paper Company (U.S.)

• Smurfit WestRock plc (Ireland)

• Mondi plc (U.K.)

• Tetra Pak International S.A. (Switzerland)

• Huhtamäki Oyj (Finland)

• DS Smith plc (U.K.)

• Sealed Air Corporation (U.S.)

• Berry Global Group, Inc. (U.S.)

• Crown Holdings, Inc. (U.S.)

• Ball Corporation (U.S.)

• Stora Enso Oyj (Finland)

• Ardagh Group S.A. (Luxembourg)

• Sonoco Products Company (U.S.)

• Coveris Holdings S.A. (Austria)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Sustainable Packaging For Food Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Sustainable Packaging For Food Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Sustainable Packaging For Food Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.