Global Sustainable Pharmaceutical Packaging Market

Market Size in USD Billion

USD

111.30 Billion

USD

262.09 Billion

2025

2033

USD

111.30 Billion

USD

262.09 Billion

2025

2033

| 2026 - 2033 | |

| USD 111.30 Billion | |

| USD 262.09 Billion | |

| % | |

|

Sustainable Pharmaceutical Packaging Market Overview

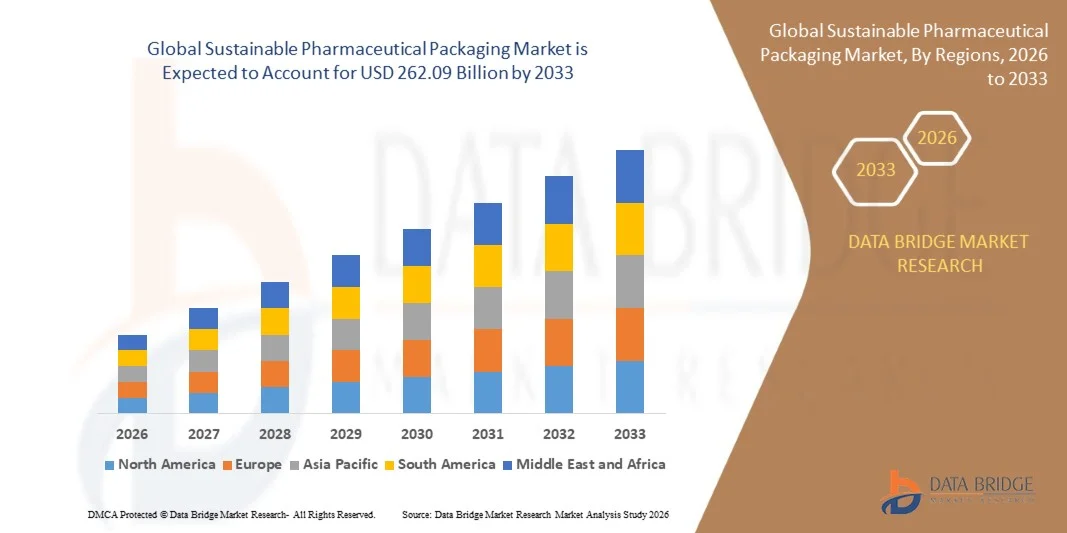

As per Data Bridge Market Research analysis the Sustainable Pharmaceutical Packaging Market was valued at USD 111.30 billion in 2025 and is projected to reach USD 262.09 billion by 2033, growing at a CAGR of 11.30% from 2026 to 2033. The market is experiencing strong growth driven by increasing environmental regulations, rising pharmaceutical industry emphasis on reducing packaging waste, and growing adoption of recyclable, biodegradable, and renewable-material-based packaging solutions.

The expansion of pharmaceutical production, biologics, and specialty drug distribution is increasing the need for high-performance packaging that protects product integrity while minimizing environmental impact. Pharmaceutical manufacturers are increasingly adopting recyclable blister packs, paper-based secondary packaging, bio-based polymers, lightweight containers, and mono-material solutions to meet sustainability targets and regulatory requirements. In addition, growing consumer awareness regarding eco-friendly healthcare products and corporate commitments toward circular economy practices are accelerating investments in sustainable pharmaceutical packaging across developed and emerging markets.

Key Market Trends & Insights

- North America dominated the sustainable pharmaceutical packaging market with the largest revenue share of 38.6% in 2025, supported by a strong pharmaceutical manufacturing base, expanding biologics and specialty drug production, advanced recycling infrastructure, and increasing adoption of recyclable blister packs, recycled-content bottles, and paper-based secondary packaging.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 13.2% from 2026 to 2033. Growth is driven by expanding pharmaceutical production, rising healthcare expenditure, increasing generic medicine consumption, government initiatives to reduce plastic waste, and growing adoption of cost-effective recyclable and biodegradable packaging materials.

- The Biodegradable Plastics segment held the largest market revenue share of approximately 36.6% in 2025, driven by the broad use of recyclable polymers, recycled-content resins, and bio-based plastic formats in bottles, blister packs, closures, pouches, and syringes. These materials are preferred due to their lightweight properties, cost efficiency, design flexibility, and ability to meet pharmaceutical barrier and safety requirements.

- The Glass segment is projected to register the fastest growth at a CAGR of 12.7% from 2026 to 2033, driven by rising demand for recyclable and chemically inert packaging for injectable drugs, biologics, vaccines, and high-value specialty medicines. Glass bottles, vials, ampoules, and cartridges are increasingly preferred for products requiring high protection against moisture, oxygen, and chemical interaction.

- The Blisters segment held the largest market revenue share of approximately 42.0% in 2025, driven by extensive use in tablets, capsules, and unit-dose pharmaceutical products. Sustainable blister packs are increasingly being developed using recyclable polyethylene, mono-material films, and lower-impact lidding structures to reduce dependence on conventional PVC and aluminum combinations.

- The Syringes segment is projected to register the fastest growth from 2026 to 2033, driven by increasing demand for prefilled syringes, biologics, injectable therapies, and self-administration drug-delivery systems. Rising adoption of recyclable plastics, lightweight materials, and reduced-material syringe components is supporting sustainable packaging innovation in this segment.

- The Pharmaceuticals segment held the largest market revenue share of approximately 49.5% in 2025, driven by high-volume production of prescription medicines, generic drugs, over-the-counter products, and oral solid-dose formulations. Pharmaceutical manufacturers are increasingly adopting recycled paper cartons, recyclable blister packs, lightweight bottles, and lower-carbon packaging formats to meet sustainability targets and regulatory requirements.

- The Biotech segment is projected to register the fastest growth from 2026 to 2033, driven by the expanding production of biologics, cell and gene therapies, vaccines, and temperature-sensitive injectable drugs. These products require high-performance, traceable, and protective packaging, creating opportunities for sustainable glass, recyclable polymer, and smart packaging solutions.

- The Sustainability Compliance segment held the largest market revenue share of approximately 63.1% in 2025, driven by increasing demand for recyclable, reusable, and biodegradable packaging formats that support circular economy targets. Recyclable packaging formats, including glass bottles, aluminum containers, recycled paper cartons, and recyclable plastic packaging, are being increasingly adopted across pharmaceutical supply chains.

- The Smart Packaging segment is projected to register the fastest growth from 2026 to 2033, driven by increasing adoption of QR codes, RFID tags, near-field communication labels, and serialization technologies. These features support product authentication, patient adherence, supply-chain visibility, anti-counterfeiting compliance, and improved disposal guidance for sustainable packaging materials.

- The Wholesale segment held the largest market revenue share of approximately 39.4% in 2025, driven by the large-scale movement of pharmaceutical products from manufacturers to distributors, hospitals, pharmacies, and healthcare institutions. Sustainable wholesale packaging demand is supported by the adoption of recyclable corrugated cartons, reusable transit packaging, lightweight shipping materials, and optimized secondary packaging formats.

- The Online segment is projected to register the fastest growth from 2026 to 2033, driven by rising e-pharmacy adoption, direct-to-patient medicine delivery, and growing demand for protective yet lightweight shipping packaging. Online pharmaceutical distribution is increasing the use of recyclable mailers, paper-based cushioning, temperature-controlled sustainable packaging, and digitally enabled labels to improve delivery efficiency and reduce packaging waste.

Market Size & Forecast

- Global Market Value (2025): USD 111.30 Billion

- Expected Market Value (2033): USD 262.09 Billion

- Forecast CAGR (2026–2033): 11.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Sustainable Pharmaceutical Packaging Market Segmentation

|

Attributes |

Sustainable Pharmaceutical Packaging Key Market Insights |

|

Segments Covered |

· By Packaging Material: Recycled Paper, Biodegradable Plastics, Glass, Metal, and Plant-based Materials · By Form of Packaging: Bottles, Blisters, Pouches, Cartons, and Syringes · By End User Industry: Pharmaceuticals, Biotech, Healthcare, and Veterinary · By Functional Features: Child Resistance, Tamper Evidence, Sustainability Compliance, and Smart Packaging · By Distribution Channel: Online, Retail Pharmacy, Hospital Pharmacy, and Wholesale |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Amcor (AU) |

|

Market Opportunities |

• Rising Adoption Of Recyclable And Bio-Based Pharmaceutical Packaging Materials • Growing Demand For Lightweight, Mono-Material, And Circular Packaging Solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Sustainable Pharmaceutical Packaging Market Trends

Trend: Growing Adoption Of Circular Materials And Recycle-Ready Pharmaceutical Packaging

The sustainable pharmaceutical packaging market is witnessing growing adoption of circular materials, recycle-ready formats, and lightweight packaging designs as pharmaceutical manufacturers seek to reduce packaging-related emissions and material waste without compromising product safety, sterility, and shelf life. Conventional pharmaceutical packaging often uses complex multilayer structures containing PVC, aluminum, and mixed polymers, which provide strong barrier protection but are difficult to recycle through conventional waste-management systems. This is encouraging packaging converters and drug manufacturers to develop mono-material blister packs, paper-based secondary cartons, bio-based polymers, and recyclable flexible laminates.

In pharmaceutical blister packaging, companies are increasingly replacing PVC-based structures with polyethylene and polyolefin-based alternatives. For instance, Amcor’s AmSky recyclable blister system uses polyethylene-based thermoform and lidding films instead of PVC and has been independently assessed to provide up to a 70% lower carbon footprint than conventional blister packaging alternatives. The system is designed to retain child-resistant and senior-friendly functionality while improving recyclability, demonstrating how sustainable formats are being adapted for highly regulated pharmaceutical applications.

The trend is also accelerating in pharmaceutical sachets, stick packs, and unit-dose formats, where packaging suppliers are developing recycle-ready high-barrier laminates that can run on existing filling equipment. For instance, Amcor’s high-shield pharmaceutical laminate portfolio offers polyolefin and paper-based alternatives designed for recycling in relevant material streams, while maintaining moisture-barrier performance of approximately 0.1–0.2 g/m² per day. Such developments are enabling pharmaceutical companies to reduce dependence on difficult-to-recycle PET/aluminum/polyethylene structures without major changes to production lines.

Growing regulatory pressure is further strengthening the shift toward circular pharmaceutical packaging. The European Union’s Packaging and Packaging Waste Regulation entered into force in February 2025 and will generally apply from August 2026, establishing requirements related to packaging composition, recyclability, and waste prevention across products placed on the EU market. In response, packaging suppliers are increasing investments in material traceability, recyclability testing, recycled-content integration, and lower-carbon packaging development.

Sustainable Pharmaceutical Packaging Market Dynamics

Key Market Driver: Rising Regulatory Pressure And Corporate Commitments To Reduce Packaging Waste

Pharmaceutical manufacturers are facing increasing regulatory, environmental, and corporate sustainability pressure to reduce the use of virgin plastics, lower packaging waste, and improve material circularity across medicine supply chains. Pharmaceutical packaging must protect drugs from moisture, oxygen, light, contamination, and physical damage; however, conventional formats often rely on mixed-material structures that are challenging to recover after use. This is creating strong demand for recyclable, renewable, and resource-efficient packaging solutions that meet strict pharmaceutical quality and safety requirements.

Government regulations are accelerating adoption, particularly across Europe, where the Packaging and Packaging Waste Regulation will generally apply from August 2026. The regulation covers all packaging and packaging waste placed on the EU market and introduces requirements related to manufacturing, composition, reuse, recoverability, and waste management. Pharmaceutical companies supplying European markets are therefore increasingly evaluating packaging designs that can demonstrate recyclability and lower environmental impact while maintaining compliance with product-protection standards.

Large packaging suppliers are also expanding their sustainable product portfolios to support pharmaceutical brand owners’ environmental targets. For instance, Amcor reported that 72% of its packaging production by weight was designed for recyclability by the end of FY2025, including 96% of rigid packaging and 49% of flexible packaging. The company also achieved its target of using 10% post-consumer recycled plastic globally, equivalent to 218,000 metric tons of recycled plastic, indicating the growing scale of circular-material adoption across packaging supply chains.

The rising focus on environmental reporting and carbon-footprint reduction is encouraging pharmaceutical companies to prioritize packaging weight reduction, material simplification, and recycled-content integration. Secondary cartons, labels, bottles, closures, blister packs, and flexible pouches are increasingly being redesigned to reduce material intensity and improve compatibility with existing recycling infrastructure. These initiatives are supporting the transition from conventional single-use pharmaceutical packaging toward more circular packaging systems.

Key Restraint/Challenge: Strict Product Protection Requirements And High Requalification Costs

Sustainable pharmaceutical packaging adoption is constrained by strict product-protection requirements, lengthy regulatory approval processes, and the high cost of requalifying new packaging materials. Medicines are sensitive to moisture, oxygen, ultraviolet light, microbial contamination, and temperature fluctuations, making packaging performance critical for maintaining drug efficacy and patient safety. Any change in packaging structure, polymer type, ink, adhesive, or barrier layer may require extensive compatibility testing, stability studies, and validation before commercial use.

Many sustainable alternatives also face limitations in moisture resistance, oxygen barrier performance, chemical compatibility, and mechanical durability when compared with conventional multilayer pharmaceutical packaging. For instance, recyclable mono-material blister packs and paper-based laminates can require specialized barrier coatings or additional engineering to meet the performance levels needed for highly sensitive drugs. Pharmaceutical companies must therefore balance sustainability objectives with the need to maintain product shelf life, dosage integrity, and tamper-evidence functionality.

Cost remains another major challenge, particularly for small and mid-sized pharmaceutical manufacturers. Bio-based polymers, recycled-content resins, specialty coatings, and recyclable high-barrier films can carry higher material costs than conventional packaging materials. In addition, converting existing packaging lines, qualifying alternative suppliers, and conducting regulatory documentation can increase implementation expenses. Industry discussions also highlight that limited recycling infrastructure and inconsistent collection systems can reduce the practical end-of-life benefits of recyclable packaging in several markets.

The availability of food-grade and pharmaceutical-grade recycled materials remains limited in certain regions, further restricting large-scale adoption. Packaging suppliers must also ensure that recycled-content materials meet stringent purity, migration, and traceability standards. These operational and technical challenges may delay the replacement of conventional materials, especially in high-barrier packaging applications for biologics, injectables, and moisture-sensitive oral solid-dose drugs.

Key Market Opportunity: Expansion Of Bio-Based, Recyclable, And Smart Pharmaceutical Packaging Solutions

The growing need for environmentally responsible medicine delivery is creating significant opportunities for bio-based polymers, recyclable mono-material formats, fiber-based secondary packaging, and smart packaging technologies. Pharmaceutical manufacturers are increasingly seeking packaging systems that reduce carbon emissions and material waste while improving supply-chain traceability, patient adherence, and drug protection. This is expanding opportunities for packaging producers that can combine sustainability with high barrier performance and regulatory compliance.

Recyclable blister packs represent a major opportunity because blister packaging is widely used for tablets and capsules globally. For instance, polyethylene-based recyclable blister systems are being developed to replace conventional PVC structures while retaining child-resistant and senior-friendly features. Amcor’s AmSky system has received multiple sustainability-focused packaging awards and represents a commercially relevant example of how pharmaceutical blister packaging can be redesigned for improved circularity.

The market is also creating opportunities for paper-based cartons, molded fiber inserts, recycled-content bottles, and lightweight closures used in over-the-counter medicines, nutraceuticals, and consumer healthcare products. These applications can enable pharmaceutical companies to reduce virgin material consumption and improve packaging recyclability without compromising brand presentation or distribution efficiency. Suppliers are also investing in digital printing, QR codes, and track-and-trace technologies that can provide patients with disposal guidance, product authentication, and dosage-related information.

Advancements in sustainable high-barrier laminates are opening opportunities in pharmaceutical sachets and stick packs, particularly for powders, oral rehydration products, and unit-dose medicines. Recycle-ready polyolefin and paper-based formats are being developed to deliver comparable moisture protection while improving compatibility with established recycling streams. For instance, recyclable high-shield pharmaceutical laminates are designed to provide moisture-barrier performance of approximately 0.1–0.2 g/m² per day and can operate on existing packaging machinery with similar efficiency, reducing the need for major capital expenditure.

Increasing regulatory requirements and corporate net-zero commitments are expected to further expand investments in sustainable pharmaceutical packaging innovation across North America, Europe, and Asia-Pacific. Companies that develop recyclable, low-carbon, lightweight, and digitally enabled packaging solutions while meeting pharmaceutical validation requirements are likely to gain opportunities in the rapidly evolving healthcare packaging value chain.

Sustainable Pharmaceutical Packaging Market Scope

The market is segmented on the basis of packaging material, form of packaging, end user industry, functional features, and distribution channel.

- By Packaging Material

On the basis of packaging material, the sustainable pharmaceutical packaging market is segmented into recycled paper, biodegradable plastics, glass, metal, and plant-based materials. The Biodegradable Plastics segment held the largest market revenue share of approximately 36.6% in 2025, driven by the broad use of recyclable polymers, recycled-content resins, and bio-based plastic formats in bottles, blister packs, closures, pouches, and syringes. These materials are preferred due to their lightweight properties, cost efficiency, design flexibility, and ability to meet pharmaceutical barrier and safety requirements.

The Glass segment is projected to register the fastest growth at a CAGR of 12.7% from 2026 to 2033, driven by rising demand for recyclable and chemically inert packaging for injectable drugs, biologics, vaccines, and high-value specialty medicines. Glass bottles, vials, ampoules, and cartridges are increasingly preferred for products requiring high protection against moisture, oxygen, and chemical interaction.

- By Form Of Packaging

On the basis of form of packaging, the sustainable pharmaceutical packaging market is segmented into bottles, blisters, pouches, cartons, and syringes. The Blisters segment held the largest market revenue share of approximately 42.0% in 2025, driven by extensive use in tablets, capsules, and unit-dose pharmaceutical products. Sustainable blister packs are increasingly being developed using recyclable polyethylene, mono-material films, and lower-impact lidding structures to reduce dependence on conventional PVC and aluminum combinations.

The Syringes segment is projected to register the fastest growth from 2026 to 2033, driven by increasing demand for prefilled syringes, biologics, injectable therapies, and self-administration drug-delivery systems. Rising adoption of recyclable plastics, lightweight materials, and reduced-material syringe components is supporting sustainable packaging innovation in this segment.

- By End User Industry

On the basis of end user industry, the sustainable pharmaceutical packaging market is segmented into pharmaceuticals, biotech, healthcare, and veterinary. The Pharmaceuticals segment held the largest market revenue share of approximately 49.5% in 2025, driven by high-volume production of prescription medicines, generic drugs, over-the-counter products, and oral solid-dose formulations. Pharmaceutical manufacturers are increasingly adopting recycled paper cartons, recyclable blister packs, lightweight bottles, and lower-carbon packaging formats to meet sustainability targets and regulatory requirements.

The Biotech segment is projected to register the fastest growth from 2026 to 2033, driven by the expanding production of biologics, cell and gene therapies, vaccines, and temperature-sensitive injectable drugs. These products require high-performance, traceable, and protective packaging, creating opportunities for sustainable glass, recyclable polymer, and smart packaging solutions.

- By Functional Features

On the basis of functional features, the sustainable pharmaceutical packaging market is segmented into child resistance, tamper evidence, sustainability compliance, and smart packaging. The Sustainability Compliance segment held the largest market revenue share of approximately 63.1% in 2025, driven by increasing demand for recyclable, reusable, and biodegradable packaging formats that support circular economy targets. Recyclable packaging formats, including glass bottles, aluminum containers, recycled paper cartons, and recyclable plastic packaging, are being increasingly adopted across pharmaceutical supply chains.

The Smart Packaging segment is projected to register the fastest growth from 2026 to 2033, driven by increasing adoption of QR codes, RFID tags, near-field communication labels, and serialization technologies. These features support product authentication, patient adherence, supply-chain visibility, anti-counterfeiting compliance, and improved disposal guidance for sustainable packaging materials.

- By Distribution Channel

On the basis of distribution channel, the sustainable pharmaceutical packaging market is segmented into online, retail pharmacy, hospital pharmacy, and wholesale. The Wholesale segment held the largest market revenue share of approximately 39.4% in 2025, driven by the large-scale movement of pharmaceutical products from manufacturers to distributors, hospitals, pharmacies, and healthcare institutions. Sustainable wholesale packaging demand is supported by the adoption of recyclable corrugated cartons, reusable transit packaging, lightweight shipping materials, and optimized secondary packaging formats.

The Online segment is projected to register the fastest growth from 2026 to 2033, driven by rising e-pharmacy adoption, direct-to-patient medicine delivery, and growing demand for protective yet lightweight shipping packaging. Online pharmaceutical distribution is increasing the use of recyclable mailers, paper-based cushioning, temperature-controlled sustainable packaging, and digitally enabled labels to improve delivery efficiency and reduce packaging waste.

Sustainable Pharmaceutical Packaging Market Regional Analysis

North America Sustainable Pharmaceutical Packaging Market Insight

North America dominated the sustainable pharmaceutical packaging market with the largest revenue share in 2025, supported by strong pharmaceutical manufacturing activity, expanding biologics and specialty drug production, and increasing corporate commitments to reduce packaging-related emissions and waste. Pharmaceutical companies across the region are increasingly adopting recyclable blister packs, recycled-content bottles, paper-based cartons, lightweight containers, and lower-carbon secondary packaging formats. The presence of established packaging manufacturers, advanced recycling infrastructure, and stringent product safety requirements further supports the development and adoption of sustainable pharmaceutical packaging solutions across prescription, over-the-counter, and consumer healthcare products.

U.S. Sustainable Pharmaceutical Packaging Market Insight

The U.S. sustainable pharmaceutical packaging market captured the largest revenue share in 2025 within North America, fueled by high medicine consumption, growing demand for e-pharmacy delivery, and increasing investments in sustainable healthcare supply chains. Drug manufacturers are prioritizing recyclable and lightweight packaging solutions to reduce material consumption while maintaining protection against moisture, oxygen, contamination, and physical damage. The growing use of biologics, injectable therapies, and self-administered medicines is also increasing demand for sustainable glass vials, recyclable polymer bottles, prefilled syringes, and temperature-controlled packaging solutions.

Europe Sustainable Pharmaceutical Packaging Market Insight

The Europe sustainable pharmaceutical packaging market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent packaging waste regulations, circular economy initiatives, and increasing pharmaceutical industry focus on recyclable and renewable materials. The region is witnessing growing adoption of mono-material blister packs, fiber-based secondary cartons, recyclable flexible films, and reduced-plastic packaging formats. Strong sustainability reporting requirements and the increasing need to comply with packaging recyclability standards are encouraging pharmaceutical manufacturers and packaging converters to redesign conventional packaging structures across residential healthcare, hospital, and retail pharmacy applications.

U.K. Sustainable Pharmaceutical Packaging Market Insight

The U.K. sustainable pharmaceutical packaging market is expected to witness significant growth from 2026 to 2033, driven by increasing demand for low-carbon healthcare products, expanding online pharmacy activity, and growing pressure to reduce plastic packaging waste. Pharmaceutical companies and retailers are increasingly using recyclable paper cartons, lightweight plastic bottles, recyclable mailers, and paper-based cushioning materials for medicine distribution. In addition, the growing adoption of digital labels, QR codes, and track-and-trace technologies is supporting improved patient information, packaging disposal guidance, and pharmaceutical supply-chain transparency.

Germany Sustainable Pharmaceutical Packaging Market Insight

The Germany sustainable pharmaceutical packaging market is expected to witness strong growth from 2026 to 2033, fueled by the country’s advanced recycling systems, strong environmental regulations, and emphasis on resource-efficient manufacturing. Pharmaceutical packaging suppliers are increasingly developing recyclable blister packs, recycled-content plastic containers, reusable transport packaging, and fiber-based cartons designed to reduce material use and improve recovery after disposal. Germany’s large pharmaceutical manufacturing base and growing demand for high-value injectable medicines are also supporting the adoption of sustainable glass vials, ampoules, and specialized protective packaging formats.

Asia-Pacific Sustainable Pharmaceutical Packaging Market Insight

The Asia-Pacific sustainable pharmaceutical packaging market is expected to witness the fastest growth rate from 2026 to 2033, supported by rising healthcare expenditure, expanding pharmaceutical production, increasing urbanization, and growing government initiatives focused on plastic waste reduction. Countries across the region are increasing investments in recyclable polymers, biodegradable packaging materials, paper-based secondary packaging, and lightweight medicine containers. The expanding generic drug industry, increasing demand for affordable healthcare products, and rapid growth in online medicine delivery are further strengthening the need for cost-effective and environmentally responsible pharmaceutical packaging solutions.

Japan Sustainable Pharmaceutical Packaging Market Insight

The Japan sustainable pharmaceutical packaging market is expected to witness strong growth from 2026 to 2033 due to the country’s advanced healthcare infrastructure, high focus on product quality, and increasing emphasis on waste reduction. Pharmaceutical companies are adopting recyclable glass, reduced-material blister packs, lightweight bottles, and high-performance paper-based cartons to meet environmental targets while maintaining strict safety and quality standards. Japan’s aging population is also increasing demand for easy-to-open, child-resistant, and patient-friendly packaging formats for chronic disease medicines, creating opportunities for sustainable packaging designs with improved usability and traceability.

China Sustainable Pharmaceutical Packaging Market Insight

The China sustainable pharmaceutical packaging market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s large pharmaceutical manufacturing industry, expanding healthcare access, and growing adoption of environmentally responsible packaging materials. The increasing production of generic medicines, vaccines, and over-the-counter products is supporting demand for recyclable plastic bottles, paper cartons, flexible pouches, glass containers, and lower-weight transport packaging. China’s broader focus on circular economy development, plastic pollution reduction, and smart manufacturing is also encouraging pharmaceutical packaging companies to invest in recyclable, bio-based, and digitally enabled packaging solutions.

Sustainable Pharmaceutical Packaging Market Share

The Sustainable Pharmaceutical Packaging industry is primarily led by well-established companies, including:

• Amcor (AU)

• BASF (DE)

• West Pharmaceutical Services (U.S.)

• Gerresheimer (DE)

• Mondi Group (U.K.)

• Sealed Air Corporation (U.S.)

• Smurfit Kappa (IE)

• Sonoco Products Company (U.S.)

• AptarGroup (U.S.)

• Berry Global Group (U.S.)

• SCHOTT Pharma (DE)

• Stevanato Group (IT)

• SGD Pharma (FR)

• Constantia Flexibles (AT)

• TekniPlex (U.S.)

Latest Developments in Sustainable Pharmaceutical Packaging Market

- In June 2026, Amcor (AU) announced a multi-million-dollar expansion of its healthcare packaging manufacturing facility in Sira, Karnataka, India. The development will strengthen the company’s capabilities in high-performance healthcare packaging and patient-centric drug-delivery solutions, supporting rising pharmaceutical demand across India and South Asia. This expansion is expected to improve regional supply availability and strengthen competition in sustainable and specialized pharmaceutical packaging.

- In April 2026, BASF (DE) expanded its ecovio portfolio with new certified home-compostable grades for flexible packaging. The materials are designed to provide customizable barriers against grease, liquids, oxygen, and moisture while supporting organic or paper recycling routes. This development broadens the availability of bio-based and compostable materials for healthcare packaging applications, accelerating innovation in sustainable high-barrier packaging.

- In October 2025, Amcor (AU) received the DuPont Tyvek Sustainable Healthcare Packaging Award for its ACT2100 Air Peel Technology. The heat-seal coating technology is designed to provide stronger seals, enhanced breathability, and improved sterilization performance for healthcare packaging. The recognition strengthens Amcor’s market position in sustainable medical packaging and highlights the growing importance of operational efficiency and patient safety in packaging innovation.

- In June 2025, BASF (DE) transitioned its Rheovis range to bio-based ethyl acrylate at its Ludwigshafen and Bradford production sites. The new range offers up to 35% biogenic content and reduces product carbon footprint by up to 30% while maintaining the same technical performance. This transition supports the availability of lower-carbon chemical inputs for packaging coatings, adhesives, and pharmaceutical packaging-related applications.

- In March 2025, Berry Global Group (U.S.) expanded its B Circular Range with packaging components containing 30% to 100% post-consumer recycled plastic. The portfolio includes child-resistant closures, jars, triggers, and flip-top closures designed to improve recyclability and reduce virgin plastic consumption. The development is expected to increase sustainable packaging options for over-the-counter medicines, healthcare products, and pharmaceutical consumer packaging.

- In June 2024, BASF (DE) introduced biomass-balanced ecoflex, a certified compostable PBAT material for packaging applications. The material provides a product carbon footprint that is approximately 60% lower than standard ecoflex grades while retaining comparable processing, performance, and biodegradation properties. This development is expected to support the transition toward renewable feedstocks and expand sustainable flexible packaging alternatives across the pharmaceutical sector.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Sustainable Pharmaceutical Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Sustainable Pharmaceutical Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Sustainable Pharmaceutical Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.