Global Synthetic Gypsum Market

Market Size in USD Billion

USD

2.56 Billion

USD

3.75 Billion

2024

2032

USD

2.56 Billion

USD

3.75 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.56 Billion | |

| USD 3.75 Billion | |

| % | |

|

Synthetic Gypsum Market Size

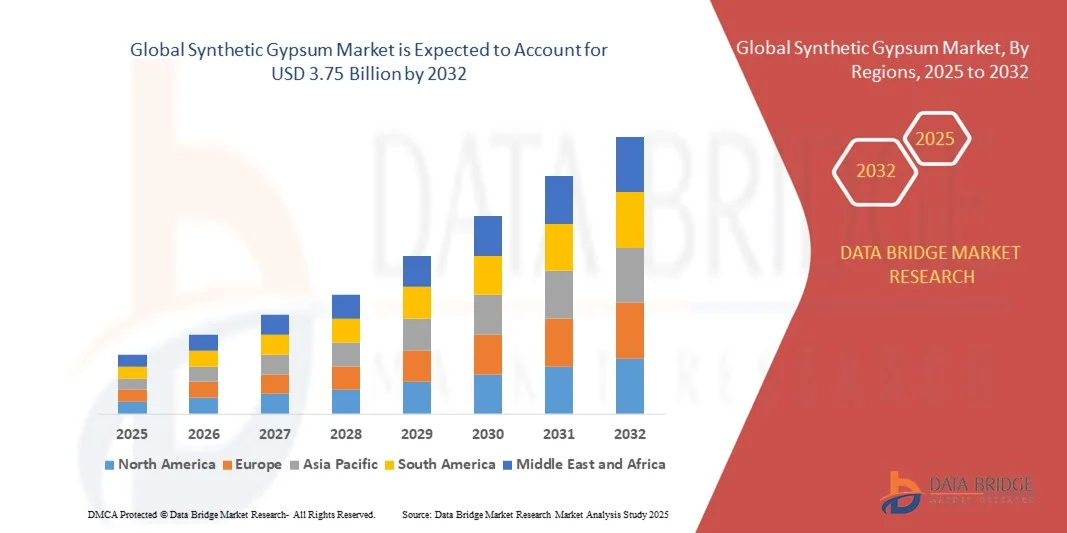

- The global synthetic gypsum market size was valued at USD 2.56 billion in 2024 and is expected to reach USD 3.75 billion by 2032, at a CAGR of 4.90% during the forecast period

- The market growth is largely fuelled by the rising demand from the construction and cement industries, which utilize synthetic gypsum as a sustainable and cost-effective alternative to natural gypsum

- Increasing environmental concerns and strict regulations on industrial emissions are encouraging power plants to adopt flue gas desulfurization (FGD) systems, thereby boosting synthetic gypsum production

Synthetic Gypsum Market Analysis

- The synthetic gypsum market is witnessing steady growth as industries focus on reducing carbon footprints and reusing industrial by-products such as FGD gypsum, phosphogypsum, and citrogypsum

- Rising investments in green construction and the use of recycled materials are driving the adoption of synthetic gypsum in wallboard manufacturing and cement production

- North America dominated the synthetic gypsum market with the largest revenue share of 38.64% in 2024, driven by the rising adoption of sustainable construction materials and the presence of major gypsum-based product manufacturers across the region. The strong demand for wallboard, cement, and plaster applications, supported by advancements in green building certifications, continues to boost market growth

- Asia-Pacific region is expected to witness the highest growth rate in the global synthetic gypsum market, driven by accelerated infrastructure development, rising demand for low-cost sustainable materials, and increasing industrial output across emerging economies such as China and India

- The flue gas desulfurization (FGD) gypsum segment held the largest market revenue share in 2024, driven by the widespread use of FGD systems in coal-fired power plants and the increasing focus on utilizing industrial byproducts in construction materials. FGD gypsum is widely adopted in the production of cement, wallboard, and plaster due to its high purity, uniformity, and cost-effectiveness, making it a preferred substitute for natural gypsum in sustainable manufacturing

Report Scope and Synthetic Gypsum Market Segmentation

|

Attributes |

Synthetic Gypsum Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Synthetic Gypsum Market Trends

Growing Adoption of Synthetic Gypsum in Sustainable Construction

- The increasing emphasis on sustainable construction practices is driving the adoption of synthetic gypsum as an eco-friendly alternative to natural gypsum. Derived from industrial byproducts such as flue gas desulfurization (FGD), synthetic gypsum helps reduce landfill waste and supports circular economy initiatives within the building materials industry. Its consistent composition and minimal impurities make it ideal for large-scale construction use, contributing to waste reduction and long-term environmental goals

- The construction sector’s shift toward green certifications such as LEED and BREEAM is further encouraging the use of synthetic gypsum in wallboards, cement, and plasters. Manufacturers are leveraging its consistent quality and purity to develop high-performance building materials with reduced carbon footprints. This growing preference among environmentally conscious builders and architects is enhancing product innovation and promoting a more sustainable building materials supply chain

- Rising awareness of environmental compliance and resource efficiency among end-users is boosting demand for synthetic gypsum-based products. Builders and contractors prefer it for its uniform composition, lower impurities, and sustainability benefits compared to mined gypsum. The adoption is also supported by government regulations encouraging the use of recycled industrial byproducts to minimize natural resource depletion and promote circular construction models

- For instance, in 2023, several cement producers in Europe and North America integrated synthetic gypsum into their clinker production to cut emissions and enhance strength performance, marking a step toward achieving net-zero construction goals. This transition not only lowered production costs but also improved energy efficiency and product consistency across key cement brands. The trend reflects a broader shift toward decarbonized construction practices within the global cement industry

- While synthetic gypsum supports sustainability objectives and cost-efficiency, the market’s growth depends on optimizing production processes, ensuring consistent supply from power plants, and strengthening collaboration between industries to promote material reuse. Manufacturers are increasingly investing in R&D to enhance quality and explore new applications, such as in 3D printing and prefabricated materials, to expand synthetic gypsum’s industrial footprint

Synthetic Gypsum Market Dynamics

Driver

Increasing Use of Synthetic Gypsum in Cement and Agriculture Industries

- The growing utilization of synthetic gypsum in cement manufacturing is one of the major drivers of market growth. It acts as an effective setting time regulator and enhances cement quality, making it indispensable in modern construction applications. With sustainability becoming a key priority, synthetic gypsum’s ability to lower production costs and improve performance makes it a preferred substitute for natural gypsum across cement plants globally

- The agricultural sector is also increasingly adopting synthetic gypsum to improve soil structure, reduce salinity, and enhance water retention. It provides essential nutrients such as calcium and sulfur, improving crop yield and soil fertility, particularly in regions facing soil degradation issues. Furthermore, synthetic gypsum’s low solubility and neutral pH make it an ideal long-term soil conditioner, promoting sustainable agricultural practices in both developing and developed regions

- The rise in global infrastructure projects and demand for eco-efficient building materials are expanding synthetic gypsum consumption across various applications. Continuous R&D efforts by manufacturers to improve product quality and reduce impurities are also strengthening market prospects. Growing demand from emerging economies such as India, Brazil, and Indonesia for low-cost construction materials is creating lucrative growth opportunities for synthetic gypsum suppliers

- For instance, in 2024, Asian cement manufacturers began large-scale integration of synthetic gypsum sourced from desulfurization units to reduce dependency on mined gypsum, enhancing cost efficiency and sustainability. This shift has improved product availability while promoting cleaner industrial processes, aligning with regional decarbonization policies. Moreover, the consistent supply from power plants ensures steady market expansion in the region

- While demand across construction and agriculture sectors is driving market growth, ensuring consistent supply, optimizing logistics, and maintaining purity standards remain vital for sustained adoption. Manufacturers are increasingly entering long-term supply contracts and investing in quality monitoring systems to ensure reliability and cost control. Strategic collaborations between utility providers and construction material producers are further improving production stability

Restraint/Challenge

Dependence on Coal-Fired Power Plants and Fluctuating Supply

- The availability of synthetic gypsum is largely dependent on emissions control processes in coal-fired power plants, particularly those using flue gas desulfurization (FGD) systems. As many countries shift toward renewable energy, the reduction in coal-based power generation may limit the future supply of synthetic gypsum. This dependence creates a potential supply gap that could impact downstream industries reliant on stable gypsum availability

- Supply chain disruptions and inconsistent byproduct quality due to variations in power plant operations can affect material availability and reliability. This dependence on external industrial sources creates uncertainty for construction material manufacturers relying on steady input supplies. To mitigate this, producers are exploring diversification strategies such as utilizing alternative industrial byproducts and synthetic processes independent of coal-based generation

- High transportation costs associated with moving bulk gypsum from production sites to manufacturing facilities also act as a significant restraint, particularly in regions where local FGD units are limited or decommissioned. The heavy and bulky nature of gypsum makes long-distance transport economically challenging, leading to regional supply imbalances and higher end-product costs. Companies are now focusing on localized processing plants to reduce logistics-related expenses

- For instance, in 2023, several power plants in Europe and North America reduced coal-based generation capacity to meet climate goals, causing fluctuations in FGD gypsum output and impacting the supply chain for wallboard and cement producers. This scenario forced manufacturers to explore alternative materials and recycling methods to maintain production efficiency and meet construction demand. The trend underlines the importance of raw material diversification for long-term resilience

- While the transition to cleaner energy poses a supply challenge, diversification of raw material sources, development of alternative synthetic processes, and regional partnerships can help stabilize supply and sustain market growth. Investments in industrial symbiosis and new chemical synthesis methods are emerging as viable strategies to ensure a continuous flow of synthetic gypsum. These advancements are expected to maintain market stability despite the global energy transition

Synthetic Gypsum Market Scope

The synthetic gypsum market is segmented on the basis of product type, application, and end-use industry.

- By Product Type

On the basis of product type, the synthetic gypsum market is segmented into citrogypsum, fluorogypsum, phosphogypsum, titanogypsum, flue gas desulfurization (FGD) gypsum, and others. The flue gas desulfurization (FGD) gypsum segment held the largest market revenue share in 2024, driven by the widespread use of FGD systems in coal-fired power plants and the increasing focus on utilizing industrial byproducts in construction materials. FGD gypsum is widely adopted in the production of cement, wallboard, and plaster due to its high purity, uniformity, and cost-effectiveness, making it a preferred substitute for natural gypsum in sustainable manufacturing.

The phosphogypsum segment is expected to witness the fastest growth rate from 2025 to 2032, supported by its rising utilization in soil conditioning, cement production, and agricultural applications. The growing focus on recycling phosphoric acid byproducts and reducing industrial waste is propelling the adoption of phosphogypsum in both developed and emerging economies. In addition, advancements in purification technologies are enhancing the usability and environmental safety of phosphogypsum-based products, further boosting market growth.

- By Application

On the basis of application, the synthetic gypsum market is segmented into dental, drywall, cement, water treatment, soil amendment, and others. The cement segment accounted for the largest market share in 2024, attributed to the growing incorporation of synthetic gypsum as a setting time regulator and performance enhancer in cement production. Its uniform particle size, high purity, and consistent chemical properties make it an essential additive in the manufacturing process, contributing to improved cement quality and reduced production costs.

The soil amendment segment is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing awareness of soil restoration and nutrient management in agriculture. Synthetic gypsum’s ability to improve soil aeration, reduce salinity, and enhance water infiltration has made it a preferred soil conditioner among farmers. The rising adoption of sustainable farming practices and government initiatives to promote soil health are further accelerating the demand for synthetic gypsum in this application.

- By End-Use Industry

On the basis of end-use industry, the synthetic gypsum market is segmented into construction industry and agriculture industry. The construction industry segment dominated the market in 2024, driven by the growing use of synthetic gypsum in cement, plasterboard, and drywall manufacturing. The shift toward sustainable construction materials and stringent environmental regulations promoting industrial byproduct reuse are key factors boosting its demand in this sector.

The agriculture industry segment is expected to register the fastest growth rate from 2025 to 2032, supported by the increasing use of synthetic gypsum as a soil conditioner and nutrient source. Farmers are adopting synthetic gypsum to improve soil fertility, reduce erosion, and enhance crop productivity. The growing emphasis on regenerative agriculture and the rising need for sustainable soil management solutions are further contributing to the expansion of synthetic gypsum usage in the agricultural sector.

Synthetic Gypsum Market Regional Analysis

- North America dominated the synthetic gypsum market with the largest revenue share of 38.64% in 2024, driven by the rising adoption of sustainable construction materials and the presence of major gypsum-based product manufacturers across the region. The strong demand for wallboard, cement, and plaster applications, supported by advancements in green building certifications, continues to boost market growth

- The growing focus on recycling industrial byproducts and reducing carbon emissions is promoting the large-scale utilization of synthetic gypsum, particularly from flue gas desulfurization (FGD) processes. Regulatory support and technological innovation in waste management further strengthen the region’s leadership position

- The increasing use of synthetic gypsum in agriculture to enhance soil productivity and water infiltration is also contributing to market expansion, especially in regions with intensive farming activities. Continuous infrastructure investments and sustainable construction practices further reinforce the dominance of North America in the global market

U.S. Synthetic Gypsum Market Insight

The U.S. synthetic gypsum market captured the largest revenue share in 2024 within North America, driven by the growing emphasis on eco-friendly building materials and robust demand from the cement and drywall industries. The country’s strong environmental regulations and initiatives to reduce power plant emissions have led to consistent FGD gypsum production. Moreover, the adoption of synthetic gypsum in agriculture as a soil conditioner is gaining momentum. The presence of major wallboard manufacturers and sustainable construction projects continues to stimulate the market across residential and commercial sectors.

Europe Synthetic Gypsum Market Insight

The Europe synthetic gypsum market is expected to witness the fastest growth rate from 2025 to 2032, fuelled by strict environmental policies promoting industrial byproduct recycling and the widespread integration of synthetic gypsum in construction materials. Growing awareness of circular economy practices and the transition toward sustainable cement manufacturing are key growth drivers. The region’s focus on reducing natural gypsum mining and enhancing material reuse supports the growing use of synthetic alternatives. Increasing government support for carbon-neutral infrastructure projects further accelerates adoption across European countries.

U.K. Synthetic Gypsum Market Insight

The U.K. synthetic gypsum market is expected to witness notable growth from 2025 to 2032, supported by increasing emphasis on sustainable construction practices and reduced reliance on natural gypsum mining. The country’s construction sector is rapidly integrating synthetic gypsum in plasterboard, drywall, and cement production to meet environmental and performance standards. Government initiatives promoting industrial waste recycling and the decarbonization of the building materials sector are key drivers. Furthermore, growing adoption among green-certified projects and renovation activities is contributing to the rising demand for synthetic gypsum across the U.K.

Germany Synthetic Gypsum Market Insight

The Germany synthetic gypsum market is expected to witness the fastest growth rate from 2025 to 2032, driven by the country’s advanced environmental policies and focus on green manufacturing processes. Germany’s strong industrial base and commitment to reducing CO₂ emissions have encouraged the use of FGD gypsum in cement and plasterboard production. The growing demand for high-quality, consistent raw materials in the construction sector is also supporting market expansion. In addition, the nation’s commitment to the circular economy and sustainable material utilization strengthens its position as a key synthetic gypsum consumer in Europe.

Asia-Pacific Synthetic Gypsum Market Insight

The Asia-Pacific synthetic gypsum market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid urbanization, infrastructure development, and growing demand for affordable, sustainable construction materials in countries such as China, India, and Japan. Expanding industrial sectors and the adoption of flue gas desulfurization systems in coal-fired power plants are enhancing synthetic gypsum availability. The region’s strong focus on industrial waste management, coupled with government initiatives for eco-efficient building materials, is further accelerating market growth.

China Synthetic Gypsum Market Insight

The China synthetic gypsum market accounted for the largest revenue share in Asia-Pacific in 2024, driven by the country's expanding construction industry, government focus on sustainability, and large-scale availability of FGD gypsum. Rapid industrialization and emission control regulations have led to increased production of synthetic gypsum as a byproduct. The nation’s strong presence of cement and plasterboard manufacturers further supports market growth. Continuous infrastructure investments, coupled with the promotion of low-carbon construction materials, are expected to sustain China’s leading position in the regional market.

Japan Synthetic Gypsum Market Insight

The Japan synthetic gypsum market is expected to witness steady growth from 2025 to 2032, driven by the country’s strong focus on environmental sustainability and technological innovation in construction materials. Japan’s advanced infrastructure and commitment to recycling industrial byproducts such as flue gas desulfurization (FGD) gypsum are key factors promoting market growth. The demand for lightweight, energy-efficient building materials continues to rise, encouraging the use of synthetic gypsum in wallboard and cement production. Moreover, Japan’s stringent emission regulations and support for circular economy initiatives further strengthen its position in the regional market.

Synthetic Gypsum Market Share

The Synthetic Gypsum industry is primarily led by well-established companies, including:

• LafargeHolcim (Switzerland)

• USG Corporation (U.S.)

• FEECO International, Inc. (U.S.)

• Delta Gypsum, LLC (U.S.)

• National Gypsum Properties, LLC (U.S.)

• Synthetic Materials (U.S.)

• Knauf Gips KG (Germany)

• American Gypsum (U.S.)

• Saint-Gobain Limited (France)

• PABCO Building Products, LLC (U.S.)

• Georgia-Pacific (U.S.)

• GYPTEC Ibérica (Portugal)

• BauMineral GmbH (Germany)

• VGB PowerTech e.V. (Germany)

• STEAG Power Minerals (Germany)

• Drax Group plc (U.K.)

• SSE (U.K.)

• EDF Energy (U.K.)

• E.ON UK plc (U.K.)

Latest Developments in Global Synthetic Gypsum Market

- In May 2024, EuroChem announced the launch of the third phase of its large-scale chemical complex project in Kazakhstan, focusing on the production of synthetic gypsum as a byproduct. The Switzerland-based company collaborated with China National Chemical Engineering to design, build, and commission the facility in Janatas, Jambyl Region. This new phase aims to produce synthetic gypsum and calcium chloride for use in construction materials, road building, coal, and hydrocarbon industries. The development is expected to strengthen the availability of industrial byproducts for sustainable construction applications and enhance EuroChem’s position in the circular economy landscape

- In February 2024, Knauf España expanded its product portfolio by introducing Maxiboard boards, a new range of oversized gypsum wallboard systems. The boards, featuring a 900mm thickness, aim to improve installation efficiency by reducing the need for studs, screws, and joint treatments by 30%. Designed for use in large-scale structures such as shopping malls, cinemas, and data centers, these boards provide exceptional fire resistance (EI 240 up to 6m and EI 120 up to 11m). This product innovation enhances construction efficiency, promotes safety, and reinforces Knauf’s leadership in advanced gypsum wallboard solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Synthetic Gypsum Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Synthetic Gypsum Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Synthetic Gypsum Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.