Global Synthetic Lethality Drug Market

Market Size in USD Billion

USD

1.93 Billion

USD

8.07 Billion

2025

2033

USD

1.93 Billion

USD

8.07 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.93 Billion | |

| USD 8.07 Billion | |

| % | |

|

Synthetic Lethality Drug Market Size

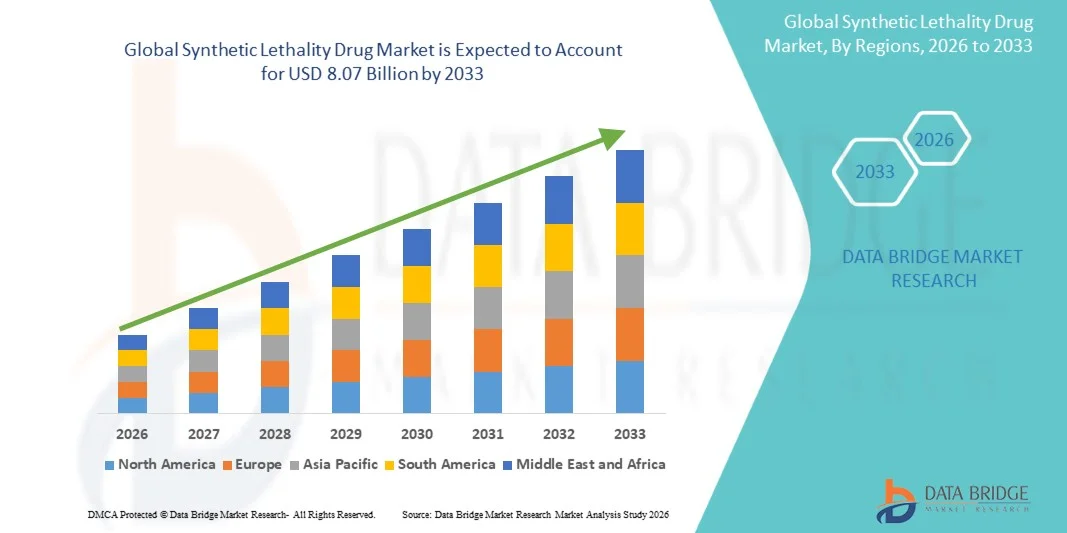

- The global Synthetic Lethality Drug market size was valued at USD 1.93 billion in 2025 and is expected to reach USD 8.07 billion by 2033, at a CAGR of 19.60% during the forecast period

- The market growth is largely fueled by the increasing research and development in targeted cancer therapies and precision medicine, leading to more effective and personalized treatment options for patients

- Furthermore, rising demand for combination therapies and the development of next-generation synthetic lethality drugs are driving innovation and adoption across oncology treatment centers. These converging factors are accelerating the uptake of Synthetic Lethality Drug solutions, thereby significantly boosting the industry's growth

Synthetic Lethality Drug Market Analysis

- Synthetic lethality drugs, offering targeted cancer therapy by exploiting specific genetic vulnerabilities in tumor cells, are increasingly vital components of modern oncology treatment regimens in both hospitals and specialty clinics due to their enhanced efficacy, reduced side effects, and potential for personalized medicine applications

- The escalating demand for synthetic lethality drugs is primarily fueled by advances in precision medicine, growing prevalence of oncology cases, and rising investment in targeted cancer therapies

- North America dominated the synthetic lethality drug market with the largest revenue share of 42.5% in 2025, characterized by strong pharmaceutical R&D infrastructure, early adoption of targeted therapies, and a high prevalence of oncology cases, with the U.S. experiencing substantial growth in synthetic lethality drug usage driven by innovations from both established pharma companies and biotech startups focusing on precision oncology

- Asia-Pacific is expected to be the fastest growing region in the synthetic lethality drug market during the forecast period, accounting for 28.7% of the market share in 2025, due to increasing healthcare infrastructure, rising cancer incidence, and growing investments in oncology drug development

- The PARP Inhibitors segment dominated the largest market revenue share of 44.5% in 2025, driven by strong clinical evidence supporting efficacy in ovarian, breast, and prostate cancers with BRCA mutations

Report Scope and Synthetic Lethality Drug Market Segmentation

|

Attributes |

Synthetic Lethality Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• AstraZeneca (U.K.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Synthetic Lethality Drug Market Trends

“Rising Adoption of Targeted Cancer Therapies”

- A major and accelerating trend in the global Synthetic Lethality Drug market is the increasing emphasis on precision medicine and targeted cancer therapies

- Unlike conventional chemotherapies, synthetic lethality drugs exploit specific genetic vulnerabilities in tumor cells, enabling highly selective and effective treatments with fewer adverse effects

- This approach is transforming the landscape of oncology care, as clinicians increasingly prioritize therapies tailored to individual patient profiles

- The trend is further reinforced by a surge in research focusing on PARP inhibitors and other synthetic lethality-based compounds. Clinical trials across North America, Europe, and Asia-Pacific are expanding the potential indications for these therapies, from ovarian and breast cancers to pancreatic and prostate cancers

- For instance, the recent approval of olaparib for BRCA-mutated ovarian cancer has not only improved patient outcomes but also established a benchmark for precision oncology in mainstream clinical practice

- Pharmaceutical companies are also exploring combination therapies, integrating synthetic lethality drugs with immunotherapies, hormone therapies, and other targeted agents

- Such combinations aim to overcome resistance mechanisms, enhance efficacy, and broaden the treatment landscape. Alongside this, the growth of genetic testing and tumor profiling in hospitals, specialty clinics, and homecare settings is enabling oncologists to identify eligible patients more efficiently, creating a stronger adoption pipeline for synthetic lethality therapies

Synthetic Lethality Drug Market Dynamics

Driver

“Increasing Cancer Prevalence and Expanding Healthcare Infrastructure”

- The growing prevalence of cancer worldwide remains one of the most significant drivers for the synthetic lethality drug market. Rising incidence rates of breast, ovarian, prostate, and pancreatic cancers, particularly in North America and Europe, are prompting greater demand for innovative and personalized treatments

- Patients and healthcare providers alike are recognizing the benefits of therapies that target specific genetic mutations, which has led to increased clinical adoption

- Significant investments by pharmaceutical companies in research and development are also propelling market growth

- For instance, in 2025, leading companies such as AstraZeneca, Bristol-Myers Squibb, and GlaxoSmithKline expanded their synthetic lethality drug pipelines to include next-generation PARP inhibitors and other novel agents, focusing on both monotherapy and combination therapy approaches

- These efforts are supported by well-established healthcare infrastructures, increasing public awareness, and reimbursement policies in developed regions, which collectively facilitate faster adoption

- Moreover, the expansion of specialty clinics, improved diagnostic infrastructure, and rising access to genetic testing and molecular profiling are strengthening the foundation for synthetic lethality drug deployment

- Emerging markets in Asia-Pacific are also witnessing rapid healthcare improvements, with new hospitals, oncology centers, and homecare services enabling wider availability and accessibility of these therapies

- In addition, ongoing collaborations between academic research institutions and pharmaceutical companies are accelerating clinical trials, further increasing patient access and confidence in these treatments

Restraint/Challenge

“High Costs, Regulatory Complexity, and Patient Accessibility”

- Despite the strong growth drivers, several challenges remain for the synthetic lethality drug market. One of the key restraints is the high cost associated with these therapies

- Advanced targeted treatments, such as PARP inhibitors, require substantial investment in research, development, and production, resulting in high prices for patients. Insurance coverage and reimbursement policies vary by region, and in some cases, patients in emerging markets may face significant barriers to accessing treatment

- Regulatory complexities also slow the entry of new synthetic lethality drugs into the market. Approval processes differ across countries, with rigorous clinical validation and long review periods delaying the availability of novel therapies

- This is particularly relevant for combination therapies, which require additional trials to establish safety and efficacy, further extending timelines

- Limited awareness among healthcare providers in certain regions regarding patient eligibility and genetic testing protocols can also hinder uptake

- For instance, In some cases, oncologists may not have access to sufficient genetic profiling infrastructure, making it difficult to identify patients who could benefit from synthetic lethality treatments. In addition, some patients may face logistical challenges accessing specialty clinics or hospitals capable of administering these advanced therapies

- To overcome these challenges, industry stakeholders are focusing on expanding patient education programs, improving accessibility to genetic testing, streamlining regulatory pathways, and advocating for broader insurance coverage

- Efforts to develop cost-effective manufacturing techniques and distribution networks are also underway, aiming to make synthetic lethality therapies more affordable and widely available across both developed and emerging markets

Synthetic Lethality Drug Market Scope

The market is segmented on the basis of drug type and application.

• By Drug Type

On the basis of drug type, the market is segmented into PARP Inhibitors, ATR Inhibitors, CHK1 Inhibitors, WEE1 Inhibitors, and Others. The PARP Inhibitors segment dominated the largest market revenue share of 44.5% in 2025, driven by strong clinical evidence supporting efficacy in ovarian, breast, and prostate cancers with BRCA mutations. Hospitals and specialty clinics favor PARP inhibitors for targeted therapy in precision oncology. Clinical guidelines encourage early adoption for high-risk patients. Insurance coverage supports patient access to these costly therapies. Hospital pharmacies ensure immediate availability for inpatient and outpatient treatment. Homecare programs integrate oral PARP therapy. Research pipelines focus on next-generation PARP inhibitors. Combination therapy with chemotherapy or immunotherapy enhances efficacy. Patient adherence programs improve long-term outcomes. Emerging markets show rising adoption due to increasing cancer incidence. Clinical trials continue to expand indications. Regulatory approvals in multiple regions support market dominance. Physician awareness campaigns enhance prescribing confidence.

The ATR Inhibitors segment is expected to witness the fastest CAGR of 7.2% from 2026 to 2033, driven by growing clinical research and pipeline development for ovarian, pancreatic, and lung cancers. Hospitals and specialty clinics integrate ATR inhibitors into combination regimens. Emerging clinical trials demonstrate efficacy in DNA damage response pathways. Insurance coverage and government programs facilitate adoption. Oral and parenteral formulations increase accessibility. Homecare integration supports long-term therapy management. Telemedicine and digital health platforms enhance adherence. Physician education and guidelines support early-stage use. Patient preference for targeted therapies drives uptake. Specialty pharmacies manage controlled distribution. Pipeline expansion for rare and aggressive tumors fuels growth. Multidisciplinary teams implement therapy protocols. Combination therapies with PARP inhibitors further boost adoption.

• By Application

On the basis of application, the market is segmented into Ovarian Cancer, Breast Cancer, Prostate Cancer, Pancreatic Cancer, Lung Cancer, and Others. The Ovarian Cancer segment dominated the largest market revenue share of 39.8% in 2025, due to high prevalence of BRCA-mutated cases and the proven clinical efficacy of PARP inhibitors. Hospitals and specialty clinics prioritize early detection and targeted treatment. Clinical guidelines strongly support PARP inhibitor therapy for recurrent ovarian cancer. Insurance coverage ensures patient access. Hospital pharmacies maintain a steady supply. Combination therapies with chemotherapy improve outcomes. Homecare programs incorporate oral therapy. Physician awareness and patient education increase adherence. Government-funded programs support early detection. Clinical trials continue to validate long-term benefits. Emerging markets report increasing adoption. Pipeline developments in combination therapies enhance efficacy. Patient-centric programs improve therapy compliance.

The Breast Cancer segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by growing adoption of synthetic lethality-based therapies in BRCA-positive and triple-negative breast cancer. Hospitals and specialty clinics adopt PARP and ATR inhibitors in targeted regimens. Homecare programs support oral medication adherence. Clinical trials expand indications and validate combination strategies. Physician education programs increase early-stage therapy adoption. Telemedicine platforms facilitate follow-up and monitoring. Insurance coverage encourages patient access. Emerging markets show increasing uptake due to rising breast cancer prevalence. Patient support programs improve adherence. Multidisciplinary oncology teams optimize therapy. Pipeline innovations in next-generation inhibitors enhance outcomes. Combination therapies with immunotherapy or chemotherapy improve efficacy. Awareness campaigns and early detection programs support adoption.

Synthetic Lethality Drug Market Regional Analysis

- North America dominated the synthetic lethality drug market with the largest revenue share of 42.5% in 2025, driven by a robust pharmaceutical R&D infrastructure, early adoption of targeted therapies, and a high prevalence of oncology cases

- The market captured the largest share within North America, propelled by innovations from established pharmaceutical companies and biotech startups focusing on precision oncology and synthetic lethality strategies. Hospitals, specialty clinics, and research centers lead in adopting PARP, ATR, and CHK1 inhibitors. Early-stage cancer detection programs and precision medicine initiatives further drive uptake. Insurance coverage for targeted therapies enhances patient access

- Hospital pharmacies ensure continuous supply for inpatient and outpatient therapies. Awareness campaigns and clinical guidelines support physician adoption. Combination therapies with chemotherapy or immunotherapy strengthen clinical outcomes. Emerging homecare programs and outpatient monitoring are being integrated. Regulatory approvals in multiple regions promote market stability. Patient adherence initiatives boost therapy continuity. Continuous pipeline expansions maintain market momentum

U.S. Synthetic Lethality Drug Market Insight

The U.S. synthetic lethality drug market captured the largest revenue share within North America in 2025, reflecting strong adoption of targeted oncology therapies and advanced precision medicine initiatives. Hospitals, specialty clinics, and cancer research centers are the primary end-users, offering PARP inhibitors, ATR inhibitors, and CHK1 inhibitors for ovarian, breast, prostate, pancreatic, and lung cancers. The market growth is fueled by innovations from established pharmaceutical companies and biotech startups focusing on synthetic lethality strategies. Early-stage cancer detection programs and precision oncology initiatives drive higher adoption of targeted therapies. Insurance coverage and reimbursement policies enhance patient access to these high-cost drugs. Combination therapies with chemotherapy and immunotherapy are widely implemented to improve clinical outcomes. Specialty pharmacies and hospital pharmacies ensure continuous availability and controlled distribution, while adherence monitoring programs support treatment continuity.

Europe Synthetic Lethality Drug Market Insight

The Europe synthetic lethality drug market is projected to expand at a substantial CAGR from 2026 to 2033, fueled by increasing oncology research, stringent cancer treatment guidelines, and rising adoption of targeted therapies. Hospitals and specialty clinics across Germany, France, and the U.K. are implementing synthetic lethality drugs in ovarian, breast, and prostate cancers. Urbanization and enhanced healthcare infrastructure facilitate access. Government healthcare programs and insurance reimbursement policies further encourage adoption. Combination therapy protocols and precision oncology initiatives strengthen the clinical use. Patients increasingly prefer hospital-based and outpatient treatment for better adherence. Specialty pharmacies ensure controlled distribution of PARP and ATR inhibitors. Clinical trials and physician education programs improve awareness and utilization. Emerging biopharma innovations support drug availability. Multi-center research projects advance therapeutic indications. Evolving oncology guidelines promote adoption across different tumor types.

U.K. Synthetic Lethality Drug Market Insight

The U.K. synthetic lethality drug market is anticipated to grow at a noteworthy CAGR during 2026–2033, driven by increasing adoption of precision oncology therapies and growing awareness of synthetic lethality drugs for ovarian and breast cancer. Hospitals and specialty clinics are central to delivering these targeted therapies. The healthcare system emphasizes early detection and personalized treatment regimens. Patient access is supported through NHS programs and private insurance. Combination therapy protocols enhance efficacy and treatment compliance. Specialty pharmacies provide controlled distribution and adherence monitoring. Clinical trials continue to validate novel indications. Physician education ensures optimized therapy selection. Homecare and outpatient monitoring initiatives are increasingly adopted. Rising patient awareness and advocacy campaigns support treatment uptake.

Germany Synthetic Lethality Drug Market Insight

Germany’s synthetic lethality drug market is expected to expand at a considerable CAGR, driven by advanced oncology infrastructure, research-focused hospitals, and high patient awareness. Targeted therapies like PARP, ATR, and CHK1 inhibitors are widely adopted in specialized cancer centers. National guidelines and insurance coverage facilitate access. Hospitals lead in combination therapy administration with chemotherapy and immunotherapy. Specialty pharmacies ensure availability and controlled dispensing. Clinical trial activity fosters innovation and pipeline growth. Patients benefit from precision oncology approaches and adherence programs. The government encourages research initiatives supporting synthetic lethality therapies. Homecare integration for oral formulations is emerging. Strong healthcare infrastructure and technology adoption support long-term growth. Patient support programs improve therapy outcomes. Continuous R&D strengthens the market position.

Asia-Pacific Synthetic Lethality Drug Market Insight

The Asia-Pacific synthetic lethality drug market is expected to be the fastest growing region, accounting for 28.7% of the market share in 2025, driven by increasing healthcare infrastructure, rising cancer incidence, and expanding investments in oncology drug development. Countries like China, Japan, and India are witnessing rapid adoption of PARP inhibitors and other synthetic lethality drugs. Hospitals and specialty clinics are expanding access for targeted therapies. Outpatient and homecare treatment models are growing. Government initiatives support oncology drug approvals and public awareness. Clinical trials and biopharma investments drive innovation and adoption. Rising disposable incomes and urbanization improve access to advanced treatments. Combination therapies are increasingly implemented. Physician education programs facilitate early adoption. Specialty pharmacies manage distribution and patient adherence. Emerging domestic manufacturers increase drug availability. Telemedicine and digital health platforms support therapy compliance.

Japan Synthetic Lethality Drug Market Insight

Japan’s synthetic lethality drug market growth is driven by rapid urbanization, an aging population, and high-tech healthcare adoption, emphasizing precision oncology and patient convenience. Hospitals and specialty clinics lead in the administration of PARP and ATR inhibitors. Homecare and outpatient monitoring models support therapy adherence. Integration with clinical trial networks accelerates new drug uptake. Physicians follow strict guidelines for synthetic lethality therapy. Government-backed programs enhance access for high-risk oncology patients. Insurance coverage facilitates targeted therapy adoption. Combination therapy protocols improve treatment efficacy. Clinical research strengthens pipeline expansion. Specialty pharmacies ensure controlled drug dispensing. Patient education enhances compliance.

China Synthetic Lethality Drug Market Insight

China synthetic lethality drug market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by a growing middle class, rising cancer incidence, and government initiatives supporting precision oncology. Hospitals and specialty clinics are central to administering PARP, ATR, and CHK1 inhibitors. Rapid urbanization and increasing disposable incomes support market growth. Homecare and outpatient therapy programs are emerging. Local manufacturing improves affordability and accessibility. Telemedicine and digital health systems enhance patient adherence. Clinical trials validate emerging indications. Government policies promote oncology drug development. Specialty pharmacies maintain supply and controlled distribution. Combination therapies with immunotherapy or chemotherapy expand clinical use. Patient awareness campaigns support adoption. Pipeline innovations ensure long-term growth potential.

Synthetic Lethality Drug Market Share

The Synthetic Lethality Drug industry is primarily led by well-established companies, including:

• AstraZeneca (U.K.)

• Pfizer (U.S.)

• Merck & Co. (U.S.)

• Clovis Oncology (U.S.)

• GlaxoSmithKline (GSK) (U.K.)

• Bristol Myers Squibb (U.S.)

• Genentech (U.S.)

• Astellas Pharma (Japan)

• Bayer (Germany)

• BeiGene (China)

• Novartis (Switzerland)

• Johnson & Johnson (U.S.)

• Takeda Pharmaceutical (Japan)

• Roche (Switzerland)

• Seagen (U.S.)

Latest Developments in Global Synthetic Lethality Drug Market

- In April 2023, the fixed‑dose combination Niraparib/Abiraterone Acetate (brand name Akeega) — a PARP inhibitor plus hormone antagonist designed to exploit synthetic lethality in BRCA‑positive metastatic castration‑resistant prostate cancer — was approved for medical use in the European Union, expanding synthetic lethality–based therapies in oncology

- In August 2023, the U.S. Food and Drug Administration (FDA) approved Niraparib/Abiraterone Acetate plus Prednisone for treatment of BRCA‑mutated metastatic castration‑resistant prostate cancer, representing the first dual‑action oral synthetic lethality‑based therapy for this indication in the United States

- In October 2023, Talazoparib (Talzenna) received European Commission approval in combination with enzalutamide for homologous‑recombination repair (HRR)‑mutated metastatic castration‑resistant prostate cancer (mCRPC), further expanding the clinical use of synthetic lethality–based PARP inhibition beyond breast and ovarian cancers

- In November 2024, Tango Therapeutics reported positive clinical data from ongoing Phase 1/2 studies with Vopimetostat (TNG462) in patients with MTAP‑deleted cancers, reinforcing the promise of synthetic lethality approaches beyond PARP inhibition for targeting DNA repair vulnerabilities in difficult‑to‑treat tumors

- In March 2025, IDEAYA Biosciences, Inc. partnered with ATTMOS to accelerate an AI/ML‑enabled drug discovery platform that aims to identify and develop novel synthetic lethal therapies in oncology, reflecting a trend toward integrating advanced computational methods into precision oncology drug development

- In May 2025, DCx Biotherapeutics Corporation partnered with Repare Therapeutics Inc. with the goal of discovering synthetic lethality‑based drug candidates for cancer treatment, indicating increasing collaboration among biotech firms in this emerging market

- In August 2025, a synthetically lethal DNA‑damaging agent ‘STAR‑001’ was approved by the FDA, marking a new class of precision oncology therapeutics designed to exploit cancer cell vulnerabilities and expand the synthetic lethality portfolio beyond traditional PARP inhibitors

- In June 2025, the **European Medicines Agency (EMA) adopted a positive opinion recommending marketing authorization for the cancer drug Ogsiveo (nirogacestat) — initially approved in the U.S. for desmoid tumors — further expanding its regulatory acceptance and potential use in oncology applications with synthetic lethality implications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.