Global Synthetic Peptide Cdmo Market

Market Size in USD Billion

USD

2.48 Billion

USD

6.82 Billion

2025

2033

USD

2.48 Billion

USD

6.82 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.48 Billion | |

| USD 6.82 Billion | |

| % | |

|

Synthetic Peptide CDMO Market Overview

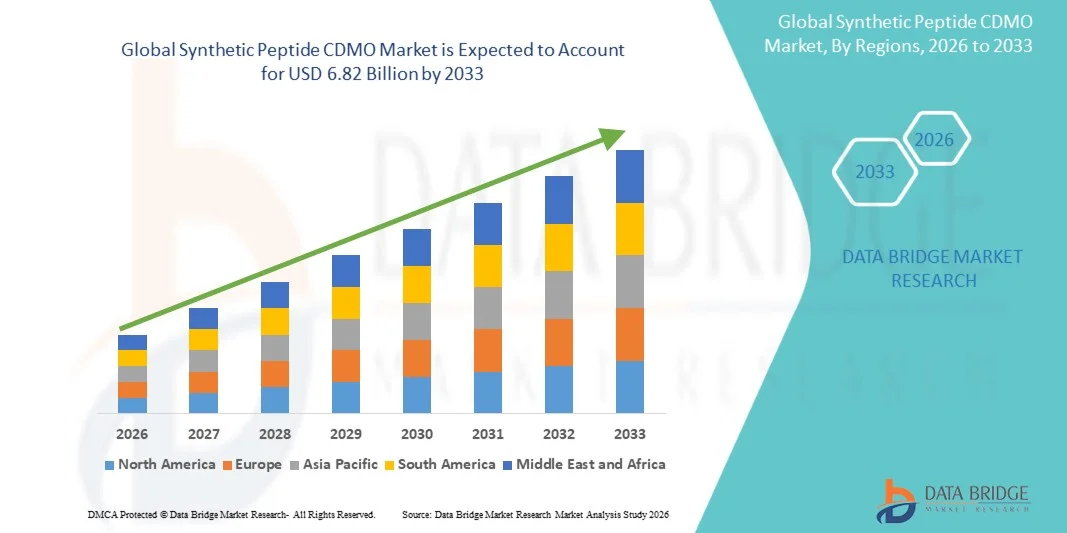

As per Data Bridge Market Research analysis, the synthetic peptide CDMO market was valued at USD 2.48 billion in 2025 and is projected to reach USD 6.82 billion by 2033, growing at a CAGR of 13.50% from 2026 to 2033. The market is experiencing consistent growth driven by increasing demand for peptide therapeutics, rising outsourcing of development and manufacturing activities by pharmaceutical and biopharmaceutical companies, and continuous advancements in peptide synthesis and manufacturing technologies.

The expanding clinical pipeline of peptide-based drugs for metabolic disorders, oncology, cardiovascular diseases, and rare diseases, coupled with the growing adoption of personalized medicine, is encouraging drug developers to partner with specialized CDMOs offering end-to-end development and commercial manufacturing capabilities. Furthermore, investments in automated solid-phase peptide synthesis, capacity expansion, and regulatory-compliant manufacturing facilities are enabling CDMOs to support increasingly complex peptide production while reducing development timelines and improving scalability.

Market Size & Forecast

- Global Market Value (2025): USD 2.48 Billion

- Expected Market Value (2033): USD 6.82 Billion

- Forecast CAGR (2026–2033): 13.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the synthetic peptide CDMO market with the largest revenue share of 36.9% in 2025, supported by a well-established pharmaceutical and biotechnology industry, strong R&D infrastructure, and significant investments in advanced manufacturing technologies

- The linear peptides segment led the market with a 42.8% share in 2025, driven by its widespread use in approved peptide therapeutics, research applications, and commercial manufacturing programs

- Asia-Pacific is expected to be the fastest-growing region, projected to register a CAGR of 14.2% from 2026 to 2033, fueled by expanding biopharmaceutical manufacturing capacity, increasing outsourcing activities, and growing investments in peptide production facilities across China, India, and South Korea

- Modified peptides are the fastest-growing peptide type, projected to register a CAGR of 15.8%, reflecting the surge in demand for peptides with enhanced stability, bioavailability, and therapeutic efficacy

- The peptide CDMO segment dominated the product category with a 66.7% revenue share in 2025, led by rapidly expanding commercial market for peptide therapeutics.

- Solid-phase peptide synthesis (SPPS) accounted for 72.4% of the market, preferred by its efficiency, scalability, and widespread adoption across commercial peptide manufacturing

- The oncology segment is the fastest-growing application category, with a CAGR of 15.4%, driven by increasing development of peptide-based cancer therapeutics and targeted drug delivery systems

Report Scope and Synthetic Peptide CDMO Market Segmentation

|

Attributes |

Synthetic Peptide CDMO Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Synthetic Peptide CDMO Market Trends

Trend: Rising Demand for GLP-1 and Next-Generation Peptide Therapeutics

The rapid commercialization of GLP-1 receptor agonists for obesity and diabetes, alongside an expanding pipeline of peptide therapeutics for oncology, rare diseases, and metabolic disorders, is significantly increasing demand for synthetic peptide CDMO services. Pharmaceutical and biotechnology companies are strengthening outsourcing partnerships to access advanced solid-phase peptide synthesis (SPPS), process development, analytical testing, and commercial-scale GMP manufacturing while accelerating product launches and ensuring supply reliability. For instance, in July 2024, CordenPharma announced a USD 1,031.8 million investment to expand peptide manufacturing capacity in the U.S. and Europe, targeting increasing global demand for GLP-1 peptides through new large-scale production facilities and integrated development capabilities.

The expanding adoption of GLP-1 and other peptide therapeutics is accelerating demand for specialized peptide development and manufacturing services worldwide.

Synthetic Peptide CDMO Market Dynamics

Key Market Driver: Increasing Outsourcing of Peptide Development and Commercial Manufacturing

The growing complexity of peptide therapeutics, stringent regulatory requirements, and the need for specialized synthesis technologies are driving pharmaceutical and biotechnology companies to outsource development and manufacturing to experienced CDMOs. Integrated providers offering process development, scale-up, analytical testing, and GMP manufacturing enable sponsors to reduce capital expenditure, accelerate clinical timelines, and efficiently support commercial production for innovative peptide drugs. For instance, in February 2025, Bachem announced major investments to expand peptide production capacity in Switzerland and the U.S., including large-scale SPPS reactors and automated manufacturing systems, to address rapidly growing global demand for peptide active pharmaceutical ingredients.

The increasing reliance on specialized CDMO partners is becoming a critical strategy for advancing peptide therapeutics from development through commercialization.

Key Restraint/Challenge: High Capital Requirements for Large-Scale Peptide Manufacturing Infrastructure

A major challenge in the synthetic peptide CDMO market is the substantial capital investment required to establish and expand GMP-compliant peptide manufacturing facilities equipped with advanced SPPS technology, purification systems, automation, and quality control capabilities. Long construction timelines, regulatory compliance requirements, and specialized production equipment increase financial barriers for new entrants and limit the industry's ability to rapidly address surging peptide demand. For instance, in March 2025, Bachem announced plans to invest more than USD 496 million during 2025 to expand its global peptide manufacturing network, including large-scale production facilities and advanced peptide manufacturing infrastructure, highlighting the significant financial commitment required to support commercial peptide production.

The high infrastructure and compliance costs continue to represent a significant barrier to entry and expansion within the synthetic peptide CDMO industry.

Key Market Opportunity: Expansion of High-Capacity Manufacturing for GLP-1 and Complex Peptide Therapies

The accelerating demand for GLP-1 therapies and other complex synthetic peptides presents substantial opportunities for CDMOs capable of providing integrated development, scale-up, and commercial manufacturing services. Investments in automated synthesis technologies, high-throughput purification, and global production networks are enabling manufacturers to support larger commercial volumes while improving operational efficiency and supply resilience. For instance, in April 2025, FUJIFILM Diosynth Biotechnologies signed a 10-year manufacturing agreement valued at more than USD 3 billion with Regeneron, highlighting the expanding commercial opportunities for CDMOs as pharmaceutical companies increasingly secure long-term outsourced manufacturing capacity for advanced therapeutics

The expansion of long-term manufacturing partnerships is creating significant growth opportunities for peptide CDMOs with scalable and specialized production capabilities.

Synthetic Peptide CDMO Market Scope

The synthetic peptide CDMO market is segmented on the basis of peptide type, product, synthesis technology, application, and end user.

- By Peptide Type

On the basis of peptide type, the synthetic peptide CDMO market is segmented into linear peptides, cyclic peptides, modified peptides, and long-chain peptides. The linear peptides segment dominated the market with an estimated 42.8% share in 2025, owing to its widespread use in approved peptide therapeutics, research applications, and commercial manufacturing programs. Linear peptides are comparatively easier to synthesize, purify, and scale up using established solid-phase peptide synthesis technologies. They are extensively utilized in metabolic disorder treatments, hormone replacement therapies, and cardiovascular disease management. The segment benefits from growing demand for GLP-1 receptor agonists and other peptide-based drugs. Pharmaceutical companies continue to prioritize linear peptide development because of their proven efficacy, manufacturing simplicity, and regulatory acceptance. Established production workflows and lower manufacturing complexity further support the segment's leadership position.

The modified peptides segment is projected to register the fastest growth at an estimated CAGR of 15.8% from 2026 to 2033, driven by increasing demand for peptides with enhanced stability, bioavailability, and therapeutic efficacy. Modified peptides provide improved pharmacokinetic profiles through PEGylation, lipidation, cyclization, and amino acid modifications. Growing development of long-acting peptide therapeutics for obesity, diabetes, and oncology is accelerating adoption. Pharmaceutical companies are increasingly investing in next-generation peptide drugs with extended half-lives and targeted delivery capabilities. Advances in peptide engineering technologies continue to expand development opportunities. Rising investments in innovative peptide pipelines are expected to further accelerate segment growth.

- By Product

On the basis of product, the synthetic peptide CDMO market is segmented into peptide CDMO, oligonucleotide CDMO, and others. The peptide CDMO segment dominated the market with a 66.7% revenue share in 2025, supported by the rapidly expanding commercial market for peptide therapeutics. Growing demand for GLP-1 drugs, peptide hormones, and oncology peptides has significantly increased outsourcing requirements. CDMOs provide specialized expertise in peptide synthesis, purification, analytical testing, and commercial-scale manufacturing. The segment benefits from a robust clinical pipeline and increasing regulatory approvals of peptide-based drugs. Pharmaceutical companies continue to rely on outsourcing partners to reduce development timelines and capital expenditures. Expanding manufacturing capacity investments by leading CDMOs further reinforce segment dominance.

The oligonucleotide CDMO segment is expected to witness the fastest growth at a CAGR of 15.1% from 2026 to 2033, driven by rising demand for RNA therapeutics, antisense oligonucleotides, gene-editing technologies, and precision medicine applications. Significant progress in genetic medicine is creating strong demand for specialized manufacturing services. Growing clinical development of siRNA, mRNA, and antisense therapies is further supporting expansion. CDMOs are investing heavily in advanced oligonucleotide production technologies and GMP-compliant facilities. Increasing regulatory approvals and commercialization activities are creating new outsourcing opportunities. The segment is also benefiting from substantial investments in nucleic acid-based drug development.

- By Synthesis Technology

On the basis of synthesis technology, the synthetic peptide CDMO market is segmented into solid-phase peptide synthesis (SPPS), liquid-phase peptide synthesis (LPPS), and hybrid synthesis. The solid-phase peptide synthesis (SPPS) segment dominated the market with an estimated 72.4% share in 2025, owing to its efficiency, scalability, and widespread adoption across commercial peptide manufacturing. SPPS enables rapid assembly of complex peptide sequences while maintaining high purity and reproducibility. The technology is extensively utilized for therapeutic peptide production and clinical-stage manufacturing. Continuous improvements in automation and process optimization are enhancing manufacturing productivity. Most large-scale peptide manufacturing facilities are built around SPPS platforms due to their proven commercial viability. Strong demand for high-volume peptide production continues to support segment leadership.

The hybrid synthesis segment is anticipated to register the fastest growth at an estimated CAGR of 14.9% from 2026 to 2033, driven by increasing production of long and structurally complex peptides. Hybrid approaches combine the advantages of SPPS and LPPS, improving manufacturing flexibility and cost efficiency. The technology is particularly useful for large-scale production of highly modified and difficult-to-synthesize peptides. Growing demand for next-generation peptide therapeutics is encouraging manufacturers to adopt hybrid synthesis strategies. Technological advancements are improving process yields and reducing manufacturing challenges. Rising investment in complex peptide development programs is expected to accelerate growth.

- By Application

On the basis of application, the synthetic peptide CDMO market is segmented into oncology, metabolic disorders, infectious diseases, cardiovascular diseases, gastrointestinal disorders, neurological disorders, and others. The metabolic disorders segment dominated the market with an estimated 38.6% share in 2025, due to the exceptional commercial success of peptide therapeutics used in obesity and diabetes treatment. Growing global prevalence of metabolic diseases continues to increase demand for GLP-1 receptor agonists and related peptide drugs. Pharmaceutical companies are investing heavily in expanding production capacity to address rising patient demand. The segment benefits from strong clinical outcomes and increasing physician adoption. Continuous innovation in long-acting peptide formulations is further supporting growth. Rising healthcare expenditure on chronic disease management strengthens the segment's market position.

The oncology segment is expected to be the fastest-growing application segment at an estimated CAGR of 15.4% from 2026 to 2033, driven by increasing development of peptide-based cancer therapeutics and targeted drug delivery systems. Peptides are gaining importance in precision medicine due to their high specificity and favorable safety profiles. Growing research activities in tumor-targeting peptides and peptide-drug conjugates are expanding market opportunities. Pharmaceutical companies are advancing numerous oncology peptide candidates through clinical development pipelines. Increasing cancer prevalence globally is creating strong demand for innovative treatment options. Continued investment in oncology research is expected to accelerate segment expansion.

- By End User

On the basis of end user, the synthetic peptide CDMO market is segmented into pharmaceutical companies, biopharmaceutical companies, academic & research institutes, and biotechnology companies. The pharmaceutical companies segment dominated the market with a 58.1% share in 2025, due to extensive outsourcing of peptide development and manufacturing activities. Large pharmaceutical organizations increasingly rely on CDMOs to access specialized expertise and advanced production infrastructure. Outsourcing helps reduce operational costs, accelerate development timelines, and improve manufacturing flexibility. Growing commercialization of peptide therapeutics is further increasing demand for external manufacturing support. Strong investments in metabolic disease, oncology, and rare disease pipelines continue to drive outsourcing activities. The segment remains the primary revenue contributor across the peptide CDMO industry.

The biotechnology companies segment is projected to witness the fastest growth at an estimated CAGR of 15.6% from 2026 to 2033, supported by a rapidly expanding pipeline of innovative peptide therapeutics. Many biotechnology firms operate with asset-light business models and depend heavily on CDMO partners for development and manufacturing services. Increasing venture capital funding and strategic collaborations are accelerating peptide drug innovation. These companies are focusing on next-generation peptide technologies targeting unmet medical needs. Growing clinical trial activity is creating significant outsourcing demand across development stages. The increasing number of emerging biotech companies entering the peptide therapeutics space is expected to sustain robust segment growth.

Synthetic Peptide CDMO Market Regional Analysis

North America dominated the synthetic peptide CDMO market with the largest revenue share of 36.9% in 2025, supported by a well-established pharmaceutical and biotechnology industry, strong R&D infrastructure, and significant investments in advanced manufacturing technologies. he region also benefits from strong investments in peptide therapeutics, increasing outsourcing of development and manufacturing activities, and a robust clinical pipeline targeting metabolic disorders, oncology, and rare diseases. Growing adoption of GLP-1 therapies, expansion of GMP-compliant production facilities, and continuous advancements in peptide synthesis technologies are accelerating market development. Increasing focus on supply chain resilience, commercial-scale manufacturing capacity, and accelerated drug development timelines continues to strengthen North America's leadership position in the global market.

U.S. Synthetic Peptide CDMO Market Insight

The U.S. synthetic peptide CDMO market is witnessing strong growth due to rising investments in peptide therapeutics, increasing outsourcing of drug development and manufacturing activities, and expanding demand for obesity and diabetes treatments. The country's mature biopharmaceutical ecosystem, extensive clinical research infrastructure, and strong presence of leading CDMOs are driving demand across commercial and clinical applications. In addition, growing emphasis on accelerating time-to-market and securing reliable manufacturing capacity is increasing outsourcing adoption among pharmaceutical companies. In July 2024, CordenPharma announced a 1,031.8 million investment to expand peptide manufacturing operations in the U.S. and Europe to address surging demand for GLP-1 peptide therapeutics.

Europe Synthetic Peptide CDMO Market Insight

The Europe synthetic peptide CDMO market remains a major contributor to global revenue, driven by strong pharmaceutical manufacturing capabilities, technological innovation, and increasing demand for peptide therapeutics. The widespread presence of specialized peptide manufacturers and contract development organizations is supporting market expansion across the region. Increasing investments in advanced peptide synthesis technologies, coupled with growing demand for GLP-1 drugs and personalized medicine, continue to strengthen market growth. In March 2025, Bachem announced plans to invest more than USD 496.25 million during 2025 to expand its global peptide manufacturing network, with a significant portion supporting European operations.

U.K. Synthetic Peptide CDMO Market Insight

The U.K. synthetic peptide CDMO market is experiencing steady growth, supported by rising adoption of outsourced drug development services, increasing biotechnology innovation, and growing investment in advanced therapeutics. Expanding research activities involving peptide-based drugs and strong collaboration between academic institutions and biopharmaceutical companies are contributing to market growth. Furthermore, increasing focus on precision medicine and complex biologic manufacturing is improving demand for specialized peptide development services. According to the U.K. Government's Bioscience and Health Technology Sector Statistics, the U.K. life sciences industry generated approximately USD 144,950 million in turnover, highlighting the country's strong foundation for advanced therapeutic development and contract manufacturing activities.

Germany Synthetic Peptide CDMO Market Insight

The Germany synthetic peptide CDMO market is expanding steadily due to the country's strong pharmaceutical manufacturing base, advanced research capabilities, and increasing adoption of next-generation peptide production technologies. Pharmaceutical companies, biotechnology firms, and research organizations are increasingly utilizing CDMO services for peptide development, scale-up, and commercial manufacturing activities. Continuous advancements in peptide synthesis, automation, and purification technologies, along with strong government support for pharmaceutical innovation, are further driving market growth. According to Germany Trade & Invest, Germany's pharmaceutical industry generated approximately USD 68,770 million in revenue in year 2023, reinforcing the country's position as Europe's largest pharmaceutical market and supporting demand for specialized drug development and contract manufacturing services

Asia-Pacific Synthetic Peptide CDMO Market Insight

The Asia-Pacific synthetic peptide CDMO market is expected to witness rapid growth, driven by expanding biopharmaceutical manufacturing capacity, increasing outsourcing activities, and rising investments in peptide production infrastructure across countries such as China, India, Japan, and South Korea. Growing demand for cost-effective manufacturing solutions, rising clinical research activity, and increasing adoption of advanced peptide synthesis technologies are supporting regional market expansion. In addition, the growing presence of global CDMO investments and favorable manufacturing economics are accelerating market development across the region. Bachem highlighted strong demand from Asia-based pharmaceutical and biotechnology customers as part of its global peptide manufacturing expansion strategy, underscoring the region's growing importance in peptide drug development and outsourcing activities.

Japan Synthetic Peptide CDMO Market Insight

The Japan synthetic peptide CDMO market is witnessing consistent growth due to rising investments in advanced therapeutics, increasing demand for peptide-based drugs, and strong pharmaceutical research capabilities. Pharmaceutical manufacturers and biotechnology companies are increasingly adopting specialized CDMO services for peptide development and GMP manufacturing. Moreover, increasing focus on innovative treatments for metabolic disorders, oncology, and rare diseases is further contributing to market growth. Japan remains one of the world's largest pharmaceutical markets, valued at more than USD 85 billion, creating significant demand for advanced contract manufacturing services.

China Synthetic Peptide CDMO Market Insight

The China synthetic peptide CDMO market is growing rapidly, driven by expanding biopharmaceutical production capacity, increasing government support for pharmaceutical innovation, and rising demand for peptide therapeutics. Growing adoption of advanced peptide synthesis technologies and increasing participation in global pharmaceutical supply chains are significantly boosting market demand. In addition, rising investments in contract manufacturing infrastructure, increasing clinical development activity, and rapid expansion of biotechnology companies are positioning China as one of the fastest-growing markets for peptide CDMO services globally. WuXi AppTec and other major Chinese CDMOs continue to expand peptide and oligonucleotide manufacturing capabilities to support growing international and domestic demand for advanced therapeutics.

Synthetic Peptide CDMO Market Share

The synthetic peptide CDMO industry is primarily led by well-established companies, including:

- Bachem Inc (Switzerland)

- PolyPeptide Group (Switzerland)

- CordenPharma (Switzerland)

- AmbioPharm, Inc. (U.S.)

- Lonza (Switzerland)

- AJINOMOTO CO.,INC (U.S.)

- Evonik (Germany)

- WuXi AppTec Co., Ltd. (China)

- Asymchem Inc (China)

- Curia Global, Inc. (U.S.)

- EUROAPI (France)

- CEM Corporation (U.S.)

- BOC Sciences (U.S.)

- Creative Peptides (U.S.)

- CPC Scientific Inc. (U.S.)

- GenScript (China)

- Biosynth (Switzerland)

- Aurigene Pharmaceutical Services Ltd. (India)

Latest Developments in Synthetic Peptide CDMO Market

- In February 2025, Bachem announced major investments to expand its global peptide manufacturing network in Switzerland and the U.S., including new large-scale solid-phase peptide synthesis (SPPS) reactors, expanded production infrastructure, and automation technologies to support rapidly increasing demand for GLP-1 and other peptide therapeutics. The expansion is designed to significantly increase manufacturing capacity and strengthen long-term supply for pharmaceutical customers worldwide, reinforcing Bachem's leadership in peptide CDMO services

- In December 2024, PolyPeptide Group announced the start of production at its new large-scale Solid-Phase Peptide Synthesis (SPPS) manufacturing facility in Braine-l'Alleud, Belgium. The new capacity supports commercial manufacturing under a long-term GLP-1 peptide supply agreement and incorporates advanced automation, proprietary manufacturing technologies, and sustainable production processes, significantly strengthening the company's peptide CDMO capabilities

- In September 2024, Ajinomoto Bio-Pharma Services became the first organization to join the Centre for Continuous Manufacturing and Advanced Crystallisation (CMAC) as a Translation to Industry Collaborator. The collaboration aims to accelerate innovation in crystallization, process analytical technology (PAT), continuous manufacturing, and digitalization, strengthening advanced pharmaceutical manufacturing capabilities and enhancing the company's CDMO services for complex therapeutics, including peptides

- In March 2023, Lonza completed a new cGMP clinical and commercial drug product manufacturing line at its Visp, Switzerland site. The expansion enhances manufacturing capacity for multiple therapeutic modalities and strengthens the company's end-to-end CDMO capabilities, enabling pharmaceutical and biotechnology customers to accelerate clinical development and commercial production of advanced therapeutics, including peptide-based medicines

- In July 2022, WuXi STA opened a new large-scale oligonucleotide and peptide manufacturing facility at its Changzhou campus in China. The expansion added multiple peptide production lines with reactors of up to 1,000 liters, significantly increasing the company's Solid-Phase Peptide Synthesis (SPPS) capacity and enhancing its ability to provide integrated development and commercial manufacturing services for peptide and oligonucleotide therapeutics worldwide

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.